Organoids and Organ-on-a-Chip in 2022: A Breakthrough Year That Was Inevitable

Xellar Biosystems

AI Drug Developer

The past year has been an unequivocal “Big Year” for the organoid and organ-on-a-chip industry.

Particularly since August 2022, the FDA has taken frequent actions: data from organ-on-a-chip technologies were used for the first time in FDA new drug applications; driven by the FDA, pharmaceutical companies, and biotech firms, the U.S. Congress, from the Senate to the House of Representatives, finally incorporated the non-mandatory nature of animal testing into legislation.

Amid several major moves by the FDA, market sentiment has been steadily rising.

One of the most direct manifestations was the publication of an article in Science on January 10, titled “FDA No Longer Requires Animal Testing Before Drug Clinical Trials.” Although the article merely interpreted the “FDA Modernization Act 2.0” issued in late December and did not disclose any actual progress, it did not dampen enthusiastic market sentiment. Seizing this opportunity, the substantial prospects of the “organoids and organ-on-a-chip” industry were once again widely discussed.

The industry’s response to this “Big Year” has been much more measured; while relevant companies are energized, they are not surprised. Those familiar with the field have long recognized that the FDA has been laying the groundwork for this transformation over the past several years.

VBInsight has interviewed more than 15 companies in the organoid and organ-on-a-chip sectors since October 2022, witnessing alongside the industry a year of rapid advancement in this field.

Excitingly, we have observed that some Chinese companies are not mere bystanders in this process, but active participants and even drivers.

Conferences within the industry have been held continuously, with those organized by domestic academic circles, industry players, and government agencies occurring more frequently than in any previous year. Some domestic startups have also begun to take the lead in organizing international conferences. The International Microphysiological Systems Society (iMPSS) was established, and the first World Microphysiological Systems (MPS) Summit was held in the United States. The second summit will return to Europe, the birthplace of organoids. With the adjustment and relaxation of epidemic prevention policies, some Chinese companies are planning to facilitate the holding of the third summit in China.

Moreover, the organoid and organ-on-a-chip industries continue to witness new financing activities. Following the publication of each of our reports on relevant companies, numerous investment institutions have reached out seeking engagement. Meanwhile, due to the interdisciplinary nature of this field, some investors who previously focused primarily on hard-tech sectors are now also looking to cover organoid and organ-on-a-chip companies.

We have also observed that companies specializing in organoids and organ-on-a-chip technologies are entering the “2.0 era” of technological development and application, pursuing high-throughput capabilities, standardization, automation, and integration with other technologies. Collaborations between startups and pharmaceutical companies, biotech firms in other fields, or government bodies and industry associations all spark considerable discussion and anticipation.

VCBeat: This article reviews the development and changes in the organoid and organ-on-a-chip industries over the past year. You are also welcome to reserve your spot in advance for our dedicated live broadcast on organoids and organ-on-a-chip technologies. Together with entrepreneurs and investors, we will capture industry signals from 2022 and look ahead to key highlights in 2023 (see event details at the end of this article).

FDA Sparks Industry Frenzy: Seemingly Sudden, Yet Inevitable

Why 2022 Can Be Regarded as a “Milestone” Year for the Organoid and Organ-on-a-Chip Industry: An Interpretation from Two PerspectivesOn one hand, the U.S. FDA, together with pharmaceutical companies and organ-on-a-chip firms, has advanced the clinical significance of organ-on-a-chip technologies and microphysiological systems to a new stage.

Phase I of U.S. organ-on-a-chip research, traceable to 2012, focused on developing the most basic chips, organoids, and cell cultures. Phase II, launched in 2015, integrated chips with cells and initiated drug-testing collaborations with 40 pharmaceutical companies, including GlaxoSmithKline. Phase III began in 2017, establishing various disease models for drug screening. As Phase III neared its conclusion in 2022, it coincided with the introduction of new FDA legislation and a series of milestone events:

In June, the U.S. House of Representatives passed the Food and Drug Amendments Act of 2022, incorporating organ-on-a-chip and microphysiological systems into the legislation as independent non-clinical drug testing evaluation frameworks.

In August, the FDA approved for the first time a new drug (NCT04658472) to enter clinical trials based entirely on preclinical efficacy data obtained from organ-on-a-chip studies. This study was conducted in collaboration between Sanofi and the organ-on-a-chip company Hesperos, aiming to treat two rare autoimmune demyelinating neurological diseases. Prior to this, it was not possible to evaluate the effects of potential therapies using animal models due to the lack of ideal animal models.

In September, the U.S. Senate unanimously passed the FDA Modernization Act 2.0, whose primary objective is to eliminate the mandatory requirement for animal testing in drug development. The legislation permits the use of alternative methods to assess the efficacy and safety of pharmaceuticals during research, development, and manufacturing, with microphysiological systems included among these alternatives.

In December, the U.S. House and Senate jointly passed the FDA Modernization Act 2.0, which was signed into law by President Biden as part of the Consolidated Appropriations Act. The legislation promotes diverse preclinical testing models, including organ-on-a-chip technologies, and commits to significantly reducing the use of dogs, primates, and other animals in laboratory testing.

Industry insiders have stated that the U.S. FDA and EPA (Environmental Protection Agency) have clearly outlined their roadmap to adopt organ-on-a-chip technology as a tool for drug evaluation and promote its inclusion in regulatory guidelines. Following Sanofi’s first collaborative application, future development is expected to accelerate. Moreover, from the perspectives of the United States, Europe, and Japan, the research, development, and application of organ-on-a-chip technology have become national strategies in various developed countries.

A series of favorable policies made 2022 the “Big Year” for organoids and organ-on-a-chip technologies.

Although industry insiders have rationally pointed out that animal testing has long been challenged, and its high cost indirectly drives up the cost of drug development, sometimes although animal data looks good, it is not necessarily useful. The FDA has long been committed to promoting the development and use of new technologies in drug research and development. The passage of the bill opens a window for the application of organoid and organ-on-a-chip technologies in the drug development process at the policy or legal level.

Xie Xin, Co-founder and CEO of Yaosu Technologystated: “In terms of regulatory policies and the level of public and capital attention, 2022 felt like a ‘peak year’ due to the approval of two FDA Investigational New Drug (IND) applications and legislative support from the FDA Modernization Act. However, the field of organ-on-a-chip has seen continuous innovation every year, with more models and drug testing data constantly refining and supporting the efficacy of organ-on-a-chip in preclinical testing. This culminated in the passage of the new FDA legislation, which may have appeared sudden but was, in fact, inevitable.”

Nevertheless, favorable policies can truly bring breakthroughs to the application of cutting-edge technologies. VCBeat New MedicineDr. Liu Dan, Senior Partner at CDH Innovation & Growth FundIn the interview, the interviewee pointed out: Looking at the present and the future, organoid technology and life science tools have ushered in a historic opportunity for development, with technological iteration and commercialization processes worthy of further exploration and attention.

The 2.0 Era of Domestic Companies

On the other hand, China has entered the 2.0 era of technological development and application in organoids and organ-on-a-chip.More companies are beginning to step out of the realm of academic research and engage in market competition, while investors are casting an eager eye on organoids and organ-on-a-chip technologies.

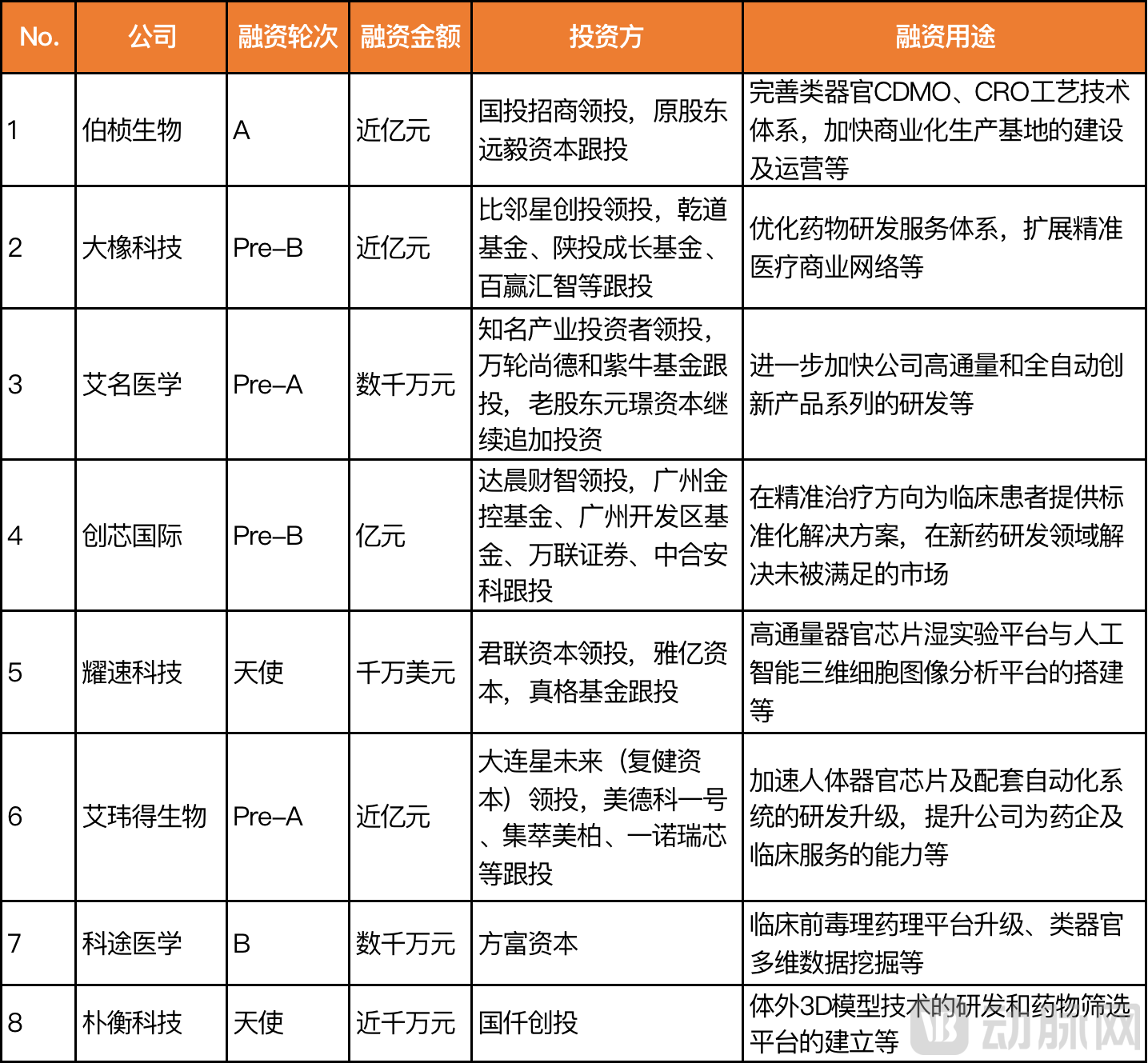

According to public data, there were eight financing events in China’s organoid and organ-on-a-chip sector over the past year. Financing activity intensified in the second half of the year, with rounds spanning from angel to Series B, and amounts ranging from tens of millions to hundreds of millions of yuan. Investors included corporate venture capital, financial investment institutions, and local government funds.

The biotechnology sector as a whole is still in its winter, and with a relatively small number of companies in the field, financing conditions are quite substantial. According to interviews conducted by VCBeat New Medicine, some companies are close to completing their financing or are preparing for a new round of fundraising.

The business activities of these financed companies are primarily concentrated in the organ-on-a-chip sector. Examples include Daxiang Technology, which has completed its Pre-B financing round and is among the earliest domestic companies to engage in the research and application of organ-on-a-chip technology; as well as Jiangsu Aiweide Biotechnology Co., Ltd. and Yaosu Technology, organ-on-a-chip companies established in the past two years with strong technical foundations and university-backed R&D capabilities.

From the perspective of financing purposes and the progress disclosed by companies over the past year, it is not difficult to observe that companies are emphasizing the advancement of automation and high-throughput technologies:

For instance, Puheng Technology has partnered with external companies to establish a high-throughput in vitro screening system for CAR-macrophage cells using the 3D NAC-Organ technology platform, aiming to accelerate the development of novel immune cell therapies for solid tumors.

Yaosu Technology leverages large-scale, high-throughput organ-on-a-chip systems to automatically generate three-dimensional, high-content cellular bioimages. Its participation in projects aimed at developing next-generation preclinical drug toxicity prediction tools involves conducting high-throughput drug testing on liver-on-a-chip platforms, thereby producing vast amounts of cellular image data that serve as a reference for joint standard-setting efforts with the FDA and pharmaceutical companies.

Similar to other fields, in the realm of organoids and organ-on-a-chip, AI and high-throughput technologies are primarily poised to address automatable manual tasks through more efficient means during future large-scale adoption and clinical application. Whereas high-throughput and automation efforts previously focused mainly on the organoid culture stage, the shift in 2022 has been characterized by a growing number of companies beginning to integrate big data at the application end.

In terms of applications, in addition to precision medicine and clinical services, many companies are expanding into the field of drug development:

For instance, Daxiang Technology targets the CGT sector by building a full-process R&D platform for CGT based on organ-on-a-chip technology. It provides drug development solutions across multiple areas, including target validation, toxicology and safety assessment, efficacy evaluation, and indication expansion, while collaborating with numerous CGT companies to advance the development of domestically originated CGT therapeutics in China.

For another example, the organ-on-a-chip platforms and systems developed by Aiweide Biotechnology have been tested and adopted by several leading Chinese pharmaceutical companies, including Hengrui Medicine, Chia Tai Tianqing Pharmaceutical, Simcere Pharmaceutical, and Qilu Pharmaceutical. Additionally, an organ-on-a-chip-based efficacy evaluation for a drug candidate conducted in collaboration with a major pharmaceutical company has been submitted as part of a Pre-IND application.

The B2B sector represents a steeper growth curve for organoids and organ-on-a-chip technologies, a view that has gained broad consensus among industry professionals. Although functional metrics for the application of organ-on-a-chip technology in pharmaceutical R&D pipelines have not yet received regulatory or official certification, certain de facto industry standards have already emerged. Historically, it was primarily foreign pharmaceutical giants that actively sought out new technologies. However, according to VCBeat New Medicine’s 2022 visits to organ-on-a-chip companies, domestic pharmaceutical firms are also gradually embracing organoid and organ-on-a-chip technologies. They are collaborating with companies in this field to achieve tangible results, thereby driving policy advancements from the ground up.

Regarding the technological and application iterations in the fields of organoids and organ-on-a-chip, Dr. Chen Zaocao, CTO of Jiangsu Aiweide Biotechnology Co., Ltd., stated: “Technologies such as organoid culture, microfabrication, biomaterials, as well as AI-based recognition and automation systems, are advancing every day. The integration of these technologies will yield more mature assay solutions and more accurate results. Importantly, technological development is embedded within the expansion of applications; the domains where these integrated technologies are applied will be novel, thereby giving rise to new outcomes.”

Organoids and Organ-on-a-Chip Will Continue to Prove Their Worth

The rapid advancements in organoids and organ-on-a-chip technologies over the past year are also reflected in the progress toward standardization and guideline development. In 2022, the US-based International Microphysiological Systems Society (iMPSS) was established to develop standards for organ-on-a-chip technologies and has been continuously integrating organ-on-a-chip consortia from other regions, including Europe and Japan, to promote industry-wide standardization.

China is also formulating various standards for organoid models and organ-on-a-chip technologies. Last July, the Expert Consensus on the Clinical Application of Organoid Drug Sensitivity Testing in Guiding Precision Oncology Therapy was jointly released by the Tumor Marker Professional Committee of the China Anti-Cancer Association. In September, driven by the China Stem Cell Standardization Committee and Academician Chen Yeguang, dozens of domestic institutions, including Danwang Medical, collaboratively developed China’s first intestinal organoid standards—the group standards Human Intestinal Cancer Organoids and Human Intestinal Organoids. Additionally, the draft national standard General Technical Requirements for Skin-on-a-Chip, led by Professor Gu Zhongze’s team at Southeast University, has been approved for project establishment and publicly notified. The monograph Non-clinical Evaluation of CGT Products, led by Wang Qingli, Director of the Pharmacology and Toxicology Department at the Center for Drug Evaluation of the National Medical Products Administration, and Professor Wang Quanjun, has initiated the project launch meeting for its second edition, incorporating organ-on-a-chip as a standalone chapter within the newly added in vitro evaluation system.

It is important to note that the development of organoid and organ-on-a-chip technologies should not be viewed in isolation from the broader context of the biopharmaceutical industry. The COVID-19 pandemic did not actively garner attention for the biopharmaceutical sector; rather, amid the global ravages of the virus, it passively became the focal point of worldwide attention.

The impact of the pandemic is “long-lasting.” In the face of continuously emerging new variants and infection patterns, people are placing their hopes on innovations and breakthroughs at the genetic and cellular repair levels, as well as in drug development. They are also concerned about the types of damage caused by different variants and whether early detection is possible.

As models capable of recapitulating physiological complexity and relevance, organoids and organ-on-a-chip systems can facilitate injury monitoring, hazard assessment, and drug screening and evaluation.

For example, last December, researchers at the University of Cambridge used organoid models to discover that the drug ursodeoxycholic acid (UDCA) can reduce FXR signaling and downregulate ACE2 in human lung, cholangiocyte, and intestinal organoids. This suggests its potential to prevent future novel variants of viruses as well as other emerging coronaviruses. This finding paves the way for future clinical trials.

In China, Jiangsu Aiweide Biotechnology Co., Ltd. has also partnered with Zhongda Hospital of Southeast University and the Jiangsu Provincial Center for Disease Control and Prevention to conduct research related to the novel coronavirus using organ-on-a-chip technology. This includes employing organ chips to assess SARS-CoV-2 infection and transmission in the lungs, as well as viral-induced vascular damage and associated coagulation responses.

Following the publication of the article in Science, a new wave of discussion has emerged regarding organoid and organ-on-a-chip technologies. On one hand, animal testing regulations in the United States are set to become more stringent; on the other, innovative drug development now has more alternatives, shifting from “animal use is mandatory for preclinical evaluation” to “animal use is not mandatory for preclinical assessment.”

Wang Haotian, Vice President of Investment at Legend Capital, believes that non-animal technologies should be viewed rationally, as they are still in their early stages and continue to rely on traditional methods to advance non-clinical research. Furthermore, the industry is actively embracing innovation, with the hope of better validating the reliability of non-animal technologies through clinical and animal data in the future.

Some investment firms are strategically positioning themselves in the life sciences tools sector by investing in both organoid and organ-on-a-chip technologies, as well as companies related to animal testing. Their goal is to eventually leverage these new technologies to effectively supplement, optimize, and upgrade the existing system, thereby accelerating drug development more efficiently.

As stated in *Science*, it will take “many, many years” for non-animal technologies to replace animal testing. Nevertheless, this year will remain a pivotal one within that extended timeline. Beyond standardization, scaling, and the integration of upstream and downstream resources, organoid and organ-on-a-chip technologies will continue to advance toward multi-organ chip interconnectivity and further integration into pharmaceutical companies’ drug development pipelines.

The other side of the pandemic is a golden opportunity for the upgrading of the modern pharmaceutical industry, and also an opportunity for frontier technologies such as organoids and organ-on-a-chip to prove their value and importance.

Industry insiders remain optimistic about the financing landscape for domestic organoid and organ-on-a-chip companies in 2023. Meanwhile, driven by policy guidance and the precedent set by the collaboration between Sanofi and Hesperos, partnerships between organoid/organ-on-a-chip firms and pharmaceutical companies are expected to become more flexible and expansive. Such collaborations are likely to be a major highlight of the industry this year.

VCBeat New Medicine 2022 "Organoids and Organ-on-a-Chip"Special Topic」Industry Insights and Interview Reports

1.After Reviewing 25+ Organoid Companies, We Compiled a Comprehensive Landscape Analysis