Five Key Technologies Driving the Billion-Dollar Aesthetic Medical Device Market: A Prospectus on Energy-Based Aesthetic Innovations

Fumeilei Medical

R&D Developer of Medical Aesthetic Devices

Driven by the tailwinds of the “appearance economy,” medical aesthetics is undoubtedly a golden track.

First, its market size is enormous, reaching hundreds of billions of yuan. According to Frost & Sullivan data, China's medical aesthetics market grew from RMB 99.3 billion in 2017 to RMB 189.1 billion in 2021, and is projected to reach RMB 638.2 billion by 2030.

Furthermore, the market is experiencing rapid growth. According to Frost & Sullivan, China’s medical aesthetics industry is projected to achieve a compound annual growth rate (CAGR) of 14.5% from 2021 to 2030, placing it among the leading segments within the consumer healthcare sector. Notably, the non-surgical market is expected to expand further, with a growth rate exceeding 20%.

In this process,As a key niche within the medical aesthetics sector, energy-based aesthetic devices are gaining increasing consumer favor and demonstrate high potential for explosive growth.According to incomplete statistics from VCBeat, since 2022 alone, more than 50 top-tier VC/PE firms have conducted due diligence or invested in this sector, sparking a wave of enthusiasm.

Why Are Energy-Based Medical Aesthetic Devices Experiencing Rapid Growth? What Is the Current State of the Industry? What Market Opportunities Exist? VCBeat Will Provide a Detailed Analysis Below.

This article is an excerpt from the White Paper on Energy-Based Devices in Medical Aesthetics. To gain insights into the industry landscape, development logic, and potential opportunities of energy-based devices in medical aesthetics, please scan the QR code to contact our assistant for the full report.

The desire for beauty is universal. In recent years, as public acceptance of medical aesthetics has grown, minimally invasive aesthetic procedures have gained immense popularity among young people, with energy-based medical aesthetic devices being particularly favored.

According to the "2021 China Medical Aesthetics Anti-Aging Consumption Trends Report" released by Xinhua Finance in collaboration with SoYoung,In the non-surgical aesthetic medicine market, energy-based device treatments are the most favored, with 86.23% of consumers seeking anti-aging aesthetic procedures opting for these modalities.

Behind this trend, the primary driver is that energy-based medical aesthetic devices offer inherent advantages such as minimal invasiveness, rapid recovery, and low risk, thereby effectively meeting the current demands of beauty-seeking consumers.

Furthermore, thanks to the continuous improvement of industry-related regulations and increasingly stringent supervision, energy-based medical aesthetic devices that are certified and compliant in circulation will gain greater market share. For instance, in 2022, the National Medical Products Administration (NMPA) issued the "Medical Device Classification Catalog" and the "Catalog of Medical Devices Prohibited from Contract Manufacturing," explicitly classifying products such as "skin boosters," "radiofrequency devices," and "thread lifts" as Class III medical devices subject to regulatory oversight and prohibiting their contract manufacturing.

Moreover, an increasing number of innovative Chinese companies specializing in energy-based medical aesthetic devices have entered the market, achieving notable progress in both R&D and commercialization, thereby providing the industry with more high-quality products and solutions. It is worth noting that China’s high-end energy-based medical aesthetic device market has been nearly monopolized by imported manufacturers, leaving substantial room for domestic substitution.

“Against the backdrop of rising living standards and an increasingly aging population in China, consumers’ demand for anti-aging treatments has grown ever stronger.” Previously, a senior investor in consumer healthcare told VCBeat.The rapid growth of the medical aesthetics market over the past decade, along with the emergence of numerous publicly listed companies with market capitalizations exceeding RMB 10 billion, amply demonstrates the broad prospects for the future of the energy-based device sector in medical aesthetics.

Of course, in addition to the high growth potential of the sector, the healthy gross profit margins of photoelectric medical aesthetics companies are also a significant factor attracting capital. A review of the entire medical aesthetics industry chain reveals that the upstream segment, represented by pharmaceuticals and medical devices, commands the highest gross profit margins. Specifically, device manufacturers typically achieve gross margins of 50%–60%. For instance, Chiopt Laser and Furui Medical Technology, representative enterprises in the photoelectric medical aesthetics field, reported gross profit margins of 55.8% and 55.7%, respectively. In contrast, the downstream segment, dominated by service providers, generally sees gross margins ranging from 30% to 50%. Representative companies such as Huahan Plastic Surgery and Langzi Shares recorded gross profit margins of 50.6% and 47.8%, respectively.

It is precisely on this basis that energy-based medical aesthetic devices have risen to prominence.

Laser, Intense Pulsed Light (IPL), Radiofrequency (RF), Focused Ultrasound, and Cryolipolysis: The Five Major Technologies Leading the Energy-Based Aesthetic Medicine Market.

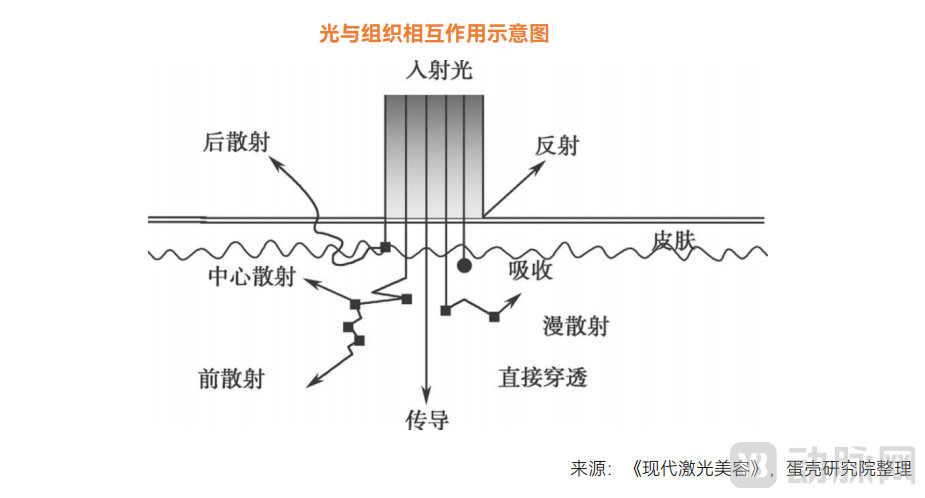

Let’s start with lasers.As a form of electromagnetic radiation, laser possesses four key characteristics: monochromaticity, coherence, collimation, and high energy. The interaction between laser and biological tissue is a complex process determined by multiple factors. When laser irradiates biological tissue, it undergoes four physical processes: reflection, scattering, absorption, and transmission. Biological tissue is a heterogeneous material composed of various types of cells and extracellular matrix. Due to differences in the structural and electromagnetic properties of different biological tissues, there are significant variations in their optical properties, including reflection, scattering, absorption, and conduction. Consequently, the outcomes of laser-tissue interactions also vary.

Lasers of different wavelengths can only interact with specific biomolecules having intrinsic frequencies in a biologically effective manner, because the absorption of laser photon energy by biomolecules exhibits frequency-selective characteristics.

In terms of application,The principle of selective photothermolysis is commonly used to treat pigmented disorders; the extended principle of selective photothermolysis can be applied to hair removal and the treatment of cutaneous vascular diseases; the principle of fractional photothermolysis enables skin remodeling and tightening, improving facial rejuvenation; the principle of photoacoustic action can effectively treat pigmented skin diseases and enhance skin rejuvenation.

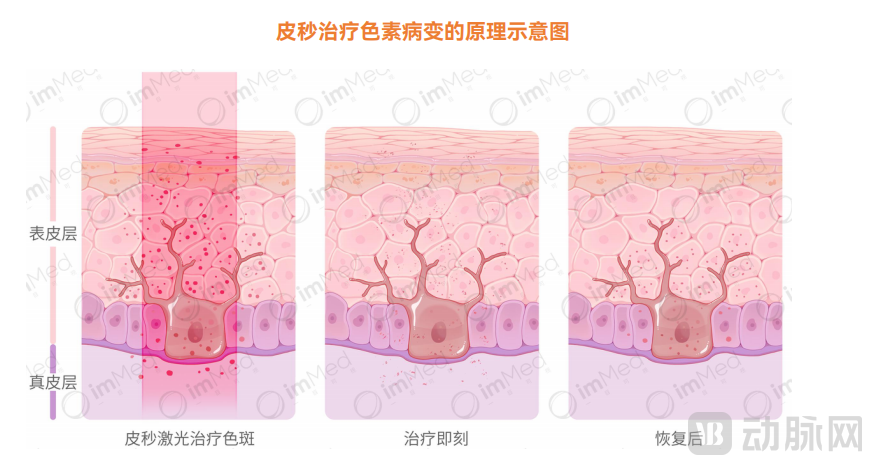

Taking picosecond lasers, which primarily operate on the principle of photoacoustic effects, as an example, they represent the ultimate solution for pigmented disorders and can achieve excellent results in spot removal. Picosecond lasers are indicated for the treatment of various epidermal and dermal hyperpigmentation conditions, demonstrating ideal efficacy for freckles, solar lentigines, and nevus of Ota. They are also effective for café-au-lait macules and lentigines, although a certain recurrence rate remains. For epidermal hyperpigmentation disorders such as freckles, solar lentigines, and café-au-lait macules, treatment can be administered using 532 nm Nd:YAG picosecond lasers or 755 nm alexandrite picosecond lasers.

Treatment parameters should be set based on the patient’s skin type and the color of the lesions, with a mild frost reaction generally serving as the clinical endpoint. For dermal hyperpigmentation disorders such as nevus of Ota and acquired bilateral nevus of Ota-like macules (ABNOM), treatment can be performed using a 755-nm alexandrite picosecond laser or a 1064-nm Nd:YAG picosecond laser. The typical interval between sessions is 3 to 6 months; with ideal therapeutic outcomes, complete clearance is usually achieved after several treatments. Therefore, as lasers with pulse widths in the picosecond range, picosecond lasers will play a significant role in the treatment of tattoos and most hyperpigmentation disorders.

▲ Graphic: Yimu Visual

▲ Graphic: Yimu Visual

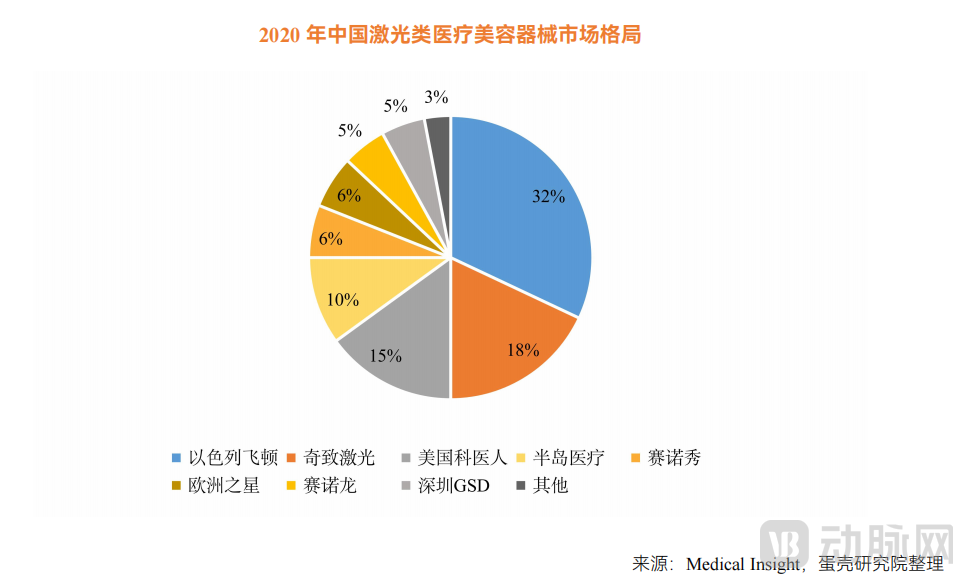

In terms of the industrial landscape of laser-based medical aesthetic devices, VCBeat Research Institute believes thatDomestic equipment is gaining momentum to catch up, with the high-end market poised to break the import monopoly and achieve domestic substitution.

According to data from Medical Insight, the CR4 market share in China’s laser-based medical aesthetic device category reached 75% in 2020, indicating a high level of industry concentration. Alma Lasers (Israel) ranked first with a 32% market share, followed closely by Qirui Laser and Lumenis (USA), with market shares of 18% and 15%, respectively. Overseas well-known brands such as Lumenis, Fotona, Syneron Candela, and Cynosure have secured certain market shares leveraging their technological strengths.

Currently, the domestic market for high-end optoelectronic products remains dominated by imports. However, Chinese enterprises are on the verge of breaking through technical barriers, shattering this import monopoly, further capturing market share, and reshaping the industrial landscape. In the field of medical aesthetic laser equipment, such as CO2 laser systems, Chinese companies have largely reached international standards, with several high-quality domestically produced devices already launched. Nevertheless, picosecond lasers, as an emerging technology within the medical aesthetic laser sector, face significant technical barriers, resulting in a market completely monopolized by renowned overseas manufacturers like Syneron and Cynosure.

Encouragingly, numerous domestic manufacturers in China have already established their presence in the picosecond laser equipment market. Fumeilei Medical, a representative enterprise specializing in the independent research, development, and manufacturing of mid-to-high-end medical aesthetic optoelectronic devices in China, officially initiated registration testing for its core product, the ForePico multi-wavelength picosecond laser system, in November 2022. Actual performance parameters of the device are fully comparable to those of imported counterparts, while demonstrating superior stability.

Therefore, it is foreseeable that as domestic enterprises continue to break through technical barriers and obtain NMPA approvals, the competitiveness of Chinese-made devices in the high-end segment of the medical aesthetic laser market will steadily increase, breaking the monopoly held by imported brands and achieving import substitution.

Next, let's look at intense pulsed light, also known as photorejuvenation, is a broad-spectrum light formed by focusing and filtering a high-intensity light source. As a broad-spectrum, intense pulsed light (IPL) can cover multiple absorption peaks such as melanin, oxyhemoglobin, and water. Due to the different properties, depths, and volumes of chromophores in normal and diseased tissues, their absorption of light and temperature rise vary. Therefore, it can effectively treat diseased tissue using temperature differences without damaging normal tissue.

The wavelength range of IPL is 550–1200 nm, with different wavelengths operating via distinct mechanisms for various indications. For instance, the 415–950 nm range can treat acne by selectively absorbing and destroying porphyrins, which are metabolic products of Cutibacterium acnes. Simultaneously, photothermal effects induce collagen denaturation and remodeling, enhancing skin elasticity, improving sebaceous gland secretion and enlarged pores, and reducing acne occurrence. Additionally, the 560–950 nm range can treat pigmentation disorders by leveraging selective photothermolysis to fragment melanocytes; superficial lesions form scabs that slough off, while deeper pigment is cleared through lymphatic metabolism.

▲ Graphic design: Yimu Visual

▲ Graphic design: Yimu Visual

In terms of market growth, intense pulsed light (IPL) technology is expected to see rapid volume expansion, with significant room for future growth. As "photorejuvenation" remains one of the most popular medical aesthetic procedures in China, the market for IPL-based medical aesthetic devices has demonstrated a stable and positive growth trend. In 2020, due to the impact of the pandemic, the market size of pulsed-light medical aesthetic devices in China declined slightly. The market value of counterfeit and unapproved products reached RMB 110 million, while compliant products accounted for RMB 690 million, resulting in a total market size of RMB 800 million, a year-on-year decrease of 1.2%. It is projected that by 2022, the market size for compliant IPL medical aesthetic devices in China will reach RMB 930 million. The industry development scale of intense pulsed light technology in the coming years should not be underestimated.

Market Dominated by Imports with High Entry Barriers for Domestic Brands. The current Chinese market for intense pulsed light (IPL) aesthetic devices relies heavily on imports. In 2020, imported IPL aesthetic devices accounted for as high as 80% of the market share, with Lumenis holding 51%, Alma Lasers (acquired by Sisram Medical) 20%, Syneron Candela from Israel 5%, and Cynosure from the United States 4%, forming a relatively stable competitive landscape dominated by leading players.

Under these circumstances, upstream medical device manufacturers possess greater bargaining power relative to the highly fragmented downstream institutions, granting them stronger control and regulatory influence over market prices, existing inventory, and technology. Furthermore, leading enterprises capture the majority of market profits, with gross profit margins of approximately 50%-60%. As these leaders expand production capacity and achieve economies of scale, they face lower difficulties and costs, thereby reinforcing a "winner-takes-all" dynamic. In this context, it is increasingly difficult for other small and medium-sized domestic intense pulsed light (IPL) device manufacturers to enter the market and compete for a share.

Based on industry development trends, VCBeat believes that for companies entering the market,"Volume growth at low prices and precision in treatment are key, while expanding application scenarios present opportunities."

Next, let’s look at radiofrequency., which is a high-frequency alternating electromagnetic wave situated between amplitude-modulated and frequency-modulated radio waves, with energy existing and propagating in space in the form of electric or magnetic fields (waves).

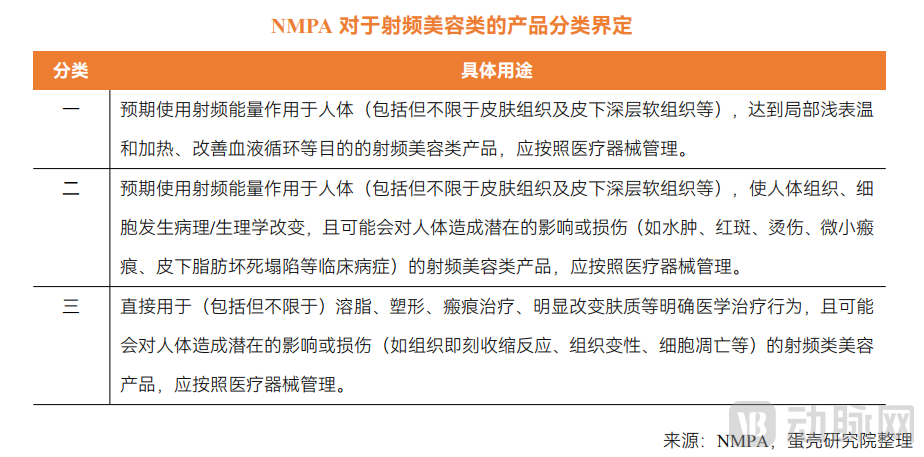

Currently, official authorities have established strict definitions and classifications for radiofrequency (RF) aesthetic devices. According to the "Guiding Principles for the Classification of Radiofrequency Aesthetic Products (Draft for Comment)" issued by the National Medical Products Administration (NMPA) in April 2021, RF aesthetic products are primarily categorized into three types based on their medical aesthetic applications and associated risks, as detailed in the table below:

According to the "Guiding Principles for Registration Review of Radiofrequency Cosmetic Devices (Draft for Comments)" issued by the Center for Medical Device Evaluation of the National Medical Products Administration in August 2022, radiofrequency cosmetic devices refer to products that utilize electrical energy, such as radiofrequency current at specific frequencies (typically around 200 kHz–5 MHz) or electric fields (typically 13.56 MHz or 40.68 MHz), to act on human tissue and generate thermal effects. These devices are intended to treat skin laxity, reduce skin wrinkles, minimize pores, tighten/lift skin tissue, treat acne and scars, or reduce fat (through fat softening or decomposition). Such products include floor-standing/desktop (large) devices powered by mains electricity, as well as handheld (small) devices powered by internal power sources.

Radiofrequency (RF) aesthetic devices can be categorized into three types based on the number of electrodes: monopolar, bipolar, and multipolar RF. The number of electrodes constrains the penetration depth of products operating at different frequencies, resulting in significant variations in their efficacy.

Based on the mode of action of the treatment handpiece, radiofrequency devices can be categorized into non-invasive and minimally invasive types. Non-invasive devices are currently the most mainstream radiofrequency aesthetic equipment in the wrinkle reduction and skin tightening market.

Compared with other photoelectric energy-based medical aesthetic devices, radiofrequency (RF) technology has relatively lower technical barriers, and its core hardware and software technologies are relatively mature. The figure below illustrates the main structural components of RF devices. The RF system emits radiofrequency signals at a fixed frequency, which undergo signal amplification and processing. Under CPU control, the system performs signal detection and impedance matching, ultimately achieving stable output within the desired energy range. The key technical challenges in RF devices lie primarily in the CPU control module, voltage standing wave ratio (VSWR) detection, and impedance matching modules.

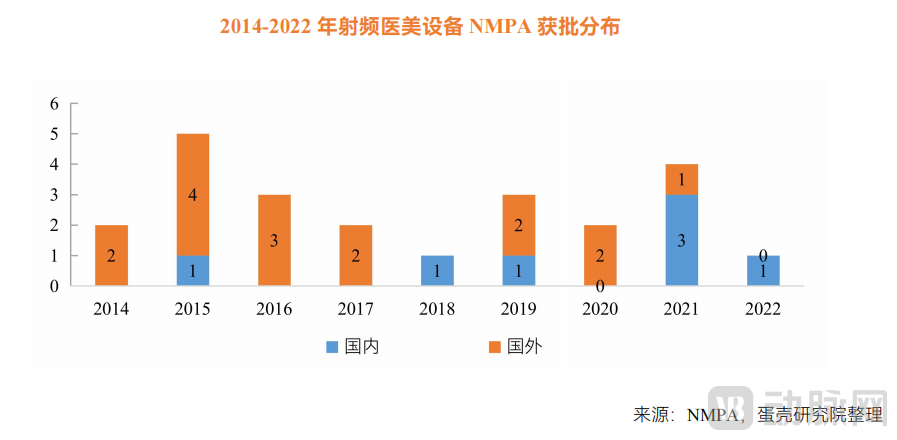

Radiofrequency aesthetic medical devices have a development history of over 20 years,The industry is currently in a period of robust growth, with 23 radiofrequency medical aesthetic devices approved in China; domestic brands are primarily focused on the mid-to-low-end market.Over the past three years, China has witnessed a surge in the market launch of radiofrequency (RF) aesthetic devices. To date, 23 RF aesthetic products have received approval from the National Medical Products Administration (NMPA), among which seven are domestically developed, accounting for 29% of all marketed products. However, in terms of regulatory classification, nearly all domestic RF aesthetic devices have been approved as Class II medical devices, whereas the vast majority of imported RF aesthetic equipment have obtained Class III medical device certifications. This indicates that most domestically produced RF aesthetic devices operate at lower energy levels and pose lower risks, thereby concentrating primarily in the low-end market.

As Thermage has driven the popularity of the radiofrequency (RF) aesthetic medicine industry, domestic brands have entered a period of rapid development over the past three years. Since 2019, the Baidu search index for Thermage has gradually risen, experiencing exponential growth from 2020 onward. At its peak, the search volume for Thermage exceeded 10,000, and its widespread popularity has significantly boosted the reputation of RF-based anti-aging treatments in aesthetic medicine.

To capitalize on the industry’s growth dividends, domestic companies have actively engaged in the market, striving to accelerate product launches and seize first-mover advantages. Between 2019 and 2021, six radiofrequency (RF) aesthetic medical devices were successively approved in China. Domestic manufacturers, represented by ThermiBeauty and Peninsula Medical, are currently building robust media matrices across platforms such as Xiaohongshu (Little Red Book), Weibo, and Douyin (TikTok), while engaging influencers and celebrities for promotional campaigns to rapidly enhance brand influence.

In the medical aesthetics sector, product efficacy is the core competitive advantage, and domestic companies still need to strengthen their internal capabilities. In many other industries, the rise of Chinese brands typically follows a path of first entering the low-end market, gaining a competitive edge through cost-effectiveness, and then gradually accumulating capital to expand into the mid-to-high-end segments. However, China’s medical aesthetics industry is still in its early stages, with the consumer base primarily consisting of mid-to-high-end clients. Medical aesthetics institutions regard high-end consumers aged 31–40 as their core customer segment. This demographic prioritizes efficacy, comfort, and overall experience over price. Moreover, due to their greater maturity, they place more emphasis on product reputation and professional aesthetic consultations. Consequently, well-established brands with proven product efficacy hold a distinct competitive advantage.

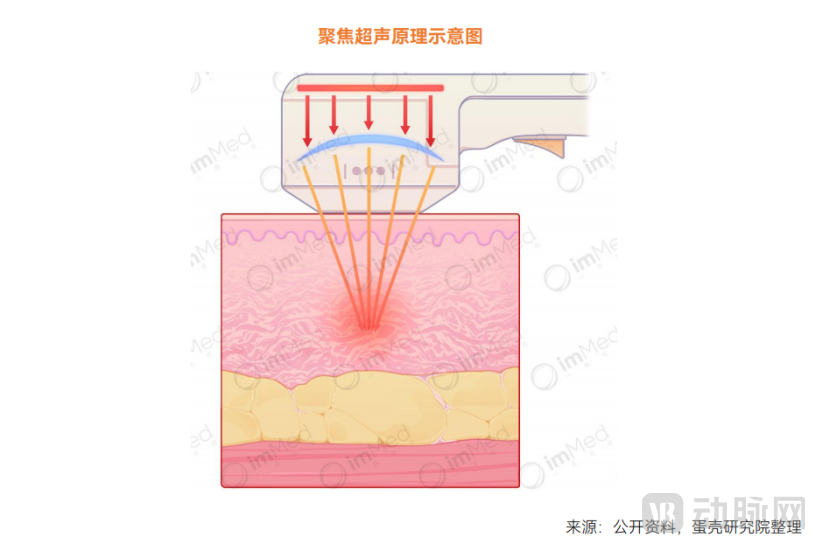

Then, let's look at focused ultrasound., it achieves focusing at a single point during the transmission of ultrasound waves, converting acoustic energy into thermal energy to rapidly create a high-temperature therapeutic focal point.

Focused ultrasound technology was initially applied to non-invasive tumor treatment. In subsequent research, investigators discovered that by appropriately adjusting the frequency of the ultrasound (as ultrasound energy is correlated with frequency, with higher frequencies yielding greater energy), focused ultrasound (hereinafter referred to as MFU when mentioned in the context of medical aesthetics) also demonstrates excellent applications in the field of medical aesthetics. It can achieve effects on the deep tissue layers of the face and body without damaging the outer layer of the skin.

▲Graphic: Yimu Visual

▲Graphic: Yimu Visual

Similar to other anti-aging technologies, the fundamental principle of MFU (Microfocused Ultrasound) for anti-aging is also to achieve lifting and tightening effects by heating and stimulating collagen regeneration. MFU delivers matrix molecular energy waves at a frequency of 60–120 million times per second deep into the subcutaneous tissue to form a focal plane, generating high temperatures through the electric field focusing effect. However, unlike other methods, MFU generates heat through the rotational friction of bipolar water molecules within collagen fibers induced by ultrasound energy absorbed by the tissue. This causes rapid temperature elevation in the focal zone, forming a network of thermal coagulation points. Although the energy level of MFU is lower than that of HIFU (High-Intensity Focused Ultrasound), it can still locally heat tissues to above 60°C, creating thermal coagulation points with a diameter of less than 1 mm. This effectively stimulates the deformation and contraction of collagen fibers and promotes the production of new collagen.

Focused ultrasound has a substantial potential market in China, estimated to accommodate three to four companies. In Europe and the United States, focused ultrasound and radiofrequency (RF) therapies are recognized as the two core technologies for facial anti-aging. These modalities target different demographic groups: Thermage primarily serves individuals aged 30–40, while Ultherapy mainly caters to consumers over 40, with each accounting for approximately 50% of the market size.

According to statistics from Market Growth Reports, the global market size for approved focused ultrasound aesthetic systems is estimated at $192.3 million. In China, the market remains untapped, as no Class III focused ultrasound products have yet received regulatory approval for commercial launch.

According to VCBeat, multiple focused ultrasound products are currently in the clinical registration phase. If regulatory authorities open up the market approval pathway for focused ultrasound devices, related products are expected to receive approval in 2023. Upon successful commercialization, the sector is poised for a modest surge over the following three years, with a projected compound annual growth rate (CAGR) of 20%, before transitioning into a stage of steady growth at an annual rate of 18%. The market size is anticipated to reach RMB 3.68 billion by 2031, with capacity to support 3–4 MFU companies.

However, at present, there are few focused ultrasound products, and obtaining regulatory approval is difficult. Only three products have been launched globally: Ultherapy, Doublo, and Sofwave.

The delayed approval of imported products for market launch presents the best opportunity for domestically produced devices to make a comeback.From the current development perspective, domestic regulation of focused ultrasound devices is extremely stringent. The fact that the U.S.-version ultrasonic scalpel has not obtained NMPA approval for over a decade indicates that its safety profile remains to be verified, and it faces continued risk of non-approval in the future. If Chinese manufacturers can seize the opportune moment, overcome the limitations of existing technologies, and focus on addressing safety issues, they have a high probability of being the first to obtain Class III medical device certification, thereby capturing the domestic market and achieving overtaking on a bend.

Finally, let’s look at cryolipolysis., primarily by delivering precisely controlled cryogenic energy via a non-invasive cooling device to targeted lipolytic areas, thereby selectively eliminating adipocytes in those regions. Specifically, lipid ice crystals induced by cold exposure disrupt adipocytes. Within 72 hours post-treatment, the damaged adipocytes trigger an inflammatory response, manifesting as a lobular panniculitis-like reaction that peaks on day 14 and persists until day 30. Macrophages phagocytose the damaged adipocytes; inflammation gradually subsides between days 60 and 90, accompanied by a reduction in adipocyte volume and thickening of the fibrous septa within fat lobules. Therefore, a 90-day period is commonly regarded as one treatment cycle for cryolipolysis.

In 2010, the first cryolipolysis device, CoolSculpting®, was approved by the FDA for the treatment of localized fat deposits in the flanks. It was subsequently approved for additional areas, including the abdomen (2012), thighs (2014), submental area (2015), and the arms, back, inframammary fold, and gluteal fold (2016).

In terms of market landscape, imports dominate, while established domestic pharmaceutical companies are actively expanding their presence. The global manufacturers of cryolipolysis devices primarily include Allergan, EnSung (South Korea), and High Tech. In China, only Allergan’s CoolSculpting® was approved for market launch in 2016. Sinclair Pharma Limited, a wholly-owned subsidiary of Huadong Medicine based in the UK, completed the acquisition in April 2021 of High Technology Products, S.L.U., a Spanish energy-based medical aesthetics device company held by Cocoon Business Investments, S.L.U. High Tech’s current non-invasive fat reduction products include Cooltech, Cooltech Define, and Crystile, with clinical trials and regulatory registration in the Chinese market expected to be completed within two to three years.

It is evident from the above that numerous innovative optoelectronic enterprises in China are progressively deepening their engagement, achieving certain progress in research and development as well as commercialization, which has brought immense possibilities to the industry.

However, it is important to note that in recent years, the medical aesthetics industry has been plagued by numerous irregularities, prompting stringent regulatory crackdowns. In March this year, the National Medical Products Administration (NMPA) issued an announcement adjusting the content of the "Medical Device Classification Catalog" concerning 27 categories of medical devices. Among these, radiofrequency therapeutic (non-ablative) devices, such as radiofrequency therapy instruments and radiofrequency skin treatment instruments, are now regulated as Class III medical devices. This signifies a further elevation of market entry thresholds.

Amid the overarching trends of technological iteration and increasingly stringent regulations, the photoelectric medical aesthetics industry is undergoing accelerated consolidation. Companies plagued by severe product homogenization and low technological value-added will be eliminated, while a cohort of enterprises daring to innovate and continuously break through will ultimately rise to the forefront of industry development.