China's Pet Healthcare Giant New RuiPeng Files for Nasdaq IPO Amid Soaring Losses

During the Spring Festival, a piece of news flooded the WeChat Moments of numerous venture capital and private equity professionals.

As China’s largest pet healthcare platform, New Ruipeng Pet Healthcare Group Co., Ltd. (hereinafter referred to as “New Ruipeng”), valued at RMB 30 billion, has officially filed its prospectus with the U.S. Securities and Exchange Commission (SEC) in preparation for an initial public offering (IPO) on the Nasdaq Stock Market. If the IPO is successful, New Ruipeng will become the first publicly listed pet healthcare institution in China.

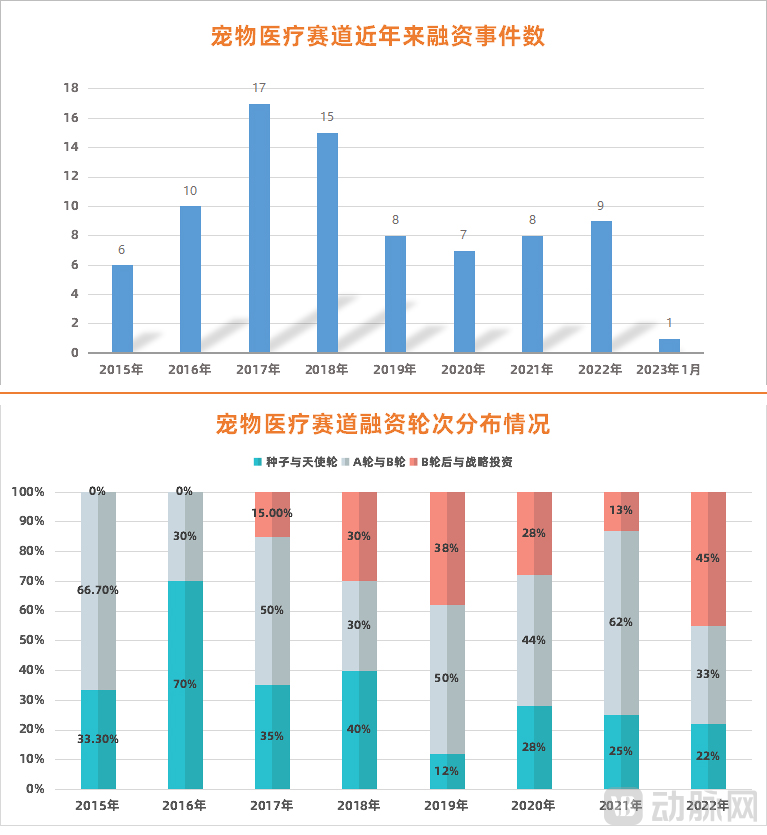

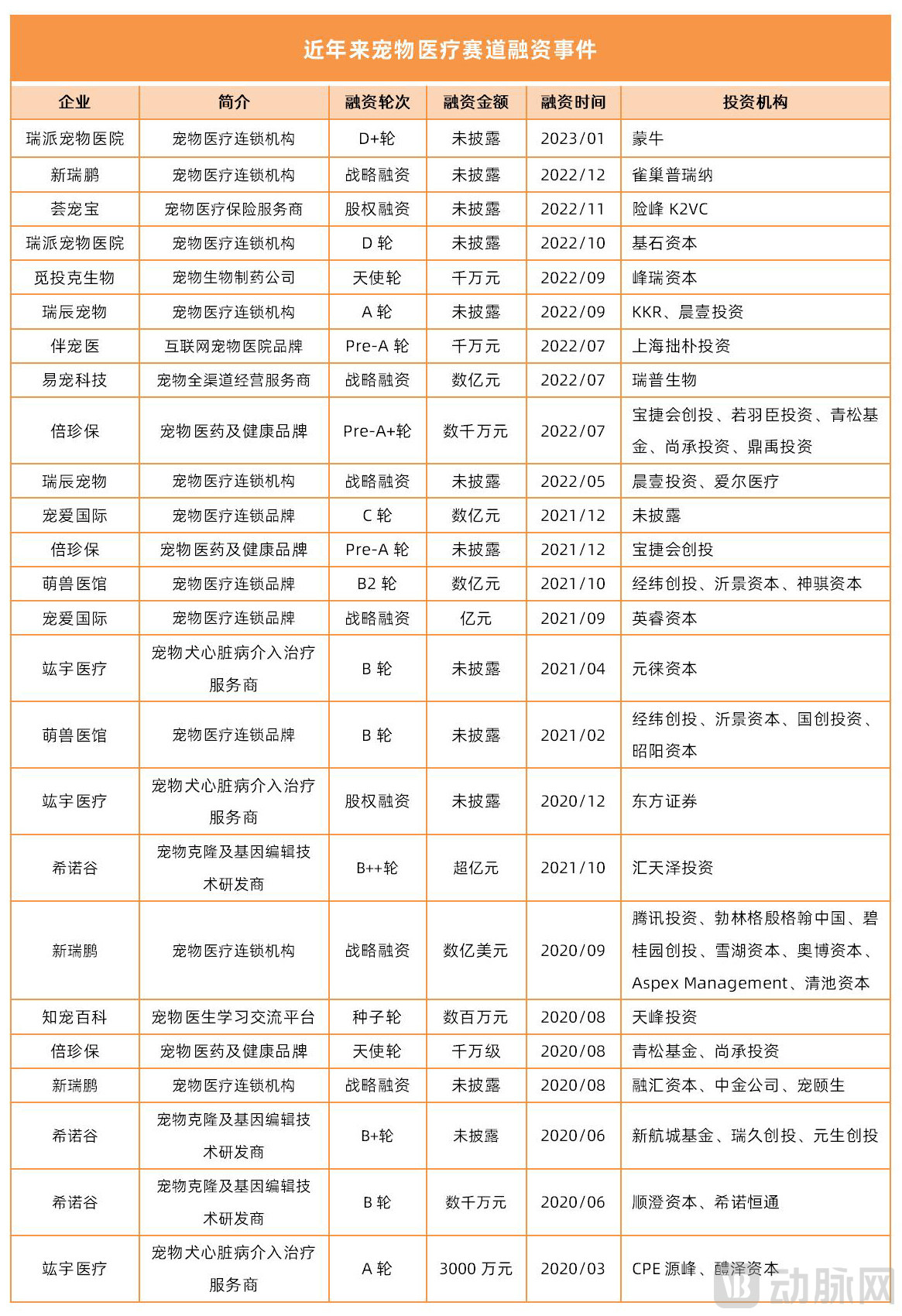

It is worth noting that since Hillhouse Capital made a significant investment in the pet market, which had received little attention from institutions, in 2014, the pet healthcare sector has entered a period of rapid development, with numerous VC/PE firms actively investing:Amidst a frenzy of massive capital inflows, the pet healthcare sector has exploded in popularity.According to statistics from the Artery Orange database, a total of 81 financing events occurred in China’s pet healthcare sector from 2015 to January 31, 2023, attracting over RMB 10 billion in investment.

(Pet Healthcare Financing Trends in Recent Years, Chart by VCBeat)

Although the number of financing events in the pet healthcare sector has shown an overall downward trend since 2019, the proportion of early-stage deals has gradually decreased, with funding stages shifting toward later rounds. In other words,As leading players in the sector enter their later stages of development, the pet healthcare industry is maturing and reaching a critical juncture for growth.

New Ruipeng’s IPO push is a representative moment of this juncture.

Prior to this IPO filing, New Ruipeng attracted significant investments from numerous prominent investors.

In addition to early-stage investors such as Fortune Capital and Hillhouse, the roster includes institutions and industry giants from both domestic and international sectors, including Tencent, Country Garden, Boehringer Ingelheim, Nestlé, CICC, Snow Lake Capital, Clear Pool Capital, and Housheng Investment.

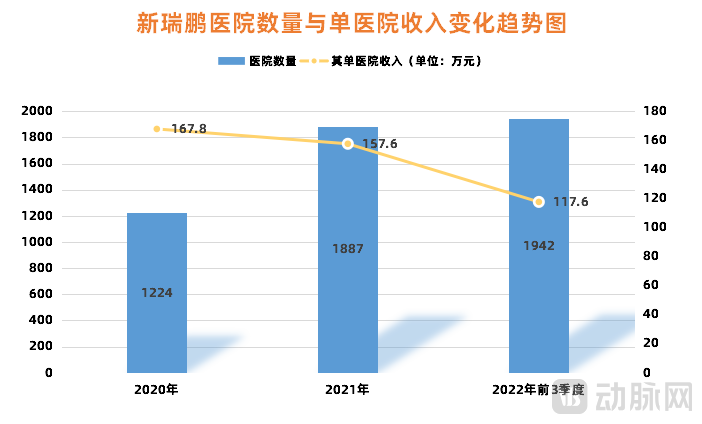

Benefiting from substantial capital support, New Ruipeng has grown into China’s largest and the world’s second-largest pet healthcare service platform (according to Frost & Sullivan data). As of September 30, 2022, New Ruipeng operated 1,942 pet hospitals across 114 cities in China, a figure significantly higher than that of any other domestic competitor.

“The pet industry is a classic sector ‘fueled’ by capital, with an influx of massive funds accelerating its development over the past five to six years.” Li Linglin (pseudonym), a Vice President at an investment firm who previously participated in due diligence for multiple pet healthcare companies, told VCBeat. Around 2017, companies represented by New Ruipeng attracted numerous VC/PE firms, and subsequentlyFrom Niche to Broad: The Pet Healthcare Sector Blossoms Across the Board, with Numerous Innovative Companies Emerging in Segments Ranging from Medical Service Providers and New Therapies to Pet Insurance and Veterinary Education—Some Securing Tens of Millions or Even Hundreds of Millions in Funding.

In the view of investor Li Linglin, there are two main reasons for the surge of capital.First, experience from developed markets indicates that pet consumption is resilient to economic downturns and can even exhibit “counter-cyclical growth.” Second, the pet healthcare sector represents a blue-ocean market with low penetration rates, offering substantial growth potential.“Demand for pet ownership continues to be unleashed, and demand for veterinary medical services will increase significantly.”

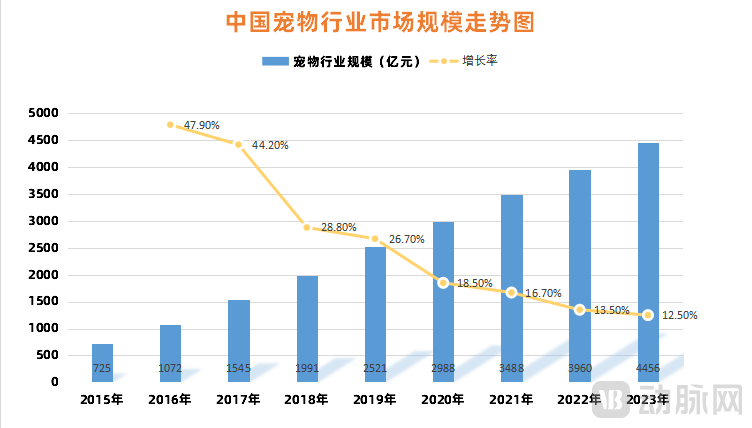

According to data from the "2021 White Paper on China's Pet Industry," the number of urban pet (cat and dog) owners in China reached 68.44 million in 2021, an increase of 8.7% compared to 2020. In terms of market size, the overall pet market grew by 13.5% from 2021 to 2022, reaching RMB 396 billion.

(Data source: 2021 China Pet Industry White Paper; graphic by VCBeat)

In this process, traditional basic healthcare services, such as vaccinations and deworming, have gradually failed to meet pet owners’ higher-level demands for their pets’ health; therefore,Specialized, multidimensional veterinary medical services have become the prevailing trend in industry development.This is also the underlying logic behind the recent concentration of capital in chain veterinary medical services and upstream novel therapies.

“An increasing number of pet owners regard their pets as their ‘children,’ and this emotional projection makes them ‘willing to spend money and bold in their spending,’” said investor Li Linglin.

Amid robust demand, capital has been heavily invested and companies have flocked to enter the market, making China’s pet healthcare sector a hotbed of rapid growth.

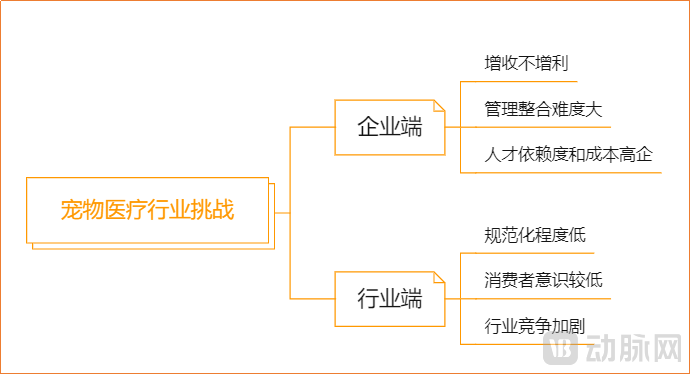

Accelerated IPOs and Financing, Yet Challenges in the Pet Healthcare Sector Remain Formidable.

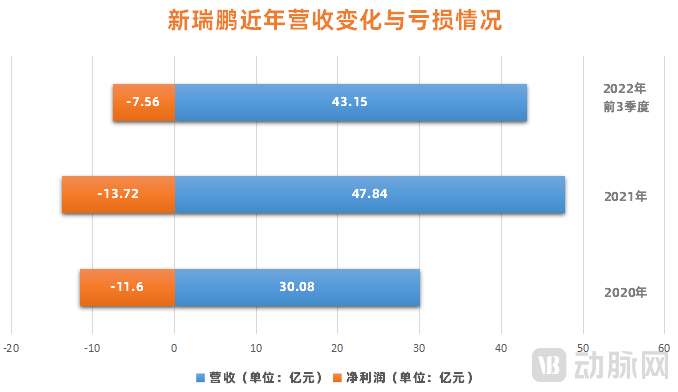

On one hand, behind the market’s rapid growth, the profit growth of pet healthcare-related institutions remains less than optimistic.Taking New Ruipeng, which recently went public, as an example, it ranks first in the industry in terms of the number of hospitals and service volume, yet it remains unprofitable, with its profitability challenges yet to be resolved.

According to the performance data disclosed in the prospectus, New Ruipeng’s revenues from 2020 to the first three quarters of 2022 were RMB 3.008 billion, RMB 4.784 billion, and RMB 4.315 billion, respectively; its net profits were -RMB 1.16 billion, -RMB 1.372 billion, and -RMB 756 million, respectively, resulting in cumulative losses of approximately RMB 3 billion over the three-year period.

(Data source: Prospectus; Graphic by VCBeat)

If industry leaders are struggling, small and fragmented pet healthcare institutions are facing even greater difficulties. According to Tencent News, China had 23,000 pet hospitals in 2022, a decrease of 7,448 from the previous year, with many hospitals hovering on the brink of profitability or already operating at a loss.

What has led to this situation? To understand this, we must examine New Ruipeng’s revenue structure. The prospectus reveals that New Ruipeng operates three major business segments: pet medical services, supply chain services (pet trading and logistics), and local lifestyle services. Among these, pet medical services constitute the core business driving its revenue.

Specifically, pet healthcare services encompass 15 specialized veterinary disciplines, including radiology, ophthalmology, orthopedics, and internal medicine. This business segment has demonstrated steady growth, with revenue increasing from RMB 2.054 billion in 2020 to RMB 2.974 billion in 2021, and rising from RMB 2.147 billion in the first three quarters of 2021 to RMB 2.284 billion in the same period of 2022.

An analysis of the prospectus reveals that the growth in pet medical services is primarily driven by expansion in scale, specifically through a continuous increase in the number of veterinary hospitals: in the first three quarters of 2022, New Ruipeng operated 1,942 hospitals, representing a year-on-year increase of 7.2%.

However, at the same time,However, the business has fallen into the trap of “scale without economies of scale.”

In theory, similar to the retail industry, as the number of stores/hospitals increases, economies of scale should help enterprises reduce average costs in areas such as procurement, training, and marketing. However, New Ruipeng has experienced a declining trend in revenue per hospital. From 2020 to the first three quarters of 2022, its revenue per hospital was RMB 1.678 million, RMB 1.576 million, and RMB 1.176 million, respectively, showing a continuous decline.

(Data source: Prospectus; Chart by VCBeat)

(Data source: Prospectus; Chart by VCBeat)

This is because M&A integration strategies have made managerial integration extremely challenging: the pet medical service sector is currently characterized by a wide variety of non-standardized offerings, leading to declining labor productivity during business expansion. From 2015 to 2021, New Ruipeng’s revenue per employee decreased by 12%.

Moreover, the pet healthcare industry is highly labor-dependent, with human capital serving as a core market resource. However, the sector has long faced a shortage of specialized and managerial veterinary professionals. This stems from two main factors: first, there is a limited pool of graduates from veterinary-related programs who enter the pet healthcare field each year; second, most managers in the industry are clinicians who possess strong technical expertise but lack management experience.

To retain talent, veterinary medical institutions need to increase salary and benefit levels. Based on New Ruipeng’s prospectus and Ruipeng’s previous financial reports (prior to its merger with Hillhouse),The sharp rise in labor costs is the primary reason for the decline in its gross profit margin, thereby diluting profits.: From 2015 to 2022, New Ruipeng's labor cost ratio rapidly increased from 22% to 52%.

On the other hand, despite the accelerated development of the pet healthcare industry, its marketization and standardization remain at a relatively low level.As previously mentioned, China’s pet healthcare industry started relatively late, with regulatory frameworks such as the “Administrative Measures for Animal Diagnosis and Treatment Institutions” only being established around 2008, leading to uneven implementation of industry standards.

Specifically, in the core areas of first- and second-tier cities such as Beijing, Shanghai, and Shenzhen, where competition in the pet healthcare market is relatively intense, government oversight and industry self-regulation are comparatively robust. However, in third- and fourth-tier cities, as well as in non-core areas of first- and second-tier cities, misconduct occasionally occurs, including unlicensed pet stores illegally providing medical services, and pet hospitals engaging in excessive marketing and arbitrary charging. These practices undermine the overall image of the industry and erode consumer trust.

Moreover, in terms of consumer awareness, as the pet consumption market has emerged only recently, pet owners’ overall understanding and perception of their pets’ needs remain to be improved.

This is reflected in consumer behavior, where pet-related expenditures are primarily concentrated on pet food, while less attention is paid to pets’ emotional and medical needs. Consequently, when pets fall ill, many owners fail to seek timely veterinary care, which further suppresses the already infrequent demand for pet healthcare services and thereby hinders the development of the pet medical industry.

Furthermore, the rapid increase in the number of hospitals has intensified competition and driven up customer acquisition costs, prompting institutions to engage in fierce price wars. Compounding this issue, the rising costs of medical equipment and pharmaceuticals required for veterinary care have trapped pet hospitals in a vicious cycle of squeezed profit margins and increasingly difficult survival.

(Graphic by VCBeat)

Therefore,How to navigate the aforementioned pitfalls and enhance the profit potential of the pet healthcare sector has become a key area of exploration for industry entrants in the next phase.

With New Ruipeng’s IPO as a turning point, the pet healthcare industry has begun to advance toward maturity, and new opportunities are emerging.

To this end, VCBeat has mapped the upstream and downstream segments of the pet healthcare industry’s value chain and, incorporating insights from investors, identifies the following micro-trends as likely directions for the next five to ten years.

First, the industrial chain of the pet healthcare industry can be divided into upstream pharmaceutical and medical device suppliers, midstream service providers, and downstream payers.

(Pet Healthcare Industry Chain, Chart by VCBeat)

(Pet Healthcare Industry Chain, Chart by VCBeat)

On the upstream end, China’s R&D capabilities in pet pharmaceuticals and medical devices remain relatively weak, with a low market share, presenting an opportunity for market entry.

For instance, in the pharmaceutical segment, imported brands currently hold nearly 70% of the domestic pet drug market. Due to the high prices and substantial profit margins of imported drugs, many companies have resorted to illegally producing substandard products, resulting in a market flooded with various counterfeit and inferior goods.

To alleviate the clinical supply-demand imbalance in veterinary medicines for pets, the Ministry of Agriculture and Rural Affairs is accelerating the registration process for veterinary drugs intended for pet use, issuing Announcement No. 330, which includes the "Requirements for Registration Materials for the Conversion of Human Chemical Drugs to Pet Chemical Drugs." Domestic pharmaceutical companies are actively following suit and entering the pet healthcare market.

As of now, pharmaceutical companies such as Sinopharm Animal Health, Livzon Animal Health, Kangchen Pharmaceutical, and Kanghua Biologics have announced their strategic initiatives in the pet medicine sector (including pet vaccines).

In the midstream segment, measures or enterprises that help pet healthcare service providers improve quality and efficiency, as well as address diseconomies of scale, will have considerable growth potential.

Opportunities Lie Behind Challenges. Industry players are currently actively building digital systems and physician training programs to address the aforementioned challenges. Taking New Ruipeng as an example, it has developed services such as continuing education for veterinarians and industry-level enterprise solutions.

According to Frost & Sullivan, New Ruipeng operates the largest veterinary talent development platform in the industry. As of September 30, 2022, New Ruipeng had 726 local instructors, 300 international instructors, and approximately 131,000 trainees.

In terms of its supply chain, New Ruipeng has maintained continuous investment. As of September 30, 2022, leveraging seven regional distribution centers, 58 provincial and municipal warehouses, and 50 trading subsidiaries, New Ruipeng had established a nationwide supply chain service network covering more than 100 major cities across China, providing services to over 45,000 pet stores, hospitals, clinics, and other facilities throughout the country.

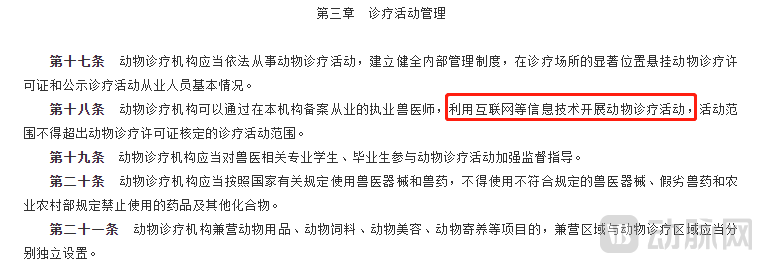

In addition to the establishment of offline service systems, internet-based pet healthcare service platforms and enterprises providing digitalization solutions for pet healthcare providers are entering a window of opportunity. In September 2022, the newly revised Administrative Measures for Animal Diagnosis and Treatment Institutions were released, stipulating that animal diagnosis and treatment institutions may conduct veterinary diagnostic and therapeutic activities via the internet and other information technologies through licensed veterinarians registered with their respective institutions. This development will further promote the growth of online pet healthcare services and, to some extent, alleviate the problem of resource misallocation.

(Image source: official website of the State Council)

On the downstream end, in addition to pet owners as the paying party, pet finance (including installment plans for veterinary care and pet health insurance) has also emerged as a minor trend in recent years.

This is because, unlike food and daily necessities, pet healthcare is characterized by low frequency and high cost per visit, which aligns well with the risk-transfer function of insurance products.

Currently, tech giants and financial institutions such as Tencent, Ant Group, Ping An, and Taikang have entered this sector, each adopting slightly different approaches. Taking Ant Group as an example, to address the challenge of identifying pet identities, the Alipay Insurance Platform has introduced nasal print recognition technology for pets. In collaboration with Dadi Insurance and ZhongAn Insurance, this technology was applied to pet insurance for the first time. This pet insurance product covers two major categories: cats and dogs. During enrollment, the Alipay Insurance Platform creates a unique electronic profile for each pet based on its nasal print information. When filing a claim, users can complete the process with a single click by verifying the pet’s identity through a nasal print scan.

However, compared with traditional financial services, the pet finance market remains niche, resulting in limited insurance products and a restricted network of partner hospitals. How to aggregate more resources to deliver a better user experience and enhance market education has become the key focus for the pet medical insurance sector moving forward.

In summary, the pet healthcare industry still offers numerous opportunities, with considerable potential for future growth.Based on the mature development experience of the U.S. pet healthcare market, the pet healthcare sector is bound to see industry leaders with market capitalizations reaching tens of billions, or even hundreds of billions, in the areas of pharmaceutical and medical device R&D, medical services, and payment solutions.

Although the landscape of the pet healthcare services segment is taking shape, significant uncertainties remain. For leading pet hospital groups, it is still difficult to predict how they will expand in the future and to what extent they can achieve integration.

In other sectors such as pet pharmaceuticals and pet insurance, new entrants and capital will continue to enter the market. Whether these stakeholders can fundamentally address challenges like the scarcity of professional talent in veterinary care and the need for market education will test their collective ingenuity.

Of course, to capitalize on the “cute pet” dividend, the trailblazers making waves in the veterinary healthcare sector need not only financial and talent support but also ample perseverance and patience.