Clinic Founders Focus on Strategic Planning as Sector Enters Full Recovery

Over the past few months, primary healthcare institutions—particularly clinics and outpatient departments specializing in general practice and pediatrics—have experienced a “rollercoaster” ride: from being nearly deserted or even closed during the containment period, to being overwhelmed at the peak of infections, and finally returning to normalcy after the Spring Festival. Of course, this new normal carries a more optimistic significance.

After the peak patient intake subsided and operations returned to normal, the clinic founders became busy with business trips, designing new services, and holding long-term strategic discussions.

The clinic, which had been dormant for several years, is now experiencing a revival.

According to data released by the National Health Commission, the number of visits to fever clinics across China peaked at 2.867 million on December 23, 2022, and has since continued to decline, falling to 477,000 by January 12, 2023—a decrease of 83.3% from the peak. During this period, a total of 16,400 fever clinics were established in medical institutions at or above the secondary level nationwide, while 43,100 fever clinics or fever consultation rooms were set up in primary healthcare institutions.

It is evident that during the peak of COVID-19 infections, when some hospitals were nearly entirely converted to respiratory care units, primary healthcare institutions played a crucial role. This included socially operated primary care facilities such as clinics and outpatient departments.

Guangrui Medical, headquartered in Anhui Province, rapidly stockpiled a batch of antipyretics before the formal implementation of the “Ten New Measures.” During the peak infection period, its clinics distributed 300,000 antipyretic tablets to patients free of charge. In Chengdu, four clinics under Xiezhuo Medical recorded 800 patient visits in a single day. A several-fold increase in consultation volume during the peak period was a common phenomenon among clinics across various regions.

Although no one wishes to see such a large-scale surge in patient numbers, it must be acknowledged that the sharp increase in clinical volume has, to some extent, offset the clinic’s losses over the past three years.

After the peak subsided, clinics rolled out various COVID-19 testing and rehabilitation programs to treat “razor throat” and alleviate symptoms of “long COVID,” seizing this opportunity tightly.

Nevertheless, responding to this wave of infection is merely a short-term endeavor. It is more worthy of attention and deep reflection to consider how to leverage the insights and operational capabilities accumulated over the past three years to formulate longer-term strategies.

“For the past three years, we have been in a deep freeze. The uncertainty was so great that anxiety and confusion were constant,” lamented a clinic founder, reflecting the prevailing sentiment across the industry at the time.

"Finding certainty amidst uncertainty has been the core competency cultivated by the clinic’s founders over the past three years; this has enabled the industry to undergo a period of trial and consolidation in the last three years, laying the groundwork for a more composed response to future infection peaks."

Historically, the core business of general practice and pediatric clinics primarily focused on common conditions, particularly respiratory diseases. During the three-year pandemic period, these services suffered significant setbacks due to restrictions on treating patients presenting with the "ten major symptoms" associated with COVID-19.

“After the outbreak, at the peak of the crisis, the volume of services for common diseases dropped to less than 10% of its original level,” recalled Luo Lin, founder of Linjia Haoyi.

How to Bridge the Remaining 90%? The company has decided to pursue related diversification based on its existing services and foundation, encompassing online services as well as expansions into physician-related and pharmaceutical sectors. For instance, to enrich the industrial ecosystem and establish service barriers, “Ruolin Yishi” was established, forming a team of physician agents to provide the industry with short-video brand operation and traffic conversion services that integrate both public and private domain strategies; an online pharmaceutical retail license was obtained to launch e-commerce retail of drugs and medical devices; patient-centered specialty disease management operations were established, accelerating the digitalization of business and products; and collaborations with insurance companies were initiated to explore innovative payment models.

The aforementioned new business initiatives not only offset the revenue shortfall in general practice services but also achieved income growth.

Guangrui Medical has diversified its specialty offerings by adding traditional Chinese medicine, dental, and optometry services, while also launching health examination operations; these new revenue streams have reduced its reliance on respiratory diseases.

“The three newly established departments contributed to a certain growth in our revenue in 2021 and 2022,” said founder Zhang Junbo. He added that the company had maintained an expansion trajectory over the past three years, opening two new clinics in 2021 and five in 2022. In addition to Anhui Province, its services now cover Zhejiang, Jiangsu, Hainan, and other regions. “Over the past three years, our workforce has grown from 400 to nearly 600 employees.”

To gain something, one must give up something else; making painful sacrifices is an unavoidable choice for clinics facing reality.

In October 2022, Yaeher Health closed its first offline clinic, Shenzhen Yaeher Jia Clinic. It is reported that the clinic was established in 2018 and achieved profitability within just five months of opening.

In 2021, Dr. Lü’s Clinic closed several outlets registered around 2018, which were primarily located in new residential communities and industrial parks where resident occupancy or enterprise tenancy rates had fallen short of expectations. While closing these underperforming locations, the clinic opened new stores to optimize site selection and slow down its expansion pace.

“In 2019, we opened six new clinics, gearing up for a major push in 2020,” said Luo Lin. However, when the pandemic struck, these clinics had not yet commenced operations and lacked an established patient base. With restrictions prohibiting the treatment of patients presenting with ten specific symptoms, they were left with no choice but to shut down. “What can now be explained in a single sentence was an extremely painful process at the time.”

In recent years, clinics have become a sector “shunned” by capital. Apart from consumer-oriented clinics such as those in dentistry and ophthalmology, as well as specialized clinics in fields like psychiatry/psychology and rehabilitation, general practice clinics have received even less attention. Over the past three years, financing activity for general practice clinics has been sluggish, with Linjia Haoyi and YAEHER HEALTH being among the few exceptions.

Nevertheless, both clinic entrepreneurs and investors have observed this shift: over the past three years, the clinic sector has seized the opportunity to undertake essential tasks that should have been addressed earlier. First, leveraging their inherent strengths in medical practice, clinics have conducted a more thorough review of their operations, optimizing and adjusting their business structures by promptly eliminating segments that contribute little to overall operational performance or even incur unnecessary costs. Second, they have attempted to extend their business scope, exploring healthcare delivery models better suited to their specific circumstances. Overall, there has been more rational reflection on their positioning and future strategies, resulting in a sharper focus on core business activities.

It is precisely because of the more rational choices and reflections made over the past three years that the clinics that have persisted now enter the new normal with greater confidence. VCBeat has learned that many chain clinics have already formulated their plans for the next three to five years around the Spring Festival.

One is to build a reserve of physician resources.

For clinics seeking rapid expansion, physicians represent the most significant bottleneck. Limited resources must be allocated between public and non-public sectors, as well as between hospitals and primary care institutions, yet the overall supply remains constrained in its growth.

According to Zhang Junbo, the optimal approach is to cultivate talent in-house, ensuring that standardized content is integrated into the training process and leveraging digital tools to align all physicians along a unified workflow. Previously, Guangrui Medical established clinical guidelines for 47 common diseases within its outpatient standardization system and embedded them into its SaaS platform to standardize diagnostic and treatment processes and homogenize clinical outcomes. Moving forward, the company will continue to refine its talent development system, strengthen standardized protocols, and ensure their effective implementation.

Linjia Haoyi plans to further expand its network of specialist resources in key cities, facilitating the enhancement of specialists’ personal brands to drive traffic conversion. In this process, the “Ruolin Yishi” brand will play a pivotal role. Built around physicians’ intellectual property (IP), the platform provides branding support that enhances physicians’ competitiveness.

Second, explore the “1+N” business model: integrating general practice with specialties, and combining primary care with long-term management.

Restoring general practice services is a consensus among general practice clinics, but the pandemic has also made the industry realize that general practice alone is far from sufficient. Combining general practice with several specialized disciplines, or integrating it with disease management programs that involve more frequent patient engagement, can generate stable revenue.

In Xiezhuo Medical’s general practice services, standard pricing has been established for ten common conditions, including adult oral ulcers, gingivitis, and acute rhinitis. The combined fee for consultation and two days’ medication ranges from 25 to 30 yuan. Within this standardized pricing framework, physicians make diagnoses and prescribe medications based on the patient’s condition; additional treatments required due to individual differences are billed separately.

On the surface, such low unit prices seem insufficient to sustain overall revenue. However, Huang Xianjin, founder of Xiezhuo Medical, stated that price-regulated services can cover a portion of patients and serve as “traffic-driving” products for the clinic. By utilizing these services for minor ailments and treatments, the clinic aims to enhance patient experience and build its reputation, while also establishing a patient flow foundation for its chronic disease management business. Currently, Huang Xianjin is working with his partners to plan a sleep center, leveraging long-term care models to improve patient conversion rates.

How to Select Specialty Disciplines on the Basis of General Practice? Linjia Haoyi Has Summarized 10 Labels, Including: Requiring Long-Term Disease Management, Difficult to Implement in Public Hospitals, Not Relying on Medical Insurance, Possessing Clinical Attributes While Leaning Towards Consumer Healthcare, etc.; During the Pandemic, It Selected Three Specialties—Men's Health, Dermatology, and New Traditional Chinese Medicine—for Focused Development Based on These Labels, and Will Continue to Deepen and Enrich Specialty Services According to These Criteria in the Future.

Third, increase investment in digital infrastructure to enable more refined digital management.

From the patient’s perspective, online services have become a standard offering for physical medical institutions. It is also an industry consensus that leveraging digital tools can make healthcare access more convenient for patients and enhance the continuity of care, which requires clinics to increase their digital investments on the patient side.

From an operational and management perspective, digital tools are powerful instruments for achieving standardized and chain-based operations. While standardization is a path that all chain enterprises must follow, differences in local environmental factors, personnel, and information make the implementation of standardization far from easy.

Multiple chain clinics have stated that digitalization can address the issues of information asymmetry and management asymmetry in chain operations.

Fourth, extend the business planning cycle.

In recent years, managers have tended to favor annual planning, with significant adjustments made on the fly during implementation due to control measures. Now, supported by specific business objectives, some clinic chains have set their plans directly on a five-year horizon, aiming to expand from the current 30-plus clinics to 100, adding more than 10 new locations each year. Some clinics also indicate that integrating in-depth health management services atop general practice could raise the average transaction value from tens or hundreds of yuan to thousands or even tens of thousands of yuan in the future.

More pragmatic business construction and bolder long-term planning are also strong manifestations of the recovery in the clinic industry.

After Enduring a Three-Year Crucible, Will the Clinic Industry Achieve Greater Success in the New Normal?

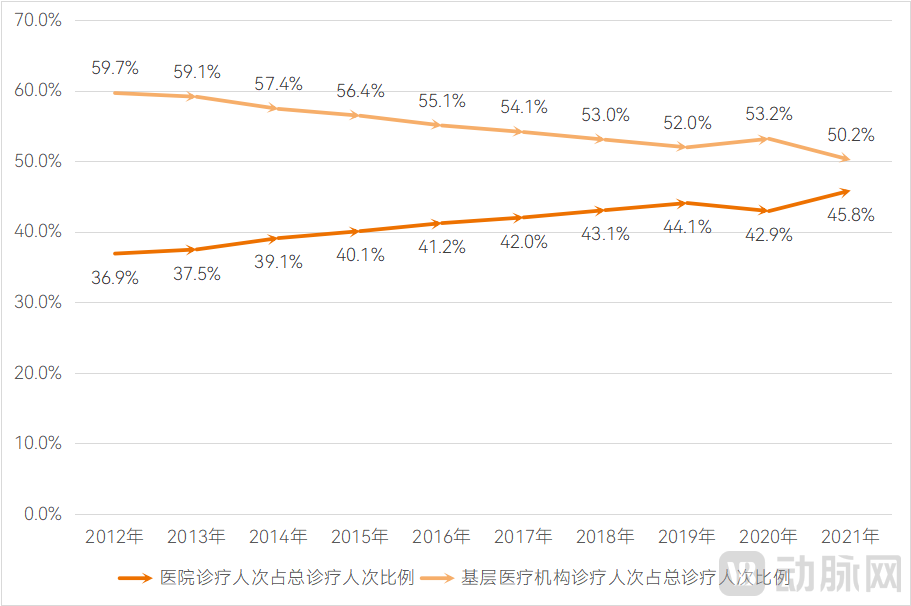

A set of macroeconomic data better illustrates the future growth potential of the healthcare industry. Over a ten-year period, both the number of medical institutions and the overall volume of services have been on an upward trend, with primary care institutions—including clinics—also experiencing continuous growth, except for a decline in service volume during the pandemic. During the same period, the number of hospitals and outpatient visits also increased. However, the development of primary care institutions has lagged significantly behind that of hospitals, primarily reflected in their share of total services.

Specifically, over the past decade, the proportion of consultations at primary care institutions in the total number of medical consultations has declined year by year, while the share accounted for by hospitals has risen annually. In 2012, consultations at primary care institutions constituted nearly 60% of the total; this figure has since gradually decreased, falling to 50.2% by 2021. Meanwhile, the proportion of hospital consultations increased from 36.9% in 2012 to 45.8% in 2021. The data trend indicates that this shift was already evident before 2019, suggesting that it is not directly related to the pandemic.

Proportion of Service Volume at Primary Healthcare Institutions and Hospitals in the Total Service Volume of Medical Institutions. Data Source: China Health Statistics Yearbook; Chart by VCBeat

In recent years, the Chinese government has vigorously promoted a tiered diagnosis and treatment system, in which primary healthcare institutions serve as a critical force by providing initial consultations and accepting patients referred down from higher-level hospitals. Previously, national assessment criteria for pilot programs on tiered diagnosis and treatment set a target that, by 2017, the proportion of outpatient and inpatient visits at primary healthcare institutions would account for no less than 65% of the total nationwide. However, the final figures fell short of this expectation. This indicates that resource allocation in primary healthcare institutions still requires improvement, and the anticipated shift of growing healthcare demand to the primary care level has not yet become significant.

If calculated based on a 65% share of total clinical visits, there remains a gap of over one billion visits between the current service volume of primary healthcare institutions and the ideal target. This disparity highlights the bias in medical resource allocation and underscores the significant growth potential for primary healthcare institutions.

Of course, primary healthcare also includes community health service centers and township health centers, which are predominantly public. Non-public medical institutions are mainly distributed across clinics and outpatient departments. In terms of service offerings, public institutions also base their operations on general practice and provide chronic disease management for residents; therefore, clinics need to differentiate themselves from these public providers.

Public primary healthcare institutions are required to fulfill the responsibilities of providing basic public health services, whereas private clinics and outpatient departments tend to focus on market-oriented operations. Significant differentiation will emerge in areas such as general practice and chronic disease management. It is encouraging to observe that the industry has already begun exploring and conceptualizing models such as value-based pricing for medical consultations and differentiated branding strategies. There is good reason to believe that, under the new normal, the thriving clinic sector is poised for a resurgence.

Note: The clinics mentioned in this article specifically refer to new-type clinics whose primary services are general practice and pediatrics.