GI Alliance: The $785M Gastroenterology Physician Group Redefining Value in U.S. Healthcare Consolidation

GI Alliance

Gastrointestinal Care Service Provider

Among the cancers with the highest incidence rates, gastrointestinal-related malignancies account for the majority: gastric cancer, liver cancer, esophageal cancer, colorectal cancer, and pancreatic cancer. According to World Health Organization data, the prevalence of gastrointestinal diseases in the general population is as high as 40%.

In terms of coverage and revenue, GI Alliance is the largest gastroenterology physician group in the United States, spanning 15 states including Texas and Florida, and bringing together nearly 800 gastroenterologists and more than 800 administrators. In September 2022, Apollo completed its acquisition of GI Alliance with a non-controlling investment of $785 million, marking the largest merger and acquisition deal involving a Physician Medical Group (PMG) in the United States in 2022.

In the United States, physician groups are quite common and are mostly initiated and established by physicians, medical service companies, or non-profit organizations. In recent years, however, physician groups driven by private equity have sprung up like bamboo shoots after rain, with GI Alliance being the most typical example.

Against the backdrop of healthcare system reform in the United States,Why Is Private Equity Beginning to Engage in the Establishment and Expansion of Physician Groups? What Impact Does Its Involvement Have on the Development of Physician Groups? Has the Nature of Services Provided by Physician Groups Changed?Driven by questions surrounding the development of physician groups under private equity involvement in the United States, VCBeat will analyze the growth trajectory of GI Alliance, the largest gastroenterology physician group in the U.S., with the aim of providing reference insights for the industry.

According to the Fraser report, the number of gastroenterology physician groups backed by private equity investment grew by 28% in 2021, reaching 68. Driven by private equity, large gastroenterology physician groups have been continuously integrating resources, expanding their portfolio of gastrointestinal medical services, and enhancing patient care, with GI Alliance emerging as the fastest-growing entity.

GI Alliance was founded in 2018 by the gastroenterology practice Texas Digestive Disease Consultants (TDDC) and private equity firm Waud Capital Partners.

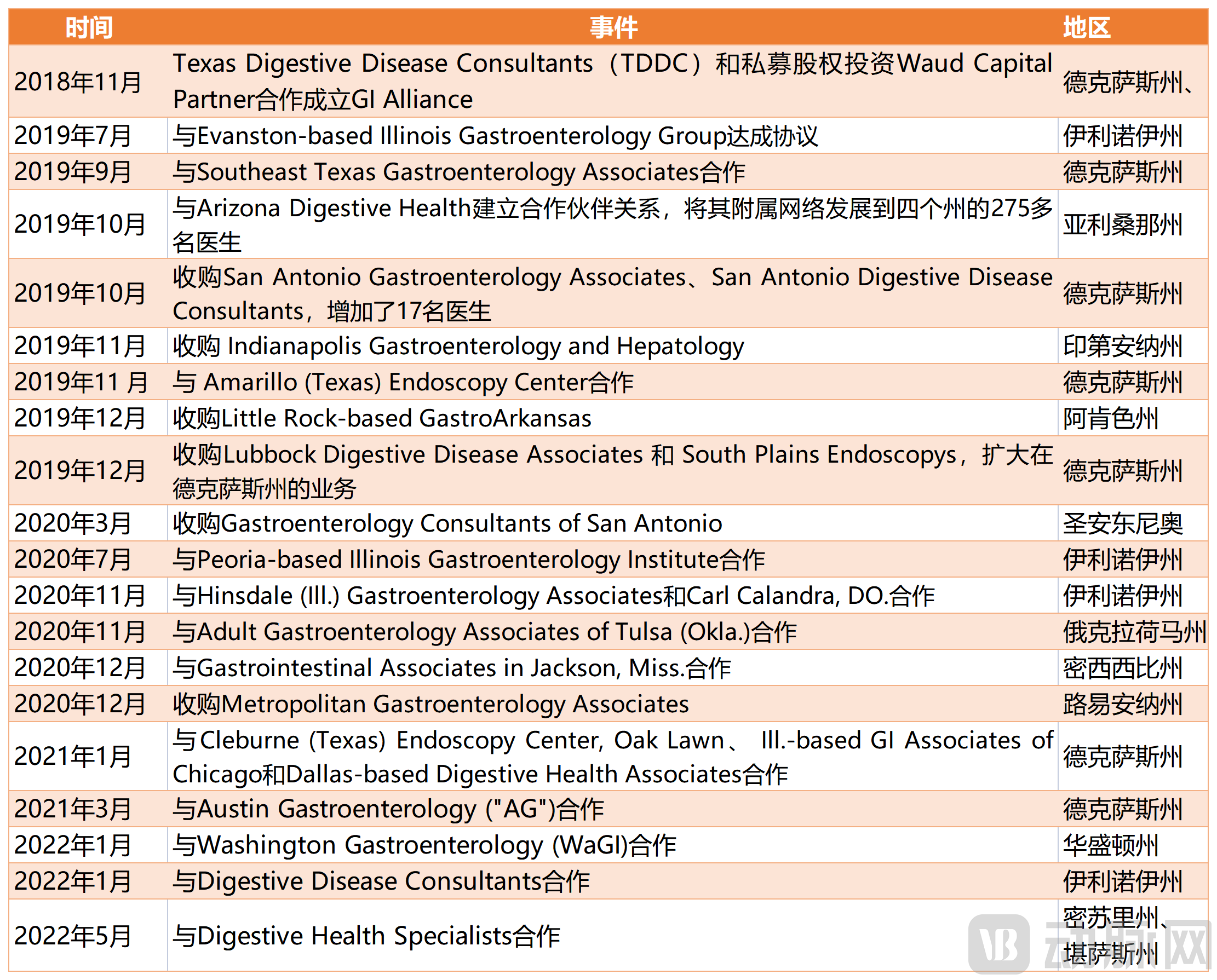

From 2018 to 2022, driven by Waud Capital Partners, GI Alliance nearly quintupled its physician headcount and expanded its geographic footprint from two to fifteen states through partnerships with or direct acquisitions of ambulatory surgery centers (ASCs) across various regions.

GI Alliance Collaborations and M&A Activities Driven by Waud Capital Partners

GI Alliance Collaborations and M&A Activities Driven by Waud Capital Partners

Source: GI Alliance official website; compiled and organized by VCBeat

GI Alliance evolved from the gastroenterology physician practice group TDDC. Founded in 1995 by Dr. James Weber, TDDC had grown by 2018 to include 159 physicians, covering more than 70 office locations, 37 endoscopy centers, 16 infusion centers, and 95 hospital-affiliated facilities across Texas and Louisiana, becoming the largest independent medical practice in the United States at that time.

James Weber specializes in internal medicine and gastroenterology. He has received numerous awards, including “Physician of the Year” from the Crohn’s & Colitis Foundation of North Texas and “Top Physician in Tarrant” from FW Weekly. In 2022, Dr. Weber served as both President and Chairman of the Board of Directors of the Digestive Health Physicians Association (DHPA), an organization that supports more than 2,300 gastroenterologists and their patients across the United States.

From TDDC to GI Alliance, James has always aspired to “build a gastroenterology practice group that is patient-centric, quality-focused, and physician-led.”

In the United States, physicians who choose to forgo employment agreements with hospitals and pursue independent practice generally have two primary options: establishing a solo private practice or joining a physician organization for group practice. In recent years, exacerbated by the impact of the COVID-19 pandemic, negotiations with insurers and government entities have become increasingly challenging. As many independently practicing physicians and small Ambulatory Surgery Centers (ASCs) struggle to maintain financial viability, joining large physician groups has become the preferred choice for the majority of doctors.

Joining a physician group enables access to shared medical resources and data within the organization. The group can handle administrative burdens such as health insurance negotiations and electronic health record (EHR) system utilization, allowing physicians to focus more on patient care. However, this arrangement also entails certain drawbacks; for instance, physician groups may establish specific clinical standards and pathways, potentially leading to a loss of “clinical autonomy.” This concern represents the primary hesitation among independent practitioners when considering joining a physician group.

GI Alliance has been able to attract numerous independent practitioners and ASCs to join, precisely because of its “Patient-Centered, Quality-Focused, Physician-Led” core philosophy.

Image source: GI Alliance official website

Image source: GI Alliance official website

At the “patient-first” level, to improve the accessibility of patient services, GI Alliance has been continuously acquiring ambulatory surgery centers (ASCs) across extensive regions of the United States, establishing ASCs catering to different age groups including adults and children, and expanding telemedicine services to maximally meet the needs of patients in diverse geographic areas and across various age groups. At the service delivery level, it collaborates with various insurance companies to accommodate the insurance coverage and treatment plans involved for different patients.

At the “quality-centric” level, GI Alliance also conducts clinical trials for a variety of conditions, including celiac disease, Crohn’s disease, eosinophilic esophagitis, gastroesophageal reflux disease (GERD), hemochromatosis, hepatitis C virus (HCV) infection, inflammatory bowel disease (IBD), non-alcoholic steatohepatitis (NASH), pouchitis, primary biliary cholangitis, and ulcerative colitis, to enable timely adjustments to treatment services and enhance the quality of care.

Furthermore, as a large gastroenterology physician group, it offers the most comprehensive range of services compared to smaller ASCs. Services provided by GI Alliance include colorectal cancer screening, management of chronic conditions (chronic gastrointestinal and liver disorders), intravenous infusion therapy, and colorectal surgery.

“At the physician-led level,” GI Alliance ensures physicians’ clinical autonomy through joint governance by a Physician Executive Committee, a Medical Advisory Committee, and an Executive Committee at the leadership level. The Physician Executive Committee establishes clinical practice guidelines; the Medical Advisory Committee is responsible for ensuring that physicians and care staff adhere to these guidelines and safeguarding patient autonomy; and the executive team handles other operational matters, such as facilities, equipment, and electronic health records (EHR), enabling physicians to focus on delivering high-quality patient care.

Furthermore, GI Alliance has established Clinical Governance Committees at all of its Ambulatory Surgery Centers (ASCs) across all regions to oversee physicians’ clinical practices and ensure the quality of care.

Guided by the philosophy of “patient-first, quality-centered, and physician-led,” GI Alliance has become the most widely distributed and highest-volume gastroenterology physician group in the United States.

Concurrent with Apollo’s non-controlling acquisition, the physician owners, who hold approximately 70% of GI Alliance, agreed to repurchase the minority stake held by Waud Capital Partners, valuing the company at $2.2 billion in total. With this transaction, Waud Capital Partners completed the sale of all its shares and exited GI Alliance.

Following the recapitalization, physician-owners led by James Weber remain the majority shareholders of GI Alliance, continuing to hold approximately 70% of the equity. Apollo has replaced Waud Capital Partners as the long-term strategic partner, supporting GI Alliance in achieving incremental growth in its existing operations going forward.

For more than a decade, the U.S. healthcare market and its regulatory landscape have been undergoing significant structural changes. From hospitals and insurers to independent practitioners, every corner of the healthcare market is experiencing investment and mergers and acquisitions, with an increasing number of large physician organizations emerging in succession.Business GrowthandResource Integrationhave become the keywords of this industry.

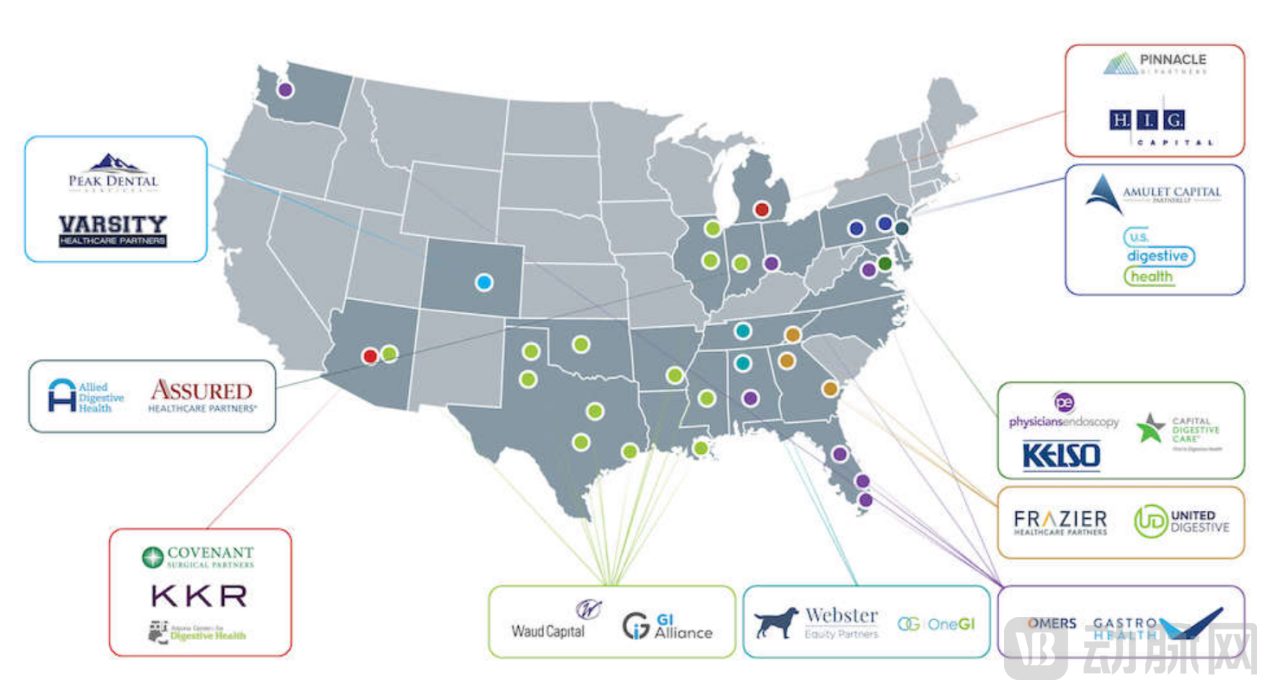

Private equity’s interest in the gastroenterology sector began in 2016 and has seen increasing investment in the subsequent years. According to a 2022 report by Physician Growth Partners, as of autumn 2021, 10% of gastroenterology practices or groups were either founded with private equity backing or employed by private equity-backed organizations, with more than 10 investments made in this sector in 2021 alone.

US Gastroenterology Groups Under Private Equity Investment

Source: Physician Growth Partners (data as of Spring 2022)

In 2022, the U.S. Centers for Disease Control and Prevention lowered the recommended age for colorectal cancer screening, urging most individuals to begin regular colonoscopies at age 45. As population aging accelerates, opportunities in gastroenterology ambulatory surgery centers (ASCs) are poised to expand significantly, which is one of the key reasons why many private equity firms are targeting physician groups.

However, private equity’s entry into the gastroenterology market does not translate to better services for patients. As investors, private equity firms adjust the operational models of Ambulatory Surgery Centers (ASCs) by shifting to cheaper suppliers and raising prices, thereby boosting profits at the expense of patient care quality. Patients now face higher costs for the same level of care they previously received, while potentially experiencing a decline in care quality.

According to U.S. Fortune magazine, as private equity has poured into gastroenterology practices, the cost of colonoscopies has risen to $1,100, nearly tripling from previous levels. A survey indicates that private equity’s entry into the healthcare industry leads to more surprise bills for patients and higher overall patient costs.

However, faced with complex government regulations, continuous technological innovation, and the growing difficulty of negotiations with the insurance industry, independent physicians operating Ambulatory Surgery Centers (ASCs) are seeing rising costs and are left with no choice but to become hospital employees or be acquired by private equity firms. Some industry leaders believe that “as healthcare resources become increasingly consolidated, independently operated ASCs will struggle to survive financially.”

This explains why GI Alliance has attracted the largest number of independent gastroenterologists to join—although it remains challenging to break free from private equity control, a greater share of GI Alliance’s equity is held by physician-owners, and its unique structure better safeguards physicians’ clinical autonomy.

According to the 2022 Gastrointestinal Market Research Report released by BizWits Consulting, the global and Chinese gastrointestinal markets reached RMB 497.053 billion and RMB 158.262 billion, respectively, in 2022, with the global market size projected to reach RMB 747.709 billion by 2028. Gastroenterology and urology have emerged as the two most stable sectors for health investment, and private equity-backed physician groups are becoming a dominant trend.

Generally, all corporate groups pursue public listing as their ultimate goal. However, the medical profession differs significantly from other industries. Physicians serve as the frontline point of contact for patients within the healthcare system and bear more direct responsibility for patients’ lives and health compared to other segments of the medical industry. Therefore, the concept of “clinical autonomy” is frequently emphasized, rooted in physicians’ sense of responsibility toward their patients.

As the U.S. healthcare system undergoes transformation, physicians’ status as “independent decision-makers” appears increasingly untenable. Opting for hospital employment may safeguard “clinical autonomy” under institutional management, yet often results in a sharp decline in income due to disproportionate compensation relative to effort. Alternatively, joining large physician groups, which are subject to corporate control, may lead to the erosion of “clinical autonomy.” This presents a difficult trade-off for every independently practicing physician.

For capital, maximizing returns is the ultimate goal. By summarizing the ways in which U.S. private equity firms join and operate physician groups, VCBeat has found that private equity typically begins by driving physician groups to continuously acquire small ambulatory surgery centers (ASCs)—Continuously absorbing more organizations through naming rights, integrating their resources to build brand awareness, and thereby achieving strong market influence and a broad service population—this is what private equity refers to as “platform practice.”。

By continuously driving business growth through resource integration, physician groups evolve into larger entities, thereby gaining greater negotiating power with insurers, government agencies, and other organizations, which leads to higher revenues. Consequently, a physician group’s refusal of IPO opportunities in order to preserve “clinical autonomy” would not be a concern for private equity investors.Large, established group brands are also valuable investments for private equity.

Private equity investment in physician groups is generally considered a medium- to short-term strategy, with investors typically exiting within three to eight years after entry. In the 2022 acquisition of GI Alliance, Waud Capital Partners exited after just three years, with Apollo Global Management stepping in as the new investor. This substantial transaction value reflects the decision made upon recognizing the significant returns that GI Alliance, as the largest gastroenterology physician group, could generate without going public.

With Apollo’s assistance, in late January 2023, GI Alliance partnered with CTGI, the largest gastroenterology (GI) practice in Connecticut, expanding its footprint to a 15th state and adding more than 80 physicians and over 400 team members.

With societal progress, public awareness and expectations regarding health have continuously risen, leading to an increasingly evident demand for comprehensive, efficient, and convenient healthcare services. In China, the development of commercial insurance, heightened professional self-awareness among physicians, the liberalization of policies on multi-site practice, growing patient demand for personalized medical care, and advancements in internet technology will all facilitate the growth of physician groups.

In 2014, Dr. Zhang Qiang announced the establishment of China’s first physician group. After years of development, the number of physician groups has grown from one to over a thousand. According to data from Gongyan Network, the revenue scale of physician groups in China was approximately RMB 10.371 billion in 2020, representing a year-on-year increase of 43.05%. In 2021, the revenue scale reached approximately RMB 15.83 billion, and it is estimated to have reached RMB 23.41 billion in 2022.

In China, physician groups not only fulfill physicians’ aspirations for independent practice but, more importantly, enhance the efficiency of medical resource allocation.The core to improving the efficiency of medical resource allocation lies in the optimized deployment of physician resources, and the inevitable path to achieving this is through physician groups.

On one hand, physician groups have broken the model of siphoning patients into large hospitals, effectively driving reforms in the operational mechanisms of public hospitals and the healthcare system, improving medical standards, and enabling true multi-site practice.

On the other hand, by joining physician groups, doctors can enter into service contracts with various medical institutions, facilitate tiered diagnosis and treatment through market mechanisms, promote the decentralization of medical resources, and provide services to patients in need, thereby truly realizing the goal of “bringing more specialists to the doorstep of the general public.”

In October 2022, the Zhang Qiang Doctor Group closed its first offline outpatient clinic and adopted an “asset-light” operational model. In an interview, Zhang Qiang stated, “Against the backdrop of medical insurance cost containment and the expansion of public hospitals, non-public healthcare remains a vital complementary component outside the public healthcare system. Non-public healthcare is developing in two directions: one is primary care accessible to the general public, such as pediatrics, dental clinics, and general practice; the other is high-end, specialized medical services that are largely uncovered by medical insurance.”

Although the pace of physician group registrations has slowed in the past two years, and some mature physician groups have begun to shift their operational models, the trend of physician groups serving as the optimal solution for allocating healthcare resources remains unchanged.