As BD Deal Uncertainty Grows, Is Blackstone’s Royalty-Based Investment Model the New Trend?

Royalty Pharma

Biopharmaceutical Royalty Provider

Recently, uncertainty has frequently arisen in business development (BD) transactions within the global biopharmaceutical industry. Abroad, Johnson & Johnson terminated its collaborations with Fate Therapeutics and Arrowhead Pharmaceuticals, while Bristol Myers Squibb (BMS) returned the rights to Dragonfly Therapeutics. In China, leading domestic pharmaceutical companies such as Hengrui Medicine and CSPC Pharmaceutical have entered into cross-border partnerships with lesser-known overseas biotech firms. The common ground bridging these parties is a shared consensus on product assets.

However, collaborations based on individual pipelines involve not only business development (BD) between companies but also a special form of investment, namelyDrug Royalty Investment。

Last year, Ruiqiao Credit Fund, under Kangqiao Capital, provided Yisheng Biopharma with a $40 million strategic investment based on royalties.PerhapsThe First Wave of Drug Royalty Investment Transactions in China’s Biopharmaceutical Industry.

Drug royalty investments exhibit, to some extent, the characteristics of business development (BD) deals, differing from traditional investment firms that acquire equity stakes in companies in exchange for capital., the investment target of this model is a single product pipeline.Royalty Pharma is the leader in this model.They invest in promising drug pipelines by collaborating with research institutions or pharmaceutical companies, targeting products that are already commercialized or have commercialization potential, and acquiring their drug royalties to finalize investment deals. In return for their investment, Royalty Pharma will receive a share of the future revenue generated from the commercialization of the corresponding drugs.

To date, Royalty Pharma has deployed $20 billion in investment transactions through this model, investing in 47 promising product pipelines, with more than 35 of these product portfolios already commercialized. Since 2020, Royalty has maintained strong revenue for three consecutive years, with profits rising year over year, reaching $2.566 billion in 2022. The company has stated that it plans to allocate an additional $10–12 billion in capital over the next five years.

The advantages of the drug royalty investment model are:First, companies seeking financing can secure capital without diluting equity, thereby avoiding the fragmentation of future organizational decision-making authority and enabling the gradual monetization of their pipelines. Second, investment institutions can achieve more flexible portfolio management of pipeline assets post-investment, resulting in reduced risk exposure in organizational management. Third, the commercialization of the underlying intellectual property (IP) of investee companies is often undertaken by Big Pharma, allowing for effective division of labor and integration among the three key innovation forces: capital, biotech/research institutions, and pharmaceutical companies.

This model has been developing in the United States for over 20 years. Investment firms such as Royalty Pharma, Healthcare Royalty, and DRI Capital specialize in this approach, while Baker Bros. and Oberland Capital, in addition to their traditional investment models, are also exploring this strategy. Even Blackstone has joined the fray.

In an interview with EY at the end of 2022, Blackstone particularly emphasized adopting a flexible approach to structuring deals, enabling partner companies to fund their pipelines without expanding their budgets. One such model is the drug royalty investment model. “We provide non-dilutive capital, which they can use to further advance their pipelines or invest in the commercial launch of products.”

Currently, domestic investment and financing in China remain dominated by equity investment, while the drug royalty investment model is still in its nascent stage.Going forward, as innovative enterprises refine their pipeline asset management and investment institutions intensify their focus on capital efficiency, this model is expected to see broader application.

VBInsight has compiled and analyzed Royalty Pharma’s investment transactions over the 27 years since its inception, aiming to provide reference value for investment models and insights into product pipeline strategy.

The Investment Path of the Largest Buyer of Drug Royalties, After 27 Years of Development and Evolution

Founded in 1996, Royalty Pharma has grown to become the largest buyer of pharmaceutical royalties in the industry, establishing itself as a leader among royalty-focused investment firms. To date, it has structured $20 billion in investment transactions. By collaborating with academic institutions, hospitals and non-profit organizations, small and mid-sized biotechnology companies, and leading multinational pharmaceutical corporations, Royalty Pharma has assembled a diverse portfolio of royalty interests, enabling it to generate investment returns based on the sales performance of these products.

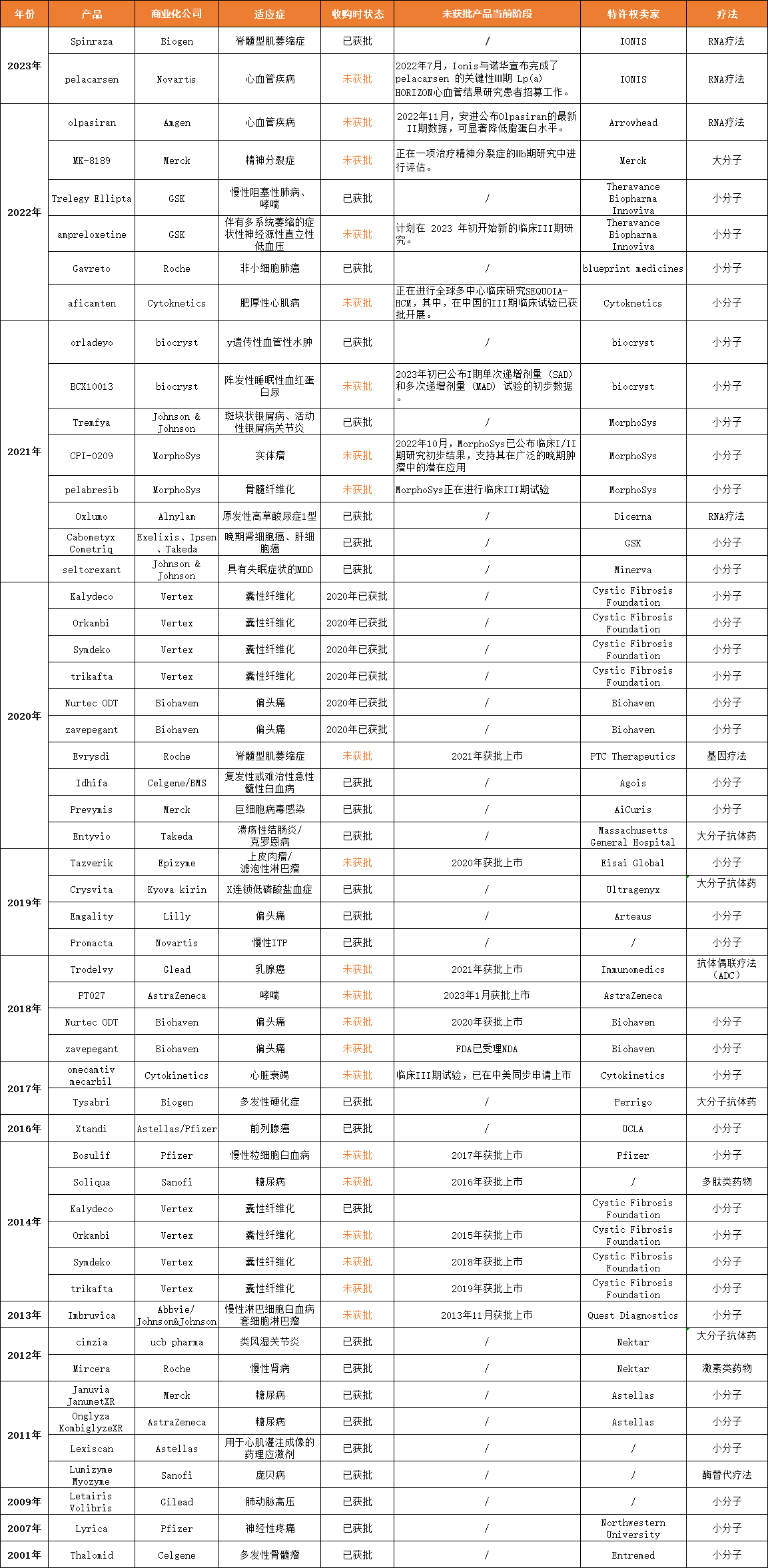

As of now,Royalty Pharma has initiated 47 drug royalty acquisitions, investing in a portfolio of more than 35 commercialized products,Blockbuster drugs with annual revenues exceeding $5 billion include the Symdeko and Trikafta portfolio, Entyvio, Januvia/Janumet XR, and Imbruvica.

Currently, Royalty Pharma has established a portfolio investment model that combines commercialized products with development-stage candidates. The maturity of this model stems from Royalty Pharma’s continuous optimization of its investment strategy behind the scenes.

Royalty Pharma funds innovative research and development in the biopharmaceutical industry through both direct and indirect investments.In the direct model, Royalty Pharma collaborates with pharmaceutical companies responsible for commercialization to jointly support late-stage clinical trials and the market launch of new products, in exchange for future royalties. In the indirect model, Royalty Pharma purchases intellectual property (IP) from original innovators to help them advance drug development and secure partners for later-stage commercialization.These two models have further evolved into three investment pathways:

I. Collaboration with Franchise Holders.Early-stage academic researchers or small biotech companies often hold drug licensing rights, and Royalty Pharma collaborates with them to tailor partnership models that meet the needs of both buyers and sellers.

II. Establish R&D partnerships with pharmaceutical companies of all sizes.Providing financial support for late-stage drug development is the strategic core of Royalty Pharma. Royalty Pharma enters into R&D collaborations with pharmaceutical companies on single, high-risk drug projects in late-stage development, thereby accelerating the drug development process.

3. Focus on M&A Transactions.Royalty Pharma partners with pharmaceutical companies acquiring biotech firms, establishing a collaborative division of labor: Royalty Pharma purchases drug royalties that are less prioritized by its partners and generated passively, while the partners acquire core strategic assets they value highly. This approach ensures that each asset finds its optimal buyer, while also enhancing the partners’ capital efficiency and competitive positioning in M&A transactions.

Focusing on Diversification: The Pipeline Layout Logic Behind 47 Investment Deals

Royalty Pharma’s unique investment model offers valuable reference points, and the logic behind its pipeline strategy is also worth studying.Diversification is the Key Word。

At the 41st Annual J.P. Morgan Healthcare Conference in early 2023, Pablo Legorreta, CEO of Royalty Pharma, noted that in 2022, the company made significant investments and expanded its royalty portfolio across six new projects. These included approved blockbuster drugs with growing sales, as well as innovative therapies in development addressing unmet clinical needs. A review of Royalty Pharma’s investment history reveals that this hybrid strategy has been a consistent feature throughout its development, underscoring the company’s ongoing commitment to diversifying its investment portfolio.

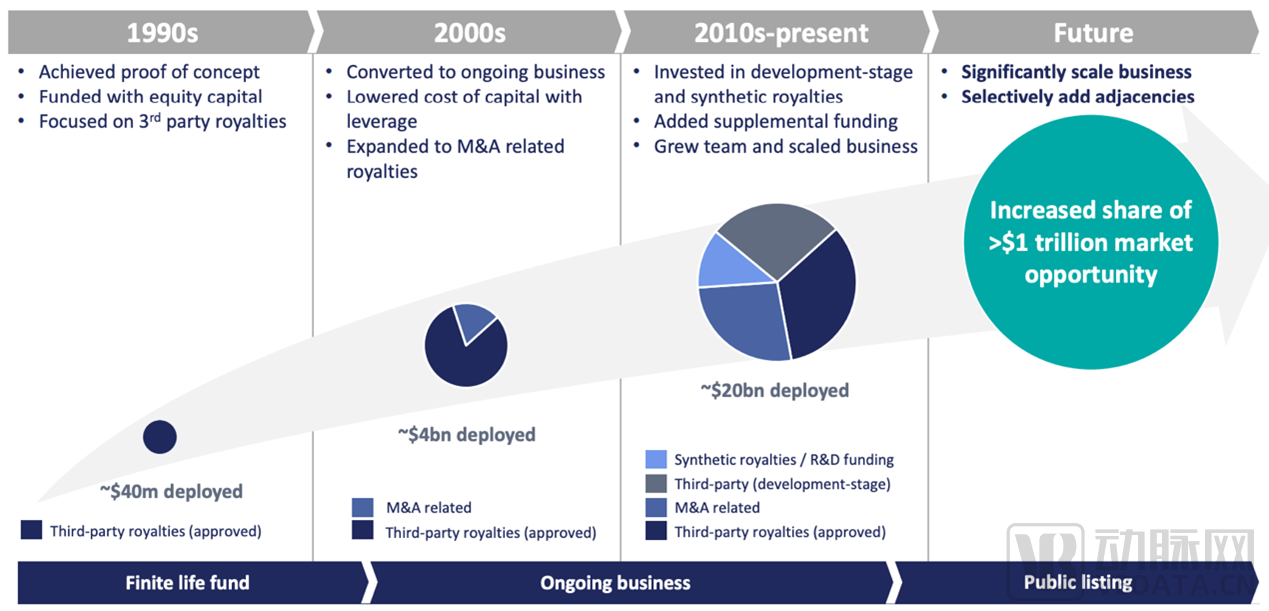

Royalty Pharma’s investment portfolio has undergone three phases of evolution: in the early stage, it accumulated initial capital by investing in marketed products; in the later stage, with enhanced risk-bearing capacity, it began to lay out early-stage projects.

Phase I (1996–2000): Investment was limited to approved product pipelines, with drug licenses acquired from third-party commercial pharmaceutical companies.

Phase II (2000–2010): Began focusing on M&A transactions, partnering with buyers in such deals to acquire passive drug royalties generated during the transaction process;

Phase III (2010–Present): Investment targets have become more diversified, with increased acquisitions of drug royalties from research institutions or scientific institutes, as well as investments in product pipelines under development acquired from third-party commercial pharmaceutical companies.

Figure 1: Phased Changes in Royalty Pharma’s Investment Strategy, Source: Royalty Pharma Official Website

An analysis of the 47 pipelines invested in by Royalty Pharma from 2001 to the present reveals that the companies ultimately commercializing these products are primarily multinational corporations (MNCs) such as Novartis, Johnson & Johnson, Roche, and Eli Lilly; the indications are diverse; the proportion of products not approved in the past two years has begun to increase; and while small-molecule drugs dominate the therapeutic modalities, other cutting-edge therapies are also being strategically deployed.

Table 1: Product Pipeline Invested by Royalty Pharma, Source: Royalty Pharma Official Website

Since its establishment,Royalty Pharma’s investment model has become increasingly mature and robust, evolving from its initially conservative strategy to one that places greater emphasis on balancing risk and return, thereby demonstrating increased confidence in investing in products at the development stage.

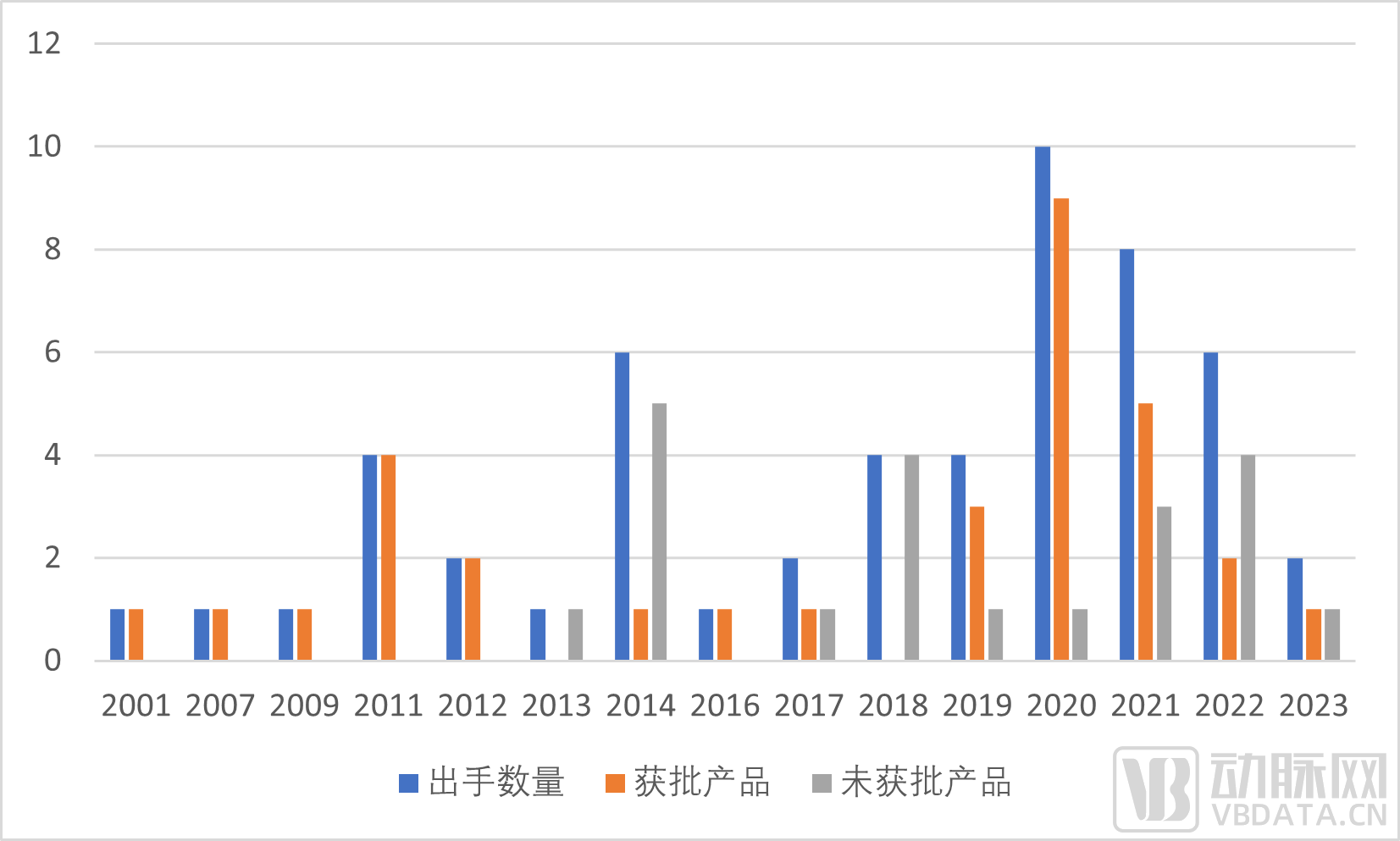

Figure 2: Statistics on Royalty Pharma’s Average Annual Transaction Volume, and Number of Approved and Unapproved Products

In terms of deal volume, Royalty Pharma’s pipeline investments were modest between 2000 and 2010, with only one product invested in per year. Two minor peaks emerged in 2011 and 2014, a trend closely tied to the cyclical fluctuations of the U.S. biotech sector. From 2011 to 2015, the biotechnology segment led gains in the U.S. stock market and sparked a wave of technological innovation, driving Royalty Pharma’s investment count to successive record highs. Between 2016 and 2022, rising financing demands in the biopharmaceutical industry fueled new opportunities for drug royalty investments, resulting in a steady growth trajectory for Royalty Pharma’s transactions, which peaked in 2020 when the company acquired royalties for ten products. Since 2020, although Royalty Pharma’s deal volume has moderated somewhat, it has remained at historically high levels.

From the perspective of the approval status of products at the time of acquisition, Royalty Pharma's risk resilience has been steadily improving.Initially, Royalty Pharma placed greater emphasis on approved, marketed products, which carry lower risk and enable a quicker return on investment. Starting in 2013, drugs in the development phase began to appear on Royalty Pharma’s investment list. Notably, from 2019 to 2022, there was a clear upward trend in the number of unapproved products in its portfolio. These unapproved assets spanned all clinical stages, from Phase I to Phase III. This shift reflects Royalty Pharma’s steadily enhancing risk resilience and growing confidence in investing in unapproved products.

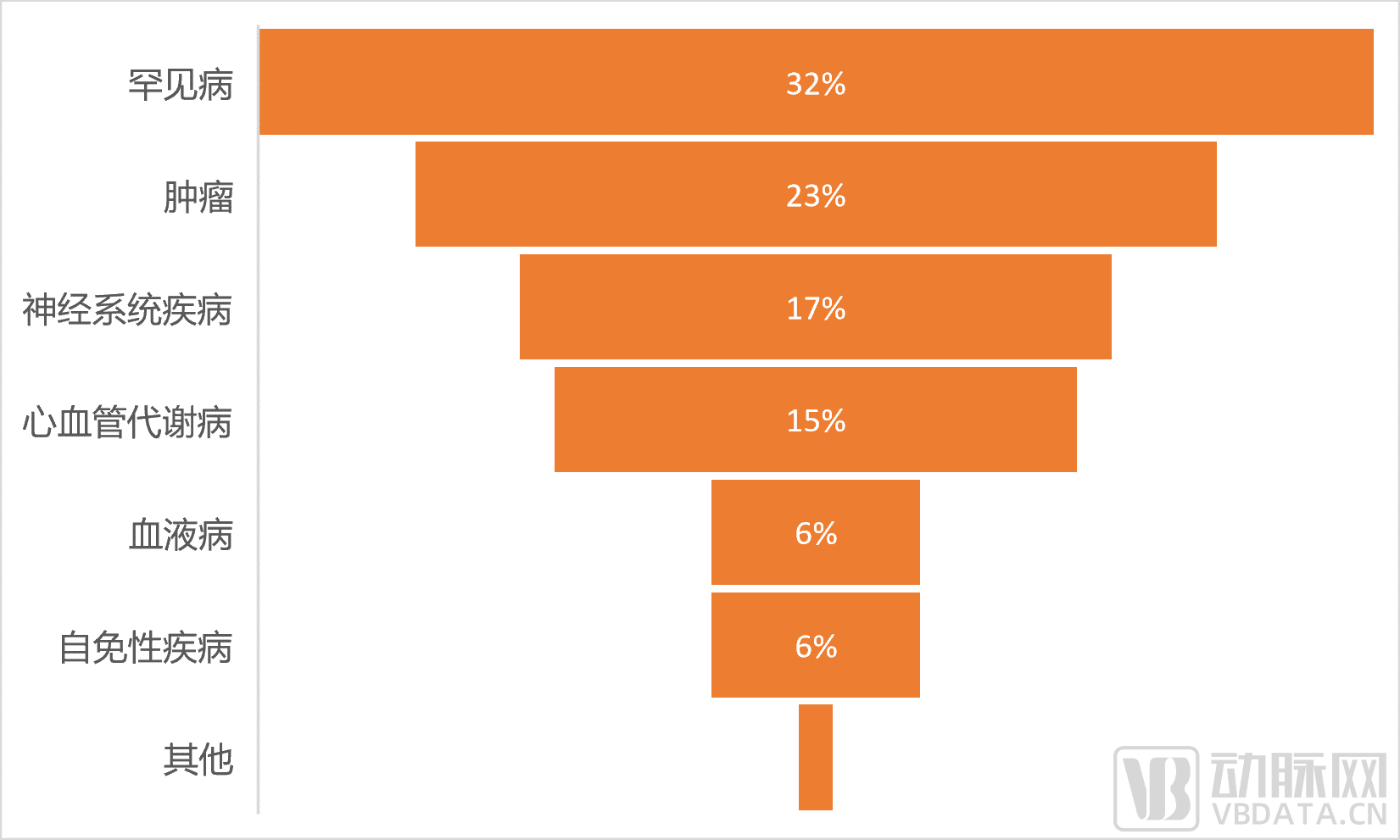

Figure 3: Summary of Indications for Royalty Pharma’s Investment Portfolio

Royalty Pharma’s investment portfolio spans a broad range of indications, covering rare diseases, oncology, neurological disorders, autoimmune diseases, cardiovascular and metabolic conditions, and hematologic disorders., among which products for the treatment of rare diseases and cancer accounted for half. When indications are further specified, it becomes evident that Royalty Pharma has invested in multiple products only for conditions with greater clinical needs, such as diabetes, cardiovascular diseases, and migraine, butThe overall indication portfolio exhibits minimal overlap., demonstrating rich diversity. This makes Royalty Pharma’s investment approach more flexible, not only expanding revenue sources but also reducing investment risks.

In terms of therapeutic modalities, small-molecule drugs account for the largest proportion of Royalty Pharma’s portfolio, while the company has also established a presence in more cutting-edge innovative therapies, including large-molecule antibody drugs, RNA therapeutics, and gene therapy.

While pursuing innovation in therapeutic approaches,Royalty Pharma has demonstrated a modular approach in its investment strategy, prioritizing investments and acquisitions across diverse indications. For any given indication, it builds product portfolios through different therapeutic modalities to expand the patient population and sales market.For example, in the field of cardiovascular disease, Amgen’s olpasirans is an siRNA therapeutic, while Ionis’ pelacarsen is an antisense oligonucleotide agent. For diabetes, AstraZeneca’s Onglyza is a DPP-4 inhibitor, and Sanofi’s Soliqua is a fixed-ratio combination product of basal insulin and a GLP-1 receptor agonist (GLP-1 RA). For migraine, Eli Lilly’s Emgality is a subcutaneously injected monoclonal antibody therapy targeting CGRP, Biohaven’s zavegepant is a nasal CGRP receptor antagonist, and Nurtec ODT is indicated for the preventive treatment of migraine.

Strong Revenue Growth for Three Consecutive Years, with a $12 Billion Capital Allocation Plan for the Next Five Years

In 2020, Royalty Pharma successfully went public.The financial reports from the past three years serve as the best validation of the drug royalty investment model.

Table 2: Royalty Pharma Financial Report Data from 2020 to 2022, Source: Royalty Pharma Official Website Financial Reports

From 2020 to 2022, Royalty Pharma continuously increased its investments, accelerating the allocation and investment in a broader pipeline of innovative assets. While its revenue experienced only a slight decline in 2022, the company demonstrated robust profit growth for three consecutive years.

Among the drivers of annual revenue growth, blockbusters are a key force; moreover, a single blockbuster product can often support royalty income for several years.:

In 2020, Royalty Pharma’s revenue was primarily driven by over $8 billion in sales from three key products—Vertex Pharmaceuticals’ cystic fibrosis portfolio, Biogen’s Tysabri, and Imbruvica (a collaboration product between AbbVie and Johnson & Johnson)—as well as royalty income from Gilead’s HIV franchise.

In 2021, Royalty Pharma’s primary revenue sources continued to be its cystic fibrosis product portfolio, Tysabri, and Imbruvica, along with other newly added royalty income.

In 2022, Royalty Pharma’s full-year growth was driven by the accelerated receipt of $458 million in royalty payments associated with Pfizer’s acquisition of Biohaven, as well as by growth in sales of its cystic fibrosis product portfolio and Johnson & Johnson’s Tremfya, along with new royalty income from products such as Trelegy.

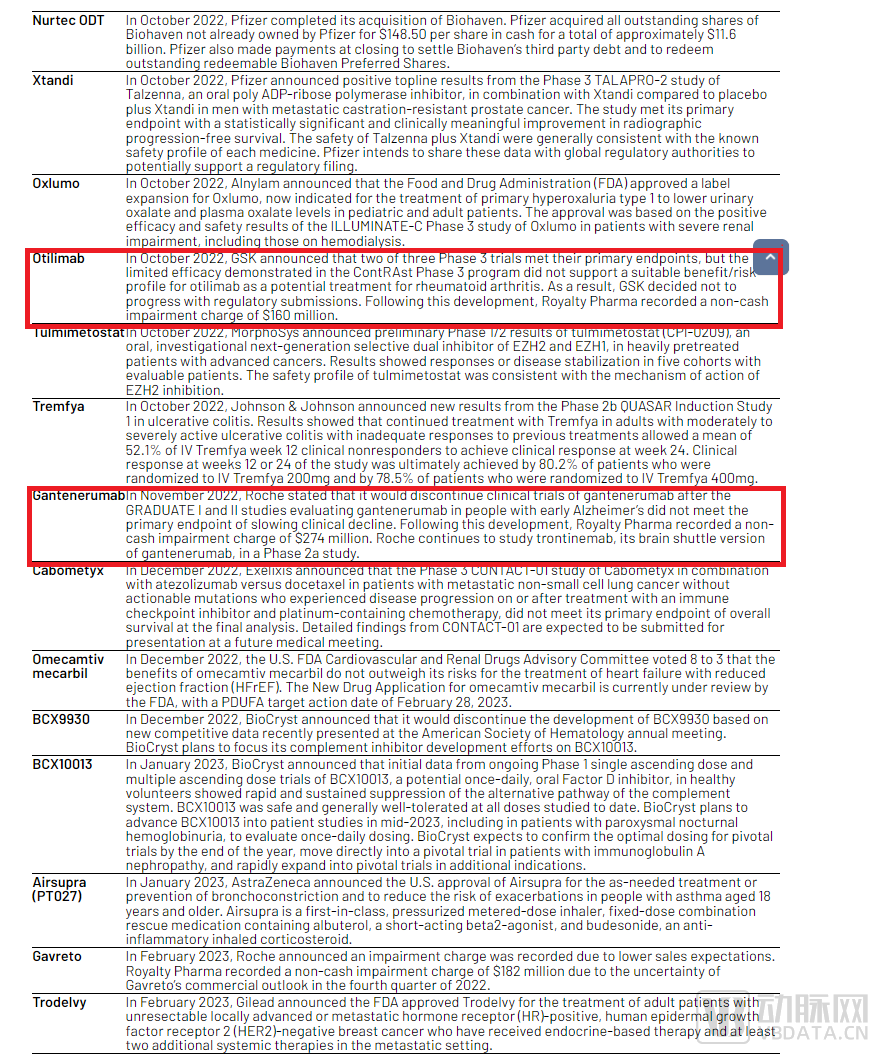

In fact, not every project pipeline invested in will bring substantial returns to Royalty Pharma.Taking the 2022 financial report as an example, in October 2022, GSK decided to abandon the submission of its product Otilimab’s treatment regimen to the FDA, resulting in a $160 million non-cash impairment charge for Royalty Pharma. Similarly, Roche’s new Alzheimer’s disease drug Gantenerumab had its subsequent trials terminated after failing to meet primary endpoints in the GRADUATE I and II clinical studies, leading to a $274 million non-cash impairment charge for Royalty Pharma.

Figure 4: Key Developments in Royalty Pharma’s Portfolio in 2022, Source: Royalty Pharma 2022 Annual Report

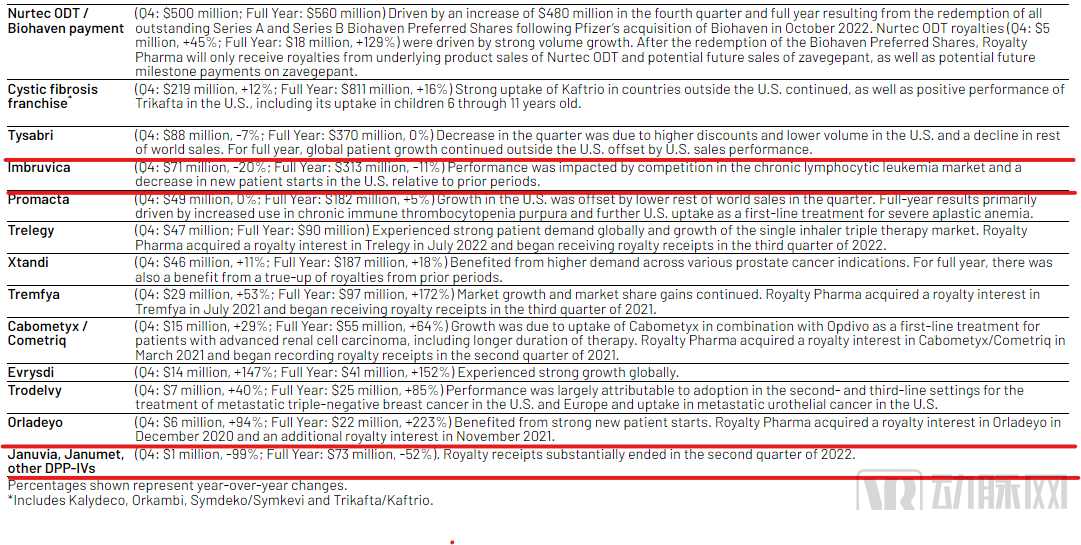

Meanwhile,As some product royalties expire or revenues decline, Royalty Pharma faces the challenge of offsetting income gaps through other products.In 2022, the royalty income from Januvia, Janumet, and DPP-4 inhibitors was largely exhausted in the second quarter, adversely affecting Royalty Pharma’s full-year continuous growth. Additionally, revenue from Imbruvica, a product developed through AbbVie’s collaboration with Johnson & Johnson, declined significantly due to competitive market dynamics, resulting in Royalty Pharma’s total royalty income reaching only $313 million, an 11% decrease.

Figure 5: List of Pipeline Assets Driving Royalty Pharma’s 2022 Revenue, Source: Royalty Pharma 2022 Annual Report

Despite the impact of these revenue declines, Royalty Pharma has offset such losses and negative growth through other blockbuster products. Its robust capital allocation strategy has facilitated strategic investments in innovative therapies, thereby driving long-term growth. A diversified portfolio of royalty investments has provided strong momentum for revenue growth, compensating for and offsetting sluggish performance in other products, thus highlighting the resilience of this investment model.

In 2023, Royalty Pharma got off to a strong start with the completion of its $500 million transaction with Ionis, and the company remains optimistic about its development this year. In addition, the company plans to allocate $10 billion to $12 billion over the next five years to continue exploring innovation in the biopharmaceutical industry.

Royalty Pharma’s investment model offers a unique perspective on innovative R&D and value creation in the biopharmaceutical sector. It may also provide valuable insights for China’s biomedical venture capital environment and even for business development (BD) transactions among pharmaceutical companies. Whether in terms of indication selection, strategic layout of innovative therapies, or flexible choices in investment pathways, this royalty-based investment model—still in its nascent stage in China—is worthy of exploration and learning.