Domestic CGM Leader Enters the Fray as New Guidelines Propel Market Growth: Can Abbott Maintain Its Dominance?

Sinocare

Rapid Detection of Chronic Disease: Product R&D, Production, and Sales

Over the past year or so, despite the successive approvals of multiple domestically produced continuous glucose monitoring (CGM) systems, the market has remained largely stagnant. This is because Abbott’s FreeStyle Libre series, leveraging its first-mover and channel advantages, has firmly dominated the market with a share approaching 80%. Among domestic brands, although products from companies such as Yuwell Medical, MicroTech Medical, and Silicon Bioimitation possess certain distinctive advantages, their overall market share remains relatively low, and they have yet to make a significant impact in the market.

On one hand, the penetration rate of continuous glucose monitoring (CGM) in China is less than 5%, whereas it has exceeded 20% in developed countries in Europe and the United States. The entire CGM market is in an early stage of accelerated growth, with substantial room for future expansion. On the other hand, current market entrants appear unable to challenge Abbott’s dominant market position.

Amid the stalemate, the market is poised to welcome a major new player. Sinocare, the leading domestic manufacturer of blood glucose meters, announced that its self-developed continuous glucose monitoring (CGM) product is expected to receive regulatory approval in the first quarter of 2023. Furthermore, the recent release of the American Diabetes Association (ADA)’s 2023 Standards of Care in Diabetes has provided a significant boost to the development of CGM technology.

In 2023, the CGM market will witness a distinctive spark.

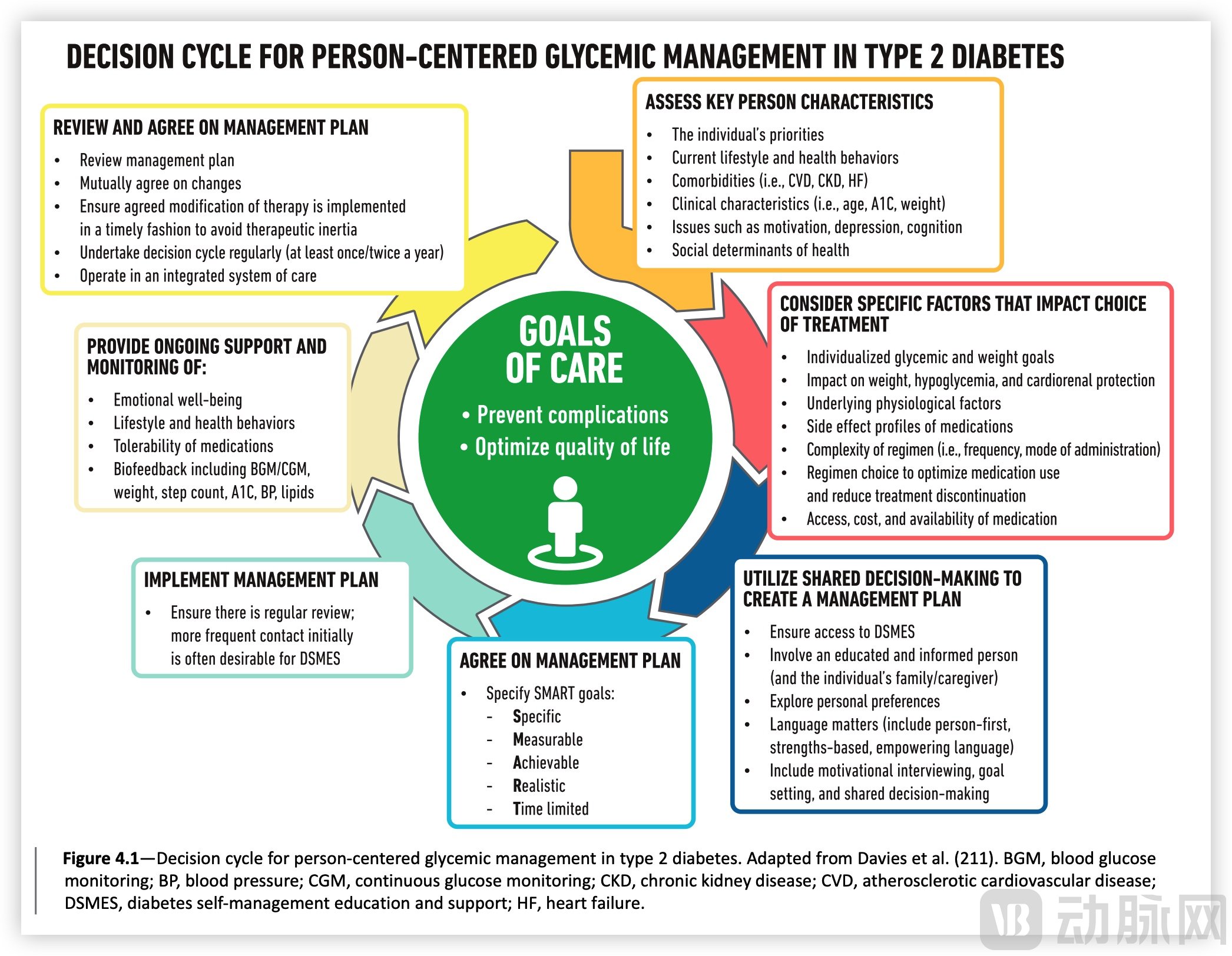

Recently, the American Diabetes Association (ADA) released the 2023 edition of the "Standards of Care in Diabetes." The most notable update is the continued elevation in the status of Continuous Glucose Monitoring (CGM) systems, which now hold a position on par with Blood Glucose Monitoring (BGM) via fingerstick testing.

Glucose Management Decision Cycle Incorporates CGM for the First Time, Image Source: ADA 2023 Guidelines

The 2023 edition of the guidelines affirms the critical role of continuous glucose monitoring (CGM) in glycemic management, noting that CGM-derived glycemic metrics and novel glucose reporting formats are gaining increasing clinical recognition. Since the guidelines first incorporated time in range (TIR) as a control metric in 2020, explicitly recommended TIR as one of the glycemic control targets in 2021, and further affirmed and reinforced the importance of CGM, its reports, and associated metrics in glycemic assessment in 2023.

The guidelines emphasize that standardized one-page glucose reports with visual cues derived from continuous glucose monitoring (CGM), such as the Ambulatory Glucose Profile, should be considered the standard printout for all CGM devices. Time in Range (TIR) is associated with the risk of microvascular complications and can be used to assess glycemic control.

When using continuous glucose monitoring (CGM) metrics to assess glycemic control, the appropriate targets for most non-pregnant adult patients are time in range (TIR) >70%, time below range (TBR) <4%, and TBR (<3.0 mmol/L) <1%. For frail patients or those at high risk of hypoglycemia, the recommended glycemic targets are TIR >50% and TBR <1%.

The control target for GMI is <7%.

In addition to the overall assessment, the guidelines also provide many specific recommendations for the use of CGM, based on the target population, timing of use, and usage scenarios, including:

For patients with type 1 and type 2 diabetes receiving insulin therapy, as well as special populations such as adolescents and pregnant women.

Patients already using continuous glucose monitoring (CGM), continuous subcutaneous insulin infusion, and/or automated insulin delivery for diabetes management should continue their use, regardless of age or A1C levels.

Schools must support students’ use of diabetes treatment devices on campus, including continuous glucose monitors (CGMs), insulin pens, and automated insulin delivery systems.

For patients with diabetes treated with multiple daily injections or continuous subcutaneous insulin infusion, real-time CGM or intermittently scanned CGM should be used for diabetes management.

Adolescents with type 1 diabetes who use multiple daily injections or continuous subcutaneous insulin infusion and can safely use the devices should utilize real-time CGM or intermittently scanned CGM for diabetes management.

For adolescents with type 2 diabetes, real-time CGM or intermittently scanned CGM should be used for diabetes management when multiple daily injections or continuous subcutaneous insulin infusion are employed and devices can be used safely.

Regarding the timing of use, the new guidelines also provide clear recommendations. The general principle is to initiate early and maintain continuous use, ensuring that patients receive optimal care.

Regarding usage scenarios, the new guidelines explicitly support the continued use of continuous glucose monitoring (CGM) devices by hospitalized patients with diabetes, and particularly emphasize the advantages of CGM devices in the hospital setting during the pandemic. Furthermore, the new guidelines provide warnings about common issues associated with CGM use, such as allergic skin reactions and the impact of medications on device readings.

Overall, in the latest edition of the *Standards of Medical Care in Diabetes*, continuous glucose monitoring (CGM) is playing an increasingly significant role in diabetes management, with its user base, scope of application, and usage scenarios approaching parity with traditional blood glucose monitoring (BGM). Endorsed by the new guidelines, global diabetes guidelines in various regions will likely draw on this framework in the coming years to keep pace with evolving trends. For the CGM industry, this signals further market expansion in the near future.

In July 2022, Sinocare announced that its real-time continuous glucose monitoring (CGM) system had received a “Notice of Acceptance” for its medical device registration application from the National Medical Products Administration (NMPA). In its latest investor activity record, Sinocare disclosed that the product was expected to obtain NMPA approval in the first quarter of 2023.

China’s CGM Market Finally Welcomes a Major Player.

Since its founding in 2002, Sinocare has grown over two decades to become a leading enterprise in China’s domestic blood glucose monitoring sector. The company holds over 50% of the retail market share for blood glucose meters in China, serves more than 20 million users, and its blood glucose meter products are available in over 180,000 pharmacies.

Building on its strong performance in China, Sinocare has established eight production bases and seven major R&D centers worldwide over the years. Its business now spans 135 countries and regions globally. With a multidisciplinary R&D talent pool and a robust, efficient research and development system, Sinocare has emerged as a leading enterprise in the field of diabetes and related chronic disease monitoring.

It is precisely due to its deep commitment to its core sector that Sinocare recognized the limitations of traditional BGM at an early stage and began investing in CGM technology R&D in 2009, undergoing an evolution from first-generation to third-generation technology.

Furthermore, the development of globalization has led Sinocare to prioritize the establishment of a global quality system from the outset of its CGM product R&D efforts, achieving quality compliance and product certification in major markets worldwide. In the second quarter of this year, Sinocare will initiate the FDA and CE certification application processes for its CGM products.

In the domestic market, several domestically produced continuous glucose monitoring (CGM) products have been approved for launch, including those from companies such as Canwell, Joynow Medical, MicroTech Medical, and Silicon Based Sensing. However, most of these firms are startups constrained by hard limitations in technical capabilities, production capacity, and channel development, leaving them unable to challenge Abbott, the international giant that currently holds nearly 80% of the market share.

In recent years, several listed companies, including Lepu Medical, Andon Health, Sinocare, and Cofoe Medical, have successively announced their in-house development of continuous glucose monitoring (CGM) systems. Currently, Sinocare has established the most comprehensive layout, with thorough preparations spanning from technology to distribution channels, thereby laying a solid foundation for the upcoming commercialization of its products.

The biggest technological barrier for CGM is the sensor, and it is Sinocare that is leading the latest technological revolution in sensors.

The first-generation sensors, represented by Dexcom, integrate O2As an electron transfer mediator, this technology is limited by the high impurity levels and low O2environment, which imposes stringent requirements on the outer membrane and results in higher production costs. The second-generation sensing technology, represented by Abbott, employs artificial redox mediators as electron transfer agents, thereby fundamentally eliminating interference from impurities and O2concentration limits, while reducing production costs.

Faced with the established dominance of multinational industry leaders, Sinocare chose not to follow suit but instead pursued independent research and development of its third-generation sensor technology—direct electron transfer technology. By modifying glucose oxidase to enable direct electron transfer capability, this technology operates without reliance on electron mediators. It offers high glucose oxidation efficiency and boasts advantages such as low potential, oxygen independence, minimal interference, and superior stability and accuracy.

Supported by next-generation sensors, Sinocare’s CGM has achieved a MARD value of 7.9%—a core metric for evaluating product accuracy—marking the best performance among current domestic products and matching that of Abbott’s FreeStyle Libre 3, which received FDA approval in 2022 (the version marketed in China is the first-generation FreeStyle Libre). Features now widely adopted in the industry, such as fingerstick-free calibration, fixed-frequency automatic blood glucose data recording, long-term continuous monitoring, and real-time data reception and alerts on mobile phones, are naturally well within its capabilities.

Major CGM Products in the Domestic Market; Data Compiled from Public Sources

To achieve these goals, technical challenges such as sensor outer membranes, calibration algorithms, enzyme technology, and manufacturing processes must be overcome. To this end, Sinocare has established an R&D team comprising experts from multiple disciplines, including chemistry, physics, biology, medicine, materials science, and computer science. According to the company’s financial reports, in the first half of 2022 alone, its 808 R&D personnel accounted for 22.52% of the total workforce, with R&D expenditures reaching nearly RMB 120 million, representing 9.25% of total revenue.

Not only has it achieved breakthroughs in sensor technology, but Sinocare has also made strategic moves in the hybrid closed-loop system that integrates CGM with insulin pumps, a key direction for the development of digital diabetes solutions.

In 2021, Sinocare established a strategic partnership with South Korea’s EOFLOW Co., Ltd., and in January 2022, founded the Sino-foreign joint venture Changsha Funuo Medical Technology Co., Ltd. EOFLOW’s flagship product is the EOPATCH, a disposable patch insulin pump. Currently, the joint venture’s R&D team is systematically advancing the domestic registration of related products. In the future, leveraging the application of Sinocare’s CGM products, Changsha Funuo will strategically position itself in the field of smart wearable insulin pumps, committed to evolving from wearable insulin pumps to wearable artificial pancreas solutions. Sinocare aims to provide innovative and systematic smart healthcare product solutions for patients with diabetes.

As can be seen, Sinocare’s layout in the CGM sector is both meticulous and comprehensive. By achieving breakthroughs in underlying technologies to develop high-performance products, and by strategically positioning itself in areas of external expansion ahead of time, the company is well-prepared for future growth. In other words, Sinocare is not merely covering niche segments; rather, it views CGM as a crucial second growth curve and has implemented a complete strategic deployment to support this vision.

In China’s CGM market, Abbott dominates. This is partly due to its first-mover advantage and partly because Abbott’s distribution channels are on an entirely different scale compared to those of startups.

Given the current limited awareness of continuous glucose monitoring (CGM) among patients in China, product selection largely depends on physician education. Physicians’ endorsement of a product requires long-term clinical observation. From product development to market education, and from market promotion to comprehensive digital services, robust product assurance and rapid iteration capabilities are essential to gain recognition from experts.

Achieving these goals is challenging for startups, but relatively easier for Sinocare.

Sinocare began its online sales operations in 2014. Through years of exploration, it has established more than 300 online teams, achieving rapid growth in its market share on the online retail front. According to Tao Data, Sinocare’s blood glucose meters accounted for 32.4% of sales on the Taobao platform in 2021, solidifying its position as the undisputed industry leader.

Not limited to online channels, Sinocare has, through years of dedicated efforts, provided relevant products and services to more than 3,000 tiered hospitals and over 6,000 medical institutions. With its brand building now relatively well-established, these in-hospital networks will facilitate the promotion of its CGM products in the future. According to product registration filings, Sinocare’s CGM products are categorized into Model I for individual use and Model H for hospital use. Upon future approval, these products will enter both the hospital and retail markets in China simultaneously.

Currently, Sinocare covers 180,000 offline pharmacies and has over 20 million users. This scale of channel network and potential customer base is Sinocare's most obvious advantage compared to startups. The domestic CGM market, which startups have been unable to disrupt, may see a different kind of power emerge with Sinocare's entry.

Not only in China, but Sinocare has also made significant strides in overseas markets.

Since initiating its global business expansion in 2016, Sinocare has successively acquired Trividia Health Inc. and PTS in the United States. As the sixth-largest blood glucose meter manufacturer worldwide, Trividia boasts a well-established sales network in the U.S., enabling Sinocare’s continuous glucose monitoring (CGM) products to enter the American market under Trividia’s brands in the future. Meanwhile, more than 40% of PTS’s revenue is derived from markets outside the United States. Its global sales channels, supply chain resources, brand assets, and extensive international operational and sales experience accumulated over many years will all contribute to the promotion of CGM products.

In addition to traditional sales channels, Sinocare’s cross-border e-commerce business has established independent self-built websites in European languages such as German, French, and Spanish. Meanwhile, it operates stores on third-party international platforms including eBay, Amazon, AliExpress, Shopee, Lazada, Cdiscount, Jumia, and Joom. Its business covers more than 200 countries and regions, including Germany, France, Italy, Spain, Portugal, the United Kingdom, Russia, Japan, Canada, and the United States. Sinocare has partnered with overseas warehouses in 17 countries across Europe, North America, and Southeast Asia, achieving localized logistics.

Unlike nascent CGM startups that must build their sales networks from the ground up for commercialization, Sinocare boasts a premium existing channel network, with its reachable customer base highly overlapping with the target demographic for CGM products. Upon regulatory approval and market launch, the combination of superior product performance and extensive distribution channels will undoubtedly deliver a significant impact on the current market.

Economies of scale are a powerful tool for leading enterprises to capture market share.

Taking Abbott as an example, its reported annual sales data showed that revenue from diabetes care reached $4.756 billion in 2022, with each quarter consistently contributing over $1 billion in sales, the majority of which was generated by continuous glucose monitoring (CGM) systems. In the Chinese market, however, there is a substantial disparity in scale: MicroTech Medical’s sales exceeded RMB 12 million in the first half of 2022, while SiBionics surpassed RMB 50 million during the same period.

The disparity in scale results in differences in cost.

From a pricing perspective, although most domestic products are listed at over RMB 600, the actual transaction prices generally range between RMB 300 and RMB 400, indicating no significant price gap between Chinese brands and Abbott. Industry insiders note that it is already challenging for domestic CGM manufacturers to match Abbott’s pricing levels. This is because Abbott benefits from higher shipment volumes and larger production scales, which naturally result in lower per-unit costs.

The reason Abbott has not yet wielded the stick of price wars is that there are currently no competitors in the market capable of challenging its position.

Currently, Sinocare has established two production lines for its CGM products. The semi-automated production line has been completed and put into operation, with an expected capacity of 2 million units. The fully automated production line will offer greater production capacity, and its output will be dynamically adjusted based on business development after the future launch of the CGM products.

We extrapolated based on the data from another listed company, MicroTech Medical. In the first half of 2022, its CGM product sales amounted to approximately RMB 13 million. Assuming full-year sales of RMB 26 million and an average transaction price of RMB 300 per unit, the annual sales volume would be around 100,000 sets. Given Sinocare’s existing offline distribution network covering 180,000 pharmacies and its production capacity reserves, Sinocare’s projected sales scale is expected to far exceed this figure.

BGM Selling Prices, Data Sourced from Tmall

Drawing on Sinocare’s strategy in the BGM sector, where annual production of blood glucose test strips exceeds 2 billion units, the company leverages economies of scale to reduce costs and compete with rivals through more advantageous pricing, intensifying market competition. It is foreseeable that the launch of Sinocare’s related products will bring a long-awaited surge of activity to the CGM market.