Spotlight on the 23 Biopharma Companies That Went Public on U.S. Exchanges in 2022: Pathways to Value Creation and Market Recovery Outlook

Initial Public Offerings (IPOs) are the lifeblood of the biotechnology industry. Going public enables young companies to raise substantial capital to advance drug clinical trials, while providing their investors with opportunities to realize returns or invest in emerging biotech ventures.

Biotech companies and their backers have reaped rewards over the past decade, with an increasing number of biotech firms going public at high valuations. In 2021, despite the significant impact of the COVID-19 pandemic, more than 100 biotechnology companies had initial public offerings (IPOs) in the U.S. stock market; this figure dropped to 23 in 2022.

Which biotech companies have successfully gone public? Which biotechs have created value? Which types of companies generate the best returns? Who are their largest investors?

Amid Challenging Conditions, Some Still Break Through the Fog: A Review of These 23 Companies. Data from Biopharma Dive May Offer Answers, Providing Inspiration for This Year’s IPOs and Realization of Innovation Value.

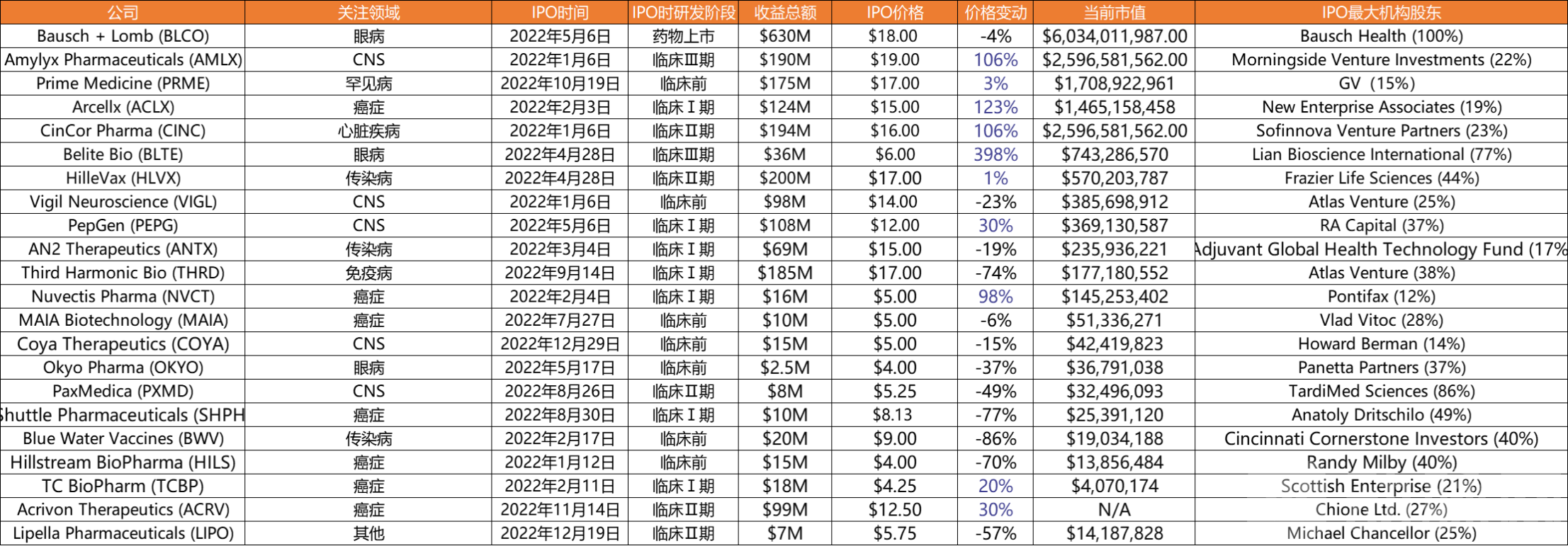

BioPharma Dive Database Statistics: List of Publicly Listed Companies in 2022 (February 1, 2023, 9:30 AM)

BioPharma Dive Database Statistics: List of Publicly Listed Companies in 2022 (February 1, 2023, 9:30 AM)

Data shows that among companies that went public in 2022, ten saw their stock prices rise. The largest increase was recorded by Belite Bio (BLTE), with a surge of 398%. This pharmaceutical company specializes in treating untreatable eye diseases, such as atrophic age-related macular degeneration (commonly known as dry AMD) and Stargardt disease, as well as metabolic disorders. The significant price increase was primarily due to its low valuation at the time of listing. Following closely were Arcellx (ACLX), Amylyx Pharmaceuticals (AMLX), CinCor Pharma (CINC), and Nuvectis Pharma (NVCT).

Arcellx is a clinical-stage cell therapy company whose technology platform primarily comprises ddCAR and ARC-SparX, both developed based on D-Domain technology. In December 2022, Kite, a Gilead Sciences company, announced a strategic investment in Arcellx’s CART-ddBCMA product valued at over $4 billion. On the same day, Arcellx released Phase 1 clinical data for CART-ddBCMA, demonstrating an overall response rate (ORR) of 100%.

Amylyx Pharmaceuticals is a pharmaceutical company specializing in providing solutions for Alzheimer’s disease and other brain disorders. Its independently developed oral powder formulation of sodium phenylbutyrate and taurursodiol received marketing approval from the U.S. Food and Drug Administration (FDA) on September 29, 2022, through the Priority Review pathway, for the treatment of amyotrophic lateral sclerosis (ALS, commonly known as Lou Gehrig’s disease) in adults.

CinCor Pharma is a biotechnology company focused on refractory hypertension and chronic kidney disease. Its core product, baxdrostat, is an aldosterone synthase inhibitor (ASI) intended for the treatment of hypertension in patients with refractory hypertension. AstraZeneca had made multiple acquisition offers for CinCor Pharma; however, the company’s market capitalization plummeted by half after issues arose in the clinical trials of its lead product. Ultimately, in January 2023, AstraZeneca acquired CinCor Pharma for $1.8 billion.

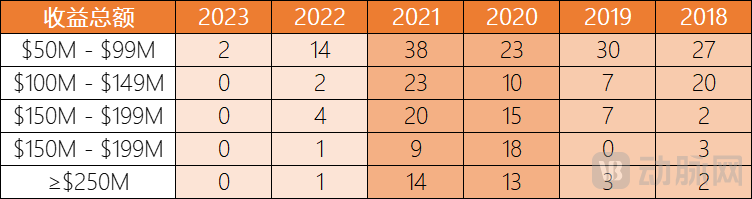

In terms of total revenue, directly impacted by the decline in the number of listed companies, overall revenue in 2022 decreased significantly compared to 2021. Only one company achieved revenue of USD 250 million, with the majority still ranging between USD 50 million and USD 100 million.

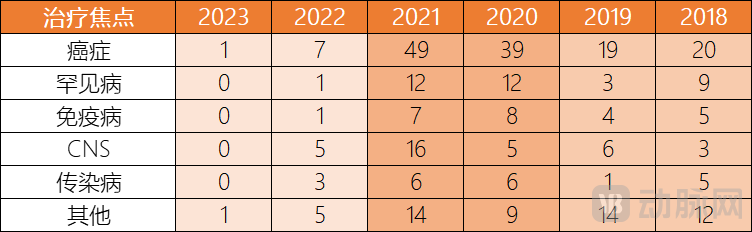

Most companies that successfully went public remain in the early clinical stages, showing little deviation from the trends observed in 2020–2021.

In 2022, biopharmaceutical companies listed in the U.S. exhibited distinct differentiated characteristics, with a significant number focusing on oncology, central nervous system (CNS) disorders, and other therapeutic areas. Among the two companies that went public at the beginning of 2023, one primarily specialized in oncology, reaffirming cancer as the most prevalent indication.

*“Other” includes liver, eye, heart, intestinal, metabolic, ear, skin, and kidney diseases.

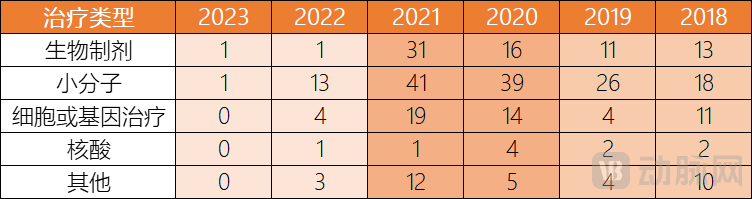

Small-molecule drugs are relatively mature and remain the primary therapeutic modality adopted by innovative pharmaceutical companies that launched new drugs last year.

*“Biologics” include biologics, antibodies, and microbiome therapeutics.

“Others” includes antibiotics, vaccines, radiopharmaceuticals, and drug delivery.

When will the recovery occur?

The IPO market for U.S. biotechnology companies has experienced its worst year in two decades, as the COVID-19 pandemic, the Russia-Ukraine war, record-high inflation, and rising interest rates have compressed public market valuations, leading to a stock market plunge.

Some experts believe that the public market will not recover quickly.

“2023 will be very challenging,” Jonathan Norris, Managing Director of Life Sciences and Healthcare at Silicon Valley Bank, said in an interview with foreign media. “We hope to see a turnaround in the second half of the year.”

Amid a sluggish IPO market, pharmaceutical companies seeking to go public may be forced to turn to alternative financing methods to sustain their operations. Companies awaiting an IPO may pivot to private equity financing; however, as demand for IPOs dries up, investors are becoming more cautious in providing capital. Fundraising declined across the board in 2022.

Will the pace of private financing continue to slow down? This is a topic of concern for the industry in 2023. A new report from Silicon Valley Bank suggests that the trend of lower transaction volumes may persist throughout 2023.

Overall financing volume has declined, which may lead to a decrease in the valuations of companies currently seeking funding. This could prompt enterprises to turn to internal financing, deferred financing, and bridge financing, all of which can provide capital without negatively impacting their valuations.

In addition to IPOs and financing, M&A activity in the biotechnology sector also stalled in 2022. However, compared with the pessimism surrounding IPOs and financing, industry participants generally hold an optimistic outlook on M&A. Some analysts and insiders anticipate that this stagnation will reverse in 2023, with both the size and volume of M&A deals expected to increase.

In January, the J.P. Morgan Healthcare Conference kicked off with the announcement of several M&A deals: AstraZeneca acquired CinCor Pharma for approximately $1.8 billion, and Ipsen acquired Albireo for €952 million. Merck & Co., which had made an offer at the end of last year, has now completed its acquisition of Imago BioSciences for $1.35 billion.

On December 13, 2022, Takeda announced a $4 billion acquisition of Nimbus Therapeutics’ wholly-owned subsidiary, securing its autoimmune disease candidate drug portfolio, a move that spurred some optimistic sentiment.

Since 2023, there have been at least six M&A transactions valued at $50 million or more, including Sun Pharma’s $576 million acquisition of Concert Pharmaceuticals announced on January 23.

BioPharma Dive Database: List of M&A Transactions in 2023 (as of 9:30 AM on February 1, 2023)

Nathan Ray, a partner at management consulting firm West Monroe, stated in an interview with foreign media that mergers and acquisitions activity may return to the pre-pandemic “new normal” levels seen in 2019.