Butterfly Network's 90% Market Cap Drop and CEO Exit Highlight Challenges in Penetrating the Portable Ultrasound Blue Ocean

Butterfly Network

Developer of Artificial Intelligence Medical Imaging Equipment

Without Fosun’s RMB 700 million investment back then, Butterfly Network would by no means have become as widely recognized in China’s ultrasound community as it is today.

However, Todd Fuchterman, the CEO of Butterfly Network—a handheld ultrasound star company that had been successively favored by investment institutions and the industry—announced his resignation as CEO in late 2022. Meanwhile, more than 100 institutional investors also divested their stakes in the company during that year.

On February 6 this year, Butterfly Network’s closing price was $2.75, representing a 90% decline from its peak, with its market capitalization shrinking to just $550 million.

Regarding Butterfly’s predicament, some attribute it to regional barriers forged by the rampant spread of COVID-19, or to the poor economic conditions under the multiple global crises of 2022. However, its fall from grace may be more closely linked to the current state of development in the digital health sector as a whole.

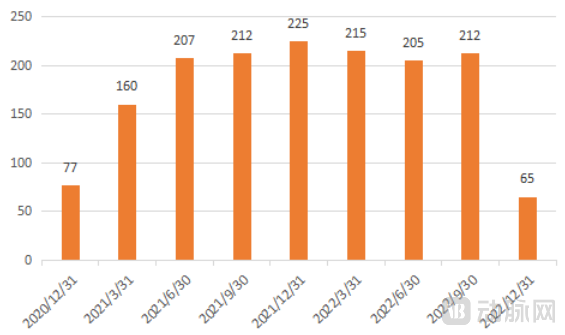

Butterfly: Institutional Shareholdings by Period (Data Source: Orient Securities)

In the year Butterfly was founded, handheld ultrasound devices received little attention, and there were few innovative products in the market. However, Butterfly chose to optimize the ultrasound imaging process and empower handheld ultrasound through an “AI-assisted diagnosis + semiconductor chip” approach. With this method, a handheld ultrasound device equipped with only a single probe can deliver imaging results comparable to those of traditional whole-body ultrasound systems that require multiple probes.

For the entire market at that time, this was undoubtedly disruptive. After all, hospitals have always sought to reduce equipment costs or improve convenience. Butterfly Network achieved high imaging quality while selling handheld ultrasound devices at a low cost, enabling more medical institutions to adopt handheld ultrasound technology.

This logic is highly compelling. In November 2017, Butterfly iQ received FDA clearance for market launch, becoming the world’s first FDA-cleared personal ultrasound device and the first single-probe ultrasound system capable of whole-body imaging. Having gained a first-mover advantage in commercialization, Butterfly’s future prospects are promising if it can capture the vast primary care market as anticipated in the near term.

In line with this vision, Butterfly Network accelerated its fundraising efforts and successfully went public via a SPAC in 2021, channeling additional capital into the sales of its current products and the R&D of its next-generation offerings.

Compared with various competitors in the ultrasound industry, Butterfly has a relatively weak product portfolio. Its currently marketed products include the Butterfly iQ and Butterfly iQ+ series, which serve obstetrics departments in general hospitals, primary care in resource-limited settings, veterinary medicine, and home healthcare scenarios.

Despite its limited product portfolio, Butterfly has demonstrated the revenue performance expected of a tech unicorn. From 2019 to 2021, the company generated revenues of $27.6 million, $46.3 million, and $62.6 million, respectively, corresponding to year-over-year growth rates of 68% and 35%. In the first nine months of 2022, it secured $54.41 million in revenue, and, barring any unforeseen circumstances, is on track to nearly meet its full-year revenue target of $73 million.

However, Butterfly’s profit conversion has not been as satisfactory as expected, with its rapid revenue growth coming at the cost of higher expenses. The company’s stock price peaked upon its IPO and subsequently experienced a nearly two-year gradual decline. Butterfly Network reported net losses of $99.7 million, $162.7 million, and $32.41 million in 2019, 2020, and 2021, respectively, and incurred a loss of $135 million in the first three quarters of 2022.

Butterfly Network’s handheld ultrasound devices are low-cost, and there is substantial demand in its target markets—regions with relatively scarce medical resources. However, reaching remote areas requires distribution through U.S.-based distributors, necessitating continuous expansion of its own distributor network to access more regions and countries. In this process, Butterfly Network not only incurs high costs for building its sales team but also assumes the risks of weak sales performance and legal liabilities in various regions and countries.

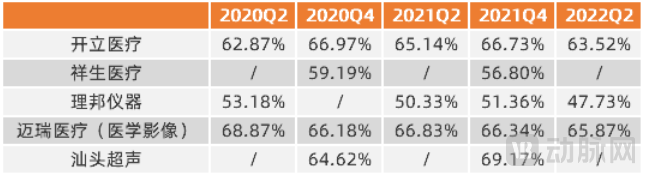

Not only did this suppress the sales price of its ultrasound devices, but Butterfly also sacrificed the product’s inherent profitability. An analysis of gross margin reveals that 30% of Butterfly’s revenue comes from software subscription services. In contrast, Mindray, Sonoscape, and ChaoShan UltraSound—the three companies dominating China’s domestic ultrasound market—maintain equipment gross margins in the range of 60%–70%, whereas Butterfly’s overall gross margin hovers between 50% and 55%.

Gross Profit Margins of Major Domestic Ultrasound Equipment Manufacturers: A Gap Between Tier 1 and Tier 2 Players

(Data sources: annual reports and prospectuses of respective companies)

Meanwhile, a significant portion of Butterfly Network’s revenue comes from its shareholder, the Bill & Melinda Gates Foundation, which procures devices through NGOs and distributes them charitably to healthcare institutions in need around the world. However, there are currently few NGO payers as generous as the Bill & Melinda Gates Foundation.

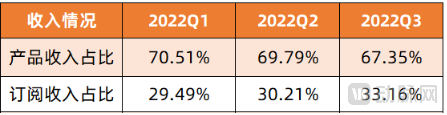

As for Butterfly Network’s subscription business, this segment represents one of its most promising areas. It has been on a growth trajectory since 2022, with related revenue gradually accounting for one-third of Butterfly Network’s total revenue.

Butterfly: Revenue Composition by Quarter in 2022 (Source: VCBeat)

On the other hand, the strategy of trading sustained high investment for market coverage will severely test Butterfly’s cash flow. As of September 2022, Butterfly had only $268 million in cash on hand; at its current burn rate, these funds would be exhausted within two years if expansion continued.

As of today, Butterfly Network is struggling to secure new investment. With only two years of runway remaining, the company faces the risk of a capital chain rupture unless it significantly reduces administrative expenses and slows its expansion pace.

Like many digital health companies, Butterfly Network has a self-consistent vision for cost reduction and efficiency improvement. However, while the logic of low costs is appealing, it also carries underlying risks.

In terms of ultrasound innovation, Butterfly Network leverages semiconductor chip technology, enabling a single probe to perform whole-body imaging. While entry-level ultrasound systems on the market previously cost $45,000–$60,000 and handheld ultrasound devices ranged from $30,000 to $40,000, Butterfly’s product achieves this capability for just $2,000, with greater ease of use. If the buyer is a newly established hospital, they would choose Butterfly’s ultrasound system without hesitation.

First, whole-body ultrasound is a product with high penetration in primary healthcare. Although Butterfly Network offers advantages in both portability and cost, product replacement does not happen overnight; rather, it follows a gradual progression that may even span a decade.

Secondly, it is necessary to clarify who the payer for ultrasound services is. For hospitals with the financial capacity to purchase equipment, Butterfly Network offers limited value in terms of performance and fails to meet the research needs of physicians; moreover, price is not a primary concern for these institutions.

A glimpse can be gained by referring to the ultrasound tendering and bidding data in the Chinese market.

According to public data disclosed on government procurement bidding websites from 2020 to 2022, not only tertiary hospitals but also a large number of secondary hospitals and private medical institutions began purchasing specialized ultrasound systems priced above RMB 2 million. In contrast, the procurement scale for conventional whole-body ultrasound systems and new portable ultrasound devices has shrunk, with particularly few hospitals acquiring portable ultrasound systems through open bidding channels.

The current challenge facing Butterfly Network is that the procurement demand for portable ultrasound devices is concentrated in markets such as Africa and South America, yet these regions often lack the funds to purchase large quantities of portable ultrasound equipment.

However, this is not the only issue facing Butterfly Network; another challenge that needs to be addressed, yet can be resolved through a singular approach, lies in supplier and market education.

In 2008, GE Healthcare’s first-generation handheld ultrasound device, the VSCAN 1.0, debuted in the U.S. market, causing an immediate sensation. It was subsequently named one of “The 50 Best Inventions of 2009” by TIME magazine and one of “The 100 Best Technological Achievements of 2010” by the renowned popular science magazine Popular Science, regarded as a groundbreaking product that ushered in a new era.

Unfortunately, GE Healthcare’s portable ultrasound devices have not sold well. After all, for a manufacturer specializing in comprehensive, large-scale medical imaging equipment, selling a low-priced small device yields significantly lower gross margins and profits for its internal sales teams and suppliers compared to selling major equipment. Therefore, although GE has continuously updated its handheld ultrasound products—most recently launching the wireless handheld Vscan Air series in 2021—handheld ultrasound remains positioned merely as a “product line supplement.” Regardless of the high acclaim it has received from the industry or the substantial real-world market demand, this situation is difficult to change.

For this reason, GE Healthcare has not provided a market education system to support handheld ultrasound devices, leaving the sector—a blue ocean within the industry—largely untapped even more than a decade after the emergence of handheld ultrasound technology.

For Butterfly, the choice is either to invest heavily in market education—a “public good” that would benefit all competitors—or to wait for the slow adoption of handheld ultrasound devices. The former means adding further pressure to already tight cash flows and bearing competitive risks, while the latter requires the company to tolerate limited market expansion speed and hope to secure new financing before running out of funds.

A Summary of the Current Dilemmas Facing Butterfly Network.

First is the equipment. The future development of ultrasound devices includes portability and high-end specialization, with portable devices entering home healthcare scenarios and high-end devices shifting from whole-body examinations to specialized treatment. The difference between the two paths lies in the fact that mid-to-high-end equipment contributes the majority of the ultrasound market size, so related technological research and development as well as sales promotion will be faster.

Although the Chinese ultrasound market does not fully reflect global development trends, it still holds certain reference value. According to VCBeat’s analysis of ultrasound procurement data from the China Government Procurement Network between January 1, 2020, and December 31, 2022, the emergence of the COVID-19 pandemic accelerated the construction of a new public health system in China, with the volume of ultrasound procurement projects increasing continuously at a rate exceeding 20%.

Two points warrant attention. First, procurement projects for high-end ultrasound systems priced above RMB 2 million account for the largest share of all publicly announced projects, with procurement volumes continuing to rise. In contrast, procurement volumes for portable and handheld ultrasound devices have shown limited change; in 2022, there were a total of 2,654 procurement records, yet the number of projects specifically for handheld ultrasound devices did not exceed 100.

Second, the vast majority of incremental growth over the past three years has come not from tertiary hospitals but from county-level hospitals and community health centers. In other words, it is unrealistic to expect handheld ultrasound devices to replace whole-body ultrasound systems, as budget allocations for equipment upgrades are increasingly being captured by high-end ultrasound platforms. Compared with handheld ultrasound, which is viewed primarily as a cost item, hospitals prefer to invest in whole-body ultrasound systems that can generate revenue.

Therefore, for hospitals, the adoption of more convenient and affordable handheld ultrasound devices has received critical acclaim but failed to achieve strong market uptake.

Revisiting Butterfly Network’s Digital Health Segment. A review of the investment logic in serious healthcare over the past decade shows that this emerging sector once reached a level of hype comparable to high-end pharmaceuticals and medical devices, but gradually lost momentum after 2020. Ultimately, digital health cannot follow the same logical framework as high-end pharmaceuticals and medical devices.

The R&D of high-end pharmaceuticals and medical devices targets existing markets with proactive purchasing demand, pursuing superior therapeutic efficacy. In contrast, digital health often needs to create demand, gradually integrating into clinical workflows through the logic of “cost reduction and efficiency enhancement” and “broad accessibility.”

Since the demand for cost reduction and efficiency improvement is not rigid, the value generated through broad outreach is difficult to equate with that of offline medical services. The fluctuations in the medical AI sector over the past decade have demonstrated that while the implementation of digital healthcare is inevitable, it is a long-term and subtle process. Large-scale financing can help companies rapidly launch products, but it struggles to assist them in educating and capturing the market—the development of medical technology requires time and careful validation.

In retrospect, the handheld ultrasound market targeted by Butterfly Network is indeed a promising blue ocean. If it can reach an agreement with investors to appropriately slow its pace and amortize the costs associated with payer engagement and market education over a longer period, Butterfly Network may lose some market share but could nonetheless navigate the early stages smoothly.

Certainly, Butterfly Network is not the only company facing this decision. Digital health, mired in a quagmire, needs to recalibrate its pace, endure the darkness, and reach the dawn.