Domestic Innovation Rises as Energy-Based Aesthetic Device Sector Poised for Breakout: 'White Paper on Energy-Based Aesthetic Devices' Released

Fumeilei Medical

R&D Developer of Medical Aesthetic Devices

People’s unending pursuit of beauty has fueled the rise of the “appearance economy,” placing the medical aesthetics industry squarely in the spotlight in recent years.

Data does not lie. On the demand side, the number of medical aesthetics users in China has continued to rise, surpassing 20 million in 2022 (data from SoYoung Data Research Institute), which is more than three times the figure in 2017. Among these users, not only are an increasing number of women opting for cosmetic surgery and anti-aging treatments, but men are also actively engaging in medical aesthetic procedures. Meanwhile, younger generations, particularly those born in the 1990s and 2000s, have become the “main force.”

On the supply side, an increasing variety of new devices and materials is driving rapid industry growth. Within this process, non-surgical medical aesthetics (commonly referred to as “light” medical aesthetics) has witnessed the fastest growth. According to Frost & Sullivan data, in China’s medical aesthetics market in 2021, non-surgical procedures grew by 26.4%, outpacing the 17.9% growth rate for surgical procedures.

▲Source: Frost & Sullivan, compiled by VCBeat.

Among these, energy-based medical aesthetic devices, as an important subsector of non-surgical aesthetics, are gaining increasing consumer favor and demonstrating high explosive growth potential.

· First, energy-based medical aesthetic devices are gaining immense popularity among young consumers due to their inherent advantages, including minimal invasiveness, rapid recovery, and low risk. According to the “2021 Report on Consumption Trends in Medical Aesthetic Anti-Aging in China,” consumers opting for energy-based treatments accounted for as high as 86.23% of the non-surgical medical aesthetics market, with this proportion continuing to rise, thereby steadily expanding the market space.

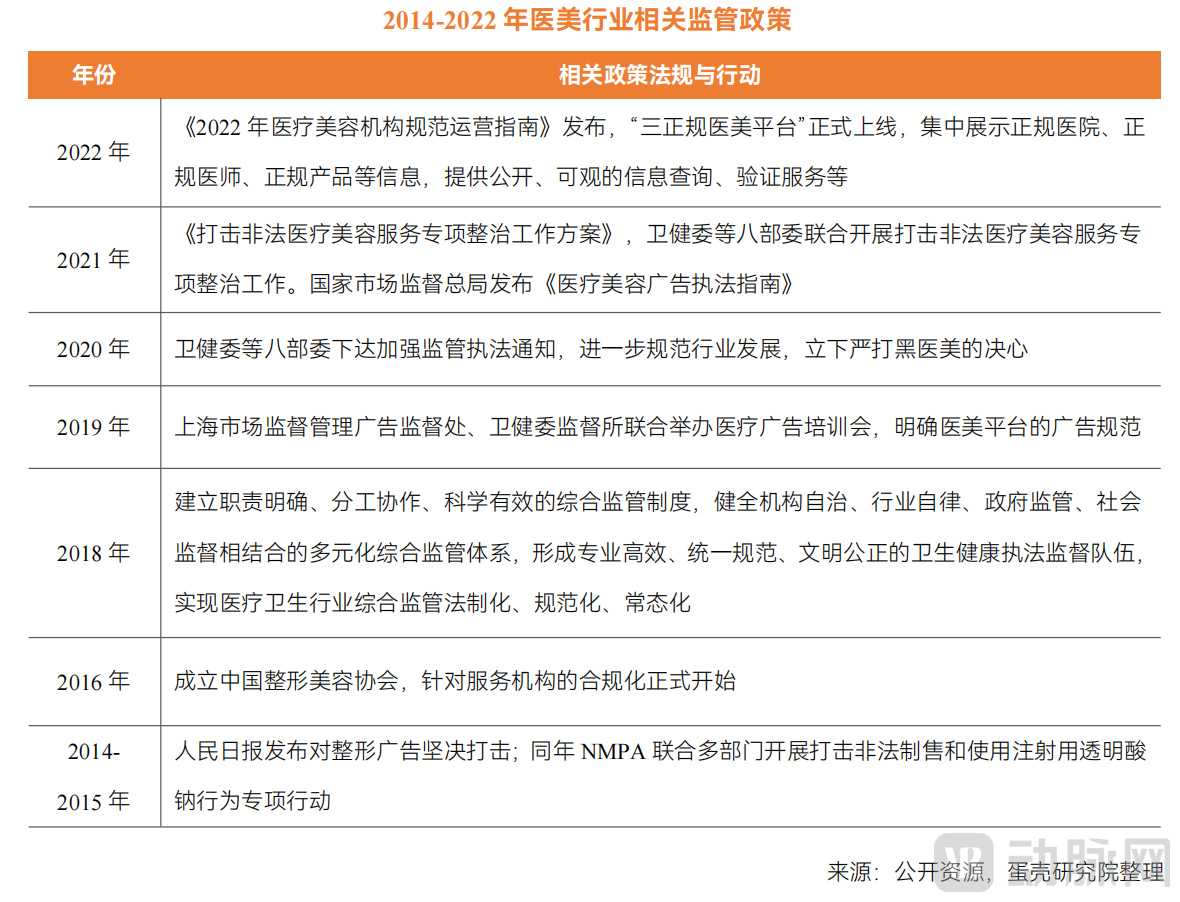

· Second, industry-related regulations are becoming increasingly comprehensive, with supervision trending toward greater stringency. For instance, in 2022, the National Medical Products Administration (NMPA) issued the “Catalogue for Classification of Medical Devices” and the “Catalogue of Medical Devices Prohibited from Contract Manufacturing,” explicitly bringing products such as “skin boosters,” “radiofrequency devices,” and “thread lifts” under Class III medical device oversight and prohibiting their contract manufacturing. This implies that certified products distributed in compliance with regulations will capture a larger market share.

· Third, an increasing number of innovative companies specializing in energy-based medical aesthetic devices have entered the market, achieving notable progress in both R&D and commercialization. The rise of domestic innovation has provided the industry with a broader range of high-quality products and solutions. It is worth noting that China’s high-end energy-based medical aesthetic device market is nearly monopolized by imported manufacturers, leaving substantial room for domestic substitution.

With immense growth potential, the energy-based medical aesthetics device sector has attracted significant attention and investment from numerous institutions. According to incomplete statistics from VCBeat, since 2022 alone, more than 50 top-tier VC/PE firms have conducted due diligence or invested in this field, sparking a wave of enthusiasm.

“Behind the ‘Boom,’ Greater Rationality and In-Depth Reflection Are Needed:”How to adopt a more comprehensive perspective for macro-level strategic planning, clarify misconceptions, and gain insight into the core trends of industry development has become a key concern for market entrants.

To this end, VCBeat Institute dedicated six months to the project, with senior industry experts Xia Yuqing, Wang Guohe, Liu Fei, and Feng Qingyu serving as advisors. Through extensive research, they completed the nearly 100,000-word White Paper on Energy-Based Devices in Medical Aesthetics. The report provides a comprehensive overview of the industry from multiple dimensions—including demand, supply, regulation, technology, business models, and talent—while identifying key variables in the sector, as well as current challenges and future possibilities.

At this pivotal moment of explosive growth in domestically produced energy-based medical aesthetic devices, let us together feel, witness, and personally experience the industry’s tidal wave.

This article provides an interpretation of the White Paper on Energy-Based Devices in Medical Aesthetics. To obtain the full report, please scan the QR code to add our assistant; if you have already added them, please feel free to inquire directly.

1. Industry Status: Energy-based Devices in Medical Aesthetics Gain Favor, with Diverse Offerings Meeting Consumer Demand

2. Underlying Variables: Five Major Technologies Lead the Way, Striking Gold in the Aesthetic Medicine Sector

3. Market Observation: Comparative Analysis of Photoelectric Energy Sources Addressing the Four Major Demands

4. Policy Logic: Combining Deregulation with Strict Enforcement Amid Strong Regulatory Oversight, Compliant Medical Aesthetics Products Enter Their Golden Age

5. Trend Evolution: Unlimited Future Potential, Four Key Trends in the Energy Source Industry

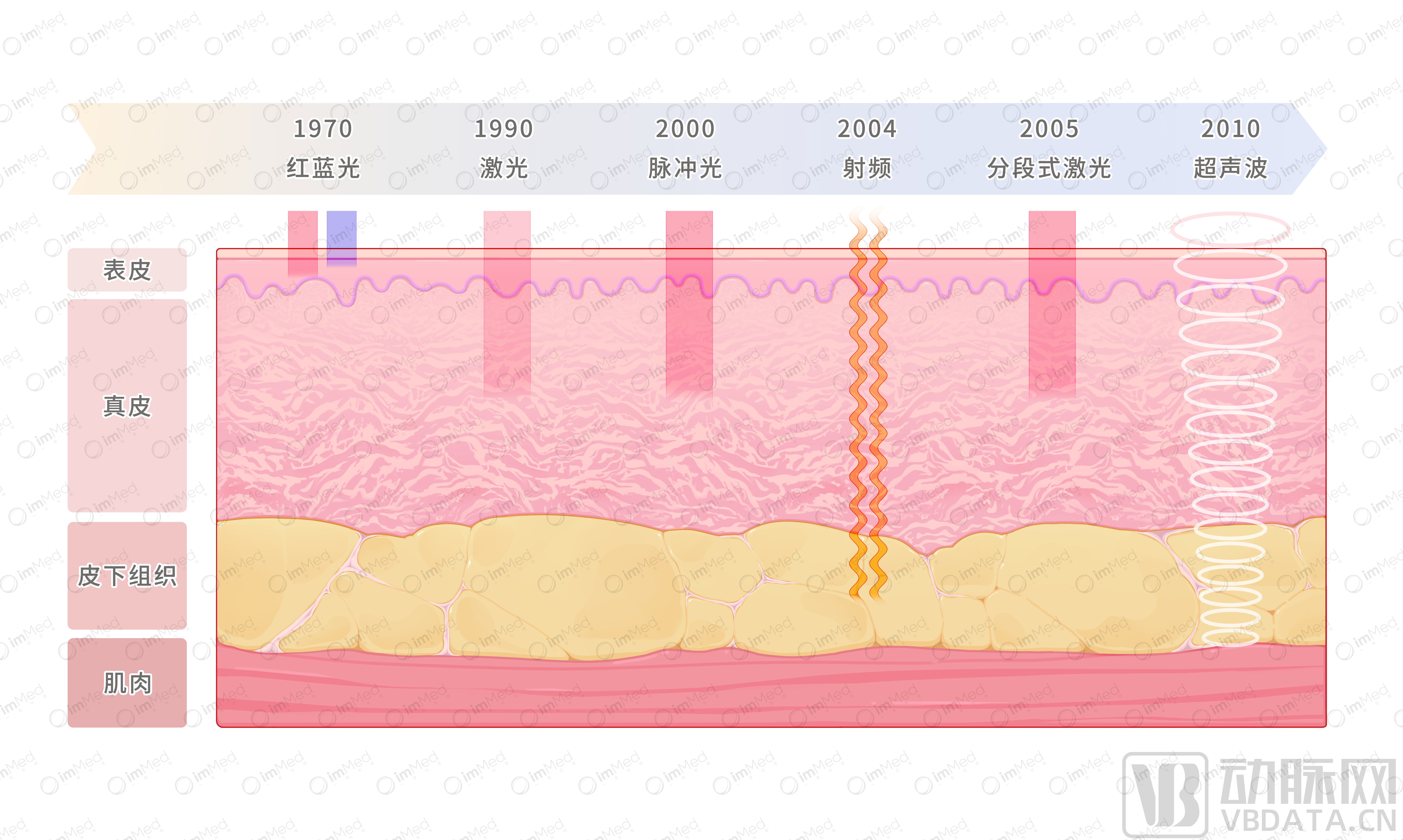

Concept Analysis:Energy-based aesthetic medicine refers to the application of energy forms such as lasers, radiofrequency, and ultrasound in medical aesthetics, where targeting different skin layers addresses specific concerns.

Specifically, energy-based medical aesthetic devices can achieve anti-inflammatory, antibacterial, acne-clearing, spot-reducing, and skin-brightening effects when acting on the epidermis; tighten skin, reduce wrinkles, and stimulate regeneration when targeting the dermis; promote fat reduction and body contouring when affecting the subcutaneous fat layer; and stimulate collagen regeneration for anti-aging benefits when acting on the SMAS (Superficial Musculoaponeurotic System) layer.

▲ Schematic diagram of energy sources acting on different layers of the skin. Illustration by: Yimu Keshi

Meanwhile, energy-based aesthetic medical devices offer advantages such as short recovery times, low cost per treatment, and high user frequency, making them suitable as adjunctive therapies for daily skincare. Furthermore, their synergistic effects with injectable aesthetic products can yield superior outcomes, garnering significant attention across various treatments.

Industry Overview: Energy-Based Devices in Aesthetic Medicine Gain Favor, Offering Diverse Solutions to Meet Consumer Demand

Among today’s aesthetic seekers, the primary demands fall into four categories: skin whitening, skin rejuvenation, anti-aging, and body contouring, all of which can be addressed by energy-based medical aesthetic devices.

Taking skin texture issues as an example, these include acne, enlarged pores, and fine atrophic scars left behind by various inflammatory diseases. Although skin texture problems do not directly affect physical health, they can exacerbate appearance-related anxiety, thereby impacting both mental and physical well-being. Alterations in skin texture are sequelae of aging or dermatological conditions, manifesting as dryness and roughness, loss of radiance, atrophy and thinning, fine lines, enlarged pores, and atrophic scars.

In this regard, photoelectric therapies stimulate the contraction of dermal collagen fibers through photothermal effects, activate fibroblasts to secrete relevant cytokines that promote collagen synthesis, or initiate the wound healing cascade by causing controlled damage to the epidermis and dermis, thereby achieving tissue remodeling and improving skin texture.

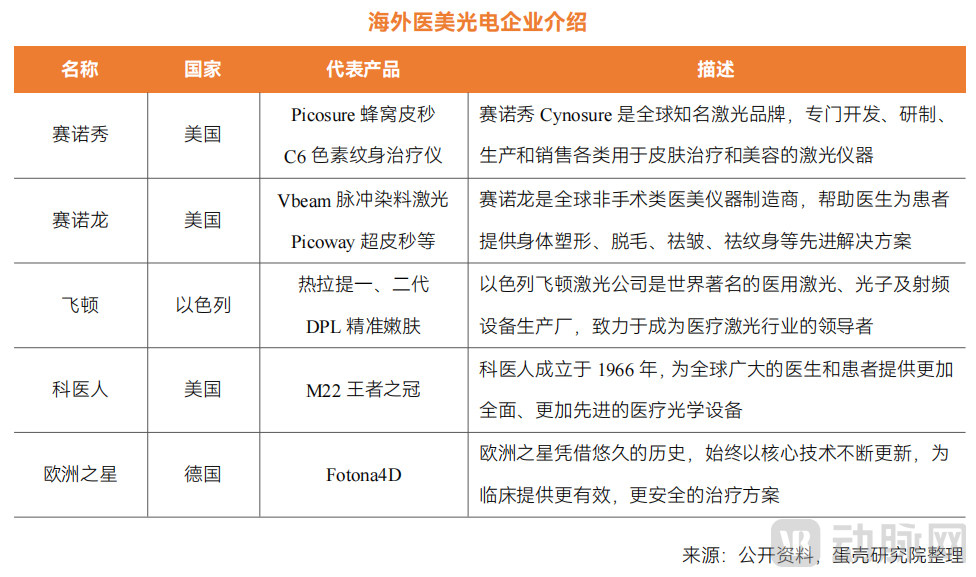

China’s medical aesthetics device industry started relatively late, and the current competitive landscape of the photoelectric medical aesthetics market is dominated by foreign companies.In the global aesthetic medicine optoelectronic device industry, the United States and Israel hold absolute advantages in terms of influence and technology. Currently, the mainstream laser equipment manufacturers in China include Cynosure (US), Candela (US), Alma (Israel), Lumenis (US), and Fotona.

In China, overseas enterprises entered the market earlier and possess significant technological advantages and industry experience; consequently, the majority of the market share remains dominated by foreign brands. Data indicates that foreign brands account for more than 60% of the mid-to-high-end market, including public hospitals and large medical aesthetics chains.

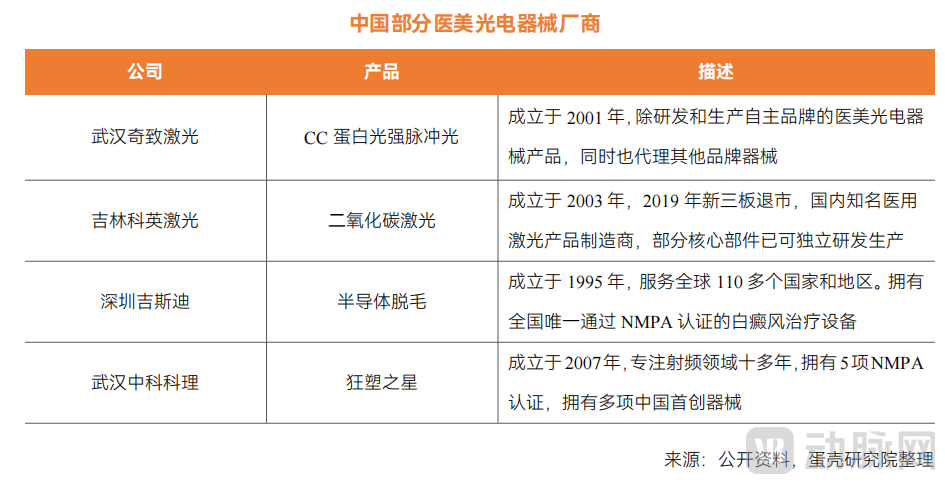

Moreover, the domestic medical aesthetics optoelectronic device industry in China is characterized by low market concentration, with a large number of small-scale manufacturers producing low-tech, low-priced products of inconsistent quality. Domestic companies in this sector hold only approximately 15% of the market share, primarily serving small and medium-sized private outpatient clinics, private practices, and lifestyle beauty salons. Furthermore, due to the high entry barriers imposed by NMPA certification, the majority of uncertified medical aesthetics optoelectronic devices operate in the gray area of beauty salons.

Underlying Variables: Five Major Technologies Lead the Way, Striking Gold in the Premium Medical Aesthetics Sector

Laser, Intense Pulsed Light (IPL), Radiofrequency, Focused Ultrasound, and Cryolipolysis: The Five Major Technologies Leading the Energy-Based Aesthetic Medicine Market

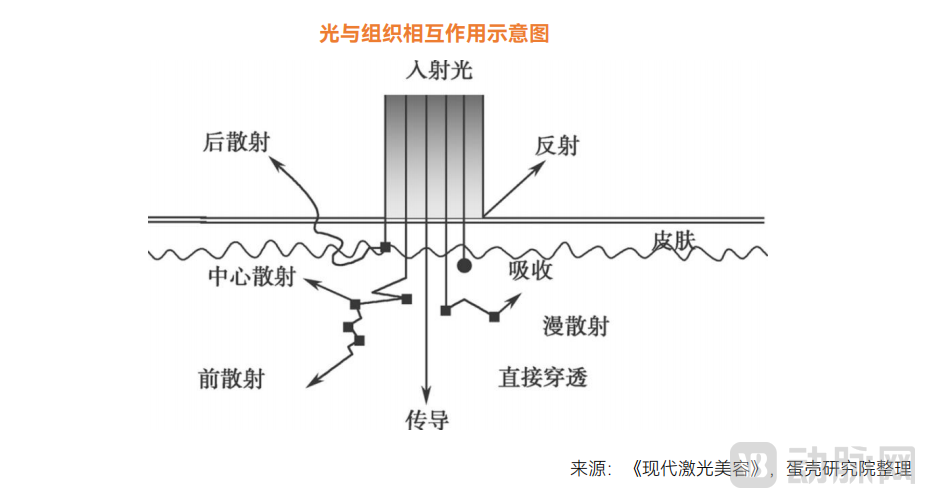

Let's start with lasers.As a form of electromagnetic radiation, laser light possesses four key characteristics: monochromaticity, coherence, collimation, and high energy. The interaction between laser and biological tissue is a complex process determined by multiple factors. When laser irradiates biological tissue, it undergoes four physical processes: reflection, scattering, absorption, and transmission. Biological tissue is a heterogeneous material composed of various types of cells and extracellular matrix. Due to differences in the structural and electromagnetic properties of different biological tissues, there are significant variations in their optical properties, including reflection, scattering, absorption, and conduction. Consequently, the outcomes of laser-tissue interactions also vary.

Lasers of different wavelengths can only interact with biomolecules of specific intrinsic frequencies in a biologically effective manner, because the absorption of laser photon energy by biomolecules exhibits frequency-selective characteristics.

In terms of application,The principle of selective photothermolysis is commonly used to treat pigmented disorders; the extended principle of selective photothermolysis can be applied to hair removal and the treatment of cutaneous vascular diseases; the principle of fractional photothermolysis enables skin remodeling and tightening, improving facial rejuvenation; the principle of photoacoustic action can effectively treat pigmented skin diseases and enhance skin rejuvenation.

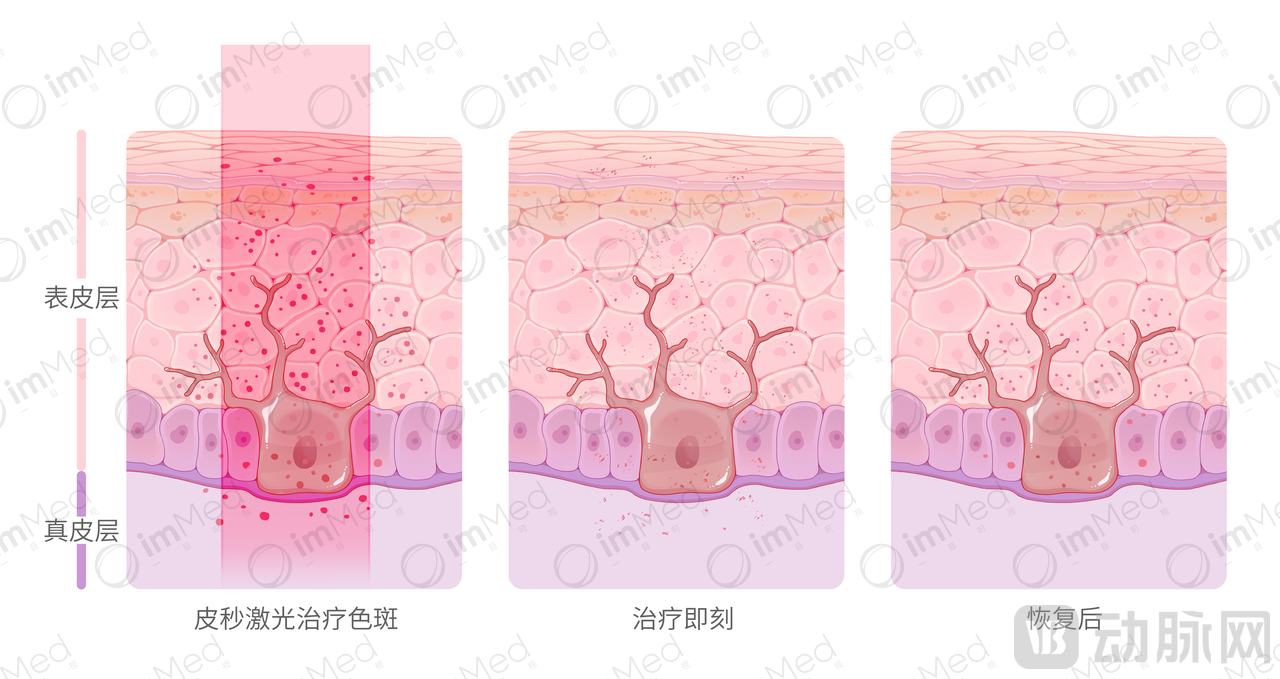

Taking picosecond lasers, which primarily operate on the principle of photoacoustic interaction, as an example, they represent the ultimate solution for pigmented disorders and can achieve excellent results in spot removal. Picosecond lasers are indicated for the treatment of various epidermal and dermal hyperpigmentation conditions, demonstrating ideal efficacy for freckles, solar lentigines, and nevus of Ota. They are also effective for café-au-lait macules and lentigines, although a certain rate of recurrence remains. For epidermal hyperpigmentation disorders such as freckles, solar lentigines, and café-au-lait macules, treatment can be administered using 532 nm Nd:YAG picosecond lasers or 755 nm alexandrite picosecond lasers.

▲ Schematic diagram illustrating the principle of picosecond laser treatment for pigmented lesions. Graphic by: Yimu Visual

Treatment parameters should be set according to the patient's skin type and the color of the skin lesions, with a mild frost reaction generally serving as the clinical endpoint. For dermal hyperpigmentation disorders such as nevus of Ota and acquired bilateral nevus of Ota-like macules (ABNOM), treatment can be performed using a 755-nm alexandrite picosecond laser or a 1064-nm Nd:YAG picosecond laser. The typical treatment interval is 3 to 6 months; outcomes are generally favorable, with complete clearance often achieved after several sessions. Therefore, as lasers with pulse widths in the picosecond range, picosecond lasers will play a significant role in the treatment of tattoos and most hyperpigmentation disorders.

Regarding the industrial landscape of laser-based medical aesthetic devices, VCBeat believes thatDomestic equipment manufacturers are accelerating their catch-up efforts, poised to break the import monopoly in the high-end market and achieve domestic substitution.

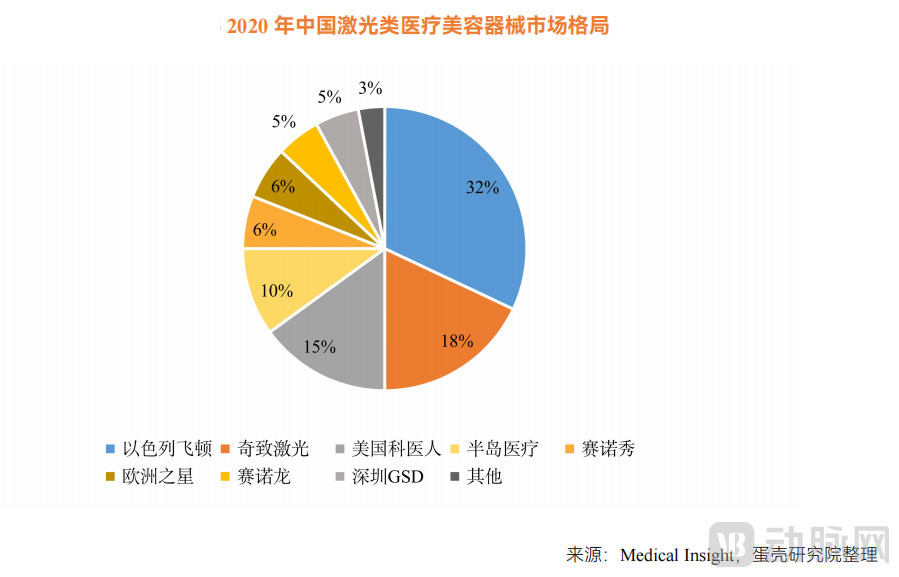

According to Medical Insight data, in 2020, the CR4 market share in China’s laser-based medical aesthetic device category reached as high as 75%, indicating a high level of industry concentration. Alma Lasers (Israel) ranked first with a 32% market share, followed closely by Qirui Laser and Lumenis (USA), with market shares of 18% and 15%, respectively. Overseas well-known brands such as Lumenis, Fotona, Syneron Candela, and Cynosure have secured certain market shares leveraging their technological strengths.

Currently, the domestic high-end optoelectronic product market remains dominated by imports. Chinese enterprises are on the verge of breaking through technical barriers, shattering this import monopoly, further capturing market share, and reshaping the industrial landscape.Currently, in the field of medical aesthetic laser devices, such as CO2Laser Devices: Chinese enterprises have largely met international standards, and several high-quality domestically produced devices have been launched. However, picosecond lasers, as an emerging technology in the medical aesthetics laser field, remain entirely monopolized by well-known overseas manufacturers such as Cynosure and Candela due to the high technical barriers associated with these products.

Encouragingly, numerous domestic manufacturers in China have already established a presence in the picosecond laser equipment market. As a representative enterprise specializing in the independent research, development, and manufacturing of mid-to-high-end medical aesthetic optoelectronic devices, Fumeilei Medical’s core product, the ForePico multi-wavelength picosecond laser treatment system, officially commenced registration testing in November 2022. Empirical performance parameters of the device are fully comparable to those of imported counterparts, while demonstrating superior stability.

In addition, in February 2023, Keying Laser’s “Nd:YAG Picosecond Laser Treatment System” officially received approval from the National Medical Products Administration (NMPA), becoming the first domestically produced picosecond laser treatment product approved for market launch in China.

Therefore, it is foreseeable that as domestic enterprises continue to break through technical barriers and obtain NMPA approvals, the competitiveness of Chinese-made devices in the high-end market of the medical aesthetic laser sector will steadily increase, breaking the monopoly held by imported brands and achieving import substitution.

Next, let us examine intense pulsed light (IPL), also known as photorejuvenation. IPL is a broad-spectrum light generated by focusing and filtering a high-intensity light source. As a broad-spectrum light, IPL can target multiple absorption peaks, including those of melanin, oxyhemoglobin, and water. Since the chromophores in normal and pathological tissues differ in their properties, depth, and volume, they exhibit varying degrees of light absorption and temperature rise. This differential thermal response allows for the effective treatment of pathological tissues without damaging normal tissues.

The wavelength range of IPL is 550–1200 nm, with different wavelengths operating via distinct mechanisms for various indications. For instance, the 415–950 nm range can treat acne by selectively targeting and destroying porphyrins, which are metabolic products of Cutibacterium acnes. Simultaneously, photothermal effects induce collagen denaturation and remodeling, enhancing skin elasticity, improving sebaceous gland secretion and enlarged pores, and reducing acne occurrence. Additionally, the 560–950 nm range can treat pigmentation disorders by leveraging selective photothermolysis to fragment melanocytes; superficial crusts then slough off, while deeper fragments are cleared via lymphatic metabolism.

▲ Graphic design: Yimu Visual

▲ Graphic design: Yimu Visual

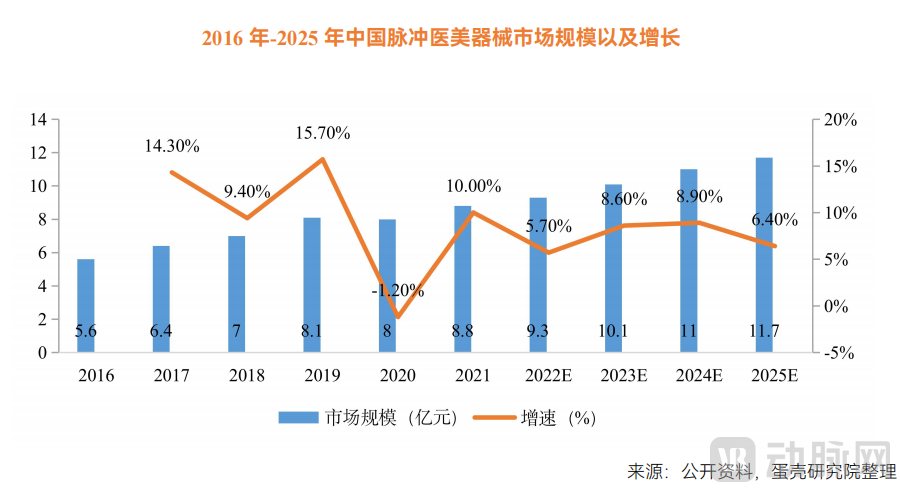

In terms of market growth, intense pulsed light (IPL) technology is poised for rapid volume expansion, with significant room for future growth. As "photorejuvenation" remains one of the most popular medical aesthetic procedures in China, the market for IPL-based medical aesthetic devices has demonstrated a stable and positive growth trajectory. In 2020, due to the impact of the pandemic, the market size of pulse-based medical aesthetic devices in China experienced a slight decline. The market value of unauthorized and counterfeit products reached RMB 110 million, while compliant products accounted for RMB 690 million, resulting in a total market size of RMB 800 million, a year-on-year decrease of 1.2%. It is projected that by 2022, the market size for compliant IPL medical aesthetic devices in China will reach RMB 930 million. The industry scale of intense pulsed light technology in the coming years should not be underestimated.

Dominance of Imported Brands Creates High Entry Barriers for Domestic Competitors. China’s intense pulsed light (IPL) aesthetic device market currently relies heavily on imports. In 2020, imported IPL aesthetic devices accounted for 80% of the market share, with Lumenis holding 51%, Alma Lasers (acquired by Sisram Medical) 20%, Syneron Candela (Israel) 5%, and Cynosure (US) 4%, forming a relatively stable competitive landscape dominated by leading players.

In this landscape, upstream device manufacturers possess stronger bargaining power relative to the highly fragmented downstream institutions, granting them greater control and regulatory influence over market pricing, existing inventory, and technology. Furthermore, leading enterprises capture the majority of market profits, with gross profit margins of approximately 50%-60%. This enables them to expand capacity and achieve scaled production with lower difficulty and cost, reinforcing a “strong get stronger” dynamic. Under such circumstances, domestic small and medium-sized enterprises (SMEs) lacking technological advantages and distinctive product features will find it increasingly difficult to enter the intense pulsed light (IPL) market and secure a share.

Based on the development of the industry, VCBeat believes that for companies entering the market,Low pricing with high volume and treatment precision are key, while expanding application scenarios present opportunities.

Next, let us examine radiofrequency (RF), which refers to high-frequency alternating electromagnetic waves situated between amplitude-modulated and frequency-modulated radio waves. Its energy exists and propagates through space in the form of electric or magnetic fields (waves).

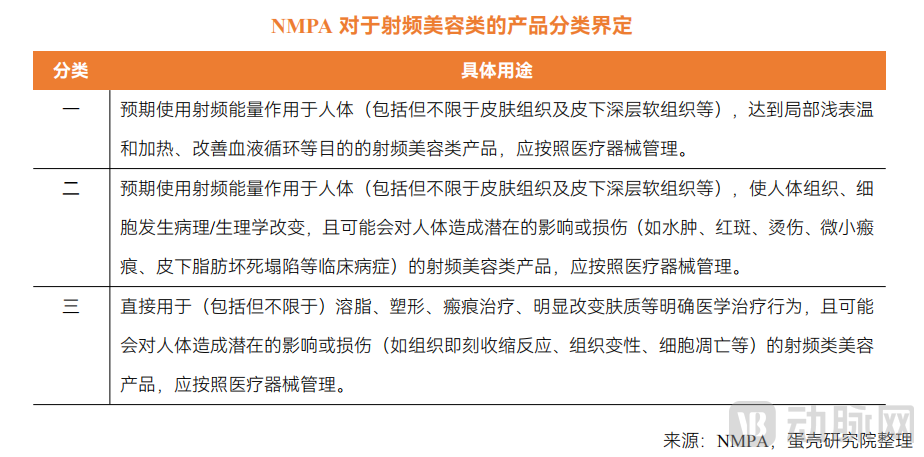

Currently, the NMPA has established strict definitions and classifications for radiofrequency (RF) aesthetic devices. According to the “Guiding Principles for the Classification of Radiofrequency Aesthetic Products (Draft for Comments)” issued by the NMPA in April 2021, RF aesthetic products are primarily categorized into three classes based on their medical aesthetic applications and associated risks, as detailed in the table below:

According to the "Guiding Principles for Registration Review of Radiofrequency Aesthetic Devices (Draft for Comments)" issued by the Center for Medical Device Evaluation of the National Medical Products Administration in August 2022, radiofrequency aesthetic devices refer to products that utilize electrical energy, such as radiofrequency current at specific frequencies (typically around 200 kHz to 5 MHz) or electric fields (typically 13.56 MHz or 40.68 MHz), to act on human tissue and generate thermal effects. These devices are intended to treat skin laxity, reduce skin wrinkles, minimize pores, tighten/lift skin tissue, treat acne and scars, or reduce fat (through fat softening or decomposition).

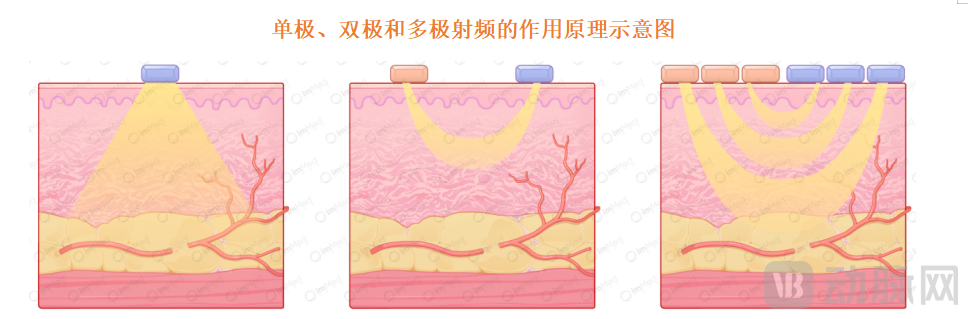

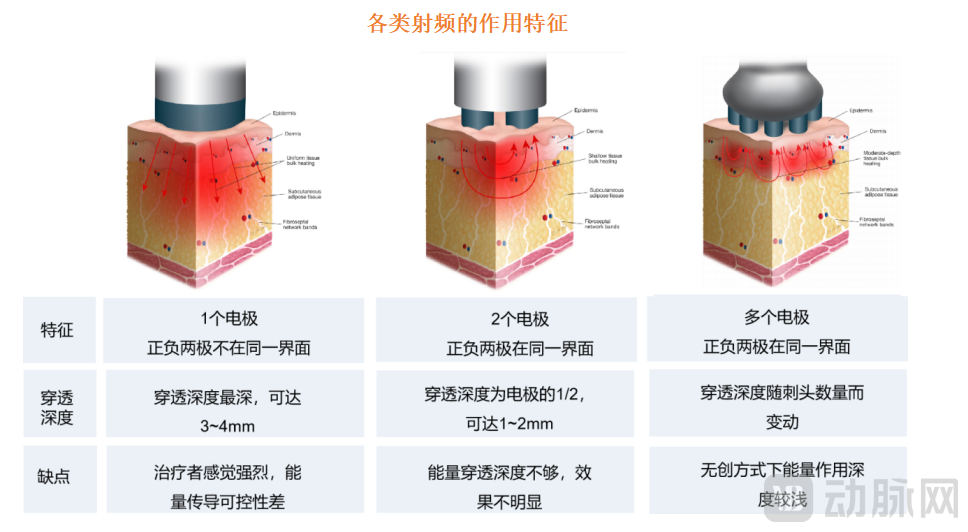

Radiofrequency (RF) aesthetic devices can be classified into three categories based on the number of electrodes: monopolar, bipolar, and multipolar RF. The number of electrodes constrains the depth of penetration for products operating at different frequencies, resulting in significant variations in clinical efficacy.

▲Graphic design: Yimu Visual

▲ Source: Public information, CNKI, J Cosmet Dermatol; compiled by VCBeat.

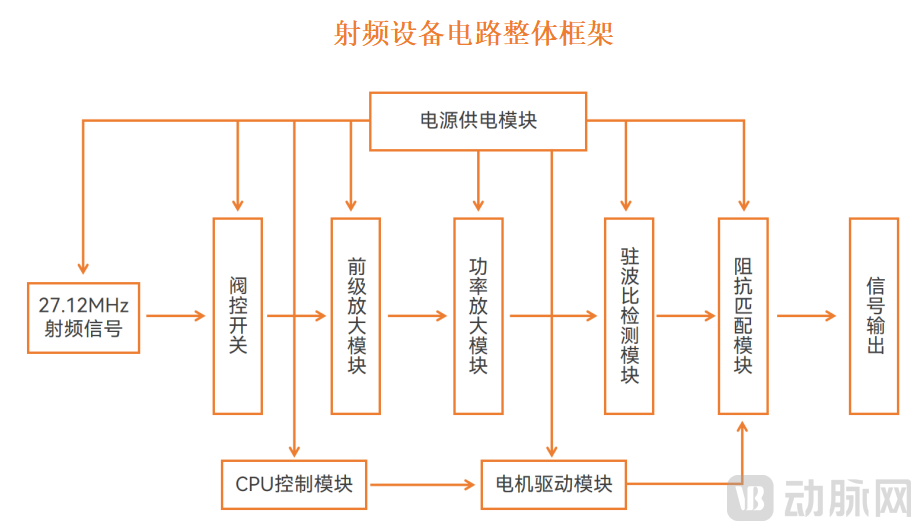

Compared with other photoelectric energy-based aesthetic medical devices, radiofrequency (RF) technology has relatively lower technical barriers, and its core hardware and software technologies are relatively mature. The figure below illustrates the main structural components of RF devices. The RF system emits radiofrequency signals at a fixed frequency, which are amplified and processed; under CPU control, signal detection and impedance matching are performed to achieve stable output within the desired energy range. The technical challenges of RF devices primarily lie in the CPU control module, voltage standing wave ratio (VSWR) detection, and impedance matching modules.

▲ Source: Public information, compiled by VCBeat.

Radiofrequency (RF) aesthetic devices have undergone more than two decades of development, with the domestic medical aesthetics market consistently led by overseas brands. In 1995, Solta Medical introduced Thermage, a monopolar RF system for skin tightening, which received U.S. FDA clearance in 2002, marking the widespread adoption of RF technology in dermatological aesthetics. Since 2014, well-known international RF aesthetic devices, including Alma’s Thermolift, Solta’s Thermage, and EndyMed, have successively entered the Chinese market, driving the rapid growth of China’s RF aesthetics industry.

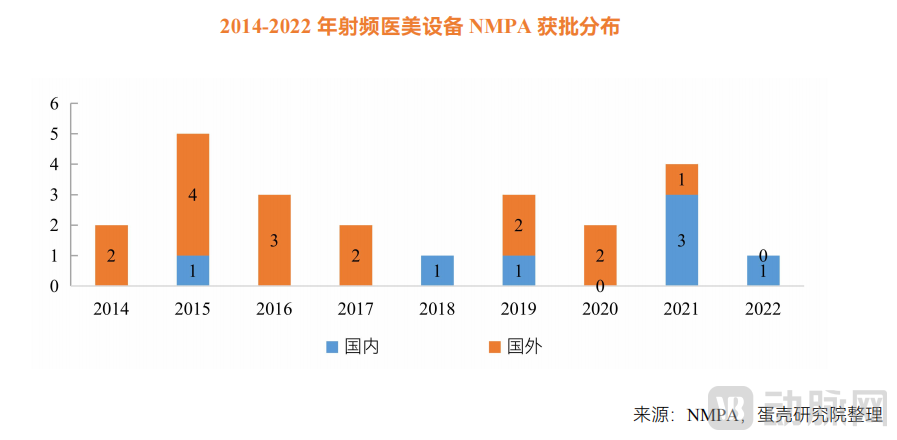

Currently, the industry has entered a period of robust growth, with 23 radiofrequency medical aesthetic devices approved in China; domestic brands are primarily focused on the mid-to-low-end market.In the past three years, China has witnessed a surge in the market launch of radiofrequency (RF) aesthetic devices. To date, 23 RF aesthetic products have received approval from the National Medical Products Administration (NMPA), among which seven are domestically developed, accounting for 29% of all marketed products. However, in terms of regulatory classification, nearly all domestic RF aesthetic devices have been approved as Class II medical devices, whereas the majority of imported RF aesthetic devices have obtained Class III medical device certifications. This indicates that most domestically produced RF aesthetic devices operate at lower energy levels and pose lower risks, thereby primarily targeting the low-end market.

As Thermage spurred growth in the radiofrequency (RF) aesthetic medicine sector, Chinese companies actively entered the market, striving to accelerate product launches and seize first-mover advantages. Between 2019 and 2021, six RF-based aesthetic medical devices were approved in China. Domestic manufacturers, represented by brands such as Refirmie and Peninsula Medical, are currently building robust media presences on platforms like Xiaohongshu (Little Red Book), Weibo, and Douyin (TikTok), while engaging influencers and celebrities for promotional campaigns to rapidly enhance brand visibility.

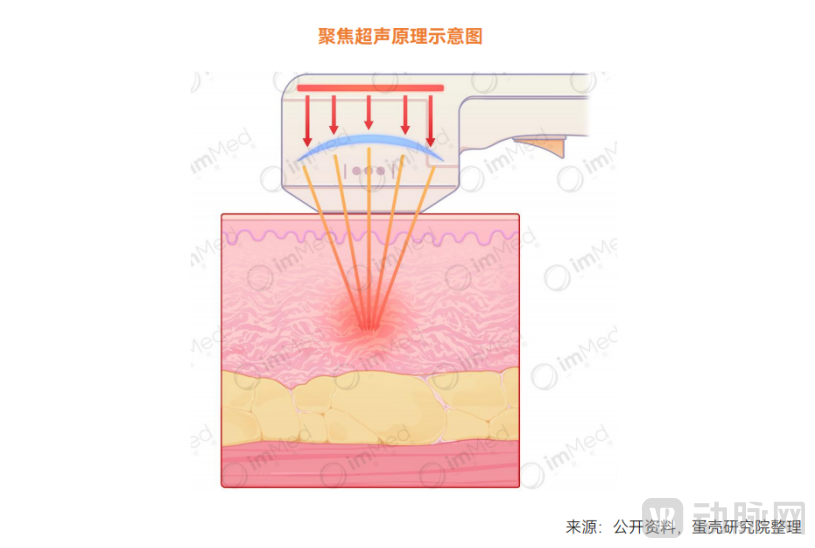

Then, let's look at focused ultrasound., it achieves focusing at a single point during the transmission of ultrasound waves. Through the conversion of acoustic energy into thermal energy, a high-temperature therapeutic focal point is formed within a short period.

Focused ultrasound technology was initially applied in non-invasive tumor treatment. During subsequent research, investigators discovered that by appropriately adjusting the frequency of the ultrasound (as ultrasonic energy is correlated with frequency, with higher frequencies yielding greater energy), focused ultrasound (hereinafter referred to as MFU when mentioned in the context of medical aesthetics) also demonstrates excellent applications in the field of medical aesthetics. It can achieve effects on the deep tissue layers of the face and body without damaging the outer skin layer.

▲ Graphic: Yimu Visual

Similar to other anti-aging technologies, the fundamental principle of MFU (Microfocused Ultrasound) for anti-aging is also to stimulate collagen regeneration through heating, thereby achieving lifting and tightening effects. Currently, focused ultrasound has a substantial potential market in China, estimated to accommodate three to four companies. In Europe and the United States, focused ultrasound and radiofrequency are recognized as the two core technologies for facial anti-aging. They target different demographic groups: Thermage primarily serves individuals aged 30–40, while Ultherapy mainly caters to consumers over 40, with each accounting for approximately 50% of the market size.

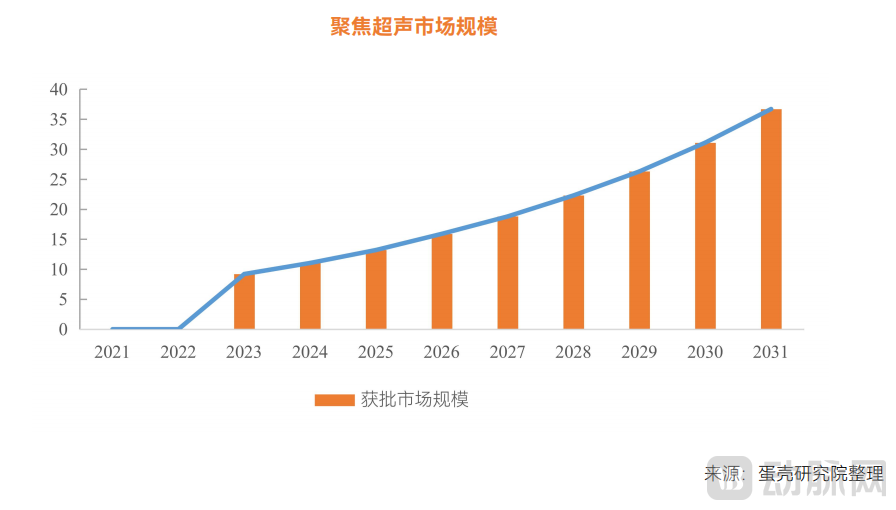

According to statistical data from Market Growth Reports, the global market size for approved focused ultrasound aesthetic systems is estimated at USD 192.3 million. In China, the market currently remains untapped, as no Class III focused ultrasound devices have yet received regulatory approval for commercial launch.

According to VCBeat Research Institute, multiple focused ultrasound products are currently in the clinical registration phase. If regulatory authorities open up the market approval pathway for focused ultrasound devices, relevant products are expected to receive approval in 2023. Upon successful commercialization, the sector is poised for a modest surge over the following three years, with an estimated compound annual growth rate (CAGR) of 20%, before transitioning into a stage of steady growth at an annual rate of 18%. The market size is projected to reach RMB 3.68 billion by 2031, with capacity to support 3–4 MFU companies.

However, the current market for focused ultrasound devices is limited, with significant regulatory hurdles for approval. Only three products are commercially available worldwide: Ultherapy, Doublo, and Sofwave. Ultherapy was the first focused ultrasound device approved by the U.S. Food and Drug Administration (FDA) for facial medical aesthetics and the first microfocused ultrasound (MFU) product to reach the market. Initially approved for lifting and tightening the eyebrows, it later received approval for treatment of the submental region, establishing it as an industry benchmark. Doublo, launched by South Korea’s Hironic, features an overall design similar to the American-made Ultherapy. However, its single-session energy output is slightly lower, necessitating multiple treatment sessions for sustained results. It obtained CE and KFDA certifications in 2017. Sofwave is the latest skin-tightening therapy approved by the FDA, demonstrating more pronounced effects on the epidermis and dermis. It received FDA clearance in 2019 for the reduction of fine lines and wrinkles. Currently, there are no MFU products commercially available in China, leaving a potential market worth RMB 3.5 billion untapped.

The delayed approval of imported products for market launch presents the best opportunity for domestically produced devices to make a comeback.Given the current regulatory landscape, China maintains stringent oversight of focused ultrasound devices. The fact that the U.S.-version ultrasonic scalpel has failed to secure approval from the National Medical Products Administration (NMPA) for over a decade indicates that its safety profile remains unverified and carries a continued risk of non-approval in the future. If domestic manufacturers can seize this opportunity, overcome existing technological limitations, and effectively address safety concerns, they stand a strong chance of being the first to obtain Class III medical device certification, thereby capturing the domestic market and achieving leapfrog development.

In the MFU sector, domestic manufacturers still hold significant advantages. On one hand, China already has a number of outstanding HIFU companies with established technical expertise in the field of ultrasound. Since MFU technology has slightly lower requirements than the HIFU industry, these companies are well-positioned to enter the MFU market, leveraging their strengths to further enhance the performance of domestically produced devices.

On the other hand, maintenance is particularly critical for focused ultrasound devices. Any decline in performance parameters may lead to deviations in therapeutic efficacy. Inadequate after-sales service and maintenance from imported manufacturers can result in devices operating for extended periods without proper inspection, making them prone to undetected functional issues that significantly compromise treatment outcomes. Domestic manufacturers, by contrast, offer relatively comprehensive integrated services, including regular inspection and replacement of components, ensuring that devices remain in optimal condition and enhancing operational safety.

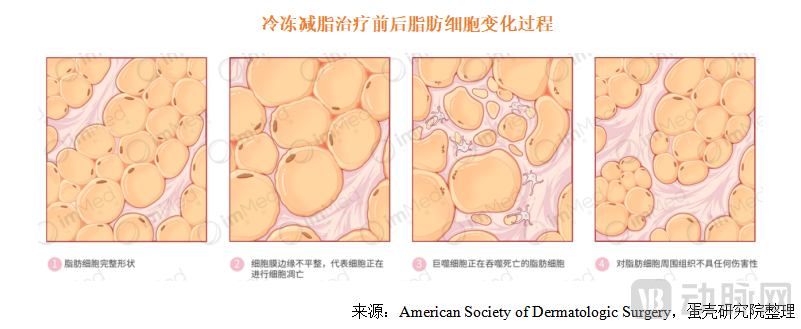

Finally, let’s look at cryolipolysis., primarily by delivering precisely controlled cryogenic energy via a non-invasive cooling device to targeted fat-reduction areas, thereby selectively eliminating adipocytes in those regions. Specifically, lipid ice crystals induced by cold exposure disrupt adipocytes. Within 72 hours post-treatment, the damaged adipocytes trigger an inflammatory response, manifesting as a lobular panniculitis-like reaction that peaks at day 14 and persists until day 30. Macrophages phagocytose the damaged adipocytes; inflammation gradually subsides between days 60 and 90, accompanied by a reduction in adipocyte volume and thickening of the fibrous septa between fat lobules. Therefore, a 90-day period is typically considered one treatment cycle for cryolipolysis.

▲ Graphic: Yimu Visual

In 2010, the first cryolipolysis device, CoolSculpting®, was approved by the FDA for the treatment of localized fat deposits in the flanks. It was subsequently approved for additional areas, including the abdomen (2012), thighs (2014), submental region (2015), and the arms, back, inframammary area, and banana roll (2016).

In terms of market landscape, imports dominate, while established domestic pharmaceutical companies are actively expanding their presence. The global manufacturers of cryolipolysis devices mainly include Allergan, ENSCON (South Korea), and High Tech. In China, only Allergan’s CoolSculpting® was approved for marketing in 2016. Sinopharm East China Pharmaceutical Group’s wholly-owned subsidiary, UK-based Sinclair Pharma Limited, completed the acquisition in April 2021 of High Technology Products, S.L.U., a Spanish energy-based medical aesthetics device company held by Cocoon Business Investments, S.L.U. High Tech’s current non-invasive fat reduction products include Cooltech, Cooltech Define, and Crystile, with clinical trials and registration in the Chinese market expected to be completed within two to three years.

Market Observation: Comparative Analysis of Photoelectric Energy Sources Addressing Four Major Needs

Next, this article will conduct a comparative analysis of photoelectric energy sources based on four major demands: skin tone improvement, skin texture enhancement, facial rejuvenation, and fat reduction with body contouring.

In terms of skin tone improvement, optical whitening demonstrates significant advantages.As the skin whitening market expands rapidly, the drawbacks of traditional approaches are increasingly evident, prompting industry consolidation; optical whitening is set to become a new growth driver.

Overall, optical whitening offers two major advantages. On one hand, it addresses the root cause of the problem, demonstrating greater efficacy and competitiveness compared to traditional methods such as pharmaceutical whitening. On the other hand, it boasts a higher safety profile with fewer side effects, making it more readily accepted by consumers new to medical aesthetics.

Although both lasers and intense pulsed light (IPL) are optical energy sources, they differ in technical principles and each possesses distinct market advantages. Essentially, lasers are high-intensity, highly focused energy sources. Due to their extremely small emission angle, lasers produce nearly perfectly parallel and collimated beams, enabling directional, concentrated emission that generates significant thermal effects. In contrast, IPL is essentially broad-spectrum, non-coherent light. With a wide range of unfiltered wavelengths, it requires filters for artificial control and constitutes a relatively low-energy, divergent energy source.

Due to the distinct characteristics of their energy sources, the future key markets for development differ: lasers, with their high specificity and prominent therapeutic properties, are geared toward more specialized markets; whereas intense pulsed light (IPL) holds significant value in treating multiple concurrent skin conditions and vascular skin diseases.

In terms of skin quality improvement, combined laser and radiofrequency therapy may be the future trend.Non-medical aesthetic interventions offer limited improvement in skin texture, making consumer demand for medical aesthetic treatments more inelastic. Lasers, intense pulsed light (IPL), and radiofrequency (RF) can all improve skin texture to varying degrees, with lasers and RF being more suitable as primary treatment modalities. This is because, although both laser and RF systems can effectively treat skin texture concerns, significant individual variability exists in these conditions, leading to differences in clinical outcomes between the two technologies. Therefore, lasers and RF do not represent a relationship of perfect competition.

▲ Graphic design: Yimu Visual

In the realm of facial rejuvenation, different energy sources target distinct customer segments. With the rapid development of the anti-aging industry in China in recent years, anti-aging concepts have become deeply ingrained among consumers. At present, a growing number of consumers recognize that anti-aging is not merely about addressing existing signs of aging, but more importantly, about prevention. According to consumer profile statistics from iiMedia Research, the concept of anti-aging has penetrated younger demographics, with individuals aged 19–35 constituting the core consumer base for the industry. The trend toward younger anti-aging consumers is becoming increasingly pronounced, and the consumer base is expected to continue expanding, driving sustained growth in the market size of the anti-aging industry.

Anti-aging interventions require a comprehensive approach to addressing skin concerns. Early signs of skin aging originate in the epidermis, manifesting as dull complexion, fine lines, or rough texture. Over time, the skin’s barrier function weakens, increasing its sensitivity to external stressors such as heat and pollution. This can lead to dryness, while reduced blood circulation contributes to dullness and roughness. Additionally, intracellular pigments gradually accumulate with cellular aging, resulting in the formation of hyperpigmentation spots.

Optical Aesthetic Treatments Offer the Best Cost-Effectiveness for Combating Early Signs of Aging. Among various energy-based devices, optical energy sources provide the most cost-effective solution for treating early aging. On one hand, optical energy sources can simultaneously address multiple skin concerns, including skin tone and texture; furthermore, compared with technologies such as radiofrequency and ultrasound, lasers and intense pulsed light (IPL) demonstrate superior efficacy in treating superficial skin issues. On the other hand, optical energy-based treatments are more affordable and safer, with a lower risk of serious adverse effects such as facial nerve injury or permanent scarring.

For aging skin, radiofrequency and ultrasound technologies demonstrate significant advantages in the deep anti-aging sector due to their superior skin penetration and high therapeutic energy delivery.

Thermage boasts a prominent brand effect and an exceptionally high reputation barrier. As is widely known, radiofrequency-based devices are currently the most popular anti-aging treatments on the market, with Thermage standing out as a star procedure in the energy-based medical aesthetics sector.

Focused ultrasound is widely favored within the industry and may eventually share equal prominence with Thermage in the future. The evolution of the anti-aging sector reveals a distinct characteristic: rapid technological iteration, with the market requiring continuous stimulation from emerging technologies. Currently, the latest radiofrequency (RF) anti-aging technology has successfully extended its treatment depth to 4.3 mm, approaching the deepest layers of the dermis. However, to achieve more significant anti-aging results and address severely aged skin, targeting the superficial musculoaponeurotic system (SMAS) layer is key. Focused ultrasound remains the only technology capable of reaching the SMAS layer, making it highly attractive to middle-aged and older consumers. Furthermore, focused ultrasound delivers higher energy levels, which constitutes a highly competitive marketing advantage from a promotional perspective.

According to research by VCBeat, there is a broad consensus within the industry that once product approval is obtained, the next major trend in anti-aging will most likely be focused ultrasound devices.

In the realm of fat reduction and body contouring, market interest continues to rise, with significant potential yet to be tapped.China’s fat-reduction technologies have evolved from an invasive era represented by liposuction to a new era of non-invasive lipolysis, characterized by cryolipolysis, ultrasound, radiofrequency, and laser-based modalities.

Currently, non-invasive fat reduction remains a blue-ocean sector, with major companies racing to develop and enter the market. However, among non-surgical body contouring technologies—namely cryolipolysis, ultrasound, radiofrequency, and laser—only a few products have obtained certification from China’s National Medical Products Administration (NMPA), leaving significant potential in this market yet to be fully realized.

Currently, cryolipolysis offers effective fat reduction with high market recognition; laser lipolysis features short treatment times and a gentle, comfortable experience; radiofrequency lipolysis involves high-heat ablation, providing dual benefits of fat reduction and skin tightening; ultrasonic lipolysis utilizes high-intensity focused energy, integrating fat reduction with anti-aging effects; magnetic wave body contouring achieves simultaneous "fat burning and muscle building"; while lipolytic injections directly destroy fat cells, making them the preferred choice for small-area fat reduction.

As the fat loss and body contouring industry increasingly moves toward specialization and standardization, fat loss and body shaping institutions will provide more professional, personalized, and comprehensive service solutions tailored to diverse consumer demands.

In the future, continuously iterated non-invasive body contouring technologies will provide consumers with diverse options, while helping institutions develop flagship services, acquire customers, and accelerate expansion. The development of non-invasive technologies is redefining the body contouring market and will unlock its significant potential through ongoing advancements. Additionally, comprehensive fat reduction and body contouring solutions based on combination therapies are likely to become a trend. Aimed at addressing consumers’ full-cycle needs for fat reduction and body contouring, the combined use of different energy-based modalities, or the integration of various energy-based devices with injectable fat-reduction treatments, will not only continuously improve treatment efficiency and outcomes but also better align with consumer demands.

Policy Logic: Under Strong Regulation, a Combination of Channeling and Blocking Us in the Best Era for Compliant Medical Aesthetics Products

Driven by profit, the current medical aesthetics industry is plagued by irregularities across multiple segments, with numerous non-compliant issues prevalent in medical aesthetic institutions, product distribution, and marketing promotions. Therefore, compliant operations are imperative for the future development of the medical aesthetics industry.

Regulatory oversight is becoming marginally stricter, promoting healthy and orderly medium- to long-term industry development, accelerating market consolidation, and benefiting leading upstream enterprises and compliant medical aesthetic institutions. In recent years, policy regulation has continued to tighten and gradually shifted toward normalized, routine supervision. For example, in 2022, the National Medical Products Administration (NMPA) issued the “Catalogue for the Classification of Medical Devices” and the “Catalogue of Medical Devices Prohibited from Contract Manufacturing,” explicitly including skin boosters, radiofrequency devices, and thread lifts under Class III medical device supervision and prohibiting their contract manufacturing. These measures strengthen the implementation of primary responsibility for product quality and safety, improve quality control in the medical device production process, and effectively combat illicit practices such as the circulation of unauthorized and counterfeit products.

Although the number of non-compliant medical aesthetic institutions is expected to decline rapidly in the short term, which may lead to a decrease in overall market demand, from a long-term perspective, market rectification and cleanup will create a more favorable marketing environment for certified, domestically produced products with compliant distribution channels. This trend will benefit medical aesthetic institutions with high compliance standards, strong operational capabilities, and robust risk resistance, ultimately delivering better and more compliant services to consumers. Therefore, it is foreseeable that certified, domestically produced products with compliant distribution channels will gain greater market share.

Energy-based Device Market Holds Significant Growth Potential, Awaiting the Emergence of Domestic Leaders. China’s optoelectronic medical device manufacturers are still in a developmental stage, with the mid-to-high-end market dominated by overseas industry leaders. Domestic brands continue to lag in technical capabilities, and the market for optoelectronic devices has long been plagued by gray-market goods and counterfeits.

However, since 2018, the medical aesthetics market has entered an era of stringent regulation, severely impacting the market for unauthorized and counterfeit products. Under this regulatory trend, the market share of unauthorized and counterfeit products in the niche segment of medical aesthetic energy-based devices will be further compressed, while the market size for authentic products will be more effectively safeguarded. On the other hand, currently, most domestically produced devices are concentrated in the mid-to-low-end product lines, with sales prices generally ranging from RMB 50,000 to 100,000, and the high-end market is almost entirely monopolized by imported manufacturers.

Therefore, domestic high-end manufacturers are urgently needed in the market. As domestically produced mid-to-high-end optoelectronic products continue to be launched, some domestic manufacturers will rapidly emerge within a short period, becoming potential industry leaders.

Trend Evolution: Limitless Future Possibilities—Four Key Trends in the Energy Source Industry

As previously discussed, the energy source industry holds boundless potential for future growth. In this context, VCBeat has identified four major trends.

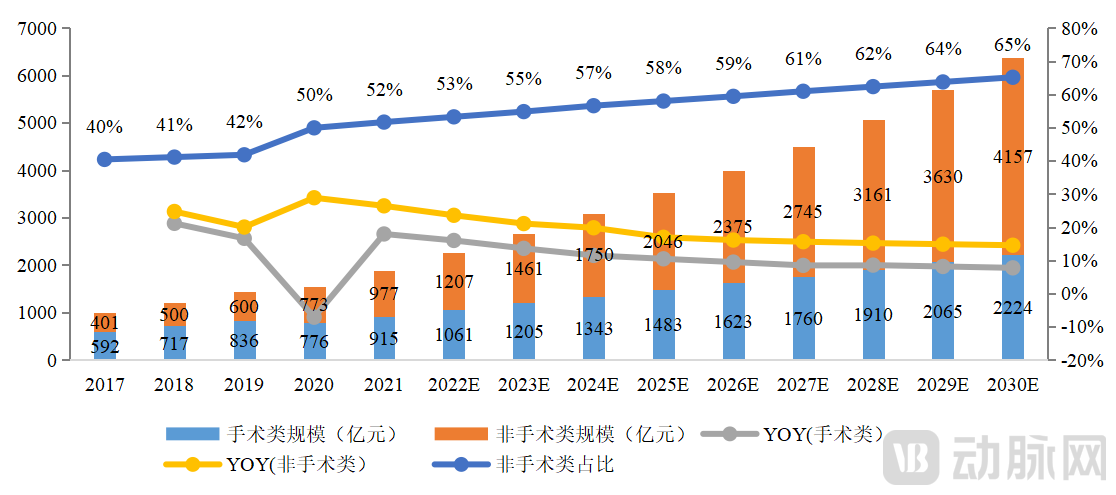

First, with rising penetration rates and declining prices, photoelectric-based procedures will gradually become mainstream.Public acceptance of medical aesthetics has increased significantly, with preferences shifting toward natural-looking results, which facilitates higher penetration rates for energy-based device (EBD) treatments. Statistics show that the number of medical aesthetics users in China grew from 4 million in 2017 to 19.13 million in 2021, and is projected to exceed 20 million in 2022. Notably, Chinese consumers’ aesthetic sensibilities are maturing, transitioning from the earlier trend of standardized, “assembly-line” surgical outcomes to personalized, natural beauty, while placing greater emphasis on potential side effects and long-term sequelae. Compared to surgical and injectable procedures, non-invasive EBD treatments carry virtually no risk of disfigurement due to procedural failure, deliver more natural-looking results, and can significantly boost consumer confidence. It is reasonable to predict that the penetration rate of EBD-based medical aesthetic treatments will continue to rise in the future.

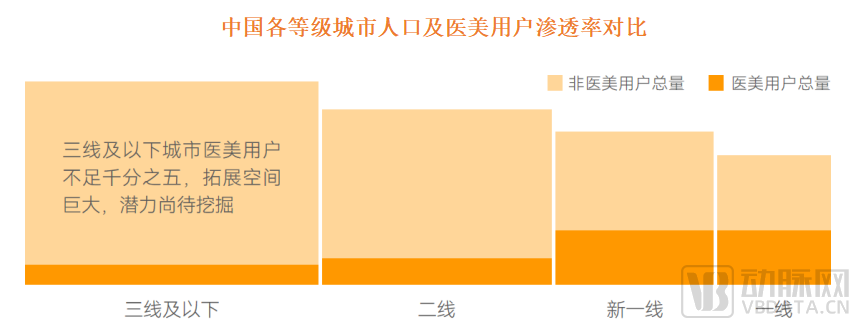

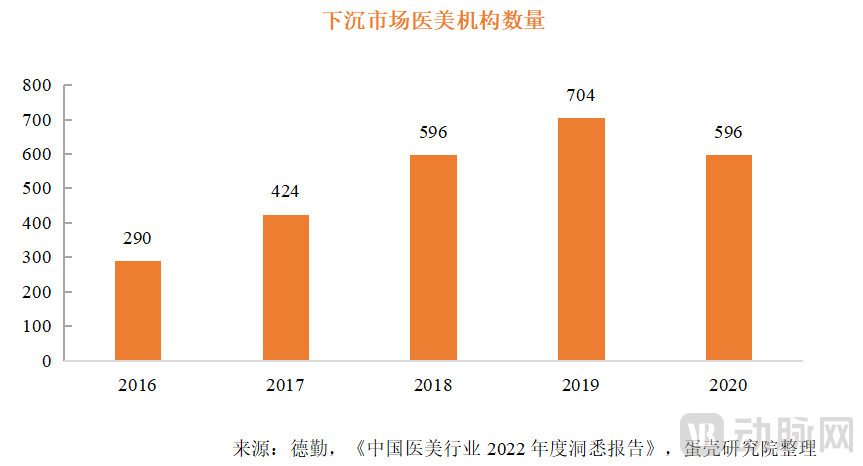

Furthermore, the trend of market penetration into lower-tier cities is becoming increasingly evident, with cost-effective and user-friendly procedures gaining widespread adoption first. Between 2018 and 2020, the number of newly registered enterprises related to “medical aesthetics” in lower-tier markets remained above 500 annually, marking a significant increase compared to 2016 and substantially improving the accessibility of China’s medical aesthetics industry in these regions. Meanwhile, enhanced information coverage in lower-tier markets has accelerated the growth of the industry’s influence and raised consumer awareness of medical aesthetic treatments.

Intensified market competition creates the possibility for lower end-user prices, while standardized industry development is transforming photoelectric treatments into mainstream, routine skincare procedures. On one hand, the rapid emergence of domestically produced devices in the photoelectric sector, coupled with the continuous entry of innovative foreign products into the Chinese market, will ultimately compel medical aesthetic device manufacturers to adjust their pricing strategies. This may even involve a shift from a high-consumable model to a low-consumable model, thereby creating room for downstream medical aesthetic institutions to reduce treatment prices. Currently, significant price reductions have already been observed for many photoelectric-based treatments on the market.

On the other hand, against the backdrop of increasingly stringent regulations in China’s medical aesthetics sector and growing consumer sophistication, industry operations will gradually shift from a marketing-driven inducement model to one led by consumer demand. Service packages will be designed to better align with the actual efficacy of products, and, provided pricing remains appropriate, energy-based device treatments will ultimately evolve into mainstream, routine maintenance procedures.

Second, energy-based medical aesthetic devices are in a window of opportunity for domestic substitution.The National Health Commission has issued a document indicating reduced budgets for public hospitals, which will impact pharmaceutical and medical device companies while favoring domestically produced equipment with more competitive pricing. Amidst this significant market substitution opportunity, an increasing number of enterprises, capital investors, and R&D and management talent are entering the field of photoelectric medical aesthetic devices.

Driven by stringent regulation and standardization in the medical aesthetics industry, the integration of diagnosis and treatment has become imperative. For this sector, the majority of consumers present with skin conditions that have not progressed to severe pathological stages but remain in relatively early phases. Meanwhile, these consumers exhibit a strong desire for aesthetic improvement and place greater emphasis on treatment efficacy. Without precise diagnosis as a foundation, there is a heightened risk of suboptimal therapeutic outcomes and poor consumer experience; for certain procedures, it may also increase operational risks. Therefore, skin diagnosis holds particular significance in the medical aesthetics industry, serving as a prerequisite for achieving effective treatment.

Furthermore, from the perspective of industry development trends, regulatory oversight is becoming increasingly stringent and policies are tightening. The medical aesthetics industry is gradually aligning with serious medical practice, leading to greater standardization of the entire patient care process. As a critical step linking clinical assessment with pathological analysis, diagnosis will become an indispensable component of future patient journeys. Consequently, the integration of diagnosis and treatment in the medical aesthetics sector has become an imperative trend.

Third, the combination of pharmaceuticals and medical devices strongly empowers the photoelectric energy-based device sector.The Limitation of a Single Business Model on the Market Size of Photoelectric Devices: Business Model Innovation Is the Key to Breaking Through. At present, the biggest challenge for photoelectric devices lies in their overly narrow commercialization scenarios, as they can only be deployed through hospital-based treatments. The lack of continuous management for end customers significantly constrains market size.

An analysis of the current market capitalizations of listed companies reveals that, compared to the ophthalmology and dentistry sectors—both of which are consumer healthcare markets valued at over RMB 100 billion—the energy-based device industry is currently undervalued, with leading overseas listed companies having market caps below RMB 10 billion. To overcome this challenge, a full-process business model may be the key to breaking through, effectively raising the ceiling for the industry’s growth scale.

The full-process model refers to providing an integrated solution spanning diagnosis, treatment, and postoperative recovery, while leveraging internet and digital platforms to offer comprehensive guidance and management for patients throughout their care journey, thereby effectively expanding the application scenarios of photoelectric medical aesthetics. In this new closed-loop system, a digital management platform serves as the essential foundation, and combination drug therapy is key to postoperative recovery and terminal-stage management.

Overall, the drug-device combination model is an inevitable path for optoelectronic equipment to break through its current market capitalization scale, although it remains in an early stage. For equipment manufacturers, proactively entering the pharmaceutical sector and exploring drug-device combination approaches can effectively strengthen competitive barriers and create greater growth potential.

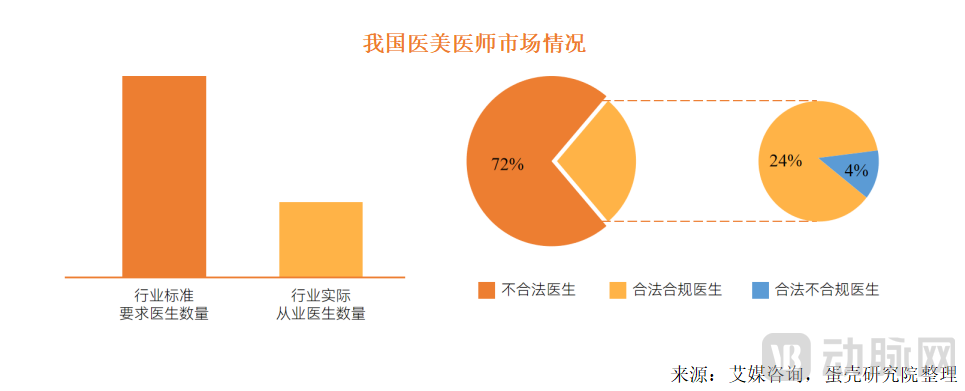

Fourth, the medical aesthetics industry faces a shortage of talent, and robotic technology may serve as an important solution.According to iResearch data, based on an estimate of 13,000 licensed medical aesthetic institutions, the demand for qualified physicians would be approximately 100,000 in the absence of multi-site practice arrangements. However, under multi-site practice policies, the actual number of practicing medical aesthetic physicians in China was only 38,000 in 2019. Amidst the industry’s sustained growth, the scarcity of top-tier doctors and the high profits offered by the black market have led to the frequent emergence of unlicensed practitioners. According to the Chinese Association of Plastics and Aesthetics (CAPA), the number of illegal practitioners in the medical aesthetics sector exceeds 100,000, with unlicensed doctors accounting for approximately 72% of the total workforce. Furthermore, out-of-scope practice is widespread, with about 4% of licensed physicians engaging in non-compliant procedures. These industry irregularities have resulted in frequent medical accidents and significant challenges for consumers seeking legal recourse.

In recent years, technological research and product development in the field of medical robotics have continued to advance, with surgical robots representing the largest and most significant segment within the medical robotics domain.

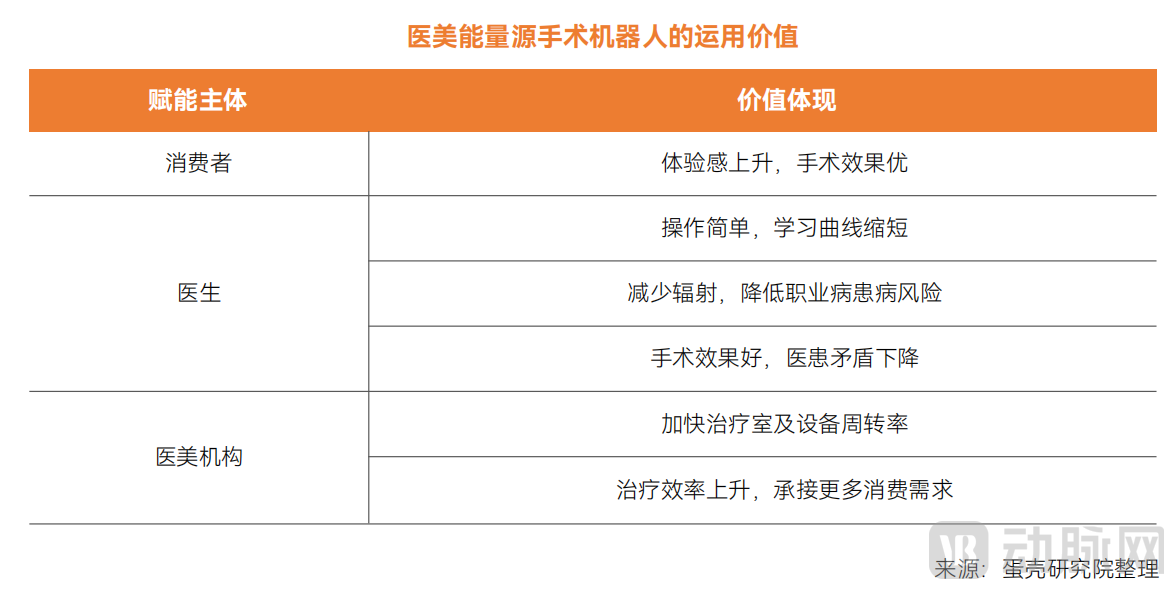

The core value proposition of surgical robots lies in achieving higher levels of automation, intelligence, and precision, which aligns perfectly with the development trends in the current niche segment of energy-based devices in medical aesthetics. Although current energy-based devices offer advantages such as ease of operation, minimal pain, rapid recovery, and low infection rates, they also present drawbacks including hand-eye coordination challenges for physicians, steep learning curves, susceptibility to fatigue, hand tremors, and potential compromise of surgical quality due to laser radiation. Energy-based surgical robotic systems not only preserve the technical advantages of energy-based devices but also enhance human-robot collaboration, offering benefits such as flexibility and convenience, resistance to fatigue and radiation, precise positioning, tremor filtration, and ease of learning.

The emergence and application of future energy-based surgical robots in medical aesthetics can significantly reduce overall surgical time, improve surgical efficiency, achieve standardization of procedures, and enhance surgical outcomes. For physicians, the proficiency that originally required years of specialized clinical training can now be achieved more readily; by utilizing surgical robots, doctors can perform procedures intuitively through control joysticks, substantially lowering operational difficulty and shortening the learning curve. Furthermore, robotic surgery is highly beneficial in reducing occupational hazards for physicians.

In summary, the era of minimally invasive aesthetic medicine has arrived. Amidst the overarching trends of technological iteration and increasingly stringent regulations, photoelectric aesthetic medicine enterprises that dare to innovate and continuously break through will ultimately rise to the forefront of industry development.

The report framework is as follows. Feel free to add the mini-program above to access the full report for free.