In-Depth Dialogue with 13 Top-Tier Investment Firms: 2023 Medical Investment Logic Unveiled

MPCi

Venture Capital Institutions in High-Tech Startup Fields

About a month ago, as the clock was about to strike midnight marking the end of 2022, a healthcare venture capitalist stared intently at his phone, quietly watching the “2022” on the screen change to “2023.”

At this moment, his feelings are complex, as 2022 was undoubtedly a challenging year for him in the healthcare industry, influenced by multiple factors such as pandemic control measures and changes in the global competitive landscape.Uncertainty in the healthcare industry is becoming increasingly pronounced, with “survival” emerging as the central theme of this high-profile sector.At the same time, with the start of a new year and the gradual waning of the pandemic’s impact, he has become filled with anticipation for the future, as if re-entering the healthcare industry.

In fact, this “he” does not refer to any single individual, but rather represents the vast majority of healthcare venture capitalists. Through a continuous process of doubt and adjustment, they navigated the tumultuous year of 2022, encountering opportunities and challenges unlike any they had faced in their careers. As the new year arrives, with the market economy gradually recovering and the healthcare industry steadily moving toward revitalization, these seasoned healthcare investors are poised to embark on a new adventure in 2023.

Therefore, for the entire healthcare industry,This year’s transition is unlike previous ones, carrying far greater significance in bridging the past and the future., and precisely because we stand at this historical juncture, VCBeat, with nearly a decade of deep engagement in the healthcare industry, seeks to document every detail of this journey through a unique format.

In response, VCBeat specially planned for the 2023 Lunar New Year《2023 Investment Barometer》Special topic, and in the past half monthIn-Depth Conversations with 15 Healthcare Venture Capitalists from 13 Top-Tier Investment Firms, we reflected on the arduous yet momentous year of 2022, and looked ahead to 2023—a year of uncertainty, yet one in which we remain convinced that hard work will bring about positive outcomes.

1. Wang Junfeng, Co-Chief Investment Officer at Legend Capital

2. Yu Zhiyun, Partner at MPCi

3. Luo Xi, Executive Director of the Healthcare Technology Group at China Renaissance New Economy Fund; Jiang Jiajia, Managing Director of the Healthcare and Life Sciences Division at China Renaissance

4. Li Gang, Partner and Co-Head of Healthcare Industry at China Renaissance

5. Chen Penghui, Founding Partner of Boyuan Capital

6. Yu Fang and Song Gaoguang, Partners at Northern Light Venture Capital

7. Liu Yu, Managing Partner of BGI Win-Win Industry Fund

8. Ouyang Xiangyu, Founding Partner of Sherpa Capital

9. Sun Xiaolu, Founding Partner of Proxima Ventures

10. Jiang Xiaodong, Partner at Changling Capital Management

11. Yang Ruirong, Founding Partner of Yuan Yi Capital

12. Chen Kan, Partner at Qiming Venture Partners

13. Li Yishi, Senior Partner at Haoyue Capital

2022 Keywords for the Healthcare Industry: Sluggishness, Difficulties, Uncertainty

When asked, “How do you view the changes in the healthcare industry in 2022?” nearly all 15 healthcare venture capitalists gave a unified answer—Cold, this can also be clearly felt from the three high-frequency words extracted from their responses, namelySlump, Difficulties, and Uncertainty. One investor even remarked with emotion during the interview,“Among investors and startups of our generation, hardly anyone has experienced difficulties of this magnitude.”

So, how exactly do these “difficulties” manifest? Let’s first look at a set of data.

·In 2022, 17 biopharmaceutical companies were listed on the A-share market, with 9 of them trading below their IPO prices; only 5 companies were listed on the Hong Kong Stock Exchange, and while just one traded below its IPO price, the other four experienced only marginal gains.Overall, the number of companies listed on the A-share and Hong Kong stock markets in 2022 decreased by more than 40% compared to 2021.

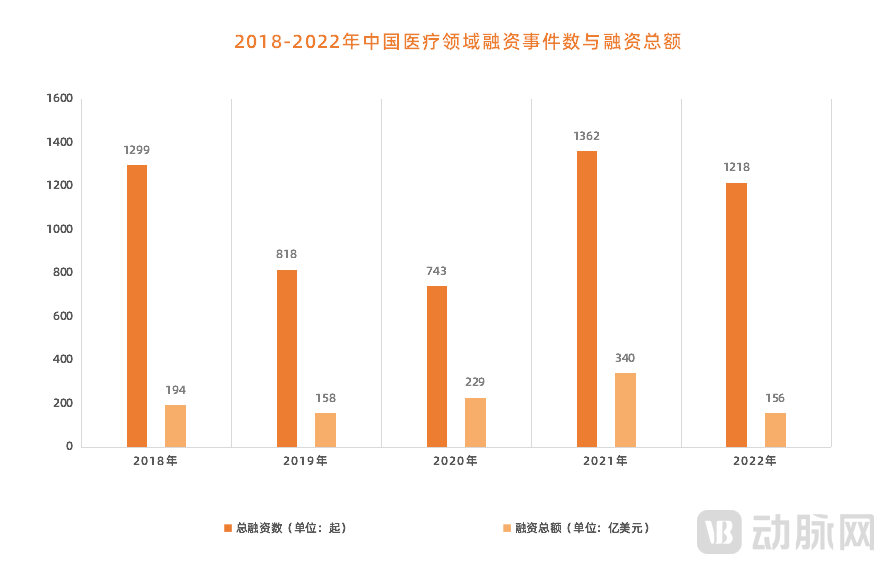

·In 2022, a total of 1,218 financing events occurred in China's healthcare sector, with the disclosed total financing amount reaching approximately USD 15.6 billion.Both the number of financing events and the total amount of financing have shrunk by more than one-third compared to 2021.

·In 2022, based on the total financing amount in China’s primary biopharmaceutical market for which specific figures were fully disclosed,The average amount per financing round was approximately RMB 246 million, representing a 46.8% decline compared with 2021 and less than half of the 2019 level.

· In 2022, angel and seed financing rounds accounted for 23.5% of China’s primary biopharmaceutical market, while Series A financings comprised 46.8%, with both figures reaching their highest levels in the past three years; however,Financing events in the mid-to-late stages declined significantly, with only 94 deals at Series D and above, representing a nearly 50% decrease compared to 2021.

Figure 1. Number of Financing Events and Total Financing Amount in China’s Healthcare Sector, 2018–2022

Accompanying this series of cold, hard data was the perplexity etched on the faces of most healthcare entrepreneurs and investors in 2022. For entrepreneurs, fundraising became extremely difficult amid a cooling capital market, while business operations also suffered significant setbacks due to pandemic-related lockdowns.This means that companies have less disposable cash on hand, and in some cases, their capital chains break down entirely.

Consequently, companies in a slightly better position have managed to survive by slowing down their R&D progress or reducing labor costs. However, some healthcare enterprises have not been so fortunate and have had to announce their exit from the market. This is particularly true for startups, which face a significantly higher risk of elimination due to their lack of established resilience against risks.

Entrepreneurs had a tough time, and healthcare investors certainly didn’t fare much better in 2022.

Like entrepreneurs, investors first face the issue of “survival.” Due to the sluggish performance of the secondary market, a shrinking M&A market, and greater difficulties in exits, many firms actively or passively chose to withdraw from the healthcare market in 2022. Those investment institutions that remain resilient in the healthcare market, however,Pace has slowed significantly, with a marked reduction in both the number of deals and the capital invested per transaction, as well as a deceleration in decision-making speed.

Amid this “slow-paced” environment, investment institutions have become increasingly cautious and rational, with fundamental shifts in their project selection criteria—transitioning rapidly from the diverse proliferation seen in the previous two years to a highly selective approach in 2022.Key FocusWhether the invested projects possess hard-core innovation, rank among the top three in their respective niche segments, and have the potential to achieve global best-in-class or first-in-class status.

Certainly, the more stringent and granular the criteria for selecting investment targets, the greater the pressure on investors. This challenges not only their understanding and foresight regarding industries and specific projects, but also the depth of their resource networks, as well as their ability to help portfolio companies “weather the winter” or even achieve a rapid breakthrough during industry downturns.

Proactively Embracing Change by Moving “Early,” with Greater Focus on the Technology Itself

In 2022, healthcare venture capitalists felt as if they had been dealt a severe blow.In the previous year, namely 2021, the entire healthcare industry stood at a pivotal growth point, with all core metrics surging at an accelerated rate of 20% to even 50%, nearly reaching historic peaks.

In the secondary market, a total of 98 Chinese healthcare companies went public on global capital markets in 2021, representing a 38% increase from 2020. Furthermore, the primary market was equally robust: in 2021, there were 1,362 financing deals in the healthcare sector, with total funding approaching $34 billion—both figures nearly doubling compared to 2020.

Impressive data gave healthcare professionals greater confidence and higher expectations as they entered 2022. However, things did not go as planned. Starting in January 2022, Shenzhen implemented widespread lockdowns due to the pandemic, followed by varying degrees of epidemic control measures in other major healthcare hubs such as Shanghai, Beijing, and Suzhou. The domestic healthcare industry began to experience periodic standstills, with successive waves of headwinds bursting one industry bubble after another.

In such an environment rife with uncertainties, naturally astute healthcare venture capitalists are also making adjustments.They all seek certainty amidst industry turbulence.. Through interviews with 13 leading investment firms, we have observed subtle shifts in their healthcare industry investment strategies in 2022.

First, the overarching direction is to resolutely advance deeper into early-stage healthcare.

In discussions with 13 leading investment firms regarding changes in their 2022 investment strategies, nearly all of them mentioned phrases such as “focusing on the early-stage market,” “moving earlier,” and “investing early.” Clearly,“Investing early and in small ventures” has become the consensus among healthcare investment firms today.。

This is certainly not without reason. From a macro perspective, in recent years, driven by multiple key policies, technology transfer and technological innovation have become keywords in the healthcare industry. Both the government and research institutions have made substantial investments to better promote medical innovation and translation, while scientists, who were previously accustomed to staying within academic circles, are gradually moving closer to the industry. Amidst this transformation, numerous innovative medical technologies have emerged, creating significant early-stage growth potential, all of which represent opportunities for the healthcare industry.

From a micro perspective, innovation in China’s healthcare industry has entered a phase that demands “genuine innovation.” Industry bubbles are gradually dissipating, and the industrial structure is undergoing further restructuring. In this process of continuous disruption yet steady progress, only innovative projects with truly original technologies and substantial market potential are more likely to stand out in the future. Therefore,“Investing early” is not a hyped trend, but a cyclical pattern inherent to the development of the healthcare industry.

As the broader trend of “early-stage investing” takes hold, investment firms are redefining healthcare projects, with core criteria broadly summarized by two keywords: hard tech and long-term value.

“Hard tech” is primarily reflected in specific niche sectors, with a focus on the most prominent areas of medical innovation, such as synthetic biology, brain science, life science tools, and gene editing. It can also be embodied in the products themselves. On one hand, products must address critical clinical needs by targeting key pain points in diagnosis and treatment, significantly improving the efficiency of healthcare resource utilization, and reducing health insurance expenditures. On the other hand, products must demonstrate strong innovativeness, characterized by high technological barriers, world-class competitiveness, and a certain pace of R&D commercialization.

“Long-term value” is reflected in a company’s future growth potential, meaning it does not target short-term gains but instead adopts a long-term development perspective and industrial vision, possessing core competencies that enable it to expand overseas and compete with global industry leaders.

Whether extending investments to earlier stages or imposing new requirements on investment targets, these are adjustments to investment strategies based on the current state of the industry. Beyond such adjustments, investment institutions also achieved a certain degree of “evolution” in 2022, primarily reflected in refining value-added services and establishing a healthcare ecosystem.

As the healthcare market cooled in 2022, companies faced mounting survival pressures. As “co-entrepreneurs,” investment institutions need to step out of their comfort zones at this juncture, stand more closely with portfolio companies, and jointly address the most pressing challenges. This requires investment firms to possess more diversified capabilities to provide long-term empowerment to enterprises, such as offering financing services, engaging in strategic planning together, executing marketing initiatives, and even assisting with workforce reductions to increase revenue and cut costs.

However, whether it is strategic adjustment or the evolution of service capabilities, 2022 inevitably presents significant challenges for healthcare venture capitalists, while also revealing certain opportunities.This may be a once-in-a-career or rare opportunity for an investor.

Which Niche Sectors Did Investment Firms Bet on in 2023?

Will the healthcare industry fare well in 2023? Thirteen leading investment firms have all given affirmative answers without exception. Amidst this optimism for the sector, they have also pinpointed new investment directions, which can be broadly categorized as follows:

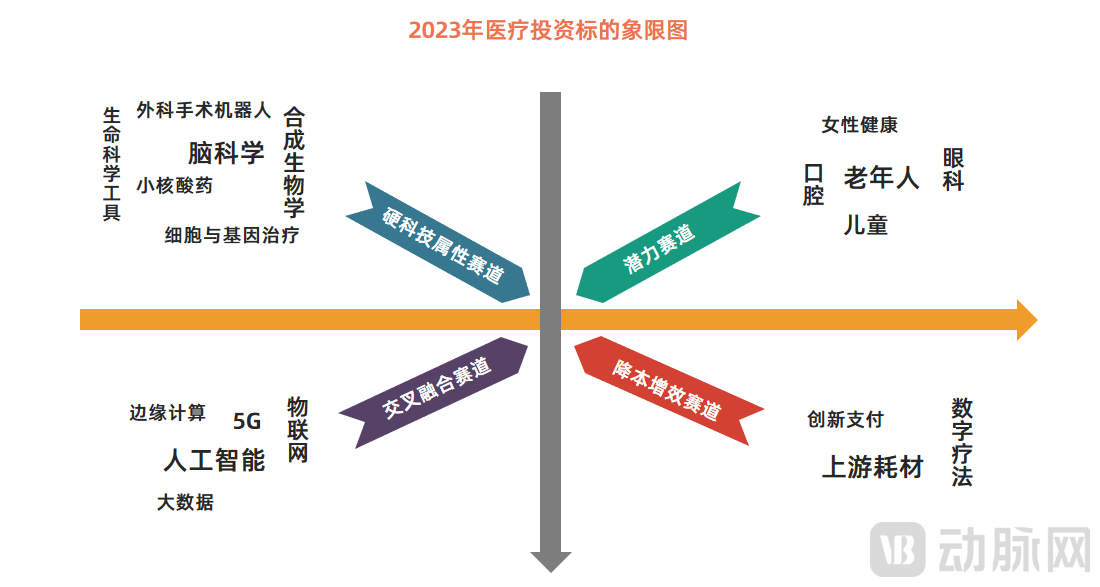

Figure 2. Quadrant Chart of Healthcare Investment Targets in 2023

Figure 2. Quadrant Chart of Healthcare Investment Targets in 2023

The first category comprises hot sectors with strong hard-tech attributes., mainly includingCell and Gene Therapy, Nucleic Acid Drugs, Brain Science, Synthetic Biology, Life Science Tools, Surgical Robotsetc. These cutting-edge medical sectors demonstrated remarkable activity in the capital markets in 2022, with a significant proportion of early-stage investments. They hold immense potential for the future and represent key areas of focus for investment institutions in the coming years.

The second category comprises high-potential sectors with substantial market space but still in the early stages of development., a typical representative is"Silver Economy", namely the health needs of the elderly in medical settings. It is reported that more than half of the 13 investment firms interviewed by VCBeat have identified this as a key investment focus for 2023. In addition, within this category,OphthalmologyandOral Cavityhave also been frequently mentioned by investment institutions.

In fact, the characteristics of these high-potential sectors are quite distinct. First, they exhibit strong consumer-oriented attributes and substantial market demand. Second, their primary focus is on enhancing patients’ experience with medical services, rather than on life-saving interventions. Finally, under the extensive reach of digital health, these high-potential sectors offer greater possibilities in terms of service scenarios. Taking the elderly population as an example, future healthcare service scenarios could include home-based medical care, as well as health protection, diagnostic products, and convenient services tailored specifically for older adults.

The third category comprises high-value sectors capable of reducing costs and improving efficiency., with typical representatives in the healthcare industryUpstream Supply Chain: From Core Components to Upstream Raw Materials. Influenced by the international landscape and geopolitical dynamics, medical resources, as a core component of national welfare and people’s livelihood, must be independently produced in China to avoid supply chain vulnerabilities. This self-reliance is not only a mandatory choice for the nation but also an inevitable requirement and key direction for the development of the healthcare industry. Among the 13 investment institutions interviewed, five expressed optimism about its future prospects.

The fourth category is the track featuring the cross-integration of innovative technologies and healthcare scenarios.The rapid development of the healthcare industry over the past decade is closely linked to the influx of internet technologies. Now, as clinical needs undergo another round of iteration, stakeholders are seeking new breakthroughs and beginning to explore the deep integration of global innovative technologies with unmet medical needs. Based on market conditions in 2022, this cross-sector integration has identified certain channels and achieved some progress; however, this is far from sufficient. Significant room for future growth remains, awaiting discovery by venture capital and investment firms.

Beyond their optimism about the sector, investment institutions also harbor certain concerns regarding their portfolio companies in the coming year.They assessed that although the healthcare market would gradually recover in 2023, the return of the economy to a growth trajectory would not be smooth, and the funding winter would not disappear overnight.

Therefore, healthcare entrepreneurs must persevere."Small Steps, Quick Iterations"proceed at a measured pace by controlling R&D investment, ensuring healthy cash flow, and allocating resources to the most critical areas. In addition, companies should seize every opportunity to secure sufficient funding as early as possible, using capital to optimize technology and products, advance R&D toward key business milestones, and enhance risk resilience, rather than focusing solely on valuation growth. Furthermore, enterprises should actively pursue global expansion, striving to develop their domestic and overseas businesses in parallel.

When discussing “changes in the healthcare industry in 2022,” investors, while acknowledging the reality of a cooling market, also identified some positive developments, stating“The significance of cold lies in ecological evolution.”

It is undeniable that the healthcare industry in 2022 was undoubtedly in a downturn. However, this industrial winter also cleared out a significant portion of non-professional and non-industry capital, as well as many projects with uncertain commercialization prospects. This is not necessarily a bad thing. In the post-trial industry ecosystem, project teams will have more objective valuations of themselves, placing greater emphasis on the innovativeness of their R&D pipelines, clinical value, commercialization progress, and prospects. On the other hand, investment institutions will become more rational, emphasizing professionalism and a deeper understanding of technical products, including a more profound comprehension of the cyclical nature and risk implications within the healthcare industry.

In other words,Everyone’s mindset has become more mature, and their behavior will inevitably be more rational.Isn’t this a signal that the healthcare industry is entering yet another new phase? Looking back at 2022,Rather than saying we are observing a market downturn, it is more accurate to say that we are witnessing the dawn of a new era.