Johnson & Johnson Exits NASH Race as ARO-PNPLA3 Rights Reverted to Arrowhead, Signaling a Pivotal Year for the NASH Therapeutic Landscape

Arrowhead Pharmaceuticals

Pharmaceutical R&D Developer

NASH Once Again Makes Headlines in Foreign Media as a Partnership Is Terminated, with Johnson & Johnson—Recently Active in the News—Remaining at the Center of Attention

On February 15, Arrowhead Pharmaceuticals Inc. (Arrowhead) announced that it had regained full rights to ARO-PNPLA3 (formerly known as JNJ-75220795) from Janssen Pharmaceuticals, a subsidiary of Johnson & Johnson. This product was part of the research collaboration and option agreement between Arrowhead and Janssen established in 2018.

ARO-PNPLA3 is an investigational RNAi therapy utilizing Arrowhead Pharmaceuticals’ TRiMTMDevelopment of Patented Technology Platform. Genetic and preclinical validation has demonstrated that PNPLA3 is a driver of hepatic fat accumulation and injury in individuals carrying the I148M mutation. This therapy aims to reduce PNPLA3 expression in the liver for the treatment of non-alcoholic steatohepatitis (NASH) and is currently undergoing Phase I clinical trials.

This was once a high-profile, blockbuster collaboration, driven almost entirely by its NASH product.In 2018, Johnson & Johnson entered into a $3.7 billion collaboration with RNA therapeutics company Arrowhead Pharmaceuticals to jointly develop and commercialize ARO-HBV, an RNAi therapy for hepatitis B. Chris Anzalone, CEO of Arrowhead, stated in an interview with Fierce Biotech that, apart from the 2018 licensing agreement for NASH, Janssen, a subsidiary of Johnson & Johnson, did not select any other candidate products. Consequently, the partnership ended as the NASH assets were returned.

For Arrowhead Pharmaceuticals, the “breakup” came as a complete surprise. Just one week ago, James Hamilton, Head of Drug Discovery and Translational Medicine at Arrowhead, assured investors that despite the recent wave of pipeline adjustments by Janssen, a subsidiary of Johnson & Johnson, which caught the pharmaceutical industry off guard, he believed their collaborative NASH project remained secure. Even upon the termination of the partnership, Arrowhead stated it was merely “notified.” Clearly, this was a decision made on short notice.

From High Hopes to Sudden Halt: Johnson & Johnson Appears to Be a Dropout in the NASH Race. Why Did J&J Choose to Temporarily Withdraw? What Changes Are Underway in the NASH Landscape?It all starts with the termination of the partnership itself.

Phase I Results Were Positive, So Why Terminate the Collaboration?

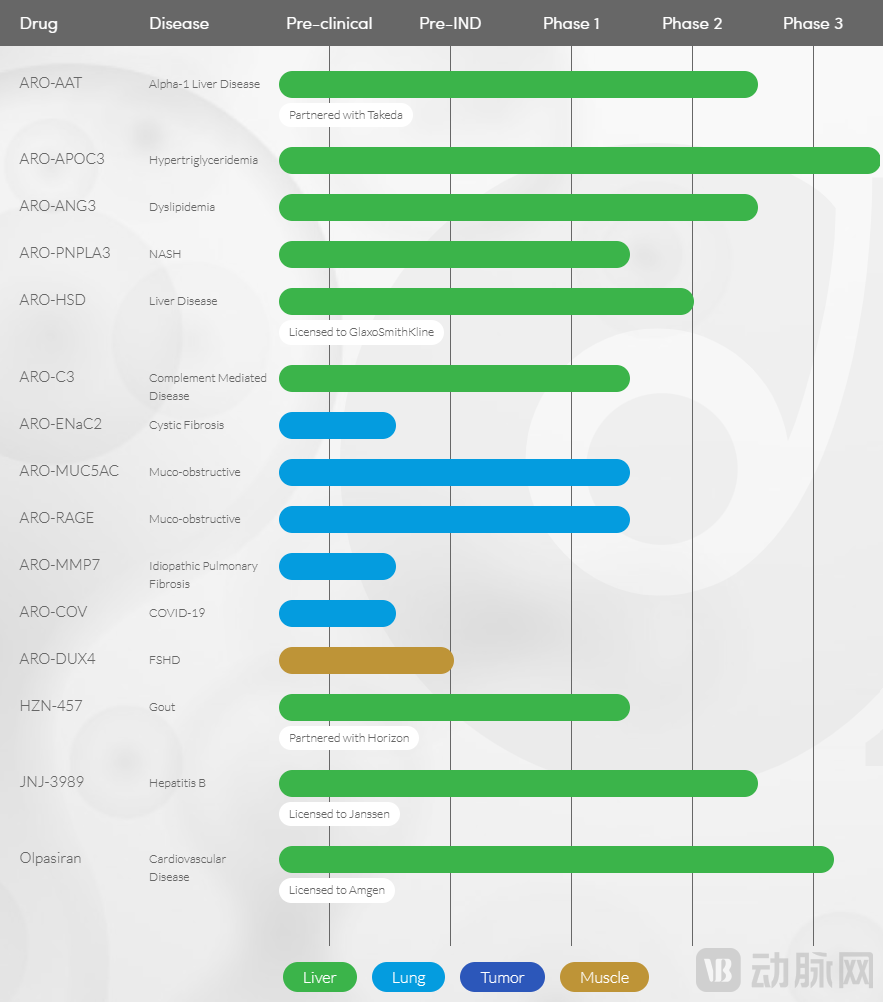

Arrowhead Pharmaceuticals was originally founded in South Dakota in 1989 and went public on the Nasdaq in 2004. Its RNAi technology platform is called TRiMTM(Targeted RNAi Molecule): The core RNAi technology patent was acquired from Novartis on March 5, 2015. Leveraging this technology platform, Arrowhead Pharmaceuticals has initiated the development of innovative therapeutics for diseases associated with genetic abnormalities. Its current R&D pipeline spans therapeutic areas including liver, lung, oncology, and muscle disorders, comprising a portfolio of 16 siRNA therapies, with the most advanced candidate having reached Phase III clinical trials.

(Image source: Arrowhead official website)

(Image source: Arrowhead official website)

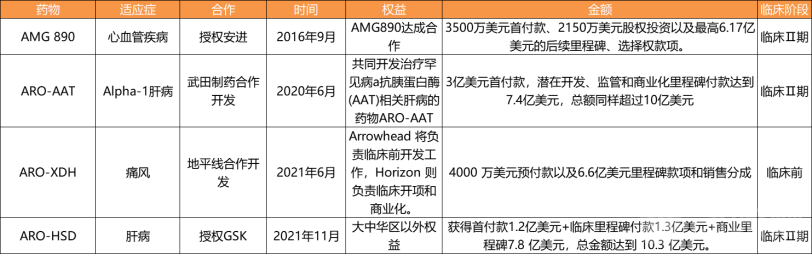

Of the nine drugs that Arrowhead Pharmaceuticals has currently advanced to the clinical stage, five have established collaborations with various pharmaceutical companies. The partnership with Janssen, a subsidiary of Johnson & Johnson, represents just one component of Arrowhead’s strategic portfolio. Following the termination of this collaboration, multiple publicly disclosed cooperative projects with other pharmaceutical firms, including Takeda Pharmaceutical, GlaxoSmithKline, and Amgen, continue to progress as scheduled.

(Data source: Compiled from public information)

(Data source: Compiled from public information)

Among these, ARO-HSD, licensed by Arrowhead to GlaxoSmithKline, is also an RNAi therapy for the treatment of NASH, with the total value of this collaboration agreement amounting to $1.03 billion.

In Greater China, Arrowhead is also actively seeking partners. On April 25, 2022, Arrowhead announced the establishment of a joint venture, Visirna Therapeutics, with Vivo Capital. Concurrently, Arrowhead entered into a license agreement with Visirna, granting Visirna exclusive rights to develop and commercialize four investigational RNAi therapies from Arrowhead’s portfolio for the treatment of cardiovascular and metabolic diseases in mainland China, Hong Kong, Macau, and Taiwan.

Returning to the collaboration between Arrowhead Pharmaceuticals and Johnson & Johnson, in the ARO-PNPLA3 project, PNPLA3 is a unique drug target for NASH. In a Phase I study, single-dose treatment with ARO-PNPLA3 yielded positive results, with patients homozygous for the I40M mutation showing a dose-dependent reduction in hepatic fat of up to 148% on average, along with good safety and tolerability.

The clinical trials have proceeded very smoothly. Arrowhead has indicated that it expects to disclose more information on ARO-PNPLA1 during the design of Phase III clinical trials and the evaluation of Phase II clinical study results. The industry also recognizes ARO-PNPLA3 as a highly promising drug for NASH. No insurmountable challenges appear to have arisen in the collaboration between the two parties.

Regarding the termination of the collaboration, Arrowhead Pharmaceuticals CEO Chris Anzalone stated that he is pleased for Arrowhead to advance the asset independently, but described the news as “unexpected,” noting that just a week prior, the company believed Johnson & Johnson would not abandon the project. Meanwhile, Arrowhead has not yet considered whether to seek new partners for its now wholly owned NASH candidate drug.

From Johnson & Johnson’s perspective, the company is undergoing a period of internal turmoil, so it is not surprising that it has abandoned its exploratory projects in the NASH field.

Johnson & Johnson’s internal restructuring has been ongoing for over a year. As early as January 2022, Joaquin Duato, who had long overseen J&J’s pharmaceutical business, assumed the role of Chief Executive Officer. Upon taking office, he announced reforms for Janssen Pharmaceuticals, including merging the Infectious Diseases and Vaccines divisions into a single integrated unit and streamlining multiple pipeline programs. The divisional merger has now been completed, with Dr. Penny Heaton, formerly head of the Vaccines division, leading the combined entity.

On February 13 this year, Johnson & Johnson made headlines across social media with a personnel announcement: John Reed, Global Head of R&D at Sanofi, announced that he would join the Johnson & Johnson Group as Chief Research Officer. With extensive experience in business restructuring and organizational realignment, Mr. Reed now stands at a pivotal juncture in Johnson & Johnson’s transformation.

Johnson & Johnson has also stated that it will continue to invest across all therapeutic areas while trimming some peripheral projects. When announcing its fourth-quarter 2022 earnings in January, the company discontinued two Phase I clinical assets for solid tumors and prostate cancer. A spokesperson noted that although the trials were ongoing, these two drugs were “not priority assets within our development portfolio.”

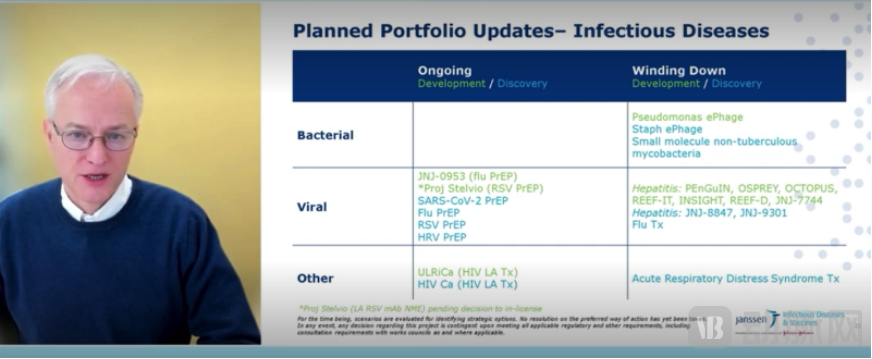

At a town hall meeting, James Merson, head of Johnson & Johnson’s Infectious Diseases division, stated that development efforts for hepatitis B and hepatitis D products within the company’s infectious disease pipeline would be discontinued, with research continuing only on “legacy projects.”

Town Hall Meeting: James Merson Presents Changes to Johnson & Johnson’s Infectious Disease Pipeline Layout (Image source: Fierce Pharma)

Town Hall Meeting: James Merson Presents Changes to Johnson & Johnson’s Infectious Disease Pipeline Layout (Image source: Fierce Pharma)

Therefore, the termination of the collaboration between Arrowhead Pharmaceuticals and Johnson & Johnson on ARO-PNPLA3 was not without warning; it was neither related to NASH drug data, nor due to troubles in the partnership, nor a sign that Johnson & Johnson had lost interest in competing. Rather, it was a routine move during the company’s current period of strategic adjustment.

Big Pharma’s Strategic Shifts: The NASH Arena Reaches a Watershed Moment

Johnson & Johnson has chosen to temporarily withdraw from the NASH field, while major pharmaceutical companies such as Gilead and Novo Nordisk continue to intensify their efforts. Regardless of whether these large pharmaceutical players enter or exit the market, it signals that the NASH sector is becoming active again, with the results of the initial wave of consolidation now coming to light.

The first wave of NASH drugs began to enter clinical trials in large numbers around 2018, with frequent reports of failure: Gilead’s ASK1 inhibitor selonsertib, Novartis’s FXR agonist emricasan, and Pfizer’s GLP-1 agonist danuglipron all encountered setbacks in clinical development.

Faced with the extremely high clinical failure rate in the NASH sector, Big Pharma is more inclined to pursue drug in-licensing, equity investments, and partnerships with publicly listed companies for co-development of NASH therapies, thereby balancing R&D risks.

Gilead and Novo Nordisk are jointly exploring the therapeutic potential of semaglutide, cilofexor, and firsocostat in combination for NASH; GSK has entered into a collaboration agreement with Arrowhead Pharmaceuticals to develop RNAi therapies for NASH; Pfizer has made an equity investment in Akero Therapeutics, which has two NASH drug candidates in Phase II clinical trials; and AstraZeneca has licensed the antisense therapy AZD2693 from Ionis Pharmaceuticals and is collaborating with Ionis to develop another novel NASH drug, ION455.

The enthusiasm of Big Pharma reflects the market’s strong interest in NASH therapeutics. Gilead has 18 NASH candidates in development; Novartis has 9; Pfizer is pursuing 7 programs; and Novo Nordisk, AstraZeneca, and Boehringer Ingelheim each have 6 ongoing projects... Although Johnson & Johnson is not a major player in this therapeutic area, it is noteworthy that its recent withdrawal of a NASH drug candidate still attracted significant attention from international media.

The entry and exit of large pharmaceutical companies are merely a footnote to the dramatically shifting market landscape. From the perspective of pharmaceutical market dynamics, the increasingly clear competitive landscape in this therapeutic area suggests that the NASH field may be approaching a watershed moment.

Over the past few years, the NASH sector has experienced significant volatility, with multiple episodes of “false prosperity.” In 2018, the stock prices of NASH-focused companies such as Madrigal Pharmaceuticals, Intercept Pharmaceuticals, and Viking Therapeutics surged. At that time, Goldman Sachs predicted that 2019 would become the “Year of NASH,” driven by the anticipated release of Phase III clinical trial results from Gilead Sciences, Intercept Pharmaceuticals, and Allergan. However, the subsequent period was marked largely by disappointing clinical data.

This year, the NASH field is likely to see its first approved drug hit the market.

At the end of 2022, obeticholic acid, a drug from industry bellwether Intercept Pharmaceuticals, began undergoing renewed FDA review, with results expected to be announced in June. Now, following initial exploration and accumulation of experience by pioneering companies in the NASH field, the market foundation is more solid than it was in 2018. GlobalData predicts that, compared with other late-stage assets currently under development for NASH in the United States, France, Germany, Italy, Spain, the United Kingdom, and Japan,The probability of this drug being approved is 64%. 。

Madrigal Pharmaceuticals, which has long been highly anticipated, has also entered a critical phase. The Phase III clinical trial results for its thyroid hormone receptor beta (THR-β) selective agonist, Resmetirom (MGL-3196; VIA-3196), were positive, with both the primary endpoint and key secondary endpoints met, positioning it as a potential first-in-class novel therapy. Meanwhile, its clinical trial design has sparked extensive discussion and emulation among NASH-focused companies both in China and abroad. In addition, Akero Therapeutics, Axcella Therapeutics, Poxel, and Galmed Pharmaceuticals have all reported positive clinical data within the past six months.

NASH Drug Company's Stock Price Rises Again.Unlike before, industry insiders have described past explorations as "hitting their heads against a wall," but now the sector has finally identified drugs that can truly help patients. Wall Street’s attitude toward NASH drugs has also undergone a noticeable shift.Metabolic diseases appear poised to become the next focal point for capital investment, following rare diseases and cancer, which means more funding will also flow into the NASH sector.

Turning to the domestic market, this fervor may soon spread to China. Viewing NASH within the broader context of metabolic diseases, GLP-1 therapies continue to undergo iterative development. As giants in the diabetes sector, Eli Lilly and Novo Nordisk have seen their stock prices multiply in recent years, with both companies now boasting market capitalizations exceeding $300 billion.The Metabolic Disease Sector’s Spotlight Moment Seems to Have Returned.