Trillion-Dollar Pharmaceutical Retail Market Transformed as New Medical Insurance Policy Drives Surge in Pharmacy Reimbursements and Stock Prices

On the morning of February 16, the pharmaceutical commerce sector surged: shares of Yixintang, Yifeng Pharmacy, and Jianzhijia hit their daily upper limits, while Shuyu Pingmin, Dashenlin, Laobaixing, and First Medicine posted gains.

On the evening before, the National Healthcare Security Administration issued the “Notice on Further Improving the Inclusion of Designated Retail Pharmacies in Outpatient Pooling Management” (hereinafter referred to as the “Notice”), actively supporting designated retail pharmacies in launching outpatient pooling services. This means that after the implementation of the new policy, patients can purchase drugs covered under the outpatient pooling scheme at designated pharmacies and enjoy the same reimbursement policies as those at designated hospitals.

Currently, the reform of mutual aid for outpatient medical insurance has been launched, with a reduction in individual accounts and an increase in pooled funds. The increased portion will be used for outpatient pooling. Pharmacies are widely distributed and located close to residential communities, providing significant convenience for patients in purchasing medications and obtaining reimbursements.

Outpatient services cover a large patient population, with higher visit frequencies compared to inpatient care. The inclusion of pharmacies in the outpatient pooling reimbursement system presents another opportunity for prescription outflow. Seizing this opportunity, the pharmaceutical retail market is on the verge of a significant transformation.

The inclusion of pharmacies in the outpatient pooling system is a key component of the medical insurance outpatient mutual aid reform.

In 2021, the General Office of the State Council issued the Guiding Opinions on Establishing and Improving the Outpatient Mutual Aid Security Mechanism for Employee Basic Medical Insurance, which proposed at that time to improve the method of crediting funds into individual accounts. After adjusting the structure of the pooled fund and individual accounts, the increased pooled fund is primarily used for outpatient mutual aid security. According to policy planning, in addition to including ordinary outpatient medical and pharmaceutical expenses within medical institutions in the pooled payment system, medication security services provided by designated retail pharmacies that meet specified conditions are also to be included within the scope of outpatient security.

Since 2022, outpatient mutual-aid reforms have been officially launched in many regions across China. In 2023, the method of allocating funds to individual accounts underwent corresponding changes in multiple pooling areas: employer contributions to basic medical insurance are no longer credited to individual accounts but are instead allocated to the pooled fund.

As a key supporting measure for the outpatient mutual aid policy, the inclusion of pharmacies in the outpatient pooling system must also be accelerated. The Notice on Further Improving the Management of Designated Retail Pharmacies Included in the Outpatient Pooling System, issued by the National Healthcare Security Administration on February 15, 2023, marked a critical milestone in accelerating the implementation of these supporting measures.

In fact, prior to this, provinces such as Hebei, Sichuan, and Hubei had already taken action by formulating detailed implementation rules for outpatient mutual aid insurance coverage and establishing conditions for including pharmacies in the outpatient pooling system.

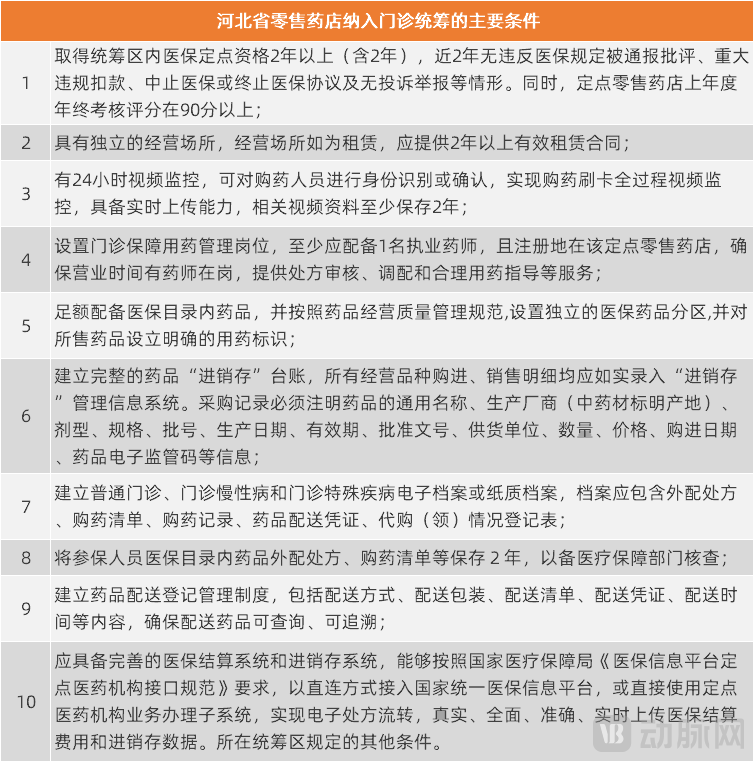

In May 2022, the Hebei Provincial Healthcare Security Administration issued the “Notice on Including Eligible Designated Retail Pharmacies in the Outpatient Care Coverage,” which outlined ten criteria for pharmacies to participate in the outpatient pooling fund and set forth plans to progressively launch pilot programs and expand the scope of participating pharmacies.

Key Criteria for Including Retail Pharmacies in Hebei Province’s Outpatient Pooling System, Source: Hebei Provincial Healthcare Security Administration

In accordance with the requirements, pharmacies must meet certain standards in terms of designated medical insurance qualification, information systems, pharmacist staffing, and operational management practices before they can apply to the medical insurance authorities. Among these requirements, pharmacies must have held designated medical insurance status within the pooling area for at least two years (inclusive), and must have no record of regulatory violations in the past two years, such as public censure for breaching medical insurance regulations, significant fines for non-compliance, suspension or termination of medical insurance services or agreements, or any complaints or reports. Additionally, designated pharmacies must have achieved a year-end assessment score of 90 or above in the previous year.

As of December 2022, there were a total of 421 retail pharmacies providing outpatient insurance coverage across Hebei Province, achieving full coverage in all counties, districts, and county-level cities.

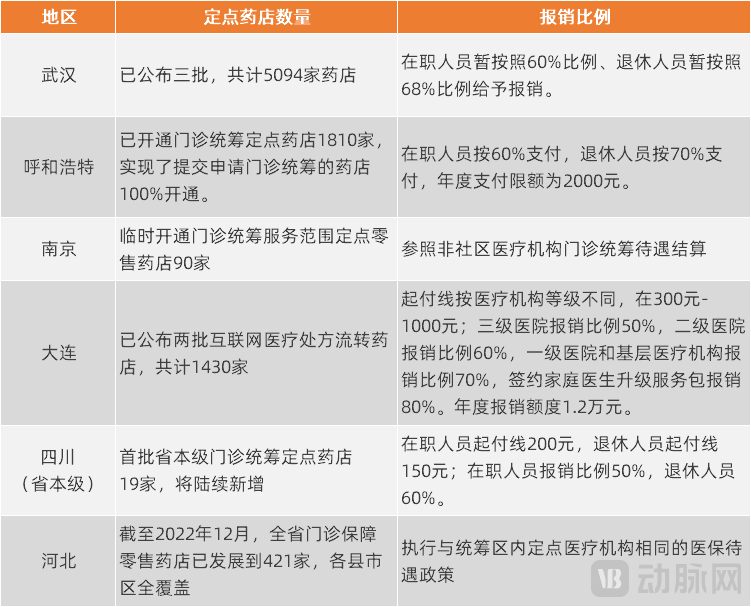

Since 2023, cities including Wuhan, Hohhot, and Dalian have launched or expanded outpatient pooling payment services at a large number of pharmacies. According to recent publicly available statistical data, at least 8,000 pharmacies have been included in the outpatient pooling system.

After launching settlement services for 1,295 designated retail pharmacies under the employee outpatient pooling scheme in October 2022, Hohhot added another 515 pharmacies in February 2023, thereby covering all pharmacies that had submitted applications.

Wuhan has not only implemented policies rapidly but also involved a large number of pharmacies in the process. On February 13 and 15, 2023, two batches of designated retail pharmacies for outpatient pooling were announced within three days, comprising 1,000 and 4,065 pharmacies respectively. Including previously published lists, the total number of designated pharmacies has reached 5,094.

Furthermore, Sichuan has designated the first batch of 19 provincial-level pharmacies for outpatient pooling reimbursement, with additional pharmacies to be added in subsequent phases.

Number of Designated Pharmacies and Reimbursement Policies for Outpatient Pooling in Certain Regions, Source: Local Healthcare Security Administrations

Meanwhile, various regions have also established deductibles, reimbursement rates, and payment caps for purchasing medications at designated pharmacies.

Overall, designated retail pharmacies refer to the reimbursement policies of designated medical institutions, as seen in Hebei and Dalian.

Compared with inpatient care, outpatient visits involve significantly higher frequencies and patient volumes. Following the implementation of the new policy, the expenditure status of the medical insurance fund remains to be observed; consequently, some regions have adopted more conservative reimbursement standards. For instance, the provincial-level basic medical insurance scheme in Sichuan Province follows the reimbursement criteria for tertiary medical institutions, resulting in lower reimbursement rates compared to those for medical institutions of other tiers.

In accordance with the requirements of the “Notice,” medical insurance departments in pooling regions shall scientifically prepare annual budgets for outpatient medical insurance fund expenditures, taking into account recent local outpatient cost trends, as well as factors such as the number of insured persons, age structure, changes in disease spectrum, benefit levels, and policy adjustments.

It is worth noting that the Notice also states that designated retail pharmacies participating in outpatient pooling may implement medical insurance reimbursement policies—such as deductibles, reimbursement rates, and maximum payment limits—that are identical to those applicable to designated primary healthcare institutions within the same pooling area.

To promote tiered diagnosis and treatment, the reimbursement rate for primary healthcare institutions is the highest among all levels of medical institutions under the overall principles of medical insurance payment. Therefore, the "Notice" leaves room for subsequent reimbursement standards for pharmacies.

Prior to the implementation of the outpatient pooling policy, pharmacies already had two main channels for pooled fund payments: outpatient coverage for chronic and special diseases, and the “Dual Channel” mechanism. Together with these two major channels, outpatient pooling will constitute a powerful driver of pharmacy growth.

Regarding chronic and special diseases, to meet the daily medical treatment and medication needs of patients with these conditions, the basic medical insurance system has established corresponding outpatient coverage mechanisms. For designated chronic and special disease categories, patients may purchase medications at designated retail pharmacies using prescriptions issued by designated medical institutions for outpatient care of chronic and special diseases, with reimbursement settled through the pooled fund according to the same standards.

Regarding the “Dual-Channel” mechanism: In May 2021, the National Healthcare Security Administration initiated the establishment of the “Dual-Channel” mechanism. This approach aims to meet reasonable demands for the supply, guarantee, and clinical use of negotiated drugs through two channels—designated medical institutions and designated retail pharmacies—while simultaneously incorporating them into medical insurance reimbursement. For drugs included in the “Dual-Channel” management, a unified reimbursement policy is implemented across both designated medical institutions and designated retail pharmacies.

In the past, patients could only have medicines covered by the National Reimbursement Drug List (NRDL) reimbursed through medical insurance when purchased at designated hospitals, where stockouts were not uncommon. With the implementation of the "Dual Channel" policy, patients can now purchase these medicines through two channels—hospitals and designated "Dual Channel" pharmacies—with reimbursement provided at the same rate. This has diversified and streamlined access to medications for patients, better meeting their pharmaceutical needs.

For pharmacies, especially specialty pharmacies, the traditional model primarily involved collaborating with innovative pharmaceutical companies to fulfill a portion of prescriptions diverted from hospitals. Following the implementation of the “Dual-Channel” policy, medical insurance reimbursement has enabled pharmacies to access a larger patient base.

Since the implementation of the above two types of policies, pharmacies have actively sought designated insurance provider status; multiple listed chain enterprises have expressed a strong willingness to integrate with pooled payment systems in their financial reports and disclosed the corresponding number of pharmacies.

As of September 2022, Laobaixing Pharmacy operated a total of 10,327 stores, including 789 stores qualified for pooled medical insurance reimbursement for special outpatient services and 181 “dual-channel” stores. During the same period, among Jianzhijia’s 3,691 pharmaceutical retail outlets, there were 529 stores covered by medical insurance for chronic diseases, 99 stores covered by medical insurance for special diseases, and 121 “dual-channel” pharmacies.

As of June 2022, among Yifeng Pharmacy’s 7,684 directly operated stores, 1,006 were designated outlets for the pooled fund covering chronic and special diseases under medical insurance; among Yixintang’s 8,990 directly operated stores, 901 were designated outlets for chronic disease management under medical insurance, and 204 were “Dual-Channel” stores.

Designated qualification for outpatient pooling will become another channel for pharmacies to receive pooled fund payments, further expanding their patient base.

In accordance with the reform plan for outpatient mutual aid under the basic medical insurance scheme, and on the basis of ensuring adequate coverage for outpatient chronic and special diseases that impose a heavy financial burden on the public, such as hypertension and diabetes, expenses for ordinary outpatient visits for frequently occurring and common diseases will be gradually included in the scope of reimbursement from the pooled fund.

In other words, outpatient coverage for chronic and special diseases, along with the “dual-channel” policy, primarily targets chronic conditions, special diseases, critical illnesses, and even rare diseases; whereas the general outpatient pooling scheme will cover patients with frequently occurring and common diseases, encompassing a much larger patient population.

Currently, there are nearly 400,000 pharmacies designated for national medical insurance coverage across China. These pharmacies are widely distributed, highly market-oriented, and offer diverse and convenient services. Some industry practitioners believe that the recent "Notice" further clarifies the roles of prescription circulation platforms and long-term prescriptions, thereby facilitating the outflow of prescriptions from hospitals. However, other industry insiders note that the role assigned to retail pharmacies under the outpatient mutual aid reform is largely consistent with that of "dual-channel" pharmacies: medical institutions remain the primary channel, while retail pharmacies serve as a supplement.

However,The opportunities brought to pharmacies by the new policy are not limited to the outflow of prescriptions and patients themselves, but also lie in the expanded value-added services.

In practice, most pharmacies leverage medical insurance payment as an entry point to provide patients with more in-depth services. By enhancing their professional capabilities through health management, chronic disease management, and pharmaceutical care services, they strengthen patient loyalty and thereby increase sales opportunities.

For these pharmacies, medical insurance reimbursement serves both as a service and a customer-acquisition strategy; while they rely on such reimbursements, they also need to reduce their revenue dependence on medical insurance.

According to data from Menet, China’s pharmaceutical retail market reached RMB 1.7747 trillion in sales in 2021, with an overall industry growth rate of approximately 8.0%. Among this, retail pharmacy sales amounted to RMB 477.4 billion, representing a year-on-year increase of 10.3%. The growth rate in the retail channel was faster than the overall industry average.

At this stage, “dual-channel” pharmacies are still being rolled out across China, and outpatient pooling has also rapidly gained momentum. Driven by the “three pillars” of outpatient care for chronic and special diseases, the “dual-channel” mechanism, and outpatient pooling, the scale of off-hospital pharmaceutical retail is expected to expand further.

While accelerating the outflow of prescriptions presents significant opportunities, outpatient pooling also poses greater challenges and higher demands for pharmacies.

In the past, numerous obstacles hindered the promotion of prescription outflow, stemming from the divergent interests of patients, medical insurance authorities, and healthcare institutions. Patients seek more convenient and professional pharmaceutical services; medical insurance authorities aim to “achieve more with less spending,” that is, to enhance coverage capabilities while ensuring the safe and sustainable operation of medical insurance funds; meanwhile, healthcare institutions lack clear incentives for prescription outflow and may even resist it.

Currently, the policy framework has been established, but there is still much for pharmacies to do.

For example,Attract patients with more competitive pricing, and secure reasonable costs and profit margins through centralized procurement.

Due to differences in procurement channels, drug retail prices vary among pharmacies and between pharmacies and medical institutions. In response, healthcare security authorities will reference drug prices at public medical institutions to negotiate with designated retail pharmacies and determine the selling prices of drugs included in the National Reimbursement Drug List, thereby minimizing drug costs as much as possible. Furthermore, they will strengthen coordinated price management between designated medical institutions and designated retail pharmacies to ensure more reasonable drug pricing in both hospitals and pharmacies.

Meanwhile, healthcare security authorities also encourage or organize designated pharmacies to participate in centralized procurement to reduce drug prices.

In fact, some pharmacies have already participated in various types of centralized volume-based procurement (VBP). For pharmacies, entering the outpatient pooling system requires balancing the profit margins of VBP drugs against the potential increase in patient volume. Although VBP may reduce profit margins, lower prices could also attract more patients.

Pharmacies also need to offer more comprehensive professional services to retain patients.

Pharmaceuticals plus management services have become a standard offering in many pharmacies. These services extend beyond one-time medication consultations, focusing instead on disease management and long-term guidance to maintain ongoing engagement with patients. Such services help improve patients’ medication adherence and repurchase rates.

Pharmaceuticals plus insurance is another innovative professional service. Large chain pharmacies can leverage their accumulated pharmaceutical operation data to collaborate with insurance companies and third-party firms, customizing personalized insurance products and services for pharmacy customers. Pharmacies can also help insurance companies identify and screen precise potential clients with insurance needs, facilitating subsequent sales conversion. In certain collaborations among pharmacies, pharmaceutical manufacturers, and insurance companies, including specific medications in the coverage of commercial health insurance can further alleviate the financial burden on patients.

Pharmacies will be subject to higher standards in information systems and standardized operations.

The newly issued "Notice," along with the detailed implementation rules and criteria for inclusion in pooled payment schemes formulated by local authorities, imposes stringent requirements on medical insurance settlement systems, inventory management (invoicing, sales, and stock) systems, and internal pharmacy operations. Pharmacies are required to invest in the updating and maintenance of information technology infrastructure, establish more robust prescription circulation systems, and strengthen self-discipline and compliant business practices.

Finally, pharmacies can also serve as a promotional force for the reform of outpatient mutual aid in medical insurance.

Following the phased rollout of outpatient mutual aid reforms for basic medical insurance across various regions, particularly after the adjustments to individual account allocations, insured individuals still lack a clear understanding of the reform’s background, implementation pathway, and the resulting changes. Although local medical insurance authorities have carried out public education campaigns through various channels, achieving full comprehension will take time. Recently, mass media outlets in multiple regions have reported on the implementation of these new local medical insurance policies, highlighting individual cases where residents expressed confusion or misunderstanding.

If pharmacies participate in policy publicity, leveraging their advantages of wide distribution and close proximity to communities and residents, and disseminate policy knowledge to the public in an accessible and easy-to-understand manner, they will significantly enhance their reputation and gain residents’ trust.

Overall, favorable policies have created a more positive environment for the pharmacy industry; whether each entity can fully seize the opportunities within it requires deeper reflection and action.