Will Teladoc Health Rebound or Plunge Deeper After a $13.7 Billion Annual Loss?

Teladoc

Telemedicine Service Provider

After reporting a record-breaking massive loss in the second quarter of last year, Teladoc, the pioneer of internet healthcare, released a relatively optimistic financial report for the third quarter of last year, with further narrowing losses, suggesting that the worst days may be over. However, this optimism did not last even two days before investors were dealt another blow.

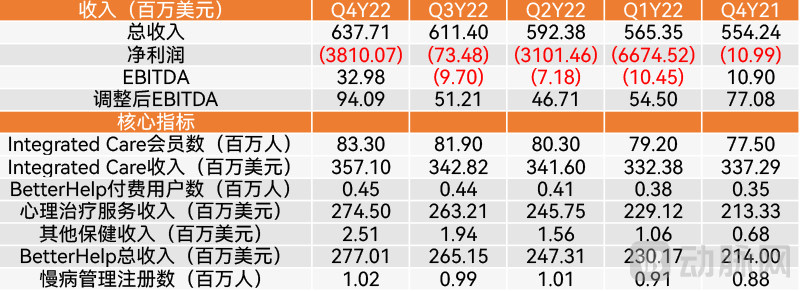

In late February 2023, Teladoc released its financial report for the fourth quarter of fiscal year 2022, reporting a quarterly loss of $3.81 billion (approximately RMB 26.289 billion) and a staggering annual net loss of $13.66 billion (approximately RMB 94.254 billion), which was alarming.

Undoubtedly, this pioneer of internet healthcare is facing an extremely severe situation. How can it save itself? Will it hit bottom and rebound or plunge into the abyss as it walks on thin ice? VCBeat (WeChat ID: VCbeat) has analyzed this issue.

A review of the full year reveals that,The primary driver of Teladoc’s massive net loss was the goodwill impairment resulting from its acquisition of Livongo. Three rounds of impairments resulted in a total full-year loss of $13.4 billion, accounting for the vast majority of its $13.66 billion net loss for the entire year 2022.

Teladoc’s Recent Financial Results Are Rather Disappointing (Graphic by VCBeat)

Back in August 2020, Teladoc’s blockbuster acquisition of Livongo, valued at $18.5 billion, propelled the combined entity to a valuation of $38 billion, marking an unprecedented milestone in the history of digital health. As the pioneer of telemedicine, Teladoc joined forces with Livongo, then the leading player in diabetes management and a frontrunner in digital therapeutics. This merger represented the convergence of “telemedicine + digital therapeutics”—a trend that remains widely recognized to this day.

At the time, both companies were racing ahead in their respective lanes. Driven by the surge in demand for internet healthcare amid the COVID-19 pandemic, Teladoc’s performance soared in the first half of 2020, with revenues increasing by more than 30% for two consecutive quarters prior to the acquisition, while its stock price skyrocketed from around $80 at the beginning of the year to approximately $190.

Livongo achieved a 253% revenue growth in just three quarters after its IPO in July 2019. Its revenue in the first half of 2020 was already very close to that of the full year 2019, with a net loss of only $7 million for the six-month period, bringing it near profitability. This performance is nothing short of legendary for a digital health company that had been in operation for only five years.

Although Livongo’s member count is only a fraction of Teladoc’s, its service price per unit is significantly higher. This is due not only to the essential nature of diabetes management but also to its integrated hardware-and-software service model: users who subscribe must also purchase Livongo’s connected devices, such as blood glucose meters, blood pressure monitors, or smart scales, to monitor the corresponding health data.

On one hand, Teladoc aims to increase the average revenue per member through this acquisition. On the other hand, patients with diabetes often present with comorbidities, creating corresponding healthcare needs. Through internal conversion, the merged entity can deliver more comprehensive services and unlock additional demand, with the core objective remaining the enhancement of average revenue per member.

However, the newly merged company peaked at its debut, with business stagnating shortly after reaching a brief high. While the post-pandemic decline certainly contributed to the downturn, it alone cannot account for such disastrous results. According to recent interviews by foreign media with former Livongo executives, cultural integration issues between the two companies appear to be one of the primary causes.

Zane Burke, the former CEO of Livongo, stated in an interview with foreign media that Teladoc’s leadership team possessed strong confidence. This was hardly surprising given Teladoc’s robust performance growth at the time. Ultimately, only the Chief Human Resources Officer from Livongo’s senior management joined the executive team of the newly merged company.

“Although I think putting shackles on people is a terrible idea, that doesn’t mean you shouldn’t create incentives to encourage them to stay. On the contrary, it’s important.” Boke’s remarks made no secret of his dissatisfaction with Teladoc.

The acquisition proceeded so rapidly that the two parties had little understanding of each other, resulting in a significant cultural divide. Bock expressed strong alignment with Teladoc’s vision for integrated virtual care, but he also noted that communications throughout the acquisition process were conducted almost entirely virtually: “I actually like Jason (Jason Gorevic, CEO of Teladoc), butWe first met in the fall of 2022. We actually completed the entire transaction virtually.”

“We didn’t proactively seek to engage in transactions with them,” Bock further mentioned: “We had just raised $500 million. Our top-line revenue saw triple-digit growth, our profit margins exceeded 70%, and we had just turned EBITDA positive. That was when we left the company. At the time of our departure, it was a terrific business.”

Although the concept was flawless, Teladoc failed to effectively promote chronic disease care among its members. Due to a lack of corresponding incentives, nurse practitioners under Teladoc had no motivation to identify patients with chronic conditions for cross-selling purposes. Furthermore, employers, as payers, lacked any incentives to encourage their employees to use Livongo’s services.

However, Teladoc refuted this claim, stating in a press release that in 2019, only 3% of Teladoc members used more than one chronic condition management program. This proportion has now risen to 28%.

An obvious challenge lies in the fact that, prior to the acquisition, Teladoc’s services were episodic and short-term, with members seeking help only when experiencing symptoms. In contrast, Livongo’s chronic disease management requires long-term, continuous, and deep engagement. Effectively integrating these two distinctly different models within a single system is not only a challenge faced by Teladoc but also an issue that must be addressed by the broader digital health sector, which is increasingly keen on combining with digital therapeutics.

Teladoc has also taken numerous measures to address this challenging situation.First, cost-cutting measures: In January, Teladoc implemented a round of layoffs, reducing its non-clinical workforce by 300 employees, representing approximately 6% of its total headcount. Additionally, the company downsized office space in certain regions to further reduce expenses.

For Teladoc, integrating its currently somewhat fragmented services is undoubtedly a top priority. Therefore, in January 2023,Teladoc has launched its new Teladoc Integrated Care and released a brand-new app, integrating Livongo’s chronic disease management business into the platform.

At least on the surface, this change has integrated Teladoc’s core businesses, including primary care, mental health, and chronic condition management. Users can now access all of Teladoc’s services through a single app and account. This restructuring has also led to changes in how Teladoc reports its financial results: the chronic condition management segment, which previously represented the Livongo business, is no longer reported separately. Perhaps Teladoc’s executives prefer not to be reminded of this business line, which incurred substantial losses.

Teladoc’s new app also adds Spanish-language support for the first time, aiming to appeal to the significant Spanish-speaking population in the United States.Currently, the Hispanic population has become the largest ethnic minority group in the United States. According to data from the U.S. Census Bureau, as of 2020, the Hispanic population in the United States was approximately 64.65 million, accounting for 19% of the total U.S. population.

For years, these populations—primarily from Mexico, Puerto Rico, Cuba, and other Spanish-speaking regions of Central and South America—have faced severe challenges in education, economics, and healthcare. Due to generally low levels of educational attainment, they are often confined to low-income jobs. Insufficient income prevents them from purchasing health insurance, making it difficult for many to access timely medical care.

Meanwhile, many Hispanic individuals may be unable to access appropriate medical services due to cultural and language barriers. They may not understand physicians’ recommendations and may lack knowledge of how to navigate the U.S. healthcare system to obtain care.

Teladoc’s launch of Spanish-language services will help address healthcare disparities among the Hispanic population and foster greater acceptance within this community. Given the rapid growth of the Hispanic population, which is projected to account for approximately one-quarter of the U.S. population by 2025, this move is undoubtedly a sound strategy for Teladoc’s long-term growth.

Furthermore, statistics indicate that Hispanics in the United States face a higher risk of chronic diseases, such as diabetes, hypertension, and heart disease. These conditions may be associated with dietary and lifestyle factors, as well as genetic predispositions. This clearly represents a significant growth opportunity for Teladoc.

In fact, Teladoc onboarded more than 100 new Spanish-language providers in 2022. These initiatives have been well received. By the end of 2022, satisfaction scores among Spanish-speaking members had surpassed those of non-Spanish-speaking members.

In addition to integrating existing services, BetterHelp, which was previously included in Teladoc’s revenue, also grew rapidly, becoming one of the few highlights in the financial report.

In January 2015, Teladoc completed its acquisition of BetterHelp for $3.5 million in cash and a $1 million promissory note. It has since grown into a major online mental health service platform, aggregating more than 25,000 online psychotherapists. Due to the surge in psychological issues triggered by the COVID-19 pandemic, demand for mental health services has outstripped supply. As a result, BetterHelp has experienced rapid growth in recent years.

According to media reports, BetterHelp compensates therapists on a pro-rata basis according to the number of hours worked per week. Typically, the first five hours are paid at $30 per hour, and the next five hours at $35 per hour. Once weekly working hours exceed 35, subsequent hours are compensated at a maximum rate of $70 per hour. This is significantly lower than the $100–$200 per session charged by private-practice psychologists in the United States, making the platform popular among users.

Psychologists within the BetterHelp network also receive additional compensation from BetterHelp, including monthly stipends, group therapy fees, bonuses, and incentives based on caseload volume. According to BetterHelp’s public statements, psychologists affiliated with BetterHelp in urban areas earn, on average, 60% more than the median compensation of locally practicing psychotherapists.

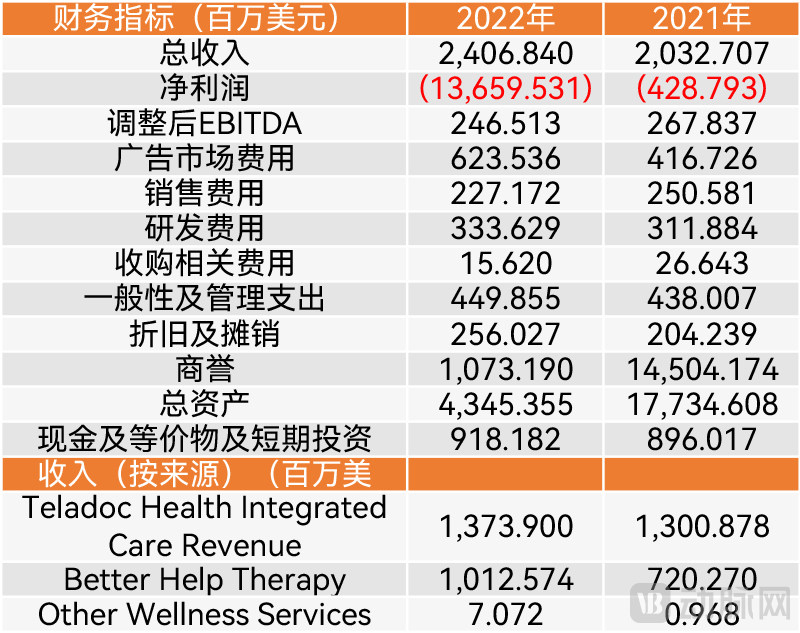

According to the financial reports, BetterHelp has experienced steady growth over the past year.In 2021 alone, BetterHelp generated $720 million in revenue, representing approximately 55.4% of the Integrated Care segment’s revenue. By 2022, BetterHelp’s revenue surged by 40.6% to reach $1.013 billion, equivalent to 73.7% of the Integrated Care segment’s revenue for that year.。

BetterHelp’s revenue is already very close to that of its core business.

Clearly, compared with the acquisition of Livongo, BetterHelp’s deal represents far greater value for money. If it maintains its current growth momentum, BetterHelp could well become the key to Teladoc’s turnaround in the future.

Nevertheless, BetterHelp faces significant challenges.First is the efficacy of treatment.BetterHelp offers various online communication methods, including video and text-based chat. However, the efficacy of text-based chat lacks robust research support, raising concerns about its potential ineffectiveness. Additionally, responses from online therapists are often delayed, with some patients waiting several hours to receive a reply from their therapist. This significantly casts doubt on the overall utility of such services.

Meanwhile, due to revenue reasons, including BetterHelp'sMost online psychotherapy services tend to attract only less experienced therapists.They use it as a springboard to enter the industry, joining as independent service providers without corresponding insurance coverage. Although this cannot be equated with the level of treatment, it still raises certain concerns.

Frankly speaking,BetterHelp’s business model is heavily reliant on human involvement and has not integrated with the increasingly popular digital therapeutics for mental health, making it appear somewhat outdated.. This also explains why Ali Parsa, CEO of Babylon Health, holds a lukewarm view of its business model, considering it predominantly physical in nature, with digital technology serving merely as technical support rather than a core strategic priority. Due to the lack of end-to-end technological capabilities and the adoption of an asset-heavy physical model, its business scalability is relatively limited and slow.

Furthermore,BetterHelp also has certain data security issues.The U.S. Federal Trade Commission (FTC) previously alleged that the company shared users’ health data with internet companies such as Meta and Snapchat for advertising purposes. BetterHelp denied these allegations, stating that it only used limited encrypted information to optimize ad effectiveness, a practice it described as common within the industry.

Not long ago, BetterHelp reached a settlement with the FTC after paying $7.8 million to users whose health data was allegedly shared. As part of the settlement, BetterHelp is now prohibited from sharing user health data with third parties for advertising purposes.

This may not have a significant impact on BetterHelp’s advertising business, but it is clearly bad news for its reputation among users. Negative reviews of BetterHelp are not uncommon on TikTok. If this affects future business development, it would be unfavorable for Teladoc at present.

For Teladoc, this is arguably its most perilous moment. The substantial losses resulting from consecutive goodwill impairments have severely undermined market confidence. Meanwhile, a brief review of Teladoc’s financial statements reveals that the company still carries over $1 billion in goodwill on its balance sheet. Given the current circumstances, further impairment charges are highly likely in the future. Should performance decline or growth slow at that time, investor confidence would be dealt an additional blow.

Meanwhile, BetterHelp, a key focus of Teladoc’s recent investments, has encountered some negative issues. Whether it can sustain high growth remains to be seen over time. Any slowdown in its growth would significantly impact Teladoc’s revenue.

The good news is that Teladoc has completed various measures, including business integration and layoffs, which essentially means the negative factors have been fully priced in. Currently, its various businesses continue to see stable growth, with its Q4 2022 and full-year financial reports reaching the upper end of previous earnings forecasts. Meanwhile, the company still holds over $900 million in cash, cash equivalents, and short-term investments.

Another piece of good news is that, unlike the initial catch-off-guard scenario, investors were somewhat psychologically prepared for Teladoc’s performance, resulting in a relatively modest fluctuation in its stock price. Over the course of one week (from February 22 to March 3), the share price declined from $29.43 to $26.88, representing a drop of approximately 9%.

In the long term, telemedicine still holds bright prospects. According to forecasts, the global telemedicine market size will reach $285 billion by 2027, with a compound annual growth rate (CAGR) of 26%. As the pioneer of telemedicine, Teladoc, having boarded the fast track, still has significant opportunities to turn the tide and secure its recovery.

However, Teladoc’s leadership has virtually no room for maneuver or error. Historically, its high growth was largely driven by continuous acquisitions, raising concerns about whether a cash-strapped Teladoc can sustain rapid expansion. Should growth in its existing business stall, the challenges facing Teladoc will become quite severe.

We will continue to closely monitor the future trajectory of this pioneer in internet healthcare.

References:

Heather Landi,Fierce Healthcare:Teladoc-owned BetterHelp to pay $7.8M to online therapy users for alleged data misuse, per FTC order

Arundhati Parmar,MedCityNews:With Livongo, did Zane Burke sell a lemon to Teladoc’s Jason Gorevic?

Harris Meyer, Kaiser Health News:Digital mental health firms draw scrutiny and growing concerns

Chris Hill,The Motley Fool:Teladoc Health: Bull vs. Bear