From Funding Winter to BD Inflection Point: The Dawn of China Biotech's Global Licensing Wave

Prior to 2022, business development (BD) was primarily an asset allocation strategy employed by large pharmaceutical companies and well-capitalized entities. However, over the past year, a company’s capability in cross-border BD has become a critical dimension for assessing the strength of innovative enterprises, serving even as an endorsement of their innovativeness and fundraising capacity—a point repeatedly emphasized and acted upon by investors and the industry. The “spotlight” on companies is no longer defined merely by backing from top-tier capital or large financing rounds; instead, securing “high-profile deals” has often been what shifts the focus of both primary and secondary markets.

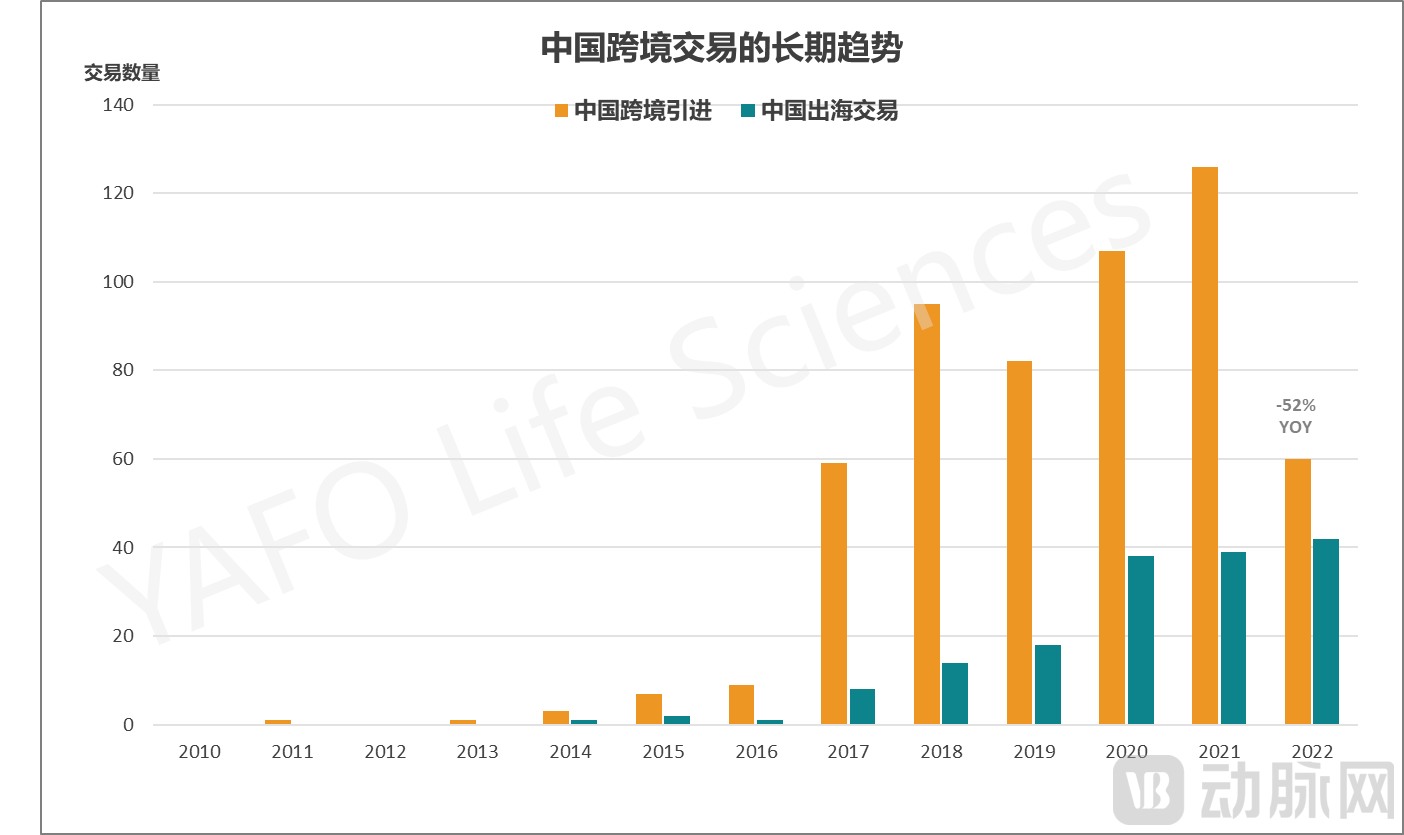

2022 was a turning point for China’s BD industry.

The turning point is multifaceted. At the data level, China’s total cross-border transaction volume experienced its first significant decline in 2022 after five years of robust growth, with a year-on-year decrease of 52%. This drop was primarily driven by license-in deals, which fell from 126 in 2021 to 60.

Meanwhile, the window for license-out deals has opened. In 2022, the trend of Chinese innovative drugs going global became pronounced. While the number of transactions remained comparable to previous years, the total value of outbound deals reached a record high of $26 billion, with a significant improvement in deal quality, as upfront payments surpassed the $1 billion mark.

At the project level, diverging from the previous demand for diversification of overseas assets, Chinese pharmaceutical companies as buyers generally showed a stronger preference for late-stage assets last year; on the sell side, the situation was different, with more early-stage, innovative assets being licensed out.

Trends in China’s Cross-Border Licensing Transactions (Source: YAFO Capital 2022 Cross-Border Licensing Transaction Report)

Follow the “VBInsight” WeChat Official Account and reply with “BD Report” to obtain the original report.

As a pioneer in cross-border business development (BD) transactions, YAFO Capital has completed its first decade, with founder Jiang Xiaoyang having witnessed the evolution of the BD landscape over the past ten years.He recognized the shifts in business development (BD) demand driven by the structural changes in the venture capital and private equity industry in 2022, fully understanding that “BD roles are permanent, while strategies are transient.” Different market environments present different transactional opportunities. In a bull market, YAFO Capital focuses more on assisting Chinese enterprises in acquiring overseas assets. In a bear market, when corporate financing becomes challenging, YAFO Capital prioritizes helping companies establish external collaborations for their products.

Drawing on YAFO Capital’s “2022 Report on Cross-Border Licensing Transactions of Innovative Drugs in China,” VCBeat New Medicine spoke with Jiang Xiaoyang.Our discussion covers BD trends behind the data: Can this wave of global expansion continue in 2023? And how can Chinese biotech companies leverage the industry’s rebound to gain momentum?

VBInsight: What Trends from China’s 2022 Cross-Border Transaction Data Deserve Our Attention?

Jiang Xiaoyang:The volume of cross-border transactions in China maintained steady growth for five consecutive years starting from 2017, but experienced a significant decline for the first time in 2022, dropping by 45% compared to the previous year. A breakdown of license-in and license-out deals reveals a mixed picture, with stark contrasts between the two.

The downward trend in license-in deals is quite evident, primarily because buyers are inclined to select assets at later stages of development, naturally resulting in fewer large-scale transactions.In addition, the buyer landscape in the market is also shifting. Last year, large pharmaceutical companies remained highly active as the primary acquirers, while transaction volumes involving biotech firms as buyers contracted significantly.

From the perspective of Chinese innovative drugs going global, last year was overall a very inspiring year.Although the number of transactions remained stable at approximately 40, similar to previous years, the total transaction volume reached a historic high of $25 billion. The quality of deals also showed significant improvement, with upfront payments surpassing the $1 billion mark.

VBInsight: You have just interpreted the major trends based on data. At the project level, what subtle changes have emerged in terms of in-licensing and global expansion?

Jiang Xiaoyang:Chinese companies, acting as buyers, previously demonstrated diversified demand for overseas assets across early-, mid-, and late-stage categories. However, a clear shift emerged last year, with a pronounced preference for late-stage assets—prioritizing lower regulatory registration risks even at the expense of reduced innovativeness.

In contrast, on the sell side, a greater number of early-stage, innovative assets were traded last year.In outbound licensing deals in 2020 and 2021, transactions involving assets at Phase III clinical trials or later accounted for more than half of the total. However, by 2022, this proportion had dropped to 34%, while early-stage assets (preclinical and Phase I) comprised 50% of transactions. Meanwhile, mega-deals with upfront payments exceeding USD 100 million occurred frequently. Akeso and Kelun Pharmaceutical secured the two largest license-out deals in China in 2022.

More importantly, we are witnessing a surge in mid-tier transactions focused on the “indication” level. We define mid-tier transactions as those with upfront payments ranging from $20 million to $100 million. For instance, Jimin Kexin secured $76.5 million in cash upfront payments by licensing its prostate cancer therapeutic product in the drug discovery phase to Genentech, and its preclinical pain management product to Orion. This reflects the increasingly diversified demand for Chinese assets in overseas markets.

VCBeat New Medicine: As buyers, firms are more willing to acquire late-stage, low-risk assets; as sellers, they favor early-stage assets, with a rise in mega-deals. This stark divergence between the buy and sell sides marks a pivotal shift. What kind of BD year lies ahead?

Jiang Xiaoyang:China’s overseas licensing-out activities will continue to gain momentum; I believe this wave is just beginning., unlike the acquisition of overseas assets, where the peak has already passed. Therefore, Chinese companies should seize this opportunity; in particular, biotech firms should capitalize on this window and even explore collaboration opportunities in non-mainstream markets, with deal closure as the primary objective.

VCBeat New Medicine: As the tide rises and more players flood into the BD market, what are your reflections and advice as an experienced veteran?

Jiang Xiaoyang:In fact, last year saw the emergence of several new small and mid-sized pharmaceutical companies in the market. Compared with leading large pharmaceutical firms, they tend to have relatively less experience in global business development (BD). As China’s pharmaceutical industry enters a new phase, we need to provide substantial coaching in deal-making, leveraging our international-localization team and network to offer support.

From 2016 to 2019, we traveled extensively across Europe, the United States, and Japan, spending one-third to one-half of each quarter on business trips to build our global partner network. By 2021, as the pandemic restricted travel, we suddenly found that our network began to demonstrate its value worldwide.

"The Art of War" states that those who fail to make effective use of guides cannot secure the advantage of terrain. In cross-border transactions, it is crucial to leverage "local connections."Over the past decade, we have been highly focused on building a multilingual, globalized local team. Our overseas partner network covers a broad range of regions, including the United States, Japan, Europe, and even India, with team members collectively speaking approximately 10 different languages.

Building such a team is primarily based on considerations across three dimensions: first, local language; second, local culture; and third, local relationships.Fluency in the local language and an understanding of cultural differences enable us to determine appropriate pricing strategies and negotiation approaches. Finally, at the relationship level, since cold outreach is difficult in many countries—much like in China—we strive to establish the most direct connections possible. In a project last year, our U.S. colleague and the head of the overseas project team happened to be former colleagues from many years ago, which proved crucial in advancing subsequent negotiations and ultimately closing the deal. Within our global network, trust with transaction partners and YAFO Capital has been built through years of project communication and collaboration, which greatly facilitates rapid project advancement.

Furthermore, many resources, including teams, are difficult to build in the short term. When China’s biopharmaceutical capital market was still at a relatively high point, we looked slightly further ahead and established our China business division one or two years earlier than usual. Now that the market has cooled down while demand has risen, we are well-positioned to meet it.

VBInsight: Under the global business development (BD) network, what patterns emerge in transaction matching between buyers and sellers? What types of partners are more likely to close deals?

Jiang Xiaoyang:During our research, we observed a rather intriguing phenomenon. Previously, it was widely assumed that multinational corporations (MNCs) would be the most interested buyers in large-scale Chinese companies and blockbuster projects, given their stronger market capacity to undertake such initiatives; meanwhile, biotech firms were considered the most natural partners for other biotech companies. However, an analysis of the entire transaction data reveals a contrary conclusion.

It is rare for multinational corporations (MNCs) to acquire mature late-stage assets in China. MNCs tend to prefer acquiring distinctive projects at relatively early stages. Meanwhile, Chinese blockbuster projects are more frequently developed through collaborations with mid-sized overseas pharmaceutical companies, which possess certain market capabilities but are not top-tier MNCs.

This is related to the global portfolio strategies of overseas multinational corporations (MNCs). For MNCs, introducing product pipelines is akin to venture capital firms making early-stage equity investments; they seek balance and possess the long-term patience required to wait for and nurture these assets. Of course, if the data proves unsatisfactory, they may return the assets and terminate the transaction.

VBInsight: How to View the Recent Rejection of Two Chinese Projects in Overseas Markets?

Jiang Xiaoyang:Asset divestment is common in cross-border transactions. Each year sees both new product deals and the termination of older ones. There are many reasons for asset returns; the return of an asset is not necessarily solely due to the product itself, but may also be related to various factors such as a company’s new strategic layout, capital planning, and partnership dynamics. Even multinational corporations (MNCs) with relatively ample funds and higher risk tolerance must comprehensively evaluate multiple factors when deciding whether to continue advancing an asset. Therefore, we should not attribute the specific reasons for the return of these two projects to a single cause.

However, in terms of transactions between China and overseas markets, there have been nearly 1,000 deals over the past five years, including both in-licensing from abroad and the global expansion of Chinese products. Given this substantial volume of pipeline transactions, when multiplied by the product development success rate, it is evident that the number of product failures certainly exceeds one hundred, although fewer such cases may be publicly announced. These two transaction news items were disclosed, thus attracting greater attention. This is quite normal.

VBInsight: We have observed a phenomenon of "substance versus prestige" in BD deals. For instance, collaborations with MNCs may not always offer the most favorable pricing, but they provide brand equity and endorsement. What is your perspective on this strategic choice in transaction structuring?

Jiang Xiaoyang:I fully agree with the perspective on the “face” and “substance” of BD deals. Most Chinese companies seeking to go global that we engage with typically insist on initiating discussions with multinational corporations (MNCs), as MNCs are more likely to facilitate large-scale transactions—a preference I consider quite natural. However, MNCs exercise extreme caution in their decision-making and pricing, and they maintain stringent control over the deal timeline. In some cases, our projects have even been subjected to evaluation by global R&D teams; at one point, a single conference call involved nearly 50 participants from around the world, while only five people represented us and the project sponsor combined—illustrating just how challenging such transactions can be. That said, successfully closing these deals undoubtedly brings considerable prestige.

Transactions reached with MNCs may account for a significant proportion of the total value, but they remain few in number.More of the action lies in the “under-the-radar” mid-tier transactions; these counterparties may well be the overseas partners that deserve greater attention.

VBInsight: In transactions involving YAFO Capital, what are some typical deal breakers? How should they be addressed? What has been the greatest challenge encountered?

Jiang Xiaoyang:There are quite a few deal breakers. Our own motto is, “We get tough deals done.” In retrospect, it seems that very few of our projects have been free from transactional challenges or closed with ease. Or rather, such cases are extremely rare—perhaps only one or two out of every ten to twenty transactions.

We set a record during the pandemic by completing a cross-border transaction in less than six months. Apart from that, project cycles typically require nine to twelve months, or even up to eighteen months. Particularly over the past three years, due to geographical separation, we have served as our overseas clients’ on-the-ground representatives in China, facilitating face-to-face negotiations with Chinese clients and helping to build sustained trust. I consider this the first level of challenge.

As Chinese companies expand overseas, the prevalence of large-scale deals has fueled a common aspiration among industry players to secure such landmark transactions. This desire for mega-deals is only natural. However, it is quite challenging for every company to expect upfront payments of $100 million. Therefore, another significant challenge lies in analyzing historical overseas transactions to help clients establish realistic expectations for international markets, thereby facilitating more efficient deal closures—a task of considerable importance.

This year marks YAFO Capital’s tenth year in cross-border transactions. Having facilitated dozens of deals, we recognize that merely connecting buyers and sellers accounts for only 10% of our work. The remaining 90% consists of advisory services that go beyond simple matchmaking. Particularly when deal breakers arise, proposing innovative solutions represents a critical value addition.

VCBeat New Medicine: YAFO Capital has witnessed the industry’s evolution over the past decade. We are curious whether it has also observed the comings and goings of professionals within the circle, as individuals serve as powerful participants and drivers of history.

Jiang Xiaoyang:Over the past two years, the turnover rate of BDs has been extremely high, yet it remains the same core group of people behind the scenes. I refer to this as“Ironclad BD, Flowing Barracks”Over the past few years, the industry has likely accumulated hundreds or even thousands of business development (BD) professionals with transaction experience. They have undertaken diverse roles across different companies and through various industry cycles. During downturns in the capital market, there was a surplus of BD talent specializing in license-in transactions. Currently, as companies increasingly seek to out-license their products to overseas markets, there is a severe shortage of BD professionals capable of handling license-out deals, given the higher complexity and entry barriers associated with such transactions. Of course, some senior BD professionals can swiftly adapt their roles in response to shifting market demands, demonstrating proficiency in both product in-licensing and out-licensing.

I personally enjoy working in the BD industry; it is very exciting.

Follow the “VB New Medicine” WeChat Official Account and reply with “BD Report” to access the original report.