Setting Sail with Renewed Momentum: 2023 Confidence Survey on Biopharmaceutical Industry Investment and Financing

In 2022, the global economy faced significant pressure, and investment momentum in China’s healthcare sector slowed, exhibiting a trend of “shifting from speculation to substance and returning to rationality.” After enduring a year-long “capital winter,” the biopharmaceutical industry finally began to sense the warmth of spring at the turn of the year.

As we bid farewell to 2022, a year rife with “black swan” events and “gray rhino” risks, what new trends will the biopharmaceutical industry embrace in the highly anticipated year of 2023, and what new challenges will it face? Furthermore, how will these trends and challenges influence capital allocation decisions?

As a leading investment bank in China’s healthcare industry, Haoyue Capital has always been committed to building a harmonious and integrated ecosystem for the sector, contributing to the advancement of China’s broader health industry. In the challenging year of 2022, Haoyue Capital defied the downturn, completing more than 50 complex transactions throughout the year, including private financing, mergers and acquisitions, and spin-offs of listed companies. Notably, over 20 of these transactions were in the biopharmaceutical sector alone. At the beginning of 2023, Haoyue Capital conducted the “2023 Biopharmaceutical Industry Investment and Financing Confidence Survey” through an anonymous questionnaire, gathering insights from more than 100 industry representatives across Biotech, Pharma, and VC firms. The report was officially released on January 12 at the “Bio Era · Embracing the Future” New Year Outlook Conference, jointly hosted by BioBAY and Haoyue Capital.

Hao Yue Capital aims to use this research report to map out the industry confidence landscape for the coming year, inviting peers in the biopharmaceutical sector to jointly embrace the dawn of a new era characterized by deep integration and symbiotic growth among Biotech, Pharma, and VC.

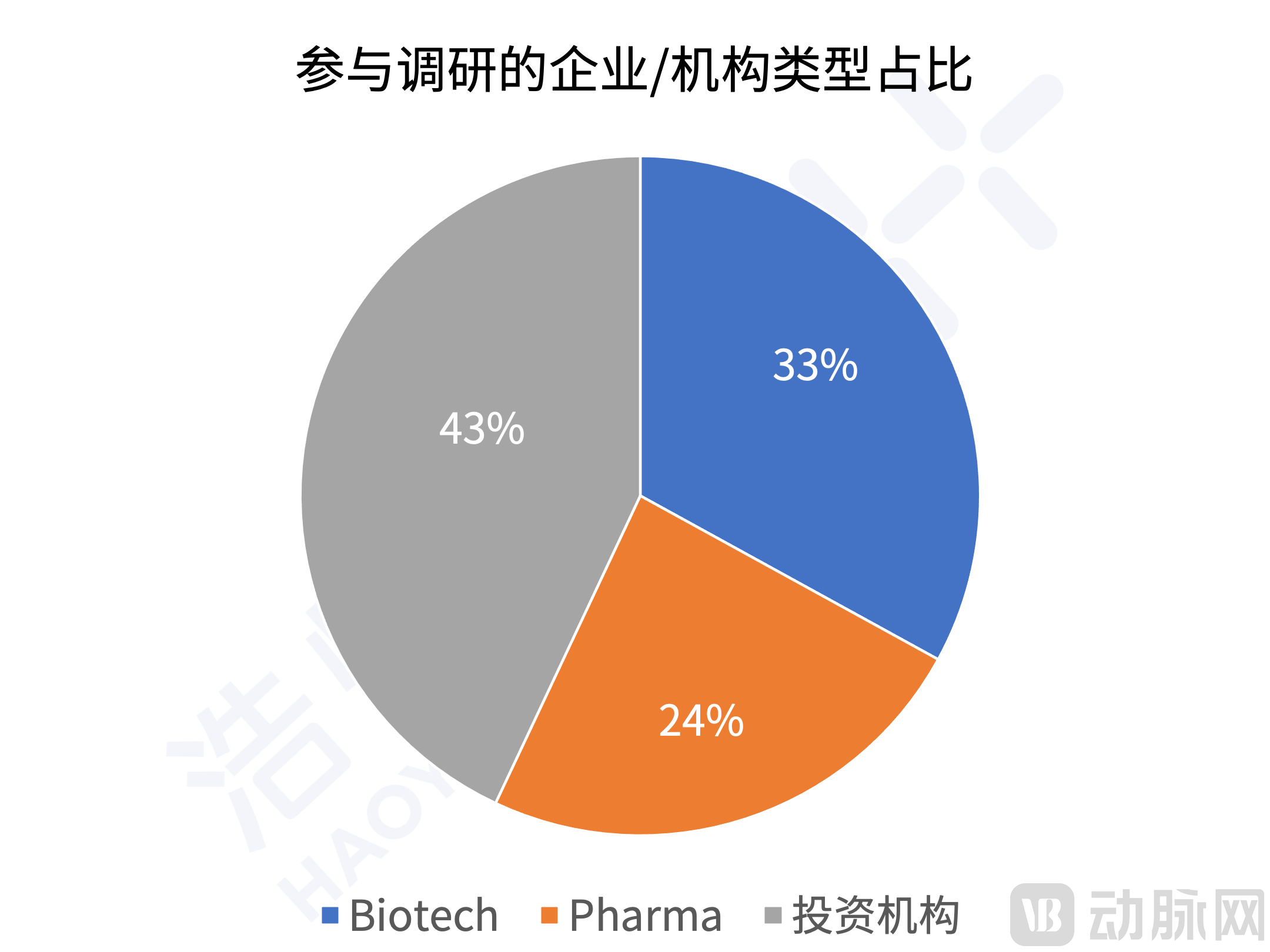

The types of organizations participating in this survey are as follows:

Biotech Section

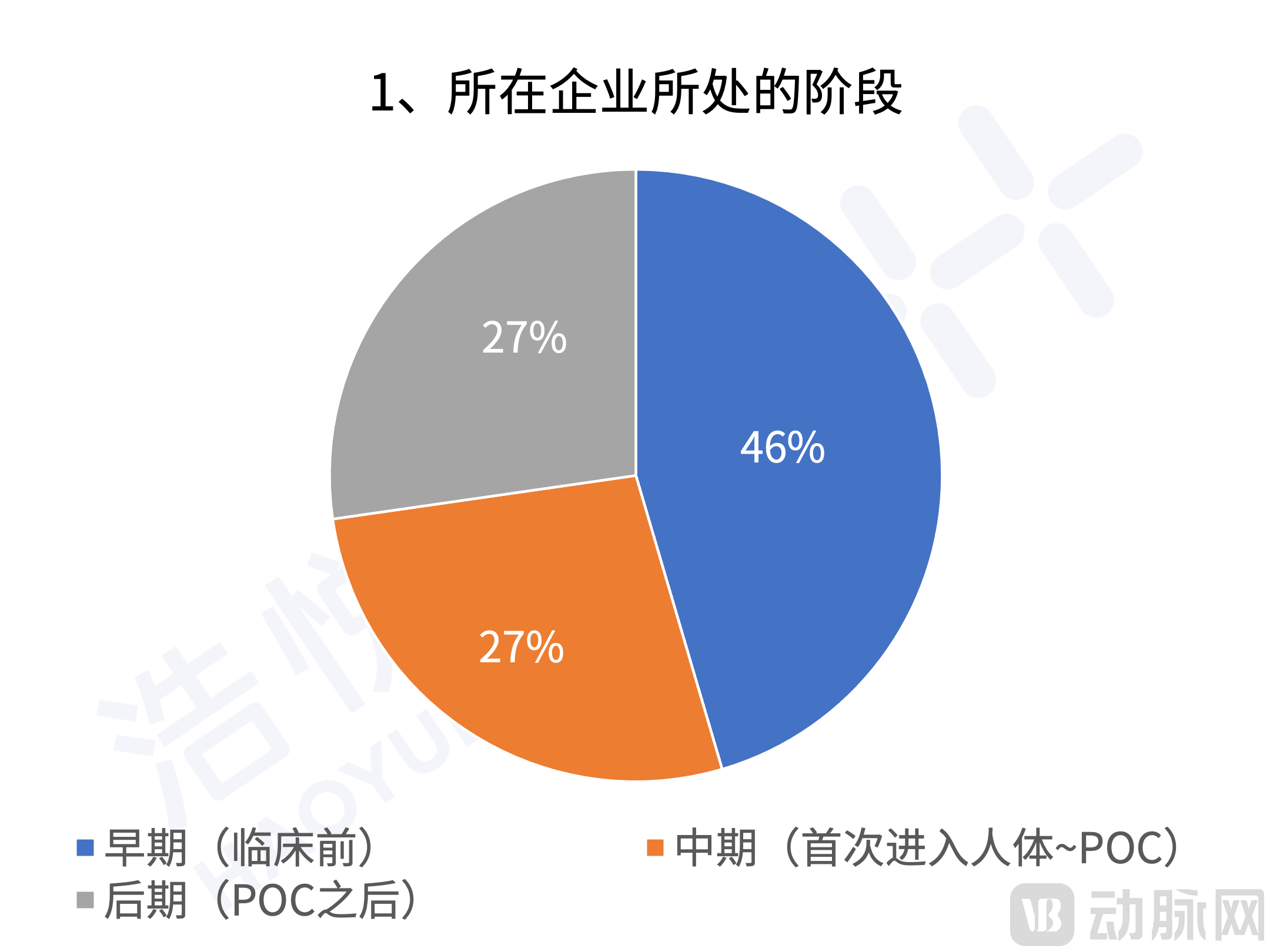

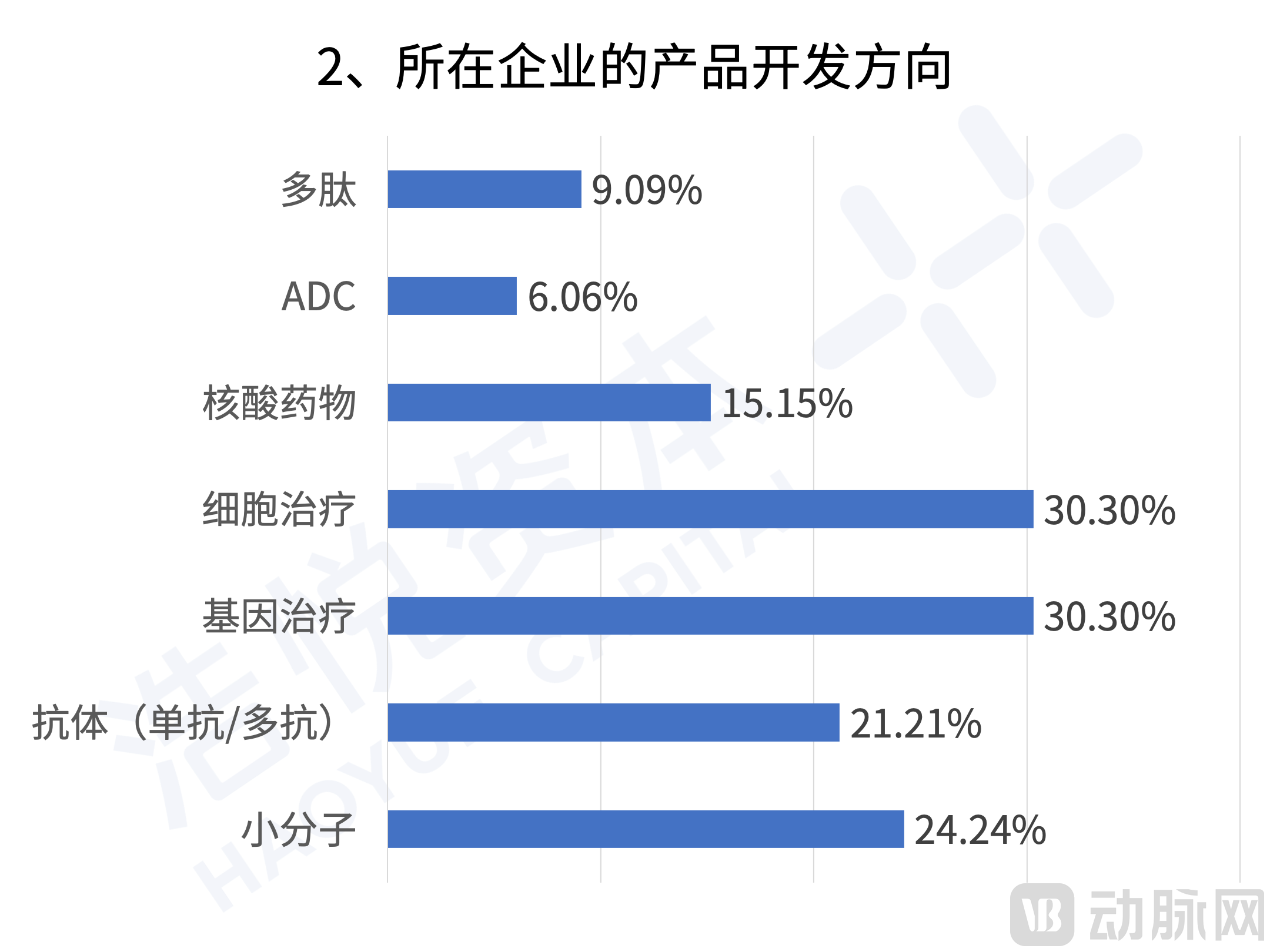

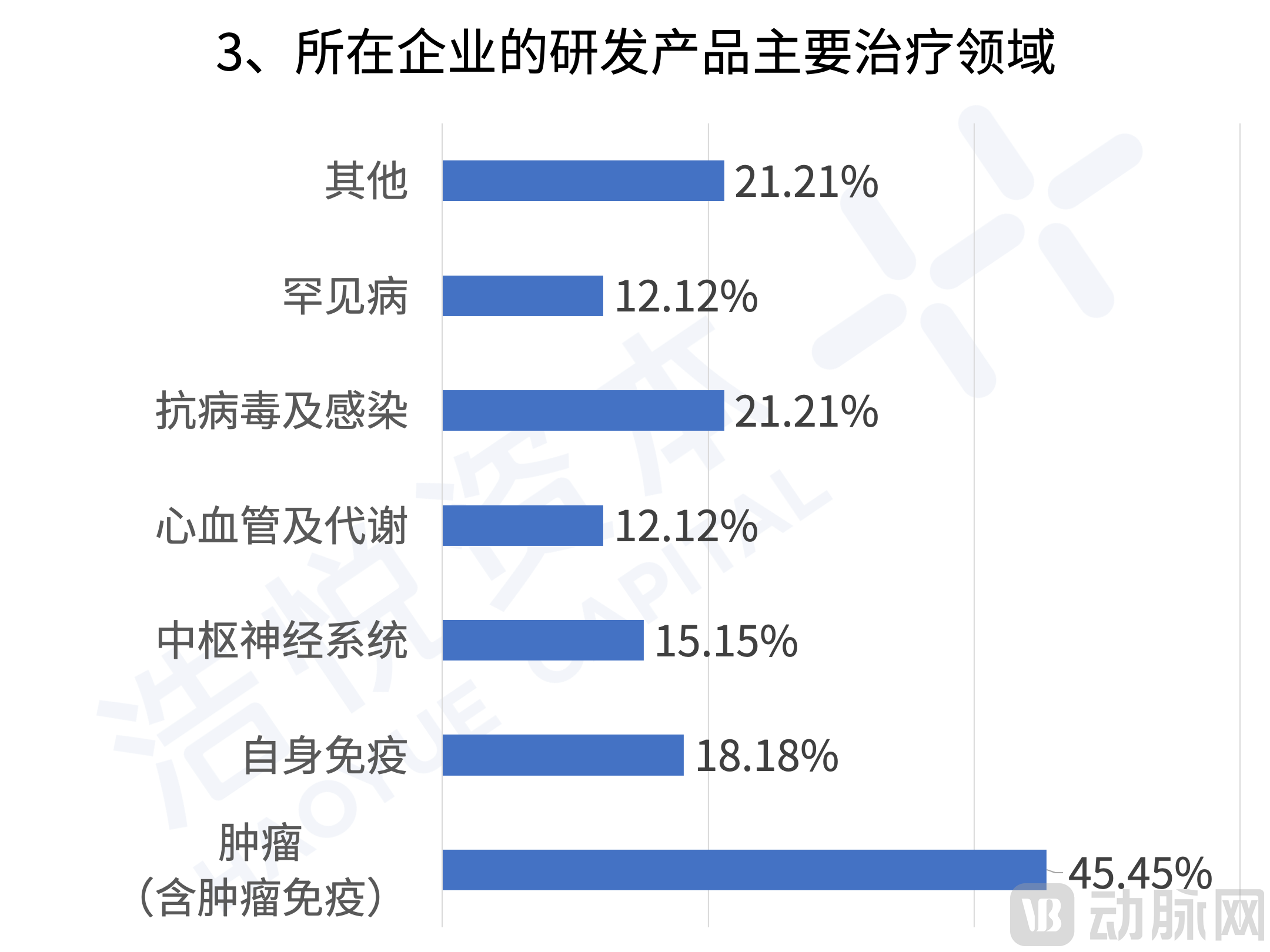

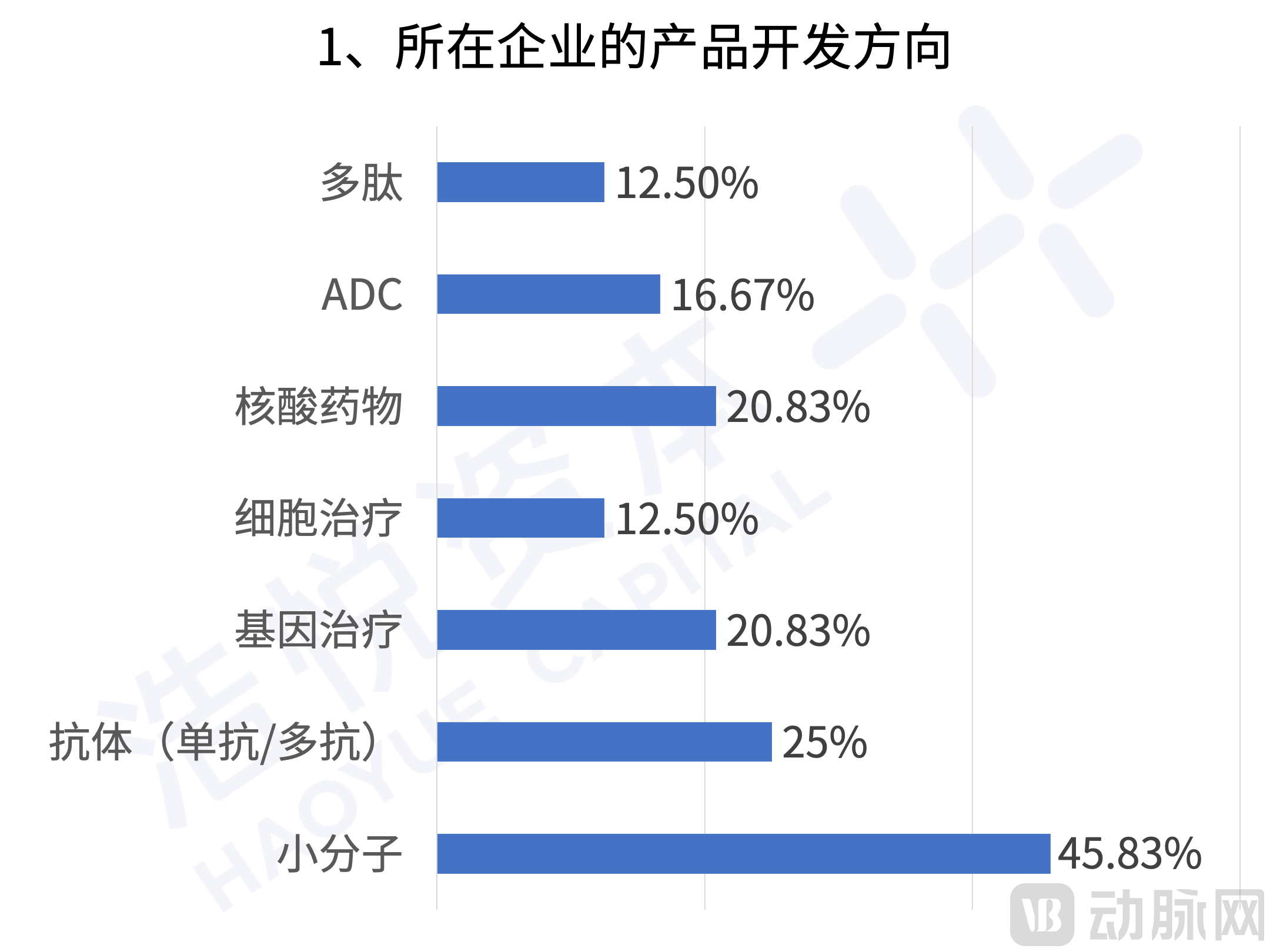

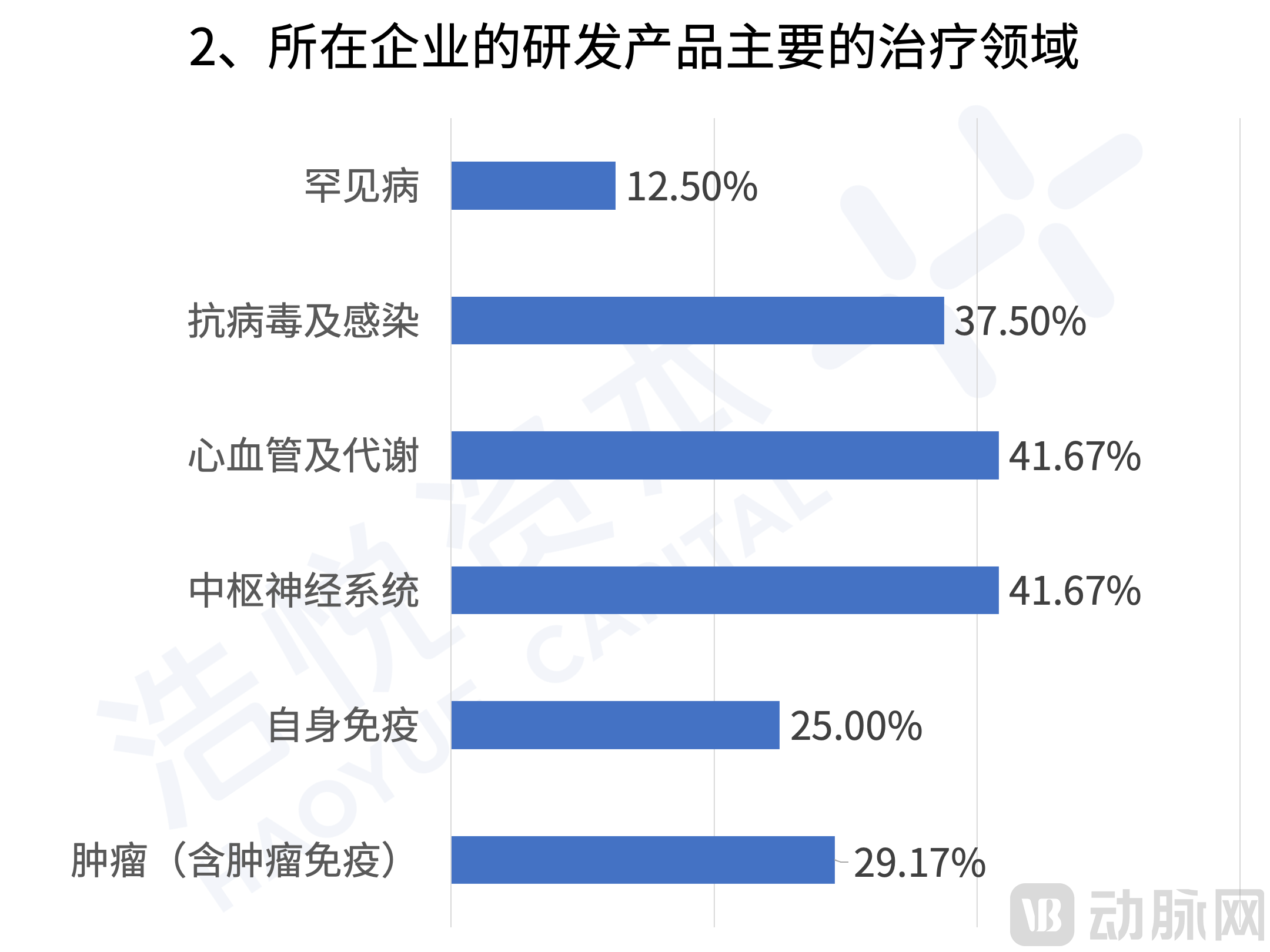

Survey results for biotech companies indicate that over 70% are still in the early to mid-stages of R&D (preclinical to proof-of-concept phase). This implies that the majority of these enterprises continue to rely on sustained external capital injection to support their R&D efforts, and founders are facing greater uncertainty in the current market environment compared to previous years. In terms of research directions, cell and gene therapy (CGT) has emerged as an industry hotspot and a primary focus for biotech companies’ strategic layouts, while small molecules and antibodies remain areas of long-term interest. Regarding therapeutic areas, oncology continues to hold a dominant position, and immunology maintains strong attention as a consistently robust field. However, we also observe concurrent advancements in antiviral and infectious diseases, central nervous system disorders, and metabolic diseases, indicating that differentiated disease-area strategies have become a prevailing trend. How to achieve differentiated, source-level innovation in popular sectors, and whether rapid breakthroughs can be made in therapeutic areas with unmet medical needs, are critical questions that biotech companies must address when engaging with investors and meeting ultimate clinical demands.

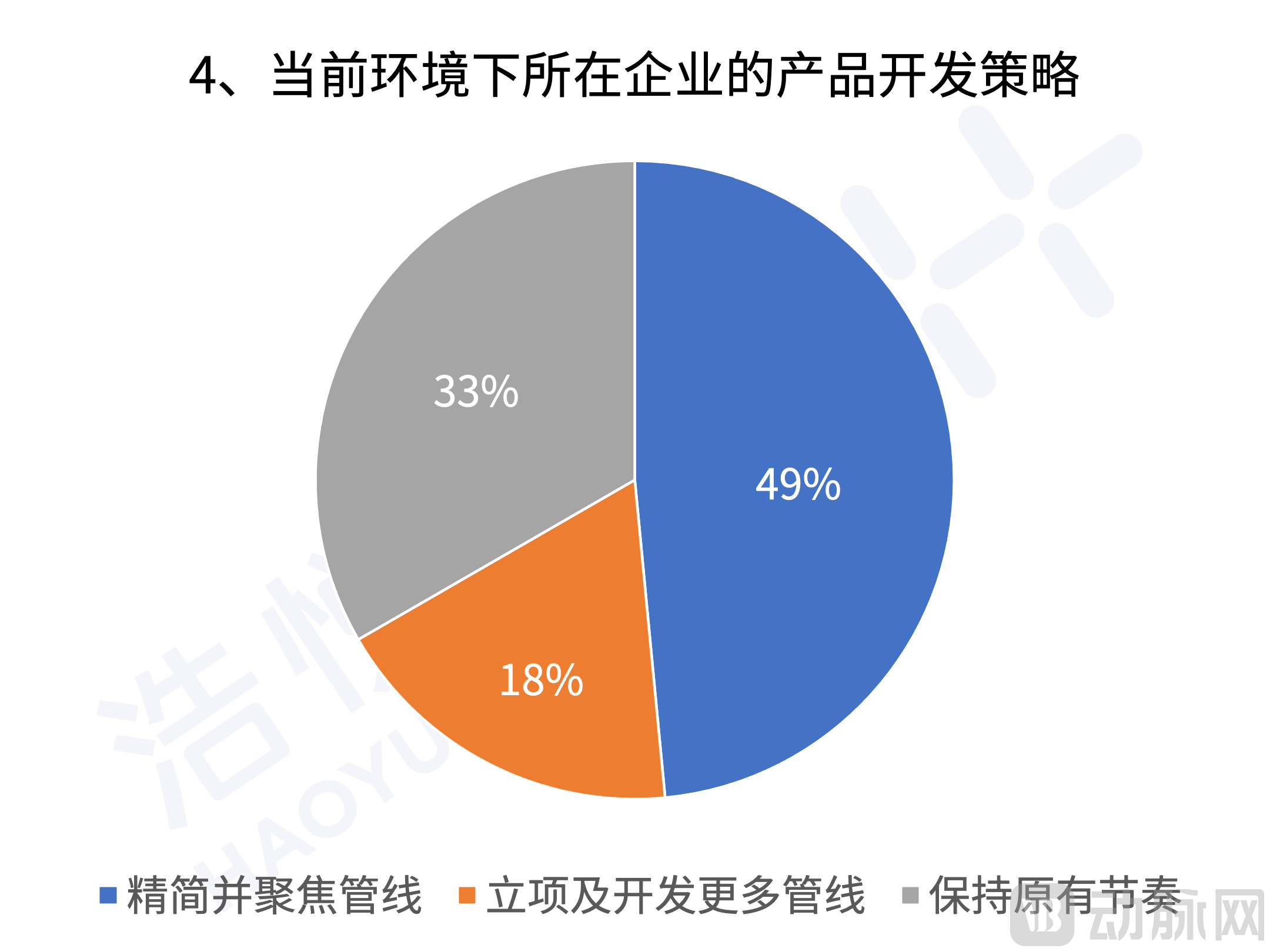

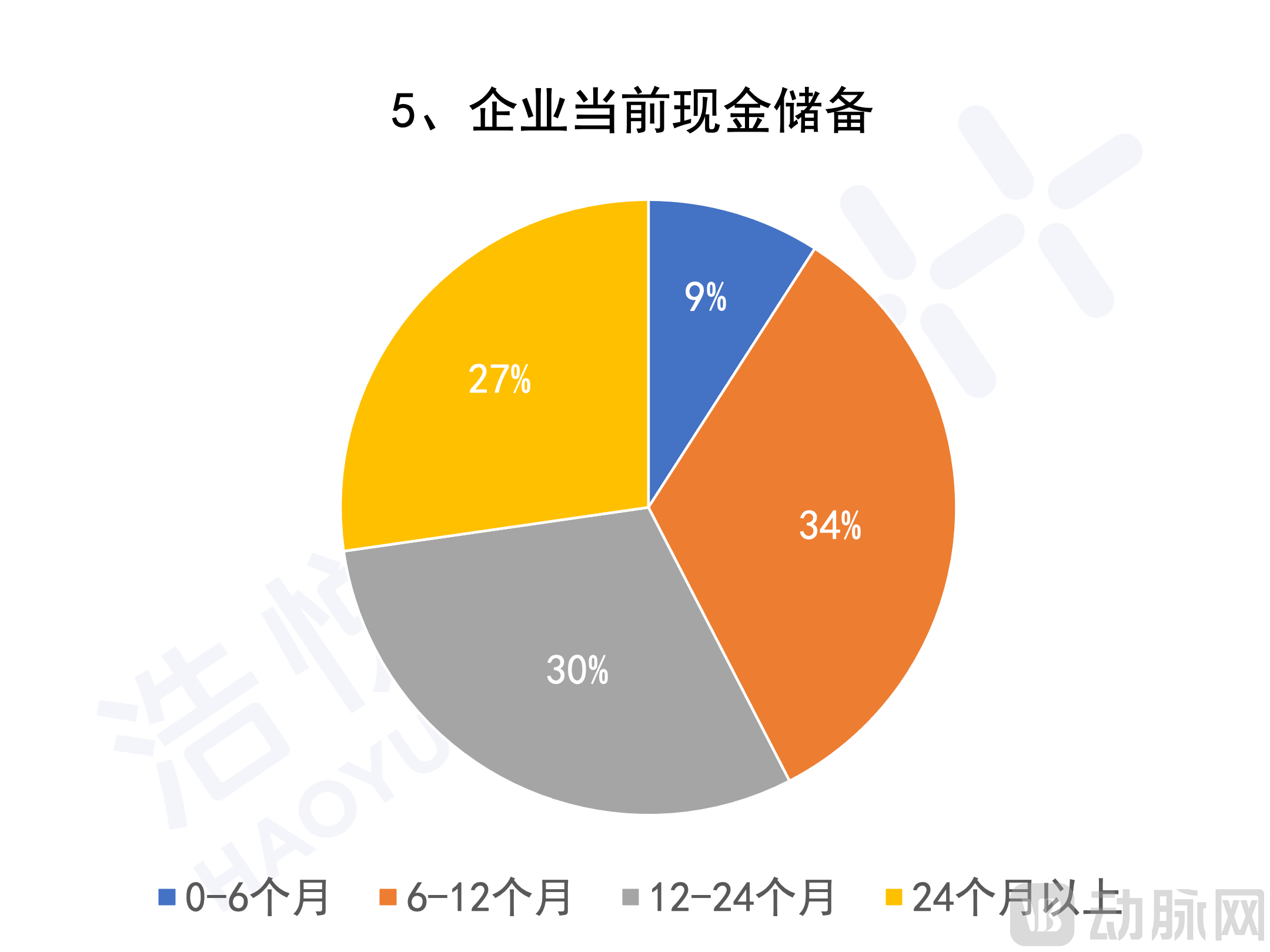

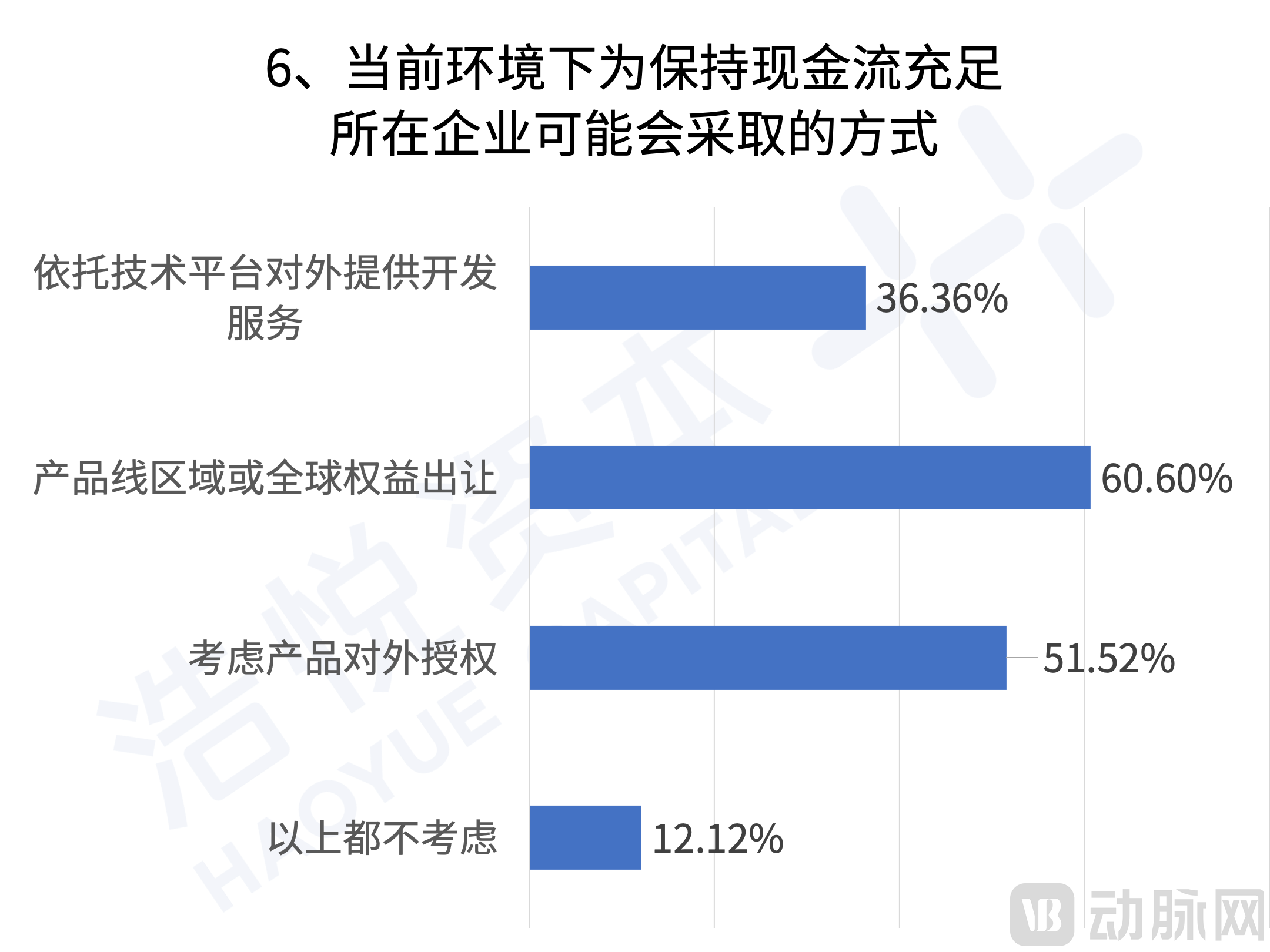

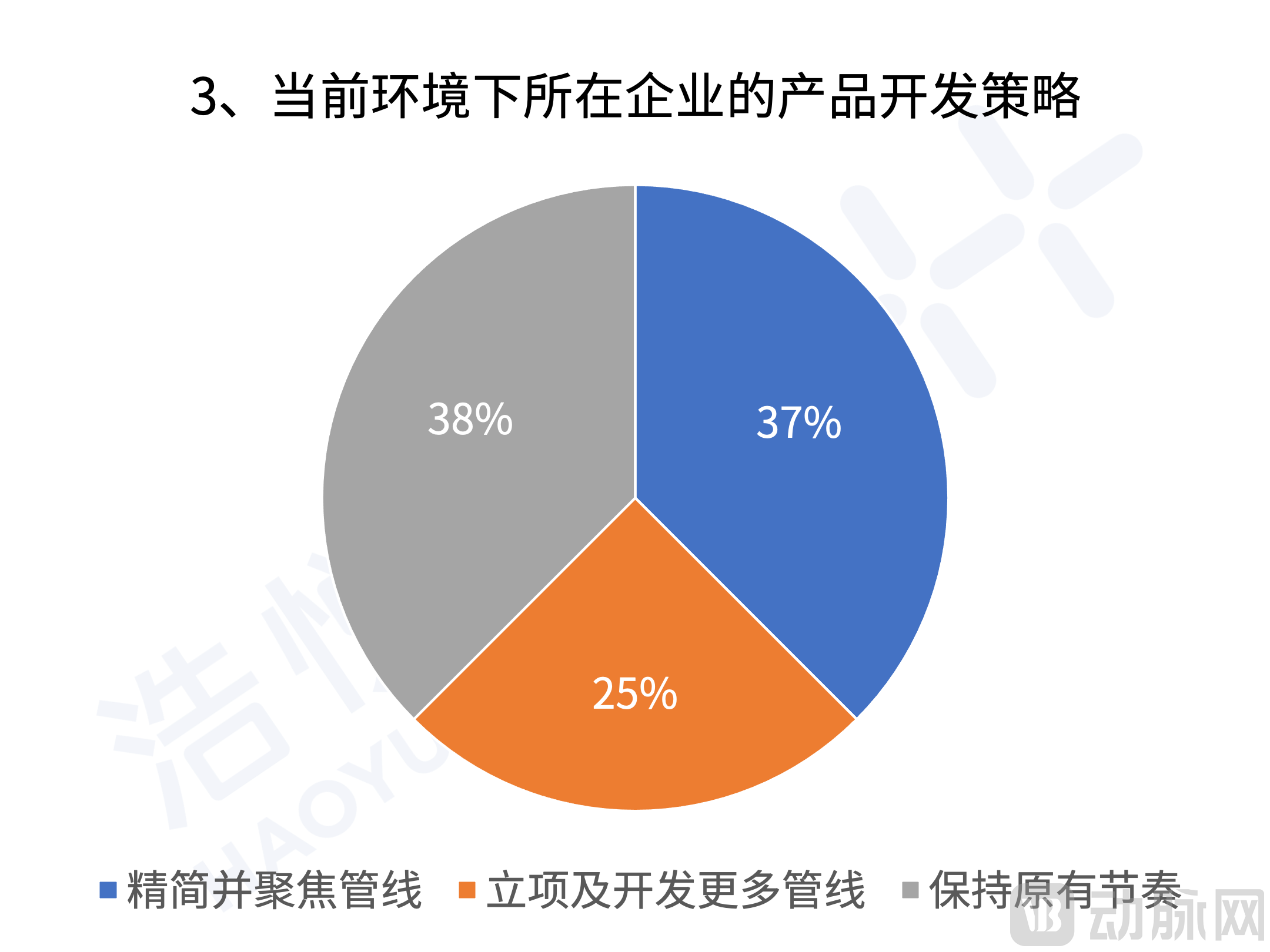

Despite ongoing market pressures, companies now possess a more thorough understanding of the market and are better prepared than in the past. Strengthening cash reserves, adopting a more steady and prudent R&D pace, and generating revenue through multiple channels have become a broad consensus among biotech firms. Nearly half of biotech companies have opted for a more focused approach in their product development strategies, concentrating resources on their most promising pipelines, while approximately one-third have decided to maintain their current R&D pace. Indeed, the pace of R&D is closely tied to a company’s cash reserves. Survey feedback indicates that although more than half of the companies have cash reserves lasting over 12 months, the majority still choose to maintain or even accelerate their fundraising efforts. Meanwhile, companies are placing greater emphasis on their own revenue-generating capabilities, embracing challenges and collaborations with a more open mindset. A combination of product equity partnerships, out-licensing, and technology development services leveraging their proprietary platforms serves not only as a crucial means of supplementing cash flow but also as a way to secure broader support and safeguards for the future commercialization of their products.

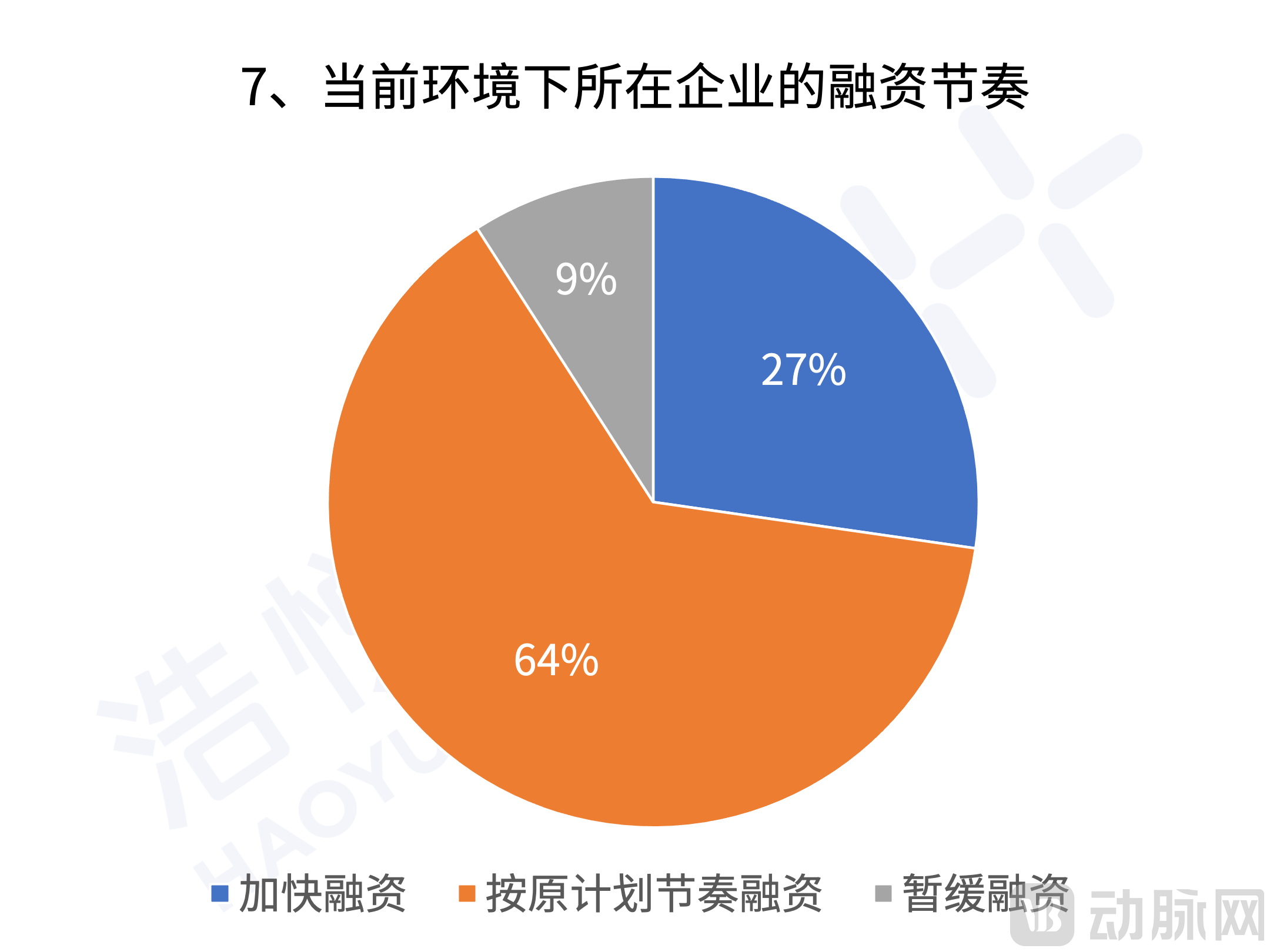

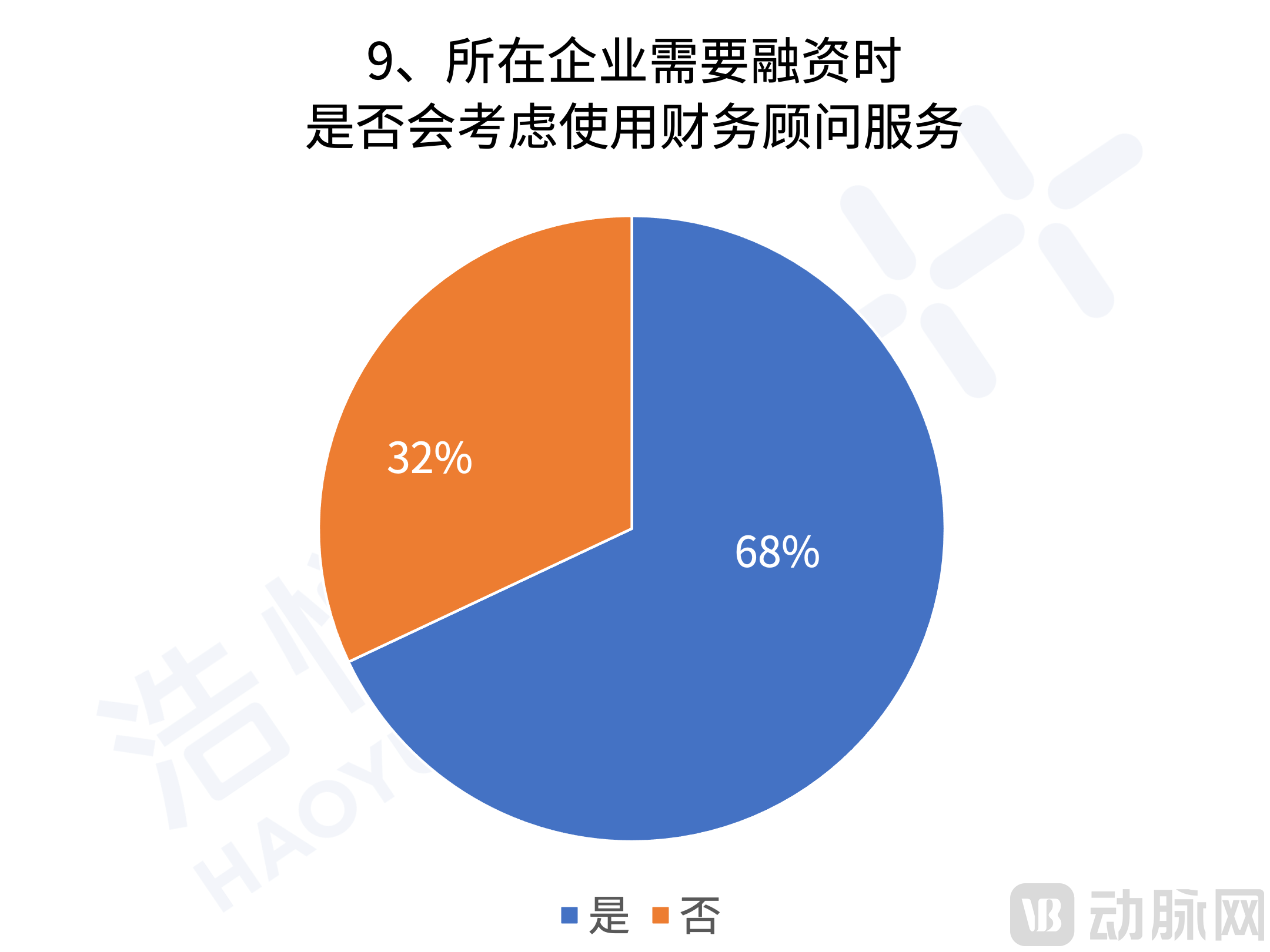

From the financing perspective, specialized division of labor within the industry is gradually taking shape. In terms of financing considerations, the funding amount has undoubtedly become the primary focus for enterprises, while the importance of speed and valuation goes without saying. For entrepreneurs, industrial resources are no less critical than these two factors, as they aim to leverage complementary advantages between startups and industrial partners. This synergy combines the specialized R&D capabilities of early-stage startups with the clinical resources and commercialization strengths of established industry players, achieving a “1+1>2” effect. Incorporating feedback from investors in the following section, their sincere advice to biotech companies is to maintain cash reserves, appropriately accelerate the pace of fundraising, and strengthen the cash safety cushion. The underlying reason is invariably the pressure from Limited Partners (LPs). In a rapidly changing market environment, accumulating sufficient resources is essential to weather the harsh winter and await the arrival of spring.

Pharma Section

As the cornerstone of innovation in the pharmaceutical industry, Pharma companies’ R&D strategies and portfolios have long attracted market attention. Survey feedback indicates that for most Pharma companies, key focus areas include cardiovascular and metabolic diseases, central nervous system (CNS) disorders, and infectious diseases. The number of companies active in these therapeutic areas even surpasses those in traditionally strong domains such as oncology and autoimmune diseases. These fields are representative of typical growth markets, characterized by widespread unmet patient needs. Reducing intense competition and zero-sum games in saturated markets, while jointly expanding into growth markets, has become a widely recognized R&D strategy within the industry. In terms of R&D direction, the vast majority of Pharma companies have established a solid foundation in small-molecule drugs. Building on this base, they continue to advance small-molecule drug development while extending their reach into emerging technology platforms, reflecting a clear trend in strategic portfolio allocation.

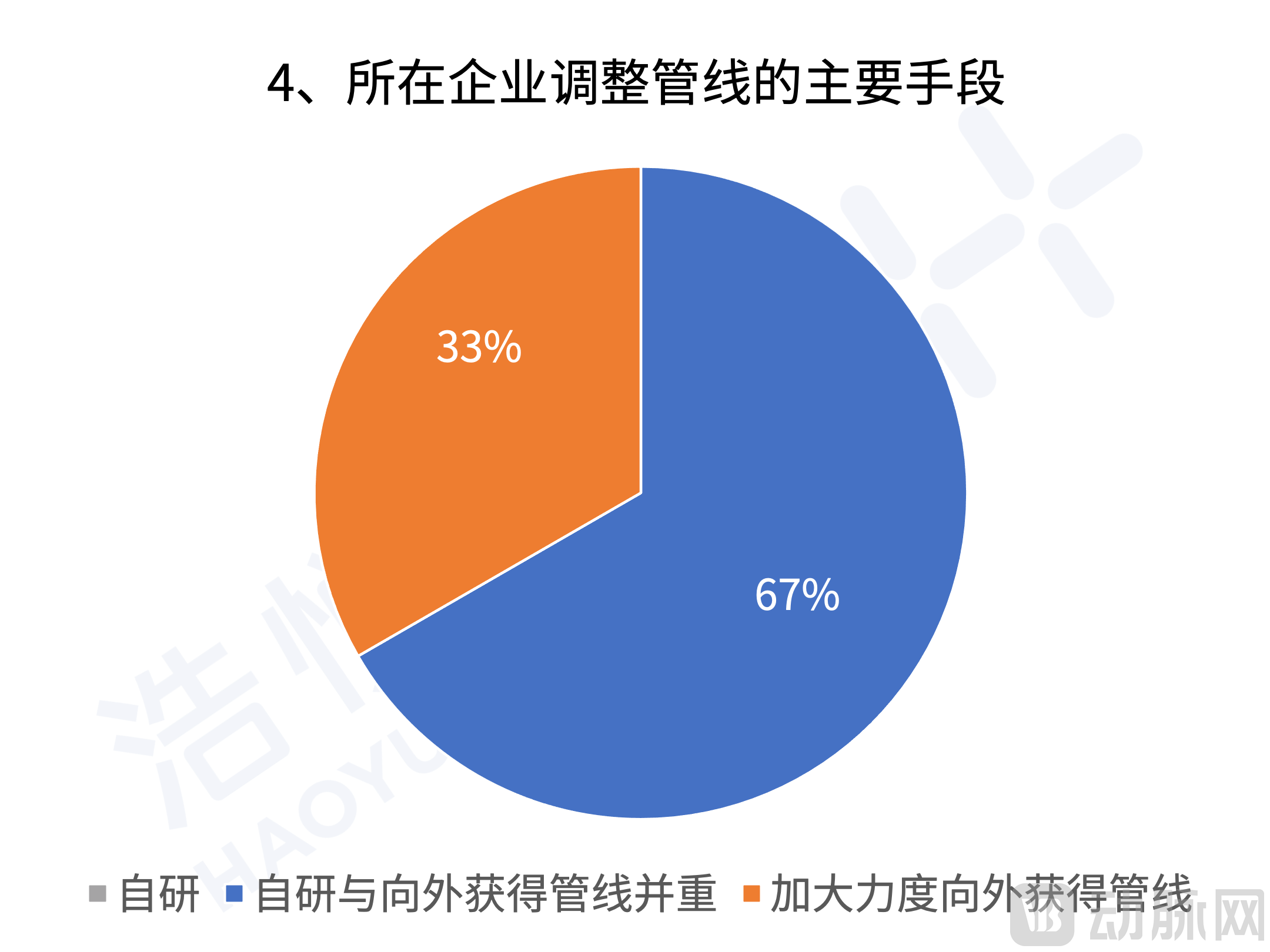

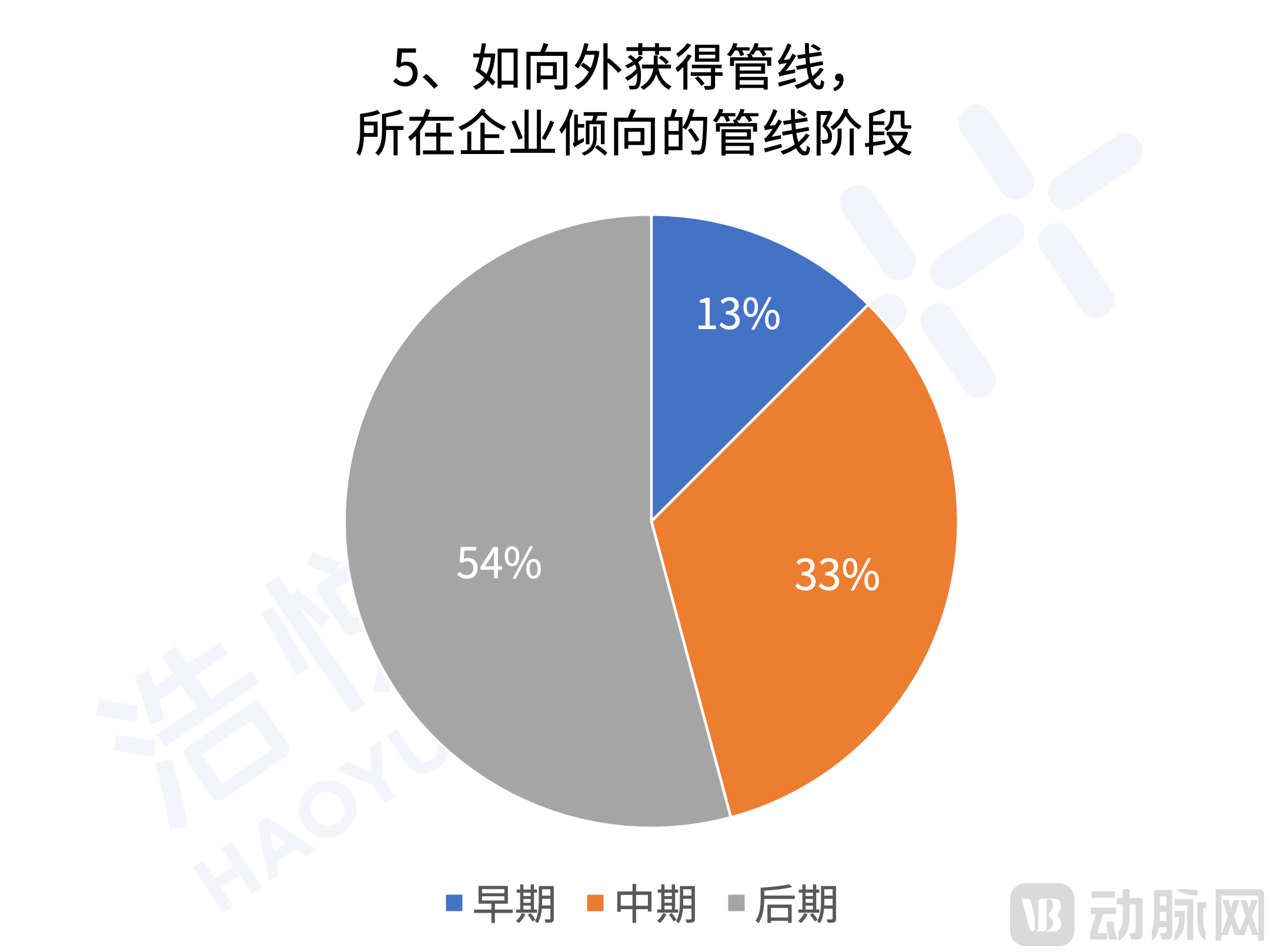

In terms of product development and introduction strategies, pharmaceutical companies vary due to their unique circumstances. However, overall, most large pharmaceutical companies (Pharma) have adopted more conservative and focused strategies in their product development approaches. Interestingly, unlike the R&D stages where most biotech companies are positioned, the majority of Pharma firms consistently choose mid-to-late stage pipelines when considering external acquisitions. What pharmaceutical companies need to evaluate is the optimal balance between internal R&D and external acquisition in terms of cost, speed, and product advantages. For Pharma companies, introducing late-stage pipelines (many after Phase II clinical trials) serves as a rapid supplement to potential commercializable product portfolios, helping to offset challenges such as volume-based procurement faced by existing products. This poses further challenges to the R&D capabilities of biotech firms. Whether they can concentrate resources to rapidly advance their leading products to the forefront of the industry and enter mid-to-late stage R&D largely determines their future opportunities and bargaining power in financing and collaborations with Pharma companies.

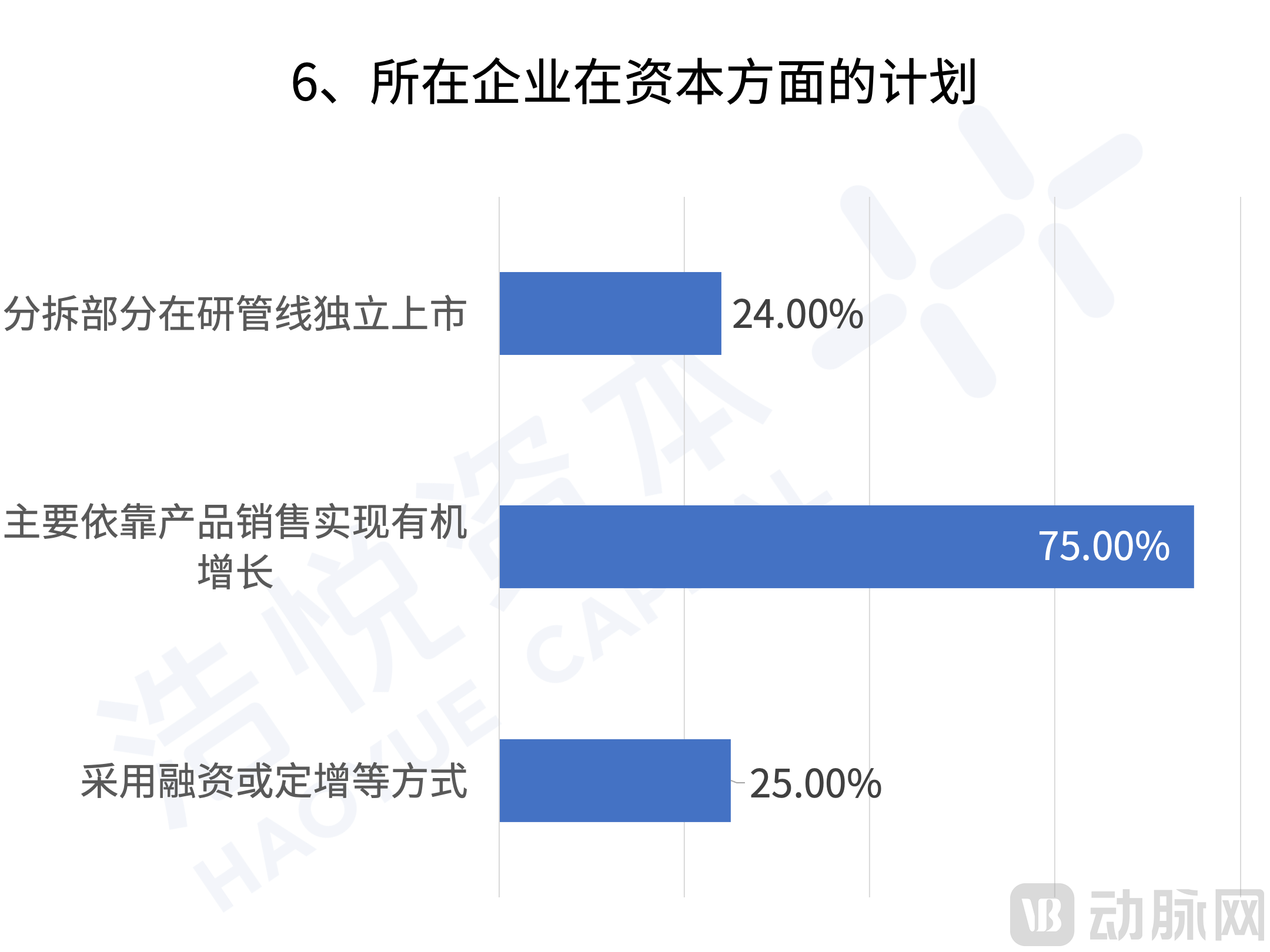

In terms of financing, for mature companies, emphasizing self-sustaining capabilities and strengthening product sales to achieve organic growth remains the preferred choice for most pharmaceutical companies. However, in the past two years, spin-off financing has become an option that more and more Pharma companies are considering. By unlocking the implicit value of assets through spin-offs, supplementing R&D funds is being accepted by an increasing number of pharmaceutical companies.

Investment Institutions

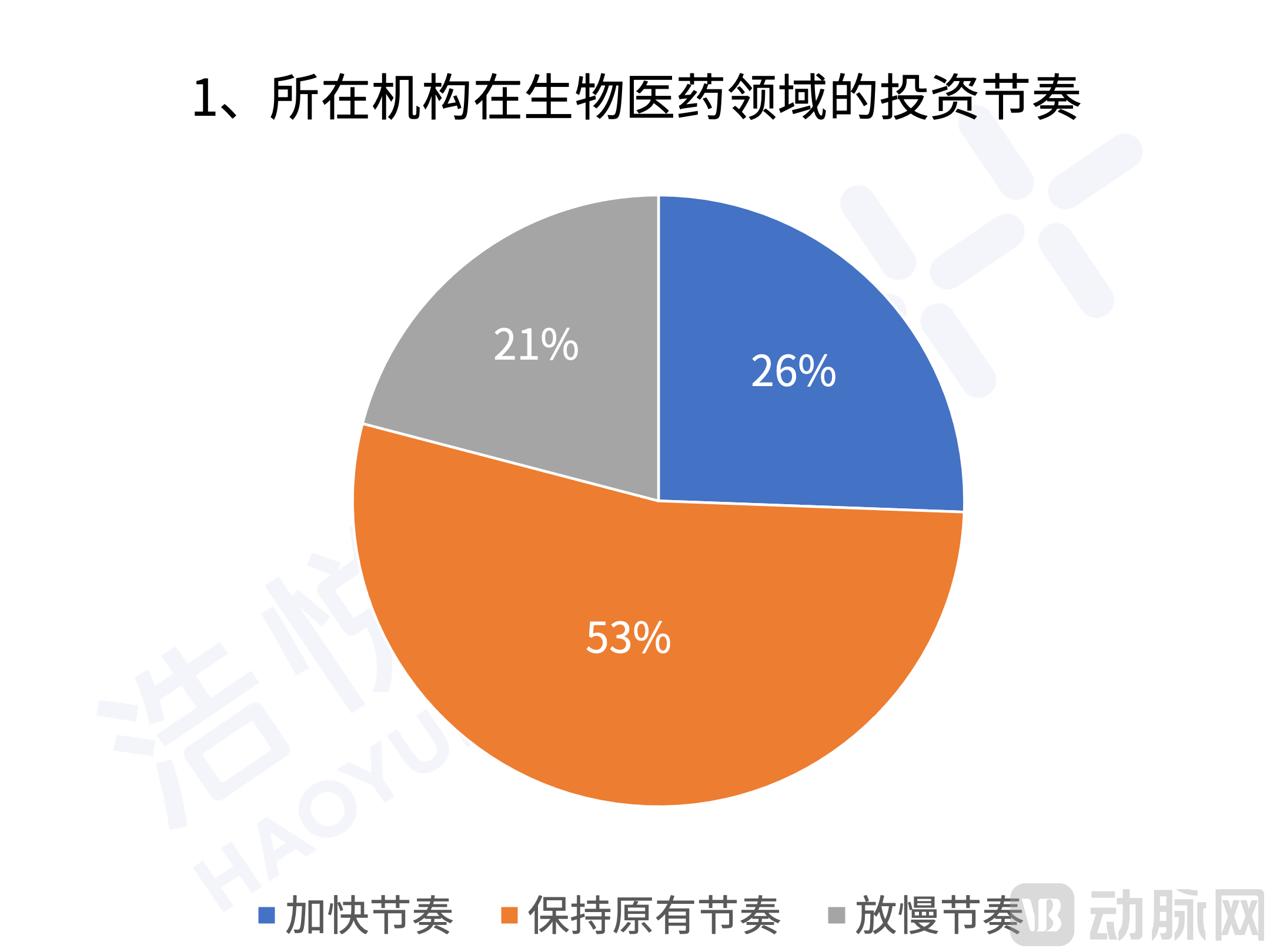

Following the turbulence and challenges of 2022, as social order recovered and restrictions were lifted, the pace of the investment market gradually returned to its familiar rhythm. Nearly 80% of investors plan to maintain or accelerate their investment pace in 2023.

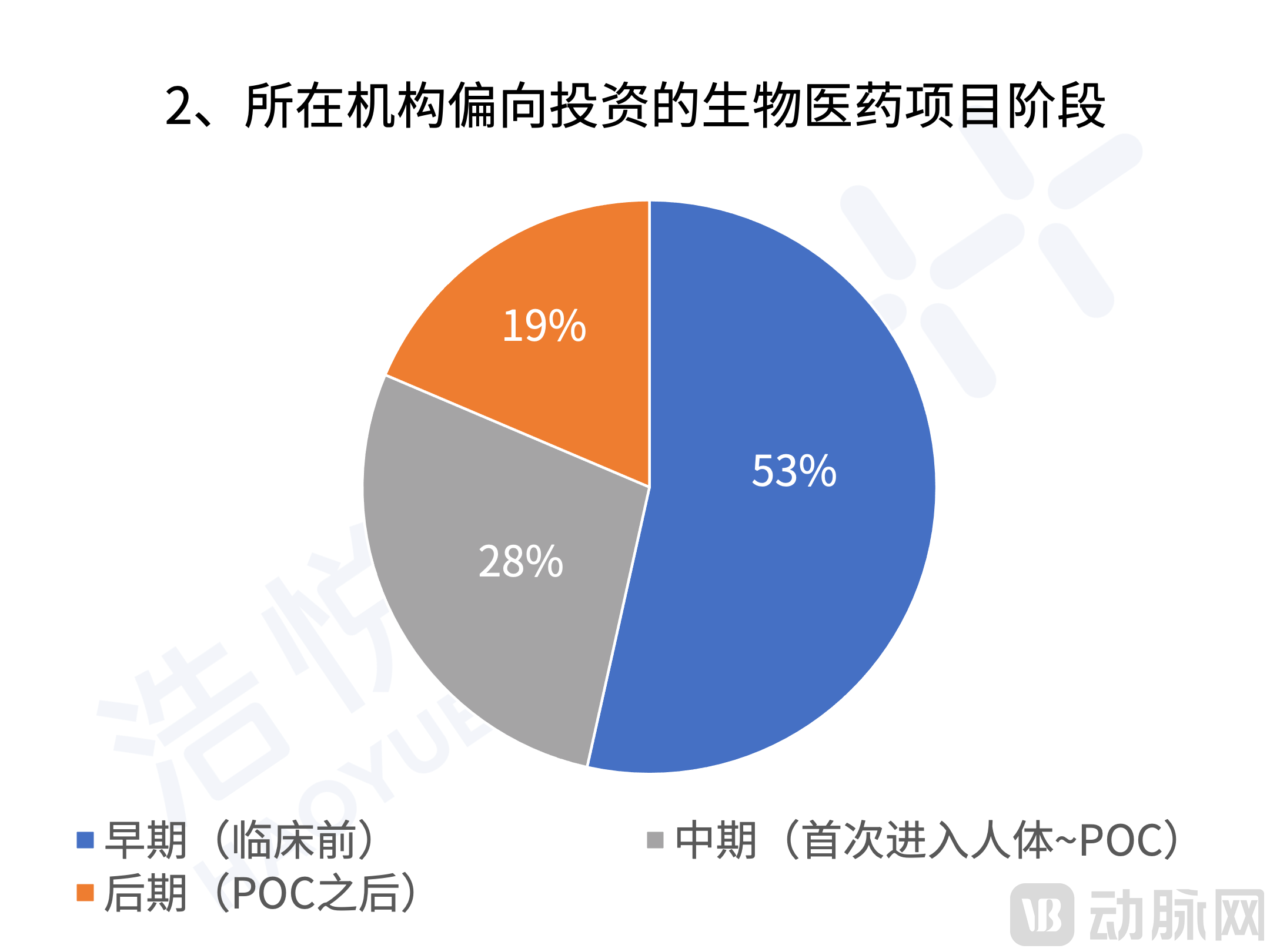

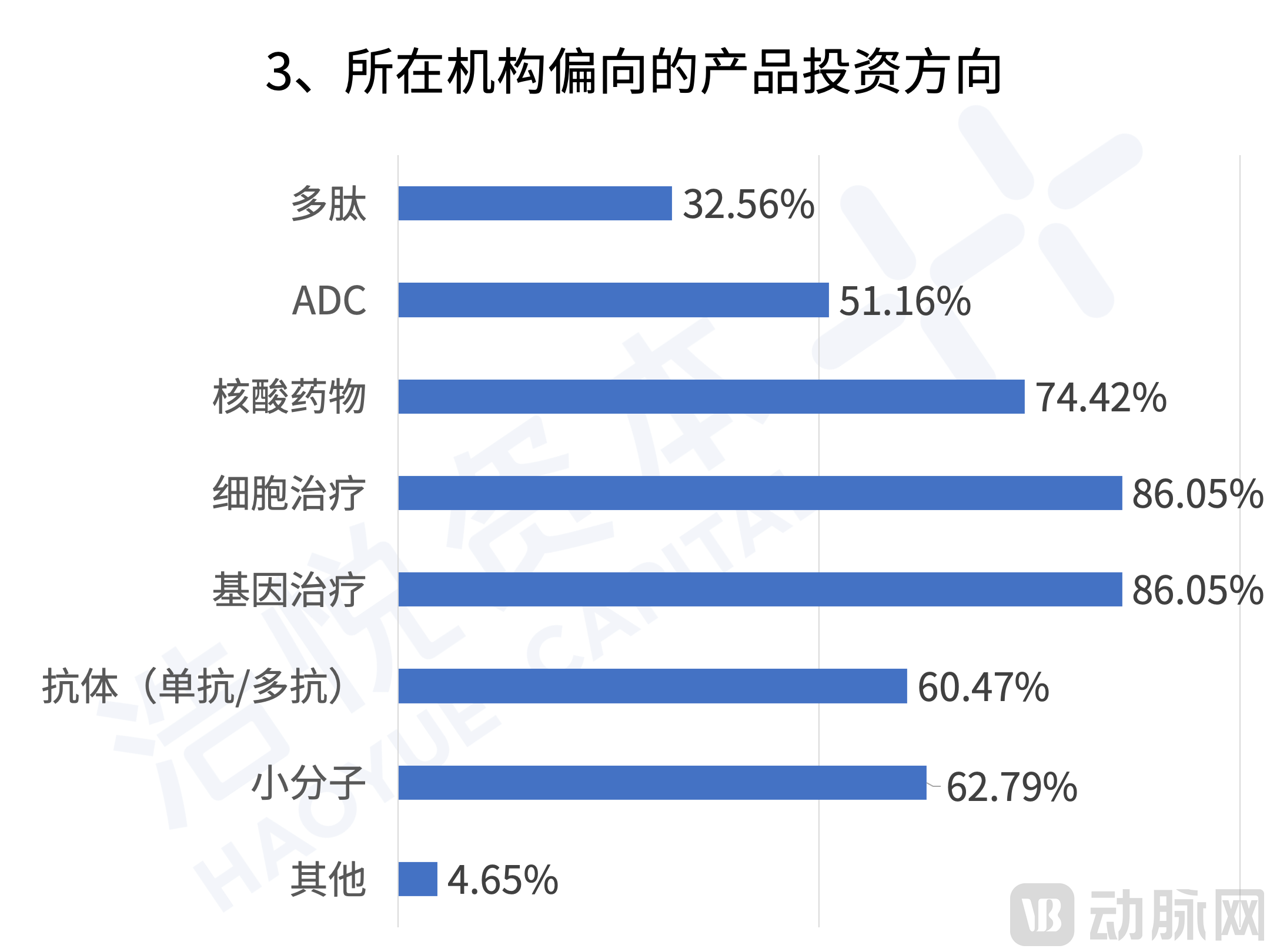

In terms of investment style, the dominant themes of early-stage and innovative investments are expected to continue in 2023. The majority of investors prefer early-to-mid stage opportunities (preclinical to proof-of-concept), which aligns closely with the development stages of numerous innovative therapies. Regarding sector allocation, cell and gene therapy (CGT) and nucleic acid-based therapies will remain industry hotspots, while small molecules, antibodies, and antibody-drug conjugates (ADCs) continue to attract investor attention. Upgrading and iterating on existing therapies to identify next-generation products is also a key strategic focus for investors.

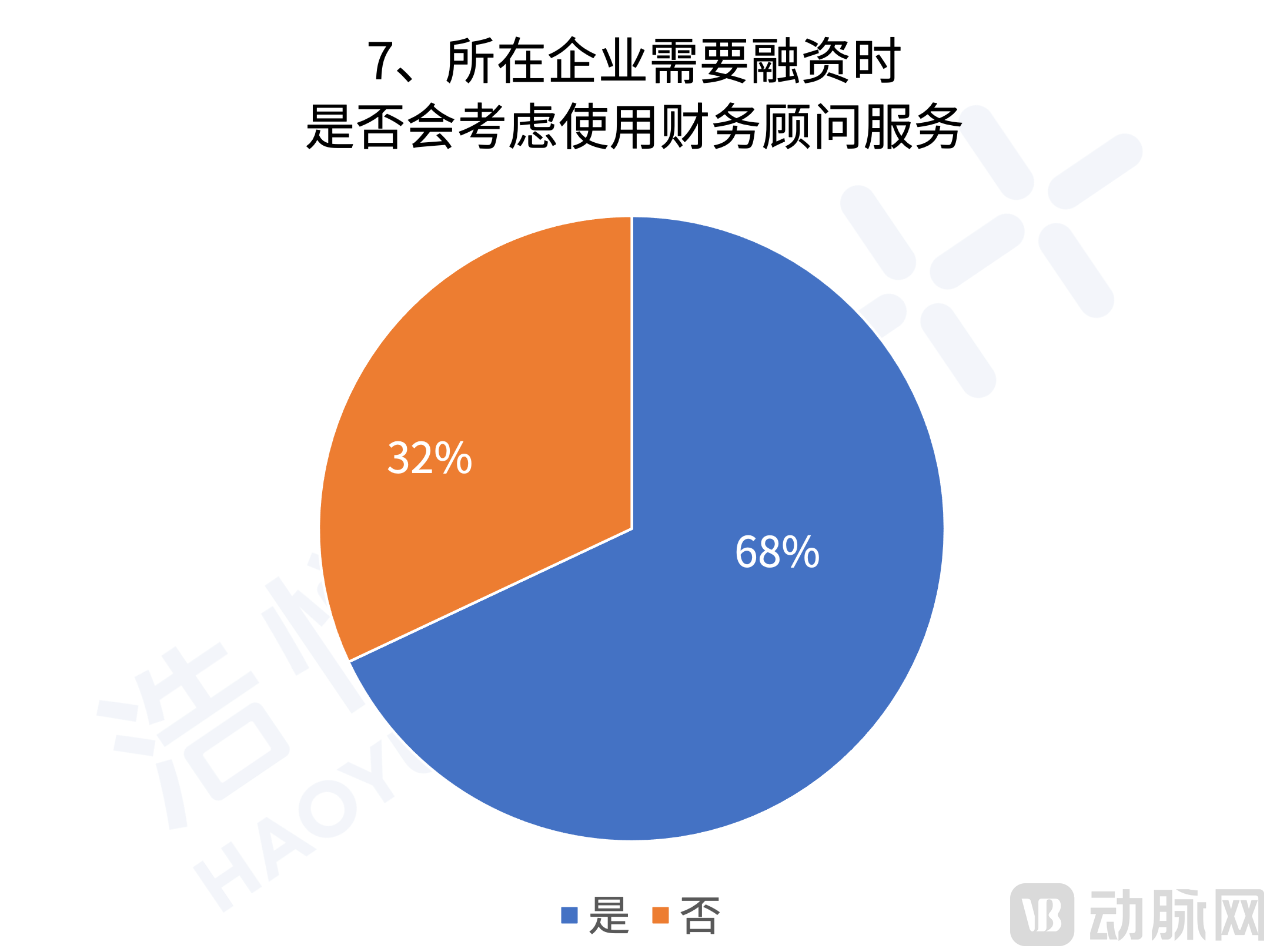

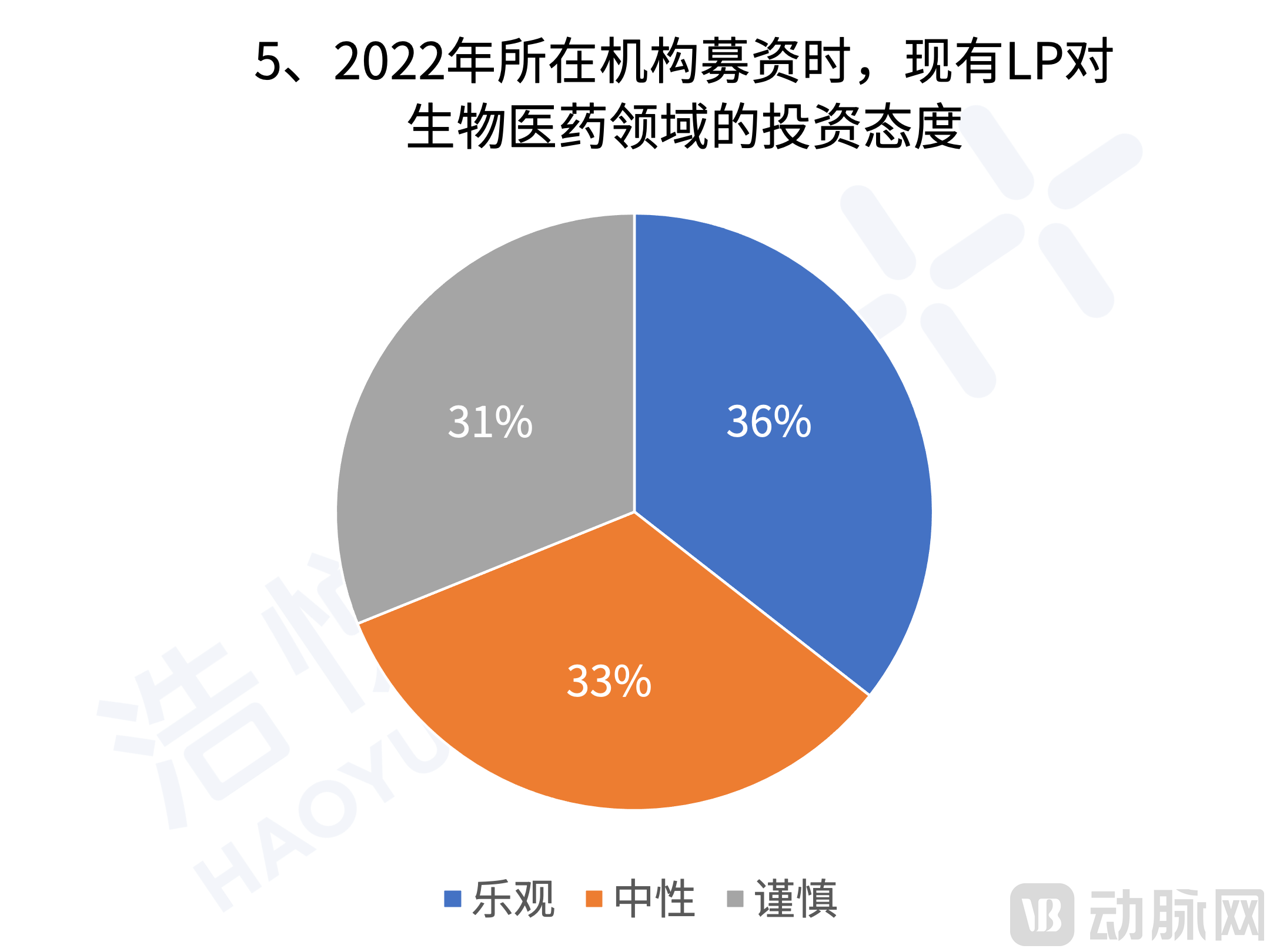

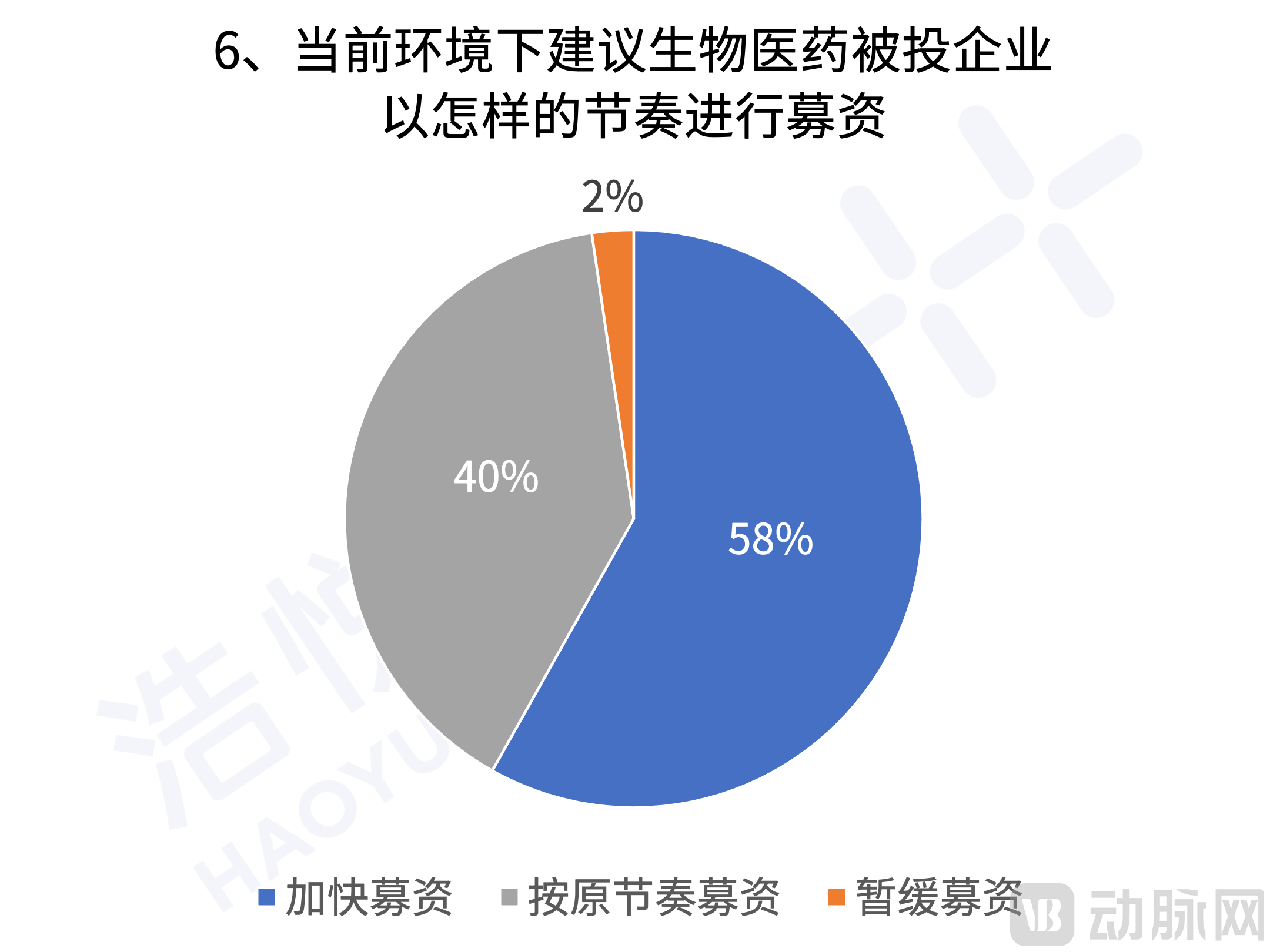

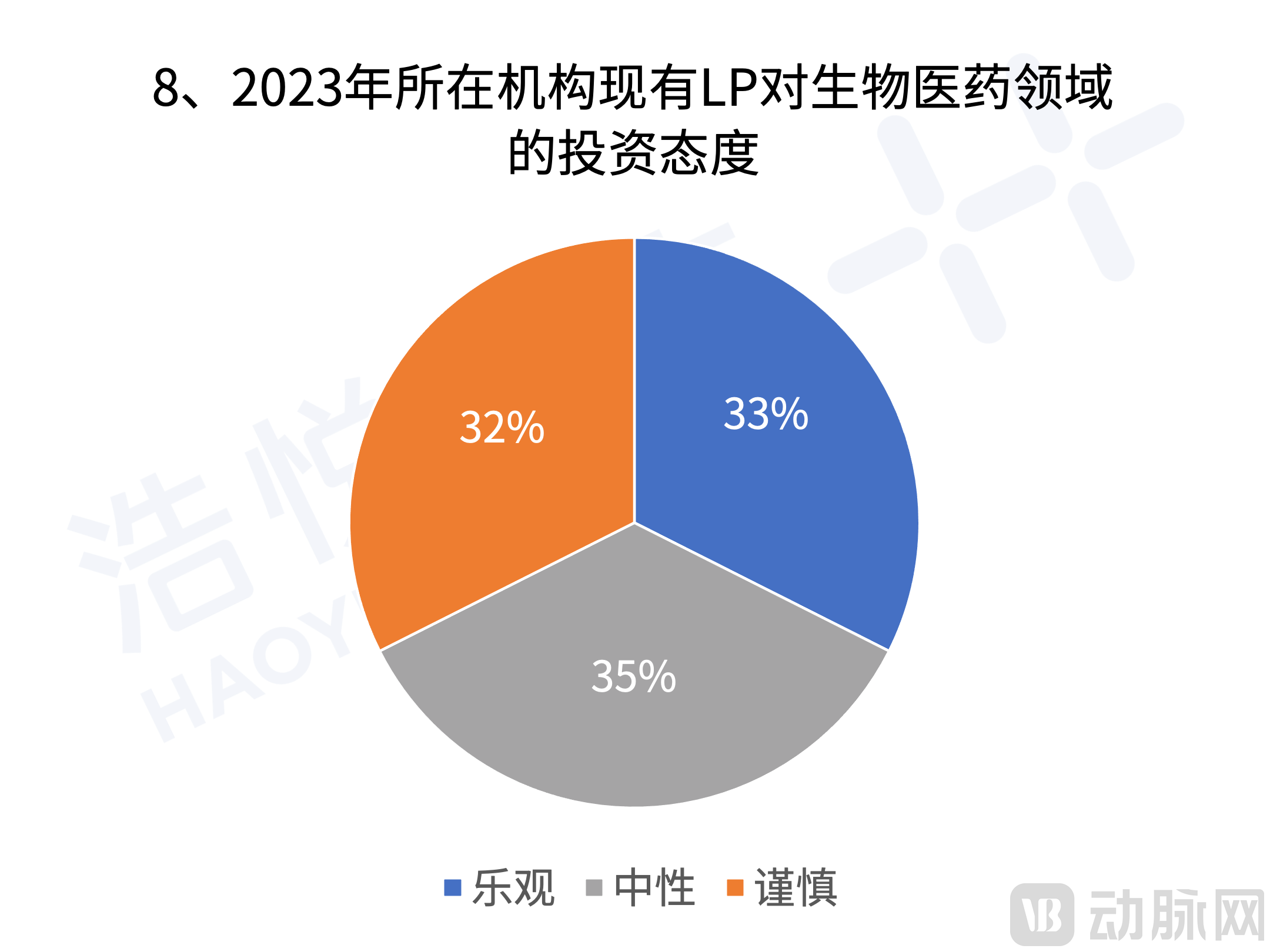

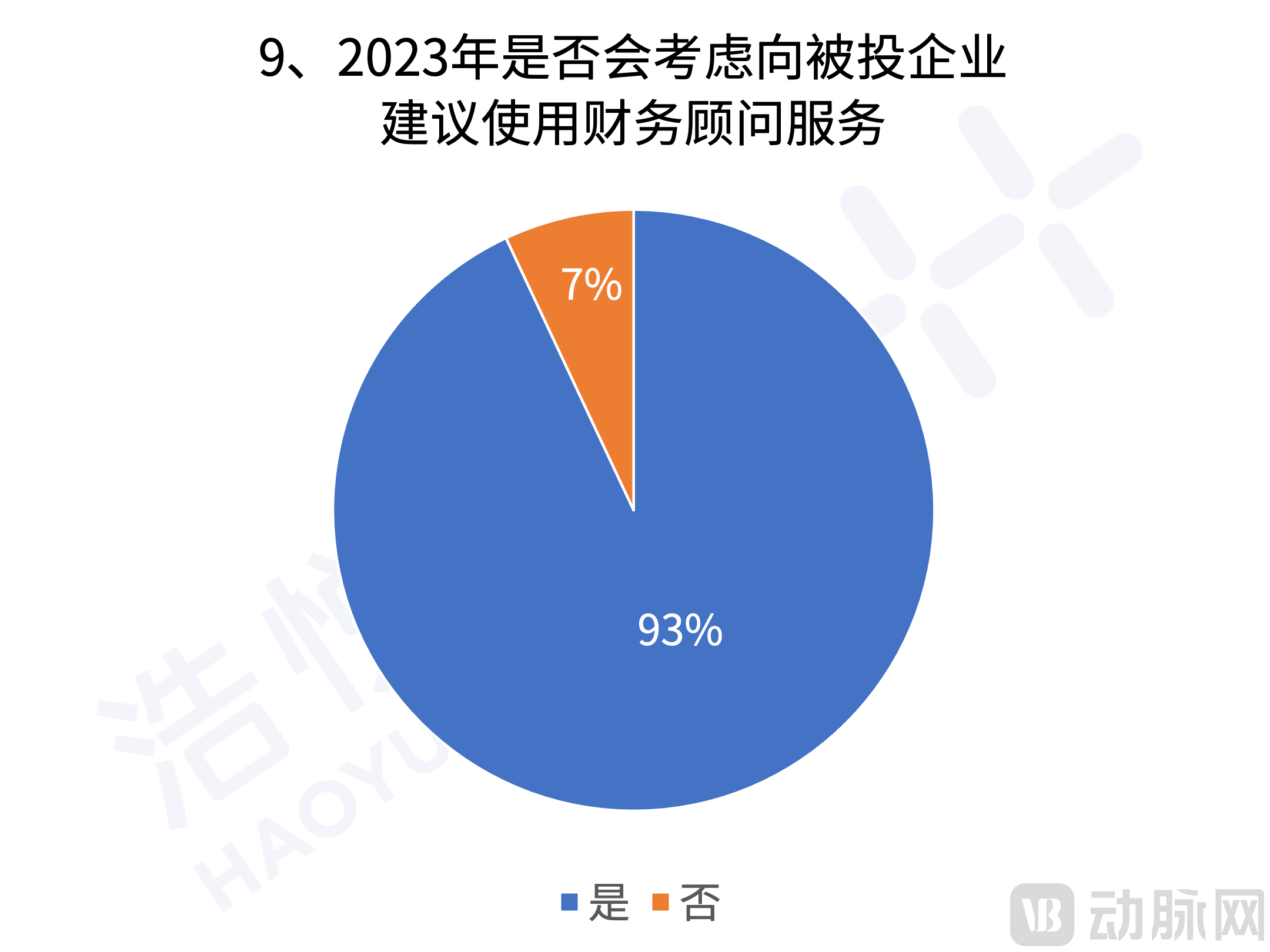

Some investors face cautious attitudes from LPs toward the biopharmaceutical sector during fundraising, with higher screening standards leading to longer investment cycles. However, for companies, the amount and speed of financing are their lifelines; therefore, leveraging professional services to accelerate fundraising is a sincere recommendation from investors to Biotech enterprises.

Conclusion

Having weathered the storm, we can still shape the future. Despite the myriad challenges of 2022, the market has emerged more rational and focused on fundamentals. Products with genuine clinical, commercial, and market value will attract capital attention; companies with differentiated competitive advantages, strong commercialization capabilities, and international growth potential will enjoy broader prospects for development.

As market dynamics shift, the investment approach of traditional pure financial investors will gradually evolve toward collaboration with capital partners possessing industrial backgrounds. Meanwhile, a significant number of Biotech companies will mutually seek partnerships with powerful Pharma companies that are active in the Chinese market. The deep collaboration among Biotech firms, Pharma companies, and Venture Capital (VC) investors has officially ushered in a new era of development and prosperity for China’s biopharmaceutical industry. At this critical juncture, Haoyue Capital is committed to joining hands with outstanding healthcare enterprises and investors, leveraging professional investment strategies to help companies achieve leapfrog growth opportunities and jointly shape a new landscape for China’s broader health industry!