Pfizer's Pursuit of Seagen Marks the Start of 2023’s Two Major Biopharma M&A Trends

On February 27, news broke that Pfizer was in preliminary negotiations with Seagen regarding a merger and acquisition deal. Although the talks between the two companies were still in their early stages, Seagen’s stock price surged by 13% in response.

The industry is eagerly anticipating the outcome; if successful, this would mark the largest deal in the biopharmaceutical sector since 2019.

Of course, there are numerous obstacles. Even setting aside antitrust hurdles, the broader market environment of 2022 and the resulting caution still pervade the entire industry, dooming a merger and acquisition deal worth as much as, or possibly exceeding, $40 billion to a fraught fate.

Importantly, if the largest biopharmaceutical M&A deal of 2022—Amgen’s $28.5 billion acquisition of Horizon Therapeutics, announced last December—was the first sign of an acceleration in the industry’s M&A trajectory, then the signal is already clear enough, regardless of whether Pfizer’s deal with Seagen closes: Mergers and acquisitions will play a core strategic role as large companies seek steady growth amid the innovation wave and strive to keep their business models from becoming obsolete.

2022 was likely the calm before the storm. As companies seek innovation not only in their portfolios but also across their entire operating models, the decline in transaction volume in 2022 could evolve into a deal-making boom in 2023.

Can such a large deal be successfully negotiated?

First, let us examine Seagen, the party rumored to be acquired. Currently valued at approximately $30 billion, Seagen is unquestionably the leading player in the antibody-drug conjugate (ADC) sector. This is not the first time Seagen has engaged in acquisition negotiations with multinational corporations (MNCs). Last July, Bloomberg reported that Merck was preparing to acquire Seagen for over $40 billion, but the deal ultimately fell through due to pricing disagreements.

Last year, the M&A market across the entire industry was highly sluggish, with Big Pharma exercising considerable caution in its deals. Merck and Seagen ultimately failed to reach an agreement; while specific details remain undisclosed, valuation and the broader industry environment were undoubtedly key considerations.

Analysis suggests that a potential acquisition could make sense for Pfizer, but not so much for Seagen. Pfizer’s new CEO, David Epstein, has recently completed an extensive internal review to best position Seagen for long-term growth. Analysts were largely surprised by the decision to sell Seagen, unless the transaction price reaches or exceeds the previously announced $40 billion.

In conclusion, price is the key factor.

Nevertheless, the industry has reason to anticipate what is being hailed as “the largest deal in the sector since 2019.” For one, domestic M&A sentiment in the United States has been gradually shifting, as evidenced by Amgen’s $27.8 billion acquisition of Horizon, which closed in late 2022.

Another reason is that the acquirer this time is Pfizer. It is no secret that Pfizer has substantial cash reserves, as its sales of COVID-19 vaccines and oral antiviral drugs have left the company with ample liquidity. In 2022, Pfizer’s revenue reached a record $100.3 billion, propelling it once again to the position of the world’s largest pharmaceutical company.

It is no secret that Pfizer needs, and indeed must, sustain its growth through acquisitions. With key patents for its vaccines and COVID-19 therapeutics expiring between 2025 and 2030 and generic competitors rapidly entering the market, Pfizer’s revenue from these products is expected to decline sharply in the coming months. The company also projects that patent expirations will result in an annual revenue loss of approximately $17 billion between 2025 and 2030.

Big Pharma is generally facing an innovation bottleneck, a situation particularly evident at Pfizer, the once-dominant legacy pharmaceutical giant, whose oncology business urgently needs revitalization. Due to emerging competition, sales of Ibrance, Pfizer’s flagship oncology asset for breast cancer, have been in decline. Pfizer’s commercial portfolio and pipeline lack new blockbuster products. Mergers and acquisitions represent the fundamental strategy for this “world’s largest pharmaceutical company” to maintain its competitive edge.

In Pfizer’s plan, annual revenue from its non-COVID-19 product portfolio is set to increase from approximately $70 billion to over $84 billion by 2030. Of this, about $25 billion will come from medicines acquired through business development transactions.

Pfizer has consistently stated that deal-making is critical to its growth. At the J.P. Morgan Healthcare Conference in January, Pfizer CEO Albert Bourla once again made it clear that a combination of small, medium, and large transactions is necessary to achieve the company’s objectives.

The 2022 Annual M&A Report shows that among the top three M&A deals last year, apart from Amgen’s $27.8 billion acquisition of Horizon Therapeutics, the second and third largest deals were both made by Pfizer, which acquired Biohaven for $11.6 billion and Global Blood Therapeutics for $5.4 billion, respectively.

Clearly, Pfizer will strive to secure a major deal this year. Antibody-drug conjugates (ADCs) have emerged as a highly sought-after therapeutic area in recent years. Seagen currently markets four commercial drugs, generating $2 billion in revenue last year, representing a 25% increase from 2021. Its pipeline is also heavily populated with a series of ADC candidates. Acquiring the ADC leader to gain strategic advantage in this new therapeutic arena appears to be Pfizer’s optimal investment choice.

The Biopharmaceutical Industry Has Over $1.4 Trillion in M&A “Firepower”

If this merger ultimately succeeds, it will send another strong signal to Pfizer and the industry at large, heralding 2023 as a major year for mergers and acquisitions.

First, industry insiders know that large pharmaceutical companies are wealthy, but just how much cash do they actually have on hand?

Data analysis released by the renowned investment firm RA Capital on January 3 this year shows that the strategic divisions of the top 20 multinational corporations (MNCs) could acquire the entire market at a 100% premium, leveraging their existing $220 billion in cash and less than 1.5 years’ worth of annual free cash flow totaling $240 billion. This market includes 660 unprofitable pharmaceutical companies listed in the United States, each with a market capitalization under $10 billion, for a combined total market value of $284 billion.

EY’s 2023 edition of the M&A Power Report provides additional data insights.

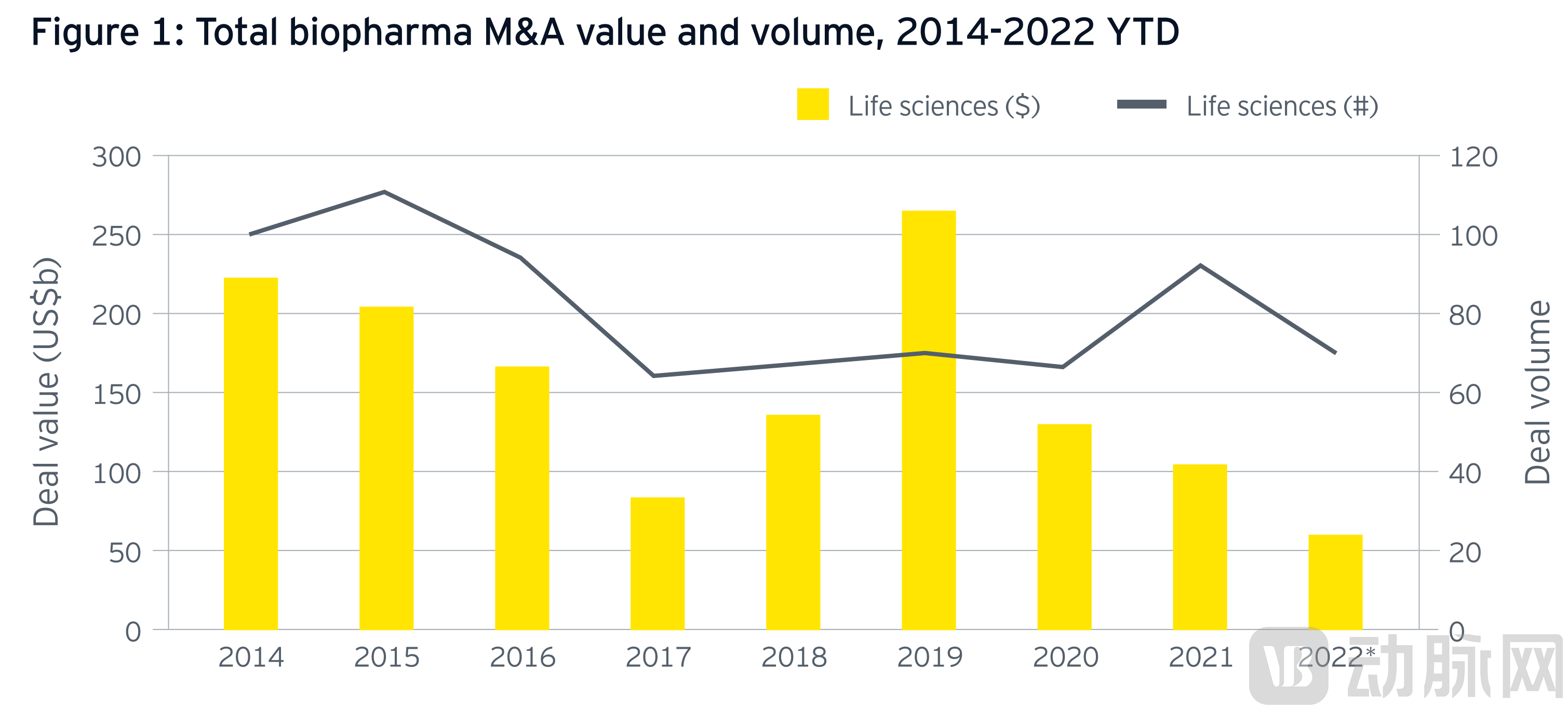

First, in 2022, mergers and acquisitions (M&A) in the biopharmaceutical industry were indeed in shallow waters. By the end of November 2022, only $105 billion worth of M&A transactions had been completed, with the total value of life sciences M&A set to hit its lowest level since 2017. As of November 30, 2022, M&A investment in 2022 had dropped by 53% compared to the full year of 2021, with a total of 117 agreements signed, representing a 27% decline from 2021. Moreover, the vast majority of deals in 2022 were small-scale add-on transactions.

The lack of M&A activity in the first 11 months of 2022 was particularly striking, with M&A spending hitting its lowest level since Ernst & Young (EY) first published its M&A Firepower report in 2014.

Currently, the industry boasts ample capital reserves. As of the end of November 2022, the biopharmaceutical sector alone held over $1.4 trillion in “firepower” assets—an 11% increase from 2021 and the highest level since Ernst & Young’s M&A Firepower Report began tracking deployable capital in biopharma (see Figure 1).

Source: Capital IQ, EY analysis. This analysis only considers publicly disclosed transactions with a value exceeding $100 million. *Q4 data as of November 30, 2022

Source: EY’s 2023 M&A Firepower Report

Not only is there robust M&A “firepower,” but following the market correction in 2021–22, high valuations of target companies should no longer pose a significant obstacle, given the pressure from growth gaps and the potential benefits of acquiring new business models and innovations. As a “buyer’s market” takes shape, declining valuations in the industry are expected to stimulate an increase in deal activity.

Three Major Structural Factors, Two M&A Trends

Despite global uncertainties, the life sciences industry continues to benefit from strong structural factors favoring mergers and acquisitions (M&A). In its M&A report released in January 2022, EY outlined several key factors that constrained M&A activity in 2021:

· Record-high valuation levels and high-premium biotech M&A targets, as the industry attracted significant investor attention during the early stages of the pandemic.

· High capital liquidity enables smaller companies to more easily access public markets through IPOs, SPACs, and venture capital (VC) financing.

Six months later, these constraints have largely dissipated. The sharp decline in biotechnology valuations has led to a corresponding drop in biotech financing. The record-breaking IPO market of 2021 has cooled alongside the downturn in the SPAC market. This will complicate the path to public markets for smaller companies and make M&A exits more attractive.

The barriers to large-scale M&A investments have largely been lowered, yet major corporations remain hesitant or are even pulling back. There are deeper driving forces behind their return to the negotiating table in 2023.

EY’s “M&A Firepower Report” also outlines three additional reasons why M&A activity is set to increase:

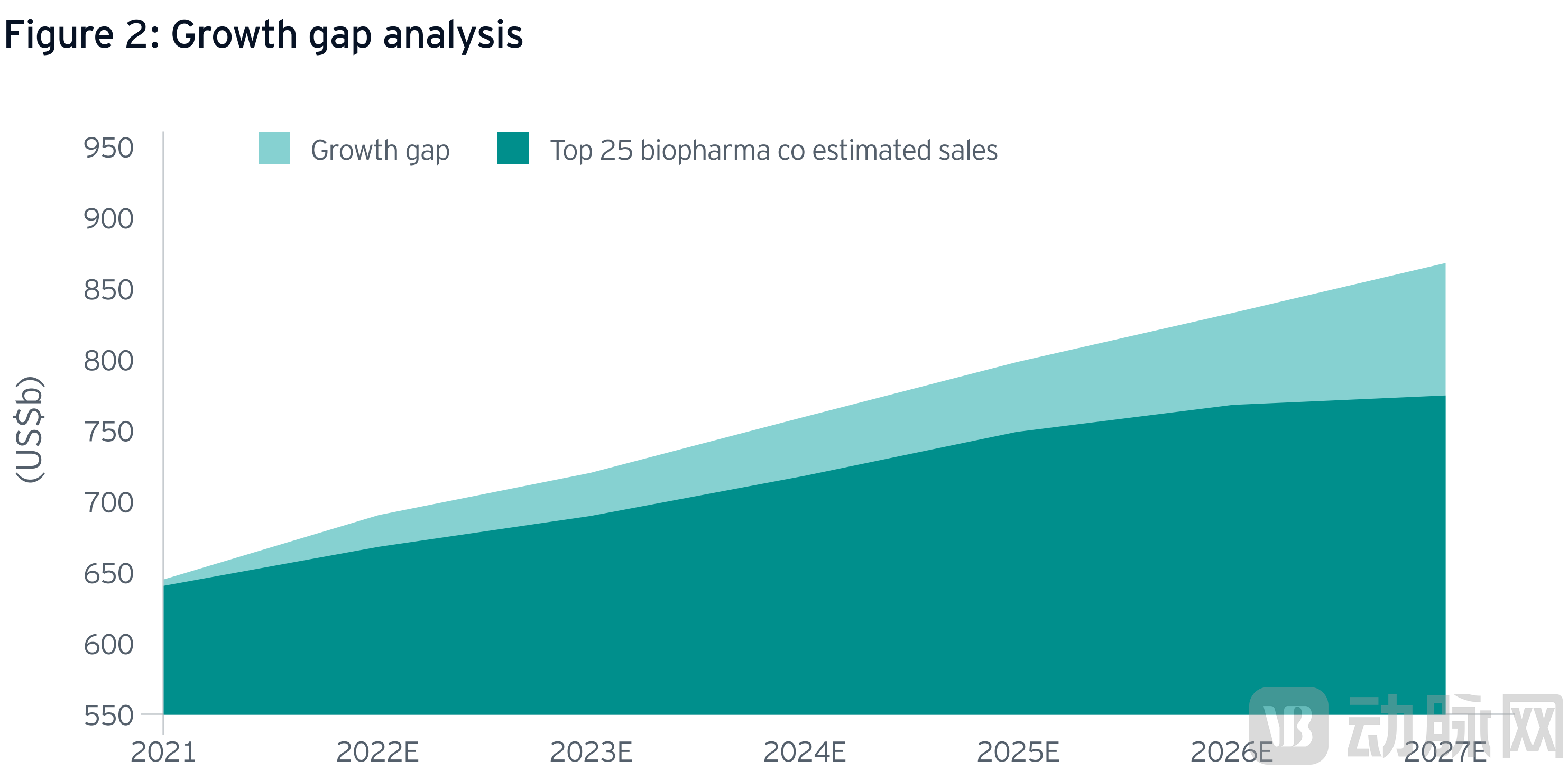

1. The industry faces a visible growth gap, particularly concerning patent expirations. According to current forecasts, as key products lose patent protection and face competition from lower-priced generic drugs and biosimilar challengers, the biopharmaceutical industry will suffer significant revenue losses over the next decade (see Figure 2).

Note: The growth gap analysis is based on pharmaceutical data evaluated in October 2022, excluding the impact of COVID-19 vaccines and therapeutics. The impact was projected to be most significant during 2021–2023, while from 2023 to 2027, moderate income losses are expected to increase year by year. The most effective strategy for Big Pharma to mitigate these losses is to secure patents in emerging therapeutic areas through mergers and acquisitions or innovation, thereby maintaining their competitive advantage.

Source: EY’s 2023 M&A Power Report

2. The industry is undergoing an innovative renaissance, providing companies with potential avenues to secure products that ensure their future growth. Due to the impact of the pandemic, a variety of new therapies—including cell and gene therapies as well as mRNA platforms—are entering the market. In the post-pandemic era, platform technology companies capable of developing new drugs will become highly sought-after targets for mergers and acquisitions.

3. Smaller life sciences companies have fewer opportunities to enter the public market, as IPOs and SPAC financings have become more challenging, thereby increasing the likelihood of exiting through mergers and acquisitions (M&A). The rapid decline of the IPO market has narrowed the options available to smaller companies. Financing needs will drive small companies to pursue M&A.

EY also summarized several M&A trends in recent years in its report.

First, to reduce trade costs, one should enter the M&A market as early as possible.

For a long time, biotech companies have reduced M&A risks by acquiring late-stage, relatively mature clinical assets—particularly products with strong growth potential. However, while this approach mitigates risk, it forces big pharma companies to pay substantial premiums. Big pharma clearly recognizes that they must either pay a premium to reduce acquisition risks or act earlier in the R&D process to secure innovation. Targets in pre-Phase III clinical stages accounted for 50% of M&A deal volume in 2022, marking the first time this has occurred since 2010.

Secondly, Biotech companies with deep expertise in specific fields are easier to sell than those with broad portfolios.

Although there are no explicit rules, analysis of past trends indicates that bolt-on acquisitions yield better outcomes when the target company operates in therapeutic areas closely aligned with the acquirer’s core portfolios. These findings are consistent with EY’s analysis, which suggests that companies are more likely to succeed by building depth and expertise in specific therapeutic areas than by pursuing diversification across a broad range of therapeutic fields.

Original article link:

1.2023 EY M&A Firepower report

https://www.ey.com/en_us/life-sciences/mergers-acquisitions-firepower-report

2.The top 10 biopharma M&A deals of 2022

https://www.fiercepharma.com/pharma/top-10-ma-deals-2022

3.Semper Maior: Time to Reboot Biotech

https://rapport.bio/all-stories/time-to-reboot-biotech