China Proposes Export Restrictions on Synthetic Biology and Gene Editing Technologies in Revised Technical Control Catalog

On December 30, 2022, the Ministry of Commerce released the draft for public comments on the newly revised Catalogue of Technologies Prohibited or Restricted from Export in China (hereinafter referred to as the “Catalogue”).

This catalog has stirred up a storm, sparking widespread discussion.

Because seven new technologies have been added to the catalog, namely: photovoltaic silicon wafer fabrication technology, LiDAR systems, human cell cloning and gene editing technology, CRISPR gene editing technology, synthetic biology technology, hybrid vigor utilization technology for crops, and bulk material handling and conveying technology.

Among these, gene editing and synthetic biology have emerged as hot investment trends in recent years, with dozens of domestic companies securing financing in these two sectors. As frontier technologies, gene editing and synthetic biology are also focal points of global technological competition, with the United States having previously imposed technical restrictions in these two fields.

Does the release of the catalog signal an escalation in technological countermeasures? Will export restrictions cool investment in these two major sectors? What is the magnitude of the impact on gene editing and synthetic biology companies? These topics have become the focal point of industry discussions. VCBeat (WeChat ID: vcbeat) interviewed industry insiders to address these two key questions.

Although the export restriction policy is currently still in the draft-for-comments stage, its implementation could disrupt the export markets for domestic synthetic biology and gene-editing companies.

In comparison, the industrialization of synthetic biology technology is more mature and may be subject to greater impact. Judging from the performance of synthetic biology companies that have already achieved commercial success, overseas market revenue accounts for a significant proportion.

Taking Cathay Biotech as an example, Cathay Biotech is a company that leverages biotechnology to implement revolutionary industrial-scale production technologies for bio-based pentamethylenediamine, bio-based polyamides, long-chain dibasic acids, and bio-butanol. According to its annual report, in 2021, Cathay Biotech generated RMB 9.9 billion in overseas revenue and RMB 12.0 billion in domestic revenue.

Another listed synthetic biology company, Huaheng Biotechnology, is primarily engaged in the research and development, production, and sales of amino acids and their derivatives. Its main products include alanine series (L-alanine, DL-alanine, β-alanine), D-calcium pantothenate, and α-arbutin. In 2019, overseas business accounted for 55.74% of Huaheng Biotechnology’s total revenue. In 2021, the company’s overseas sales continued to grow and remained significant, representing 47.38% of its total operating revenue.

Data disclosed in the prospectus of Shanghai Yikelai Biotechnology, a platform-based enterprise in synthetic biology, showed that its overseas revenue in 2021 amounted to RMB 23.1293 million, accounting for 6.99% of the total.

Will the implementation of the catalog impact companies with a high proportion of overseas revenue? Based on the full text of the catalog, the answer is that even if the policy is implemented, the impact on the aforementioned synthetic biology companies will be limited.

The scope of restrictions on synthetic biology in the Catalogue of Technologies Prohibited or Restricted from Export covers key technologies such as efficient DNA synthesis and assembly, directed evolution, and cell factory creation, as well as synthesis technologies for major chemicals including amino acids, proteins, and starch.

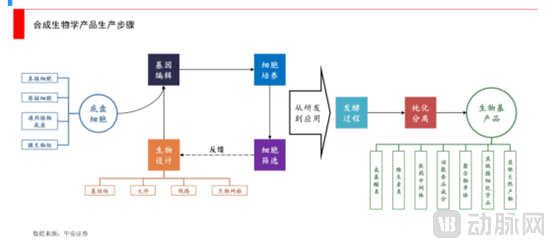

From the perspective of synthetic biology product manufacturing steps, the technologies restricted from export in the catalog are predominantly cell factory technologies at the R&D stage. Although Cathay Biotech and Huaheng Biotechnology derive a significant portion of their revenue from overseas markets, their core competencies lie in large-scale production, specifically in downstream processes such as fermentation.

For companies building “cell factories,” the impact of export restrictions is more evident in the long term, as domestic enterprises currently remain focused on the Chinese market.

For gene editing companies, the scope of restrictions in the catalog pertains to the application of gene editing in ethically controversial areas, including its use in embryonic cells, oocytes, sperm cells, and research that could result in significant harmful consequences.

Current gene editing in the human body is divided into two directions: one is editing patients' somatic cells to treat diseases, and the other is editing germ cells (i.e., sperm, egg cells, or fertilized eggs) with the aim of preventing certain genetic diseases or enhancing specific functions.

These two applications differ significantly. Somatic cell modification is used to treat patients, with therapies designed to affect only the treated individual and not their offspring. In contrast, genomic changes occurring during or after embryogenesis can be found in some or all of the child’s cells, including the germline. Unlike somatic editing, germline-edited humans can pass these modifications on to their descendants; therefore, this gene-editing technique is not employed due to the potential risk of contaminating the human gene pool.

Most gene-editing companies focus on editing patients’ somatic cells to treat diseases, without involving germline cell editing.

In addition to ethical controversies, gene editing of germline cells also presents technical concerns. Currently, gene editing technologies still face challenges related to side effects such as off-target effects and potential immune responses. In the clinical application of gene editing technologies, regulatory agencies such as the FDA and NMPA are most concerned about off-target risks, explicitly requiring that off-target effects in clinical gene editing products be minimized to the lowest possible level.

Gene editing and synthetic biology are at the forefront of research across multiple fields worldwide. The third-generation gene-editing technology, CRISPR/Cas, is widely employed as a gene-editing tool in areas such as synthetic biology, metabolic engineering, and medical research. Meanwhile, synthetic biology is gradually replacing traditional chemical synthesis to become a key approach for “green synthesis” in global industries including pharmaceuticals, food, and materials.

These two major technologies play a crucial role in the development of emerging industries and represent the primary focus of strategic emerging industries across nations. They are of great significance for seizing the commanding heights of the new round of scientific and technological revolution and industrial transformation, accelerating the growth of new industries, fostering the new economy, and cultivating new drivers of economic growth.

To secure its position at the forefront of industry and maintain its leadership in technology, science, and other fields, the United States has implemented a series of control measures targeting China’s high-tech sector. On November 19, 2018, the U.S. Department of Commerce’s Bureau of Industry and Security (BIS) issued an export control framework for critical technologies and related products, with biotechnology—including synthetic biology—listed as the first controlled area. According to official data released by the BIS, the value of U.S. advanced biotechnology exports to China declined from $2.285 billion in 2019 to $1.851 billion in 2020, representing a 19% drop. The U.S. Innovation and Competition Act of 2021 designated synthetic biology, biotechnology, and genomics as critical technology areas.

Are the newly issued domestic policies aimed at preventing the outflow of key technologies and securing a commanding position in gene editing and synthetic biology?

Currently, from the perspective of technological gaps, the disparity between China and the United States in the fields of synthetic biology and gene editing is not significant. China is not lagging behind in these two areas.

In the field of gene editing, China’s technological capabilities are advanced in certain high-end areas, but have not surpassed global leaders overall.

Domestic companies have also independently developed gene-editing tools. Taking Huida Gene as an example, its self-developed gene-editing tools have been granted patents by the United States Patent and Trademark Office.

The primary gap between China and the United States in gene editing lies in clinical applications. In China, many companies are overly constrained to monogenic hereditary diseases and rare diseases in their clinical translation efforts. In contrast, their U.S. counterparts have a broader selection of therapeutic indications and greater experience. Furthermore, the raw materials for manufacturing gene-editing drugs in China currently rely heavily on imports, resulting in higher costs.

In the field of synthetic biology, which is still in its nascent stage, China has maintained a level of development commensurate with international standards. Driven by advances in synthetic biology disciplines and technologies, China’s biomanufacturing industry has experienced rapid growth. Technological upgrades for traditional products such as amino acids and vitamins are continuously advancing, with partial breakthroughs in patent barriers achieved for certain key products. In cutting-edge research areas that will shape future industrial layouts, including novel pathway design and gene editing, China generally remains on par with global counterparts.

China’s greatest advantage in the field of synthetic biology lies in its complete biomanufacturing industry chain. Today, China has become one of the world’s largest suppliers of fine chemicals, and it is expected that the global high-end fine chemicals industry will further shift toward and concentrate in China in the future. With a large number of downstream manufacturing enterprises, China holds a distinct advantage over U.S. synthetic biology companies. Startups can more easily identify market demands and secure customers.

These two technologies also command a substantial presence in the domestic Chinese market. In terms of market size, the “13th Five-Year Plan” for the Development of the Bioindustry pointed out that since the “12th Five-Year Plan” period, China’s bioindustry has achieved a compound annual growth rate of over 15%. By 2015, the industry’s scale exceeded RMB 3.5 trillion, reaching levels comparable to those of developed countries in certain sectors and even demonstrating certain competitive advantages.

From a policy perspective, the Chinese government is vigorously promoting the development of synthetic biology technology. In 2021, “carbon peaking” and “carbon neutrality” were included in the Government Work Report for the first time during the Two Sessions. Synthetic biology technology achieves the goal of large-scale production of high-value products from simple raw materials (such as glucose and glycerol) by redesigning and technologically transforming biological systems—including enzymes, synthetic pathways, or cells—to create biological systems with novel functions, thereby reducing carbon dioxide emissions and minimizing environmental pollution. The 14th Five-Year Plan for Bioeconomy Development explicitly states that innovation in synthetic biology technology should be promoted, and its application should be advanced in an orderly manner in fields such as new drug development, disease treatment, agricultural production, substance synthesis, environmental protection, energy supply, and new material development.

Synthetic biology will be one of the key areas prioritized for development and support by national and local governments in the future. Guided by the national medium- to long-term strategy of carbon neutrality, synthetic biology has the potential to bring about genuine transformation to society and industry.

In the primary investment market, synthetic biology and gene editing are hotspots of attention.

According to statistics from the U.S. synthetic biology media outlet Synbiobeta, investment and financing in the synthetic biology sector reached a record high in 2021, with global startups in the field raising a total of $18 billion—nearly equivalent to the combined investment and financing totals for the entire period from 2009 to 2020.

In 2022, despite the overall cooling of industry-wide financing, the field of synthetic biology still witnessed significant large-scale funding rounds. The gene editing sector likewise maintained its momentum; one investor noted that in both China and the United States, a new gene editing company emerges every two to three months, each securing substantial financing and boasting a prestigious team of experts.

How Will the Draft Guidelines Affect Investment Trends? VCBeat Consulted Multiple Investors in Gene Editing and Synthetic Biology, Most of Whom Indicated That the Impact Would Be Limited, as the Domestic Market Already Offers Ample Room for Growth.

Drawing on the development of the semiconductor industry, competition over the global supply chain is inevitable; only by mastering core technologies can one maintain greater composure in technological competition.

References:

Shanghai Yikolai Bio's IPO Prospectus

The U.S.-China Biotech Rivalry: What Are the Opportunities for Synthetic Biology Startups? | A Dialogue with FreeS Fund

How Can Chinese Companies Seize Market Opportunities in Gene Editing Innovation? — Weiming Sci-Tech