2023 Rehabilitation Robotics Industry Report: Rapid Market Recovery, Record-High Funding, and Emerging Trends in Out-of-Hospital and Early-Stage Rehabilitation

Preface

The results of the seventh national population census in 2020 have propelled rehabilitation medicine into an unprecedented wave of growth. The population aged 60 and above reached 264 million, accounting for approximately 18.70% of the total population—a 5.44 percentage point increase from a decade ago. Moreover, this figure is projected to rise further as fertility rates decline. The rapid onset of population aging has caught many by surprise, while the subsequent policy measures underscore the nation’s high level of attention to this issue.

From “surviving” to “thriving in health” has become the pursuit of people in the coming era; however, the shortage of rehabilitation therapists and their uneven professional standards fail to meet this demand. From rehabilitation to assistance, rehabilitation robotics is an emerging field on the rise.

Amid continuous technological innovations and numerous product approvals, commercialization remains a challenge—a struggle mirrored abroad. What “philosophy” and “methodology” will rehabilitation robots follow to provide answers to the questions of our time?

Guided by these questions, we engaged in discussions with more than 16 companies and nearly 30 experts, and authored the “2023 Rehabilitation Robotics Industry Research Report,” which primarily examines the current state of commercialization and future trends in rehabilitation robotics. Regarding products, application scenarios, and stages of rehabilitation, we have drawn the following conclusions:

Broadening Indications and Expanding Functions Have Become Product Development Trends, with Continuous Iteration in Comfort and Intelligence。Current rehabilitation robots primarily target the upper limbs, lower limbs, joints, and hands. Future developments may extend to the spine and other indications, such as osteoporosis, while expanding and integrating functional capabilities. The target population has broadened from patients requiring rehabilitation therapy to individuals with mobility impairments, achieving integrated assessment and training functions. In the future, product evolution will focus on enhancing comfort, safety, personalization, and intelligence, through the adoption of new materials and new energy sources, as well as the exploration of adaptive technologies. Meanwhile, products will become lighter and offer stronger interactivity.

Application scenarios are beginning to expand from within hospitals to outside settings, with communities and home care becoming key battlegrounds.Driven by the “9073” elderly care model, policy incentives, and increased capital investment, domestic enterprises are also expanding into community- and home-based sectors, offering integrated rehabilitation solutions. The consumer-facing (B2C) market holds immense potential; in the future, as public awareness of rehabilitation strengthens, a wide range of products will be introduced for home use, making home and community rehabilitation centers key battlegrounds for large, comprehensive enterprises. For home-based scenarios, product diversification is inevitable. While safety remains fundamental, aesthetics, portability, and comfort will be primary focal points, while digitalization will empower the entire rehabilitation lifecycle.

Early rehabilitation has been included in performance assessments, presenting significant growth opportunities for bedside rehabilitation.。Early rehabilitation yields greater health economic benefits. With the release of the "Quality Control Indicators for Rehabilitation Medicine (2022 Edition)" and its inclusion in the "Accreditation Standards for Tertiary Hospitals (2022 Edition)," the early rehabilitation intervention rate has become a key performance indicator for tertiary hospitals.; In February 2023, the "National Healthcare Quality and Safety Improvement Goals for 2023" outlined the core strategy for increasing the rate of early rehabilitation intervention.In the future, key focus areas will include how this policy is specifically implemented, how clinical care and rehabilitation will be coordinated, and how personnel and equipment will be allocated.

In addition, products for early rehabilitation, such as bedside rehabilitation robots, will present opportunities. Currently, compared with upper- and lower-limb devices, bedside rehabilitation robots in tertiary hospitalslower hospital penetration,Moreover, there are no effective solutions to address the differentiated needs for early rehabilitation across various departments. In the future, tailored early rehabilitation solutions should be provided for departments such as neurology, orthopedics, and the intensive care unit (ICU).

Overview: Policy Tailwinds Persist, Financing Rebounds

The Lancet shows that patients in China with rehabilitation needs mainly include the elderly, postoperative patients, chronic disease patients, and people with disabilities, totaling approximately 460 million. As one of the four major branches of medicine, rehabilitation medicine not only eliminates and alleviates functional impairments in patients with diseases and disabilities but also enhances their self-care abilities and quality of life.

Taking stroke as an example, the "China Stroke Center Report 2020" indicates that China is facing the world's largest stroke challenge. According to the Global Burden of Disease Study, in 2019, there were 3.94 million new stroke cases, 28.76 million prevalent stroke cases, and 2.19 million stroke-related deaths in China.

Furthermore, stroke is the leading cause of disability-adjusted life years (DALYs) in China.

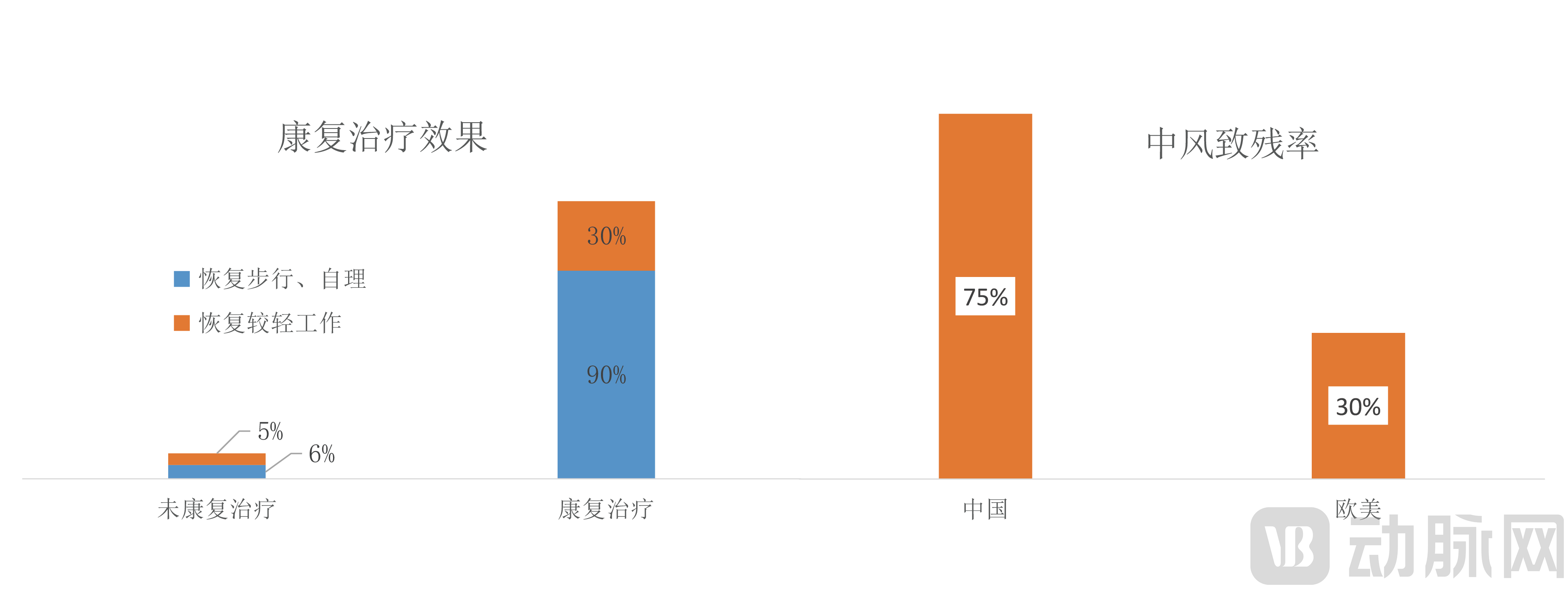

On the other hand, *Nursing Coordination in Stroke Rehabilitation Therapy* indicates that rehabilitation therapy enables 90% of stroke patients to regain walking ability and activities of daily living, and allows 30% of patients to return to light-duty work; without rehabilitation therapy, only 6% regain walking ability and activities of daily living, and 5% return to light-duty work.

Severe imbalance between supply and demand has given rise to rehabilitation robots. First, there is a significant shortage of rehabilitation professionals and institutions in China. According to the China Health Statistics Yearbook, in 2020, there were 49,000 licensed (assistant) physicians specializing in rehabilitation in China, accounting for only 1.2% of the total number of licensed (assistant) physicians in the country.

Secondly, traditional rehabilitation equipment relies heavily on the experience of rehabilitation therapists to achieve optimal outcomes. However, given the uneven competency levels among rehabilitation therapists in China, it is difficult to guarantee consistent rehabilitation efficacy using conventional devices. Amidst a shortage of rehabilitation medical resources, the stroke-related disability rate in China stands at 75%, compared to only 30% in Europe and the United States.

Finally, traditional rehabilitation devices lack quantitative evaluation metrics, making it difficult for patients to perceive the therapeutic benefits after use; this often leads to a loss of confidence and discontinuation of rehabilitation treatment.

Efficacy of Rehabilitation Therapy and Stroke-Related Disability Rates in China and Abroad

Image source: VCBeat

Rehabilitation robots, as a product of the integration of medicine and engineering, aim to assist rehabilitation therapists, streamline the labor-intensive traditional "one-on-one" therapy process, improve the efficiency of rehabilitation treatment, and help patients rebuild their central nervous system.

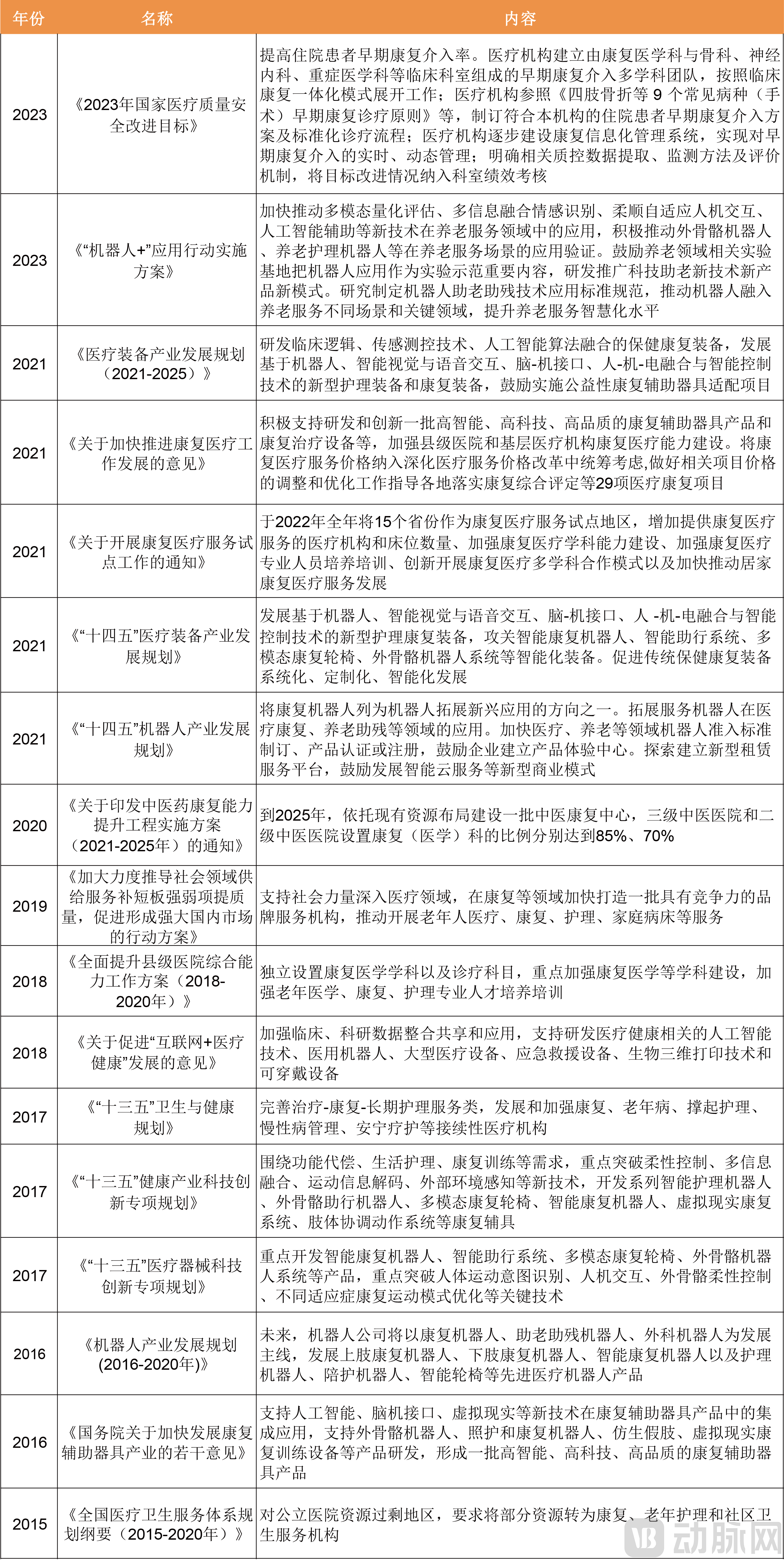

From technology to resources and then to business models, policies have become increasingly intensive in recent years. Overall, these policies mainly focus on three aspects: technology, resources, and development models.

Technologically, the focus is primarily on advancing the intelligence of rehabilitation robots, encouraging the application of emerging technologies such as human-robot interaction, brain-computer interfaces, and flexible robotics in this field. In terms of resources, investment in rehabilitation medical service institutions is being gradually increased, private capital inflow is encouraged, and insurance coverage is progressively expanding. Regarding development models, new paradigms and application scenarios are being promoted.

Review of Policies Related to Rehabilitation Robots

Image source: VCBeat

According to a Frost & Sullivan report, China’s rehabilitation robotics market emerged in 2017, reaching RMB 210 million in 2018. It is projected to grow at a compound annual growth rate (CAGR) of 57.5% in the coming years, attaining approximately RMB 2.04 billion in 2023 and around RMB 7.95 billion in 2026.

Fortune Business Insights research projects that the global rehabilitation robotics market will achieve a compound annual growth rate (CAGR) of 43.6% from 2022 to 2029, which is lower than the growth rate in the Chinese domestic market.

The aging trend and favorable policies are strong drivers of market growth. From the demand side, the increasingly severe aging problem is the fundamental force propelling the rehabilitation industry. According to data from the Seventh National Population Census, the proportion of China’s population aged 60 and above and aged 65 and above increased by 5.44 and 4.63 percentage points, respectively, between 2010 and 2020.

In 2020, there were 264 million people aged 60 and above, accounting for approximately 18.70% of the total population, while the number of people aged 65 and above reached 191 million. Older adults constituted nearly 30% of the population receiving rehabilitation medical services.

In recent years, the rehabilitation industry has gained momentum, with an increase in investment frequency. A growing number of technology-driven companies have injected fresh vitality into the market, while comprehensive enterprises are actively positioning themselves in the rehabilitation robotics sector.

Traditional rehabilitation equipment manufacturers such as Xiangyu and Weishi have also begun to enter the rehabilitation robotics sector, while affiliated companies like Siasun, Estun, MicroPort, Lepu Medical, and WEGO have started to make their move. Large corporations such as iFlytek, Samsung, Panasonic, and Midea have crossed industry boundaries to join this field.

In terms of financing, there were 10 deals in 2022 alone, marking a resurgence in funding for rehabilitation robots and related products in recent years.

What sets this resurgence apart is the significant leap forward in both technology and product development. Although China started later, the gap with international counterparts remains narrow. Today, against the backdrop of an aging population, China’s rehabilitation robotics sector has entered a critical phase of rapid expansion.

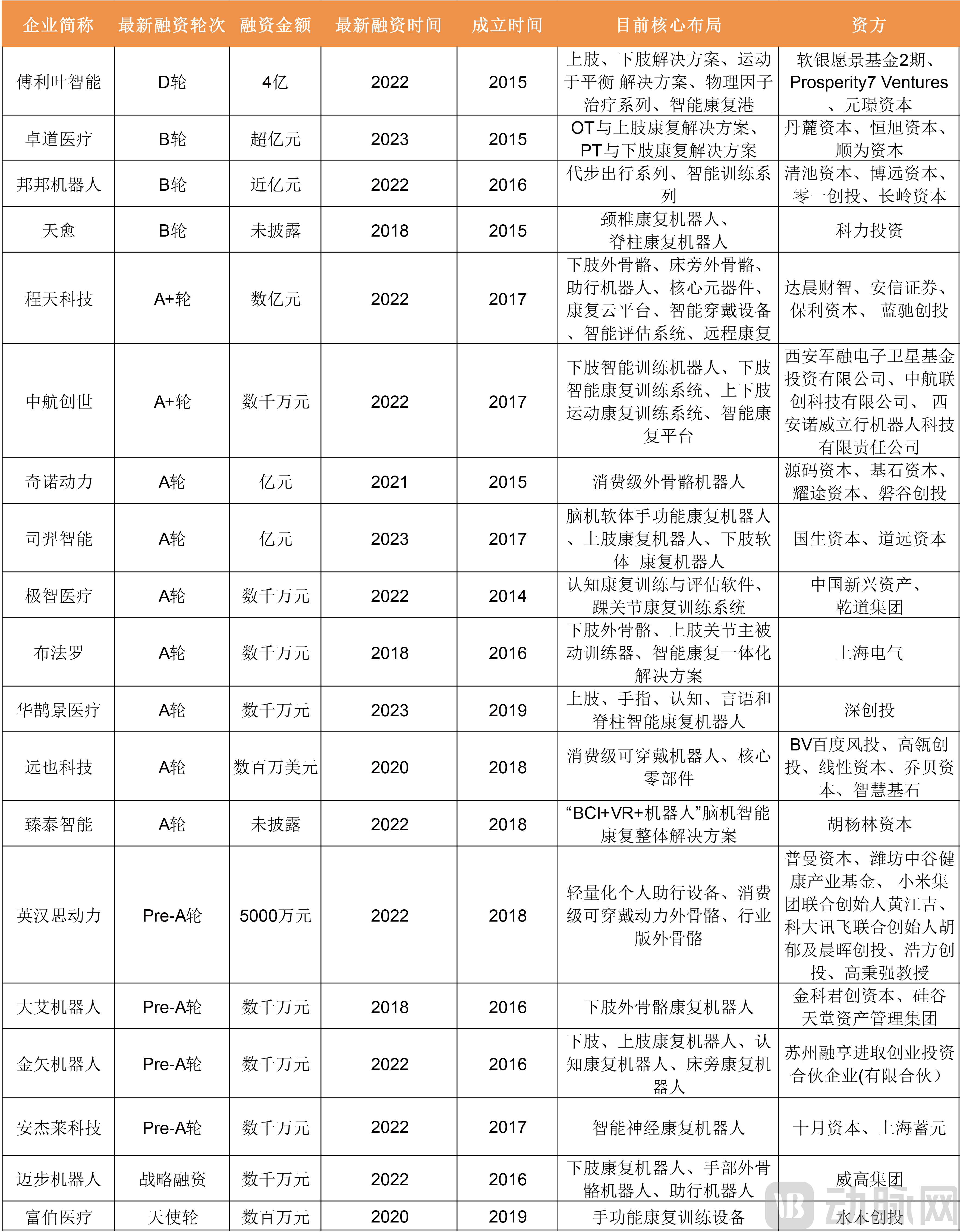

We have conducted an incomplete statistical analysis of corporate financing for rehabilitation robots and related products in recent years, as follows:

Review of Corporate Financing in Rehabilitation Robotics and Related Products in Recent Years

Image source: Compiled from public data, produced by VCBeat.

Among them, companies at Series A and below accounted for 63.2%. Notably, in 2023, there were three financing rounds with a total amount exceeding RMB 200 million, setting historical highs in both financing frequency and average deal size.

Overall, the domestic rehabilitation robotics industry is in a blue ocean stage, with low market concentration and significant potential yet to be fully realized.

Technology: Integration of hardware and software, human-computer interaction

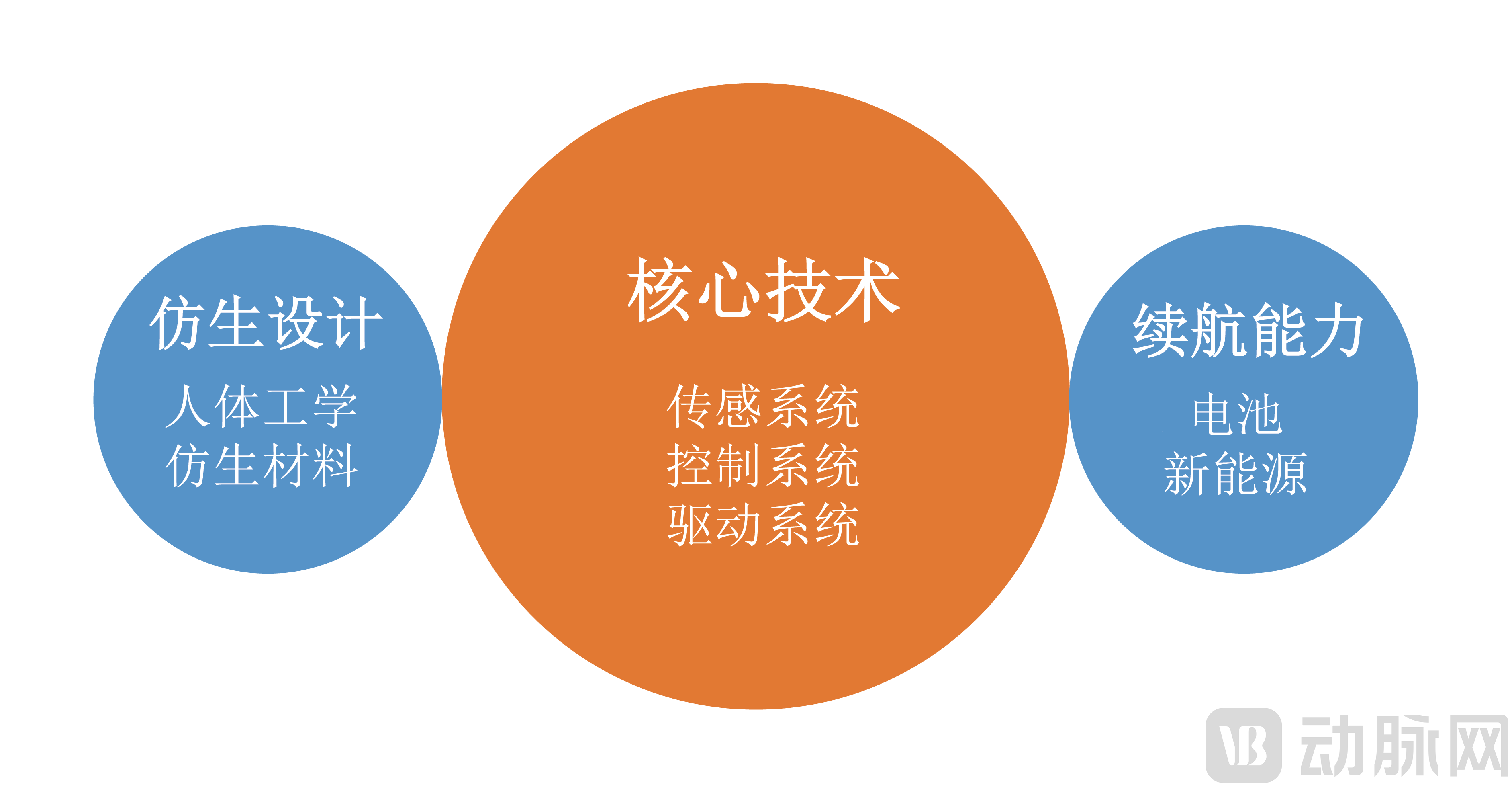

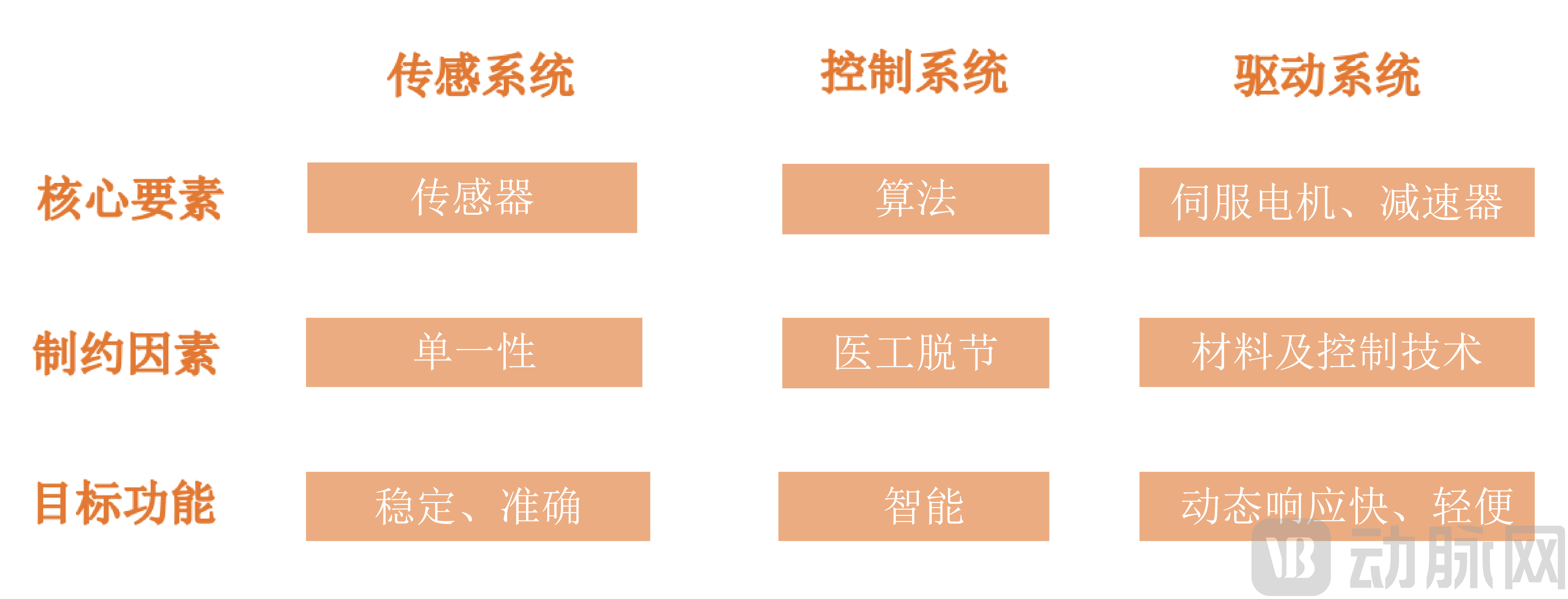

Core technology is the key to intelligent rehabilitation robots, with bionic design and battery endurance serving as value-added features. Core technology dominates the realization of system functions in rehabilitation robots, primarily manifested in three major systems: the sensing system, the control system, and the actuation system.

Bionic design primarily relies on ergonomics to create parts or components that conform to the shape and physiological movements of joints and muscles, with the goal of enhancing comfort and safety; the key breakthrough lies in the materials used.

In terms of endurance, new energy represents the future direction. For instance, leveraging bioenergy and other alternative sources to harvest and store the kinetic energy generated by human leg movements is a key area for future breakthroughs.

Three Key Points of Rehabilitation Robots

Image source: VCBeat

Specifically, the core elements, constraints, and target functions of the sensing system, control system, and drive system are as follows:

Core Elements, Constraints, and Target Functions of the Three Major Systems

Image source: VCBeat

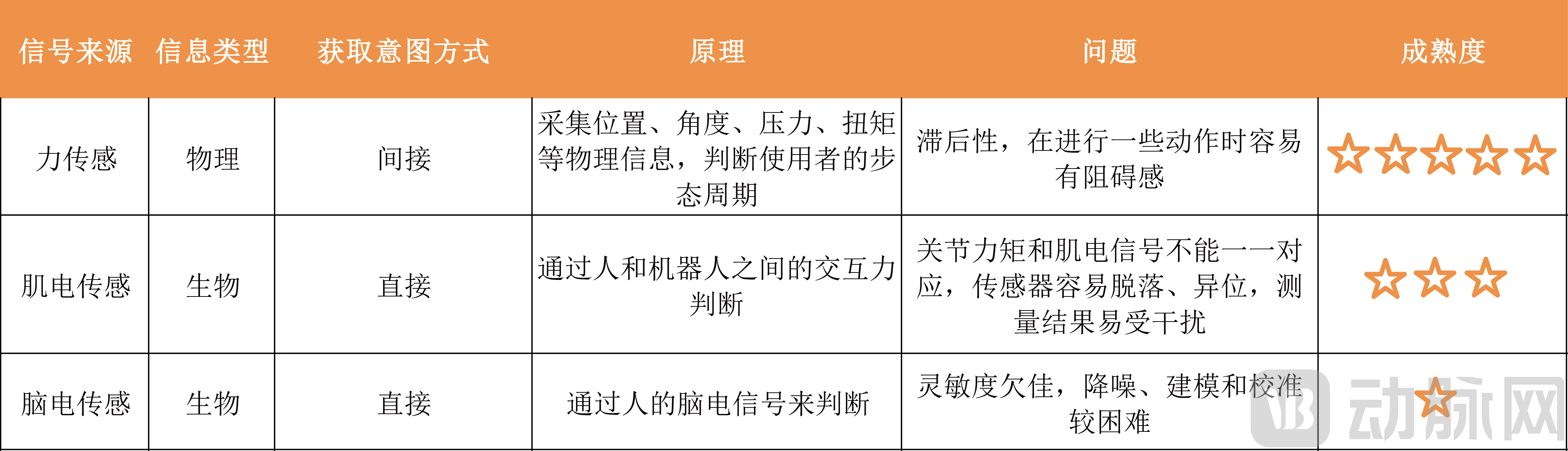

Sensing systems perceive patient and environmental information, primarily categorized into force sensing, electromyography (EMG) sensing, and electroencephalography (EEG) sensing. Currently, force sensing is the most widely applied and mature technology. While EMG and EEG sensing enable enhanced interaction, they face challenges related to signal recognition instability.

Comparison of Force, Electromyography (EMG), and Electroencephalography (EEG) Sensing

Image source: VCBeat

The control system serves as the central hub of rehabilitation robots. Taking lower-limb rehabilitation robots as an example, the control system analyzes data fed back by the sensing system to plan gait patterns and implements closed-loop control over the drive system. This process involves a series of software modules, including sensor fusion algorithms and control algorithms.

The drive system executes specific tasks transmitted by the control system. Located at the terminal end of machine operation, the drive system is responsible for actuating mechanical structures to carry out these tasks. Based on different driving mechanisms, it is primarily categorized into three types: electric motor drive, pneumatic drive, and hydraulic drive. Currently, electric motor drive is the most widely adopted.

In contrast, motor-driven rigid exoskeleton robots can bear heavy loads but are less comfortable to wear, whereas pneumatically driven soft exoskeleton robots are lighter and more comfortable but have limited load-bearing capacity. Therefore, rigid exoskeleton robots are currently mainly applied to the lower and upper limbs, while soft exoskeletons are primarily used for the hands.

Core components are no longer a barrier, as domestic substitution has been achieved. Whether driven by motors or pneumatic systems, the core components of current rehabilitation robots are primarily servo motors and reducers. These two components are no longer considered barriers or "choke points."

Compared with imported components, although most domestically produced components differ slightly from imported ones in terms of noise, lifespan, and weight, they can fully achieve the required functions and offer significant cost advantages, requiring only short-term validation. Currently, domestic substitution has been achieved for core components, and an increasing number of enterprises are choosing to collaborate with leading domestic component suppliers.

Meanwhile, Chinese companies have already achieved mass production of core components and successfully expanded into overseas markets. For instance, in the modular system of motors and reducers, Chengtian Technology’s motors feature high energy density, while its reducers can be integrated into a compact form factor and sustain three times the rated overload. Through co-design with torque sensors and drivers, the powertrain achieves optimal performance at a significantly reduced cost. The company has already realized mass production and exported its products to 34 countries and regions.

Mirror therapy, grounded in the theories of neuroplasticity and the mirror neuron system, has demonstrated significant therapeutic efficacy. It is currently employed in the treatment of conditions such as phantom limb pain, complex regional pain syndrome, stroke, peripheral nerve injury, hemiplegic cerebral palsy, and unilateral neglect.

Novel mirror therapy enables coordination between the unaffected and affected sides. Taking the upper limbs as an example, this novel approach utilizes sensors to acquire real-time motion data from the patient’s unaffected side. An exoskeletal robotic hand then assists the movement of the affected arm based on this data, thereby achieving mirrored tracking of the affected side following the unaffected side. This constitutes bilateral synchronized mirror movement training for both the affected and unaffected limbs.

Mirror therapy based on task-oriented training yields significantly greater therapeutic efficacy than mirror therapy alone. Cognitive dual-task training is more challenging than single-task training; it enhances the activation of executive cortical regions, accelerates synaptic signal transmission among brain neurons, and thereby significantly improves patients’ attention and executive function.

For example, the Wisebot 3D Upper Limb Mirror Rehabilitation Robot developed by Huaquejing Medical® During training sessions, the X5 records parameters such as duration, movement speed, and intensity. Combined with dual-task-oriented scenario-based training programs that incorporate elements of fun, challenge, and motivation, it significantly enhances patients' active engagement and the efficacy of mirror therapy.

Training systems that integrate rehabilitation robotics with virtual reality technology can enhance rehabilitation outcomes. According to the theory of neuroplasticity, patients’ active participation in rehabilitation training leads to better outcomes; therefore, improving adherence is key. Virtual reality technology enhances the enjoyment of the training process for patients. It enables rehabilitation therapists to design various scenarios and games tailored to different stages of rehabilitation, making patients’ rehabilitation exercises more engaging.

As of March 8, 2023, our incomplete statistics on approved rehabilitation robots and related products are as follows:

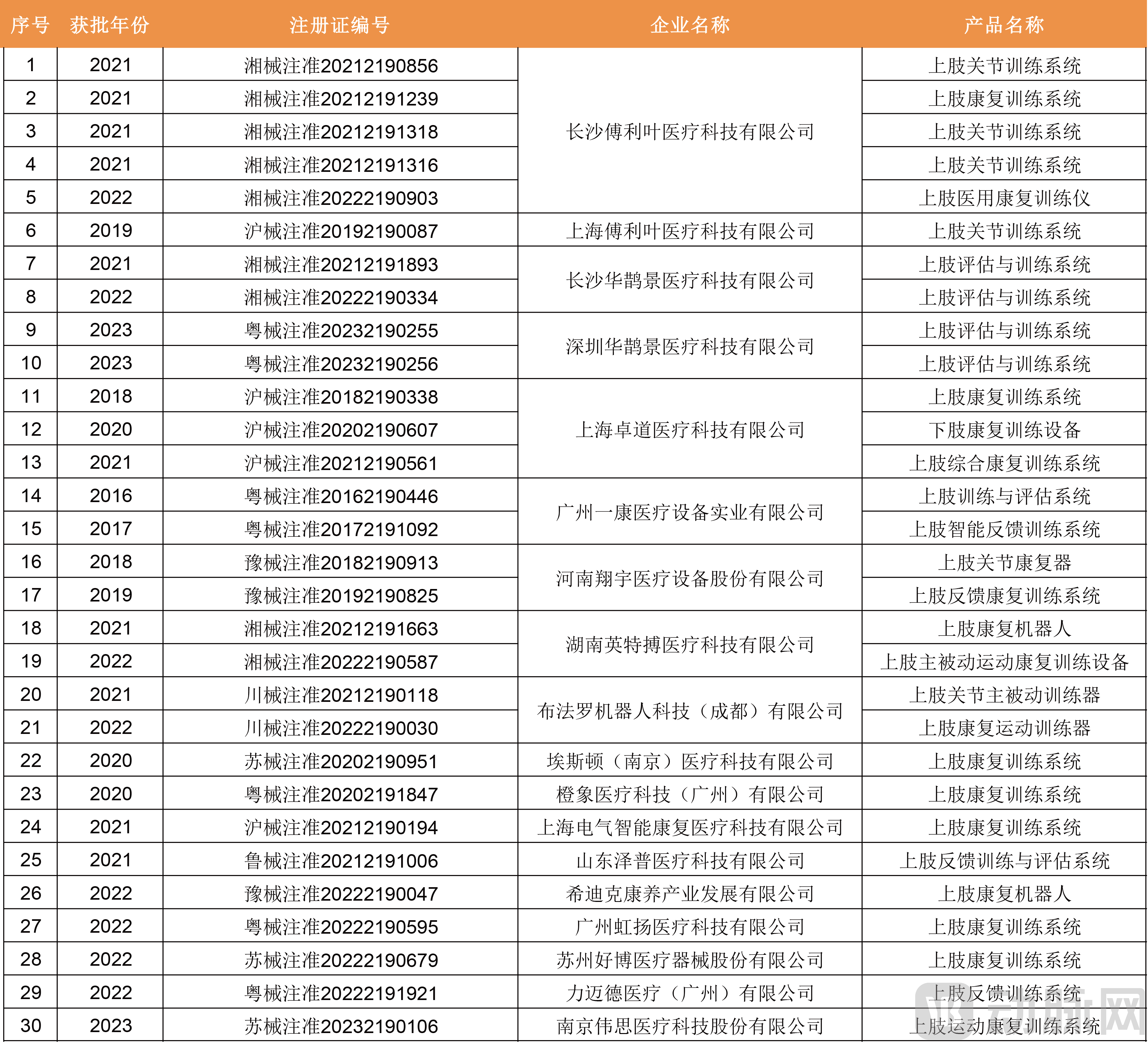

Among them, the table below shows the approval status of upper limb rehabilitation robots and related products. In terms of product functionality, some are designed for rehabilitation training, while others integrate training with assessment. Additionally, active and passive modes have been added to the training modalities.

The number of approved products peaked in 2021 at 10, accounting for 33.3%; there were 8 in 2022, and notably, 3 products have already been approved in 2023.

Overview of Approved Upper Limb Rehabilitation Robots and Related Products

Image source: NMPA, produced by VCBeat

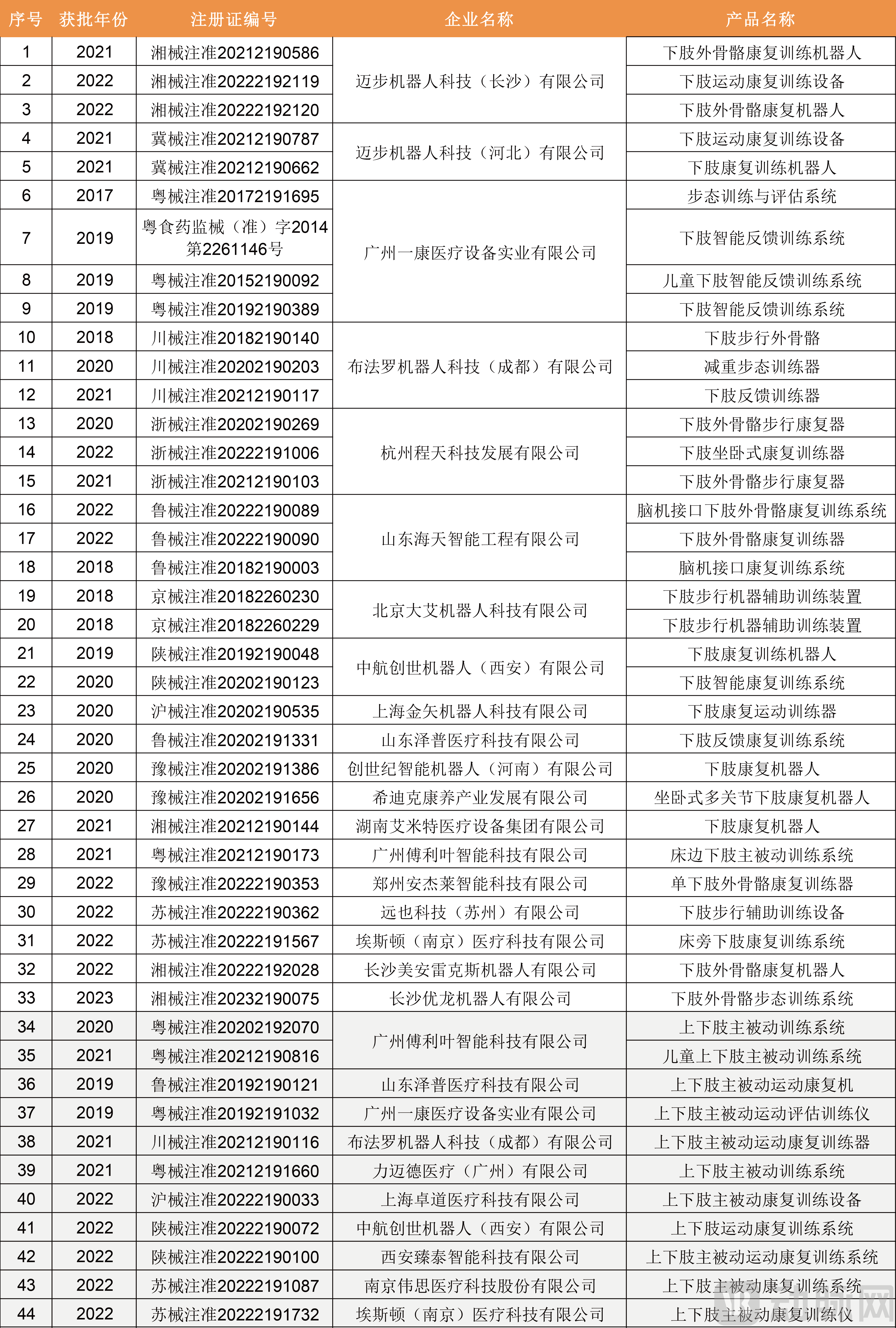

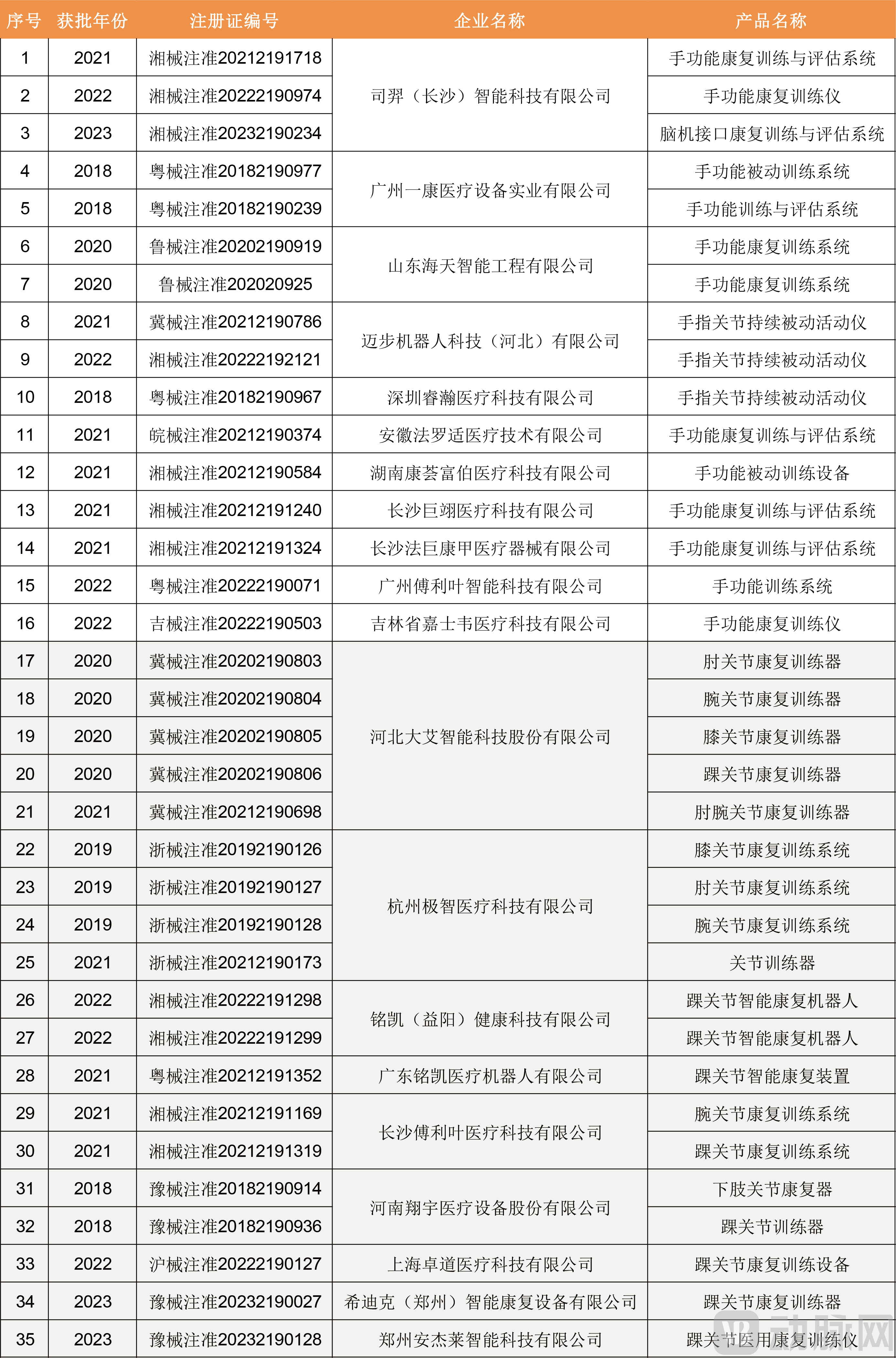

Lower-limb rehabilitation robots and related products have received the most approvals. The table below lists a total of 33 lower-limb rehabilitation robots and related products, with the last 11 products designed for both upper and lower limbs. Among the approved lower-limb products, there are pediatric-sized versions, and in terms of structure, both bilateral and unilateral lower-limb configurations are available.

Meanwhile, application scenarios include bedside lower-limb and seated/reclined multi-joint lower-limb systems, while technologies such as brain-computer interfaces are being incorporated, resulting in an increasingly diverse product portfolio.

Review of Approved Lower-Limb and Upper-and-Lower-Limb Rehabilitation Robots and Related Products

Image source: NMPA, produced by VCBeat.

The rehabilitation robots and related products approved for the hand and joints are listed in the table below. In comparison, the fewest products have been approved for the hand, largely due to the high degree of mobility of the hand, which poses significant challenges in product design and technology. Regarding joint-related approvals, ankle joint devices account for the largest share of single-product approvals at 47.3%, and there are also rehabilitative devices targeting the entire lower limb joints.

Review of Approved Hand and Joint Rehabilitation Robots and Related Products

Image source: NMPA; produced by VCBeat.

Commercialization: Product Evolution, Diversified Models, and Hospital-Enterprise Collaboration

In recent years, rehabilitation robots have become increasingly diversified in terms of products, application scenarios, and business models. Most domestic companies in China have followed a development trajectory from “single-product” to “small but comprehensive,” and finally to “large and comprehensive.” The path toward commercialization has been arduous yet marked by continuous innovation. Technologies, products, and business models are being continually validated in this increasingly competitive sector. With few valuable international benchmarks for commercialization, the market remains full of opportunities.

The external environment in China is improving, with factors such as policy support, hospitals’ growing emphasis on rehabilitation, and innovations in payment models accelerating the commercialization process.

In recent years, the development of rehabilitation robots in China has undergone a qualitative transformation. Both rehabilitation and assistive devices have become increasingly intelligent and comfortable, evolving from imitation to innovation, and ultimately to independent innovation. Products now exhibit diversified characteristics, pursuing enhanced comfort while expanding their applicability across body parts, functions, and training modes. Meanwhile, application scenarios are being continuously explored and gradually penetrated.

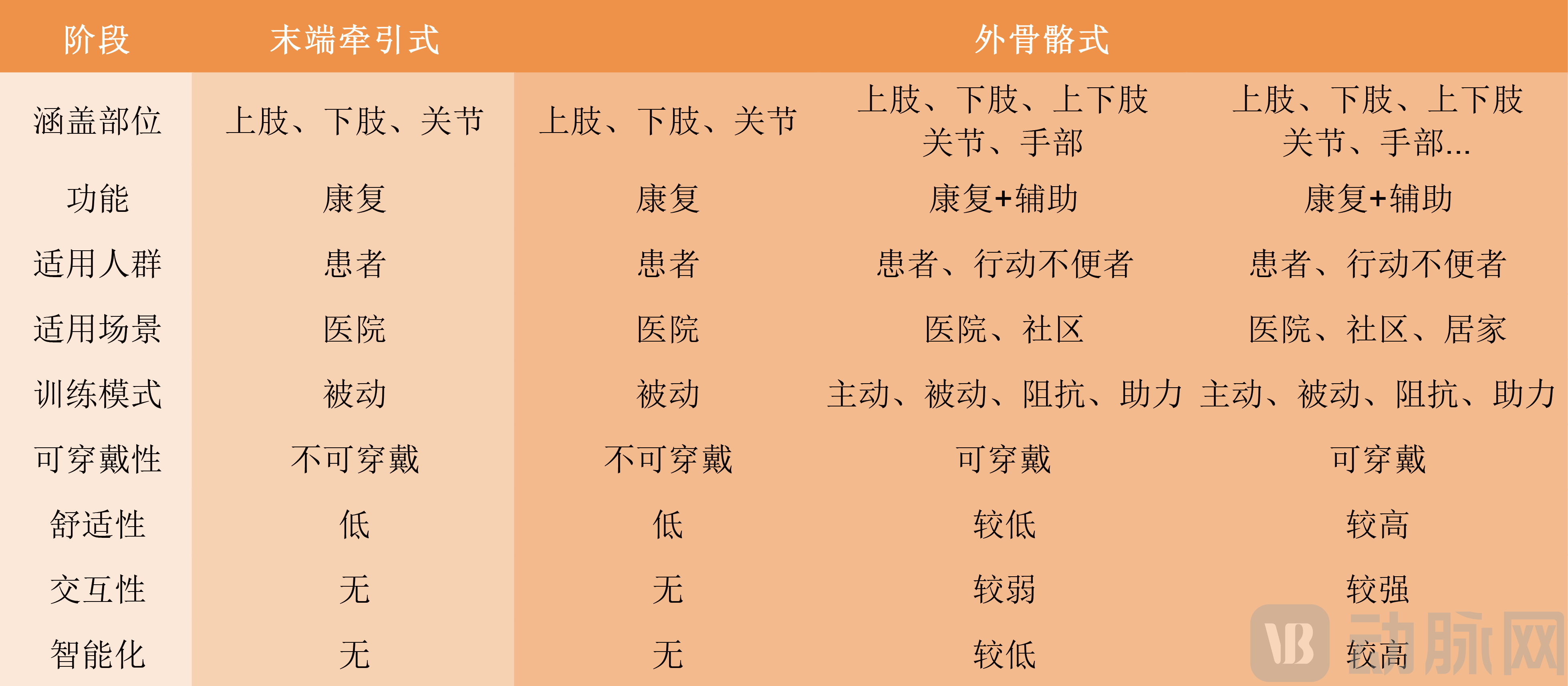

Overall, rehabilitation robots have evolved from end-effector traction-based systems to exoskeleton-based systems, with continuous improvements in product completeness, human-centered design, and intelligence. Currently, the industry is in the second phase of exoskeleton development, covering body parts including the upper limbs, lower limbs, both upper and lower limbs, joints, and hands. These devices offer rehabilitative and assistive functions with diverse training modes. However, wearable devices still suffer from insufficient comfort, as well as low levels of interactivity and intelligence.

In the future, product evolution will primarily focus on comfort and intelligence, marking the third stage, as detailed below:

Characteristics of the Development of Rehabilitation Robotics Products

Image source: VCBeat

Throughout the evolution of rehabilitation robotics, numerous innovative products have emerged. By leveraging innovative theories or cutting-edge technologies and addressing critical clinical needs, these products enhance both the efficiency and outcomes of patient rehabilitation.

For example, AngelAlign Technology's LiteStepper®Single-Leg Hemiplegia Rehabilitation Robot and ExoMax®Bilateral Ankle Rehabilitation Training Robot Based on Brain PlasticityThe Closed Loop of (Brain Plasticity)Clinical Theory of Neurorehabilitation: Providing Patients with Full-Cycle, Proactive, Efficient, Personalized, and Exercise-Induced "Central-Peripheral-Central" Closed-Loop Neurorehabilitation.

For another example, Siyi Intelligence has launched a hand function rehabilitation robot based on brain-computer interface (BCI) technology. Its EEG cap acquires and records electroencephalogram (EEG) signals in real time, decodes motor intent through intelligent algorithms, and converts it into motion commands to assist movement of the affected hand, thereby enabling mind-controlled operation and achieving a bidirectional closed-loop neural stimulation for “sensing-control.”

Meanwhile, cutting-edge products are emerging for home-based scenarios. Compared with hospital settings, home environments feature more diverse activity spaces and a wider range of motion, thereby demanding higher levels of safety and technological integration. In addition, the need to address personalized requirements across different population groups is greater, and consumers place a stronger emphasis on cost-effectiveness, which places higher demands on companies’ soft capabilities.

Certainly, in the face of this imaginative market, domestic companies are actively positioning themselves and launching innovative solutions.

For instance, Bangbang Robotics’ intelligent assistive mobile robots enable individuals with mobility impairments to achieve independent living at home, while its assistive travel robots help those with limited mobility travel safely and stably, fulfilling the expectations of people with mobility challenges for “warm high-tech” solutions that integrate intelligent services, proactive safety protection, and multi-environment adaptability.

Overall, domestic enterprises, whether in rehabilitation or assistive devices, generally follow a development trajectory from “single product” to “small but comprehensive” and then to “large and comprehensive.” In this context, achieving vertical or horizontal scalability based on single products is key.

On one hand, hospital rehabilitation departments often adopt bundled procurement strategies, favoring enterprises that can provide comprehensive solutions for rehabilitation robots covering both upper and lower limbs. On the other hand, some Grade 3A hospitals purchase individual units, where products with superior performance and robust clinical data hold a competitive advantage.,On the other hand, consumer-facing (B2C) products must cater to diverse needs and undergo rapid iteration.

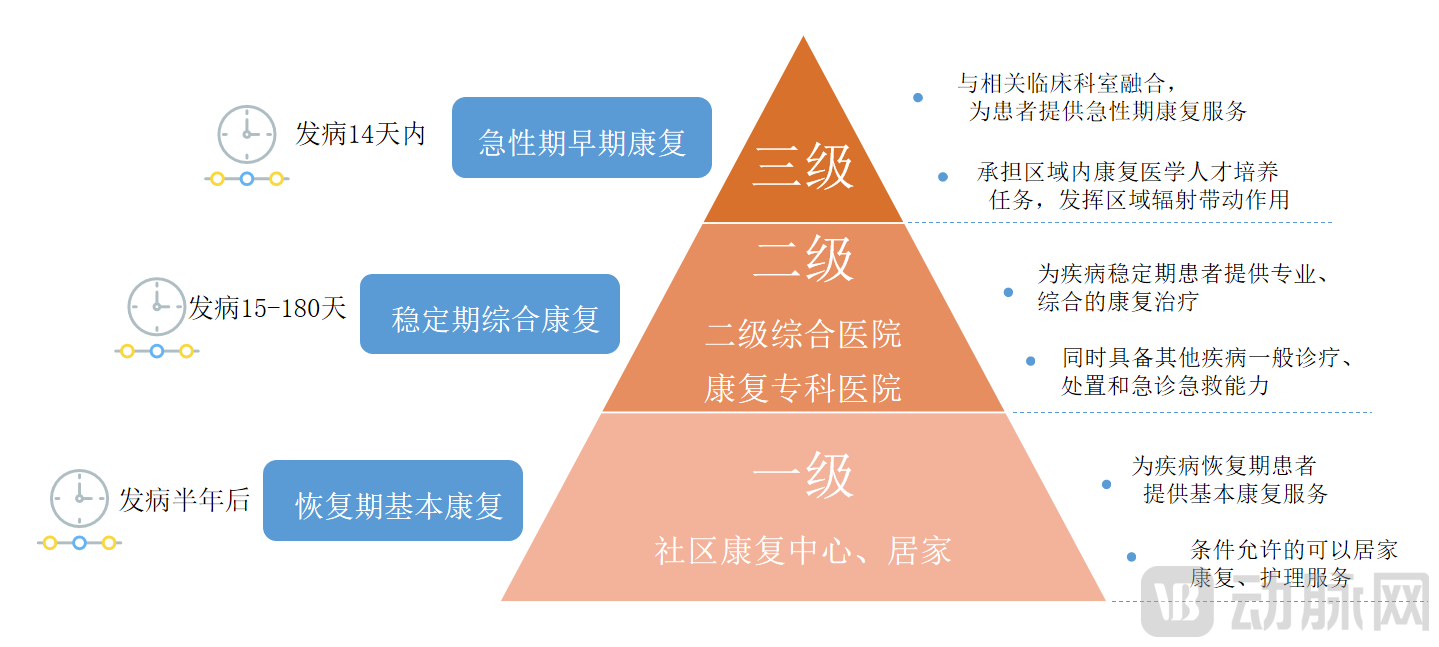

The three-tier rehabilitation medical service system is a widely recognized model internationally. The diagram below illustrates the three-level diagnosis and treatment system aligned with rehabilitation stages:

Integrating the Three-Tier Diagnosis and Treatment System into the Rehabilitation Phase

Image source: VCBeat

From a product perspective, factors such as functionality, target population, and resources across various scenarios influence its business model. By integrating rehabilitation stages with key application scenarios, we have summarized the prevailing mainstream business models as follows:

Core Product Requirements, Key Considerations, and Mainstream Business Models Across Various Scenarios

Image source: VCBeat

Overall, public Grade A tertiary hospitals prioritize product performance and clinical data. Additionally, physicians have needs for scientific research projects; therefore, companies with a strong research background hold a relative advantage when product differentiation is not significant. Meanwhile, enterprises must provide training and other support to hospitals during both pre-sales and post-sales phases, excelling in service and academic marketing to lay the groundwork for comprehensive solution offerings in the future.

Private rehabilitation hospitals place greater emphasis on costs and return on investment (ROI), making leasing and revenue-sharing models more popular for high-end rehabilitation robots. Under the revenue-sharing model, companies provide rehabilitation robots to private hospitals free of charge and share revenues based on utilization. In contrast, private rehabilitation hospitals have shorter decision-making chains.

For community- and home-based settings, which predominantly utilize assistive products, the diversity of scenarios and consumers’ personalized needs drive high demands for product iteration. To achieve “consumer-grade” rehabilitation robots, key factors—beyond ensuring safety—include product comfort, aesthetics, pricing, and after-sales service.

Domestic practice has shown that early rehabilitation yields better outcomes. Research results from Jinjiang Hospital in Fujian Province indicate that the overall effective rate for neurological function recovery was 71.8% among stroke patients who began rehabilitation within two weeks of onset, whereas it was only 29.2% among those who started rehabilitation more than two weeks after onset.

Domestic policies have been released, with growing emphasis placed on the rate of early rehabilitation intervention. In December 2022, the “Quality Control Indicators for Rehabilitation Medicine (2022 Edition)” was issued and incorporated into the “Accreditation Standards for Tertiary Hospitals (2022 Edition),” making the early rehabilitation intervention rate a key performance indicator for tertiary hospitals.

On February 28, 2023, the “2023 National Medical Quality and Safety Improvement Goals” were released, outlining four core strategies to increase the rate of early rehabilitation intervention. These strategies are: establishing multidisciplinary teams, developing intervention protocols and standardized diagnosis and treatment pathways, building an information management system for rehabilitation, and defining quality control metrics for inclusion in departmental performance evaluations. The key challenge ahead lies in the practical implementation and standardization of this policy.

For hospitals, on the one hand, greater emphasis may be placed on the allocation of rehabilitation resources, such as integrating resources between the Department of Rehabilitation and closely related departments like Orthopedics—for instance, assigning dedicated physicians to manage hyperacute postoperative rehabilitation. On the other hand, hospital performance evaluations may be incorporated into individual physician assessments.

For physicians, it means that clinicians need to be moreAdditionally, considering patients' future rehabilitation outcomes may impact the performance evaluations of both individual healthcare providers and their departments. For enterprises, there is a need to develop a deeper understanding of rehabilitation and to manufacture products that better align with clinical needs.

Traditional rehabilitation assessments primarily rely on rating scales, with therapists conducting one-on-one manual evaluations of patients. During assessment, patients often fail to perform movements to the required standard and exhibit sluggish motor responses, which is time-consuming for clinicians. Furthermore, due to the subjectivity and bias inherent in manual evaluation, assessment results vary between different evaluators.

Currently, rehabilitation robots can generate visualized reports from all patient-generated data, enabling therapists to promptly assess rehabilitation outcomes, such as improvements in range of motion. Some rehabilitation robots have achieved integration of assessment and training, significantly enhancing therapists' work efficiency.

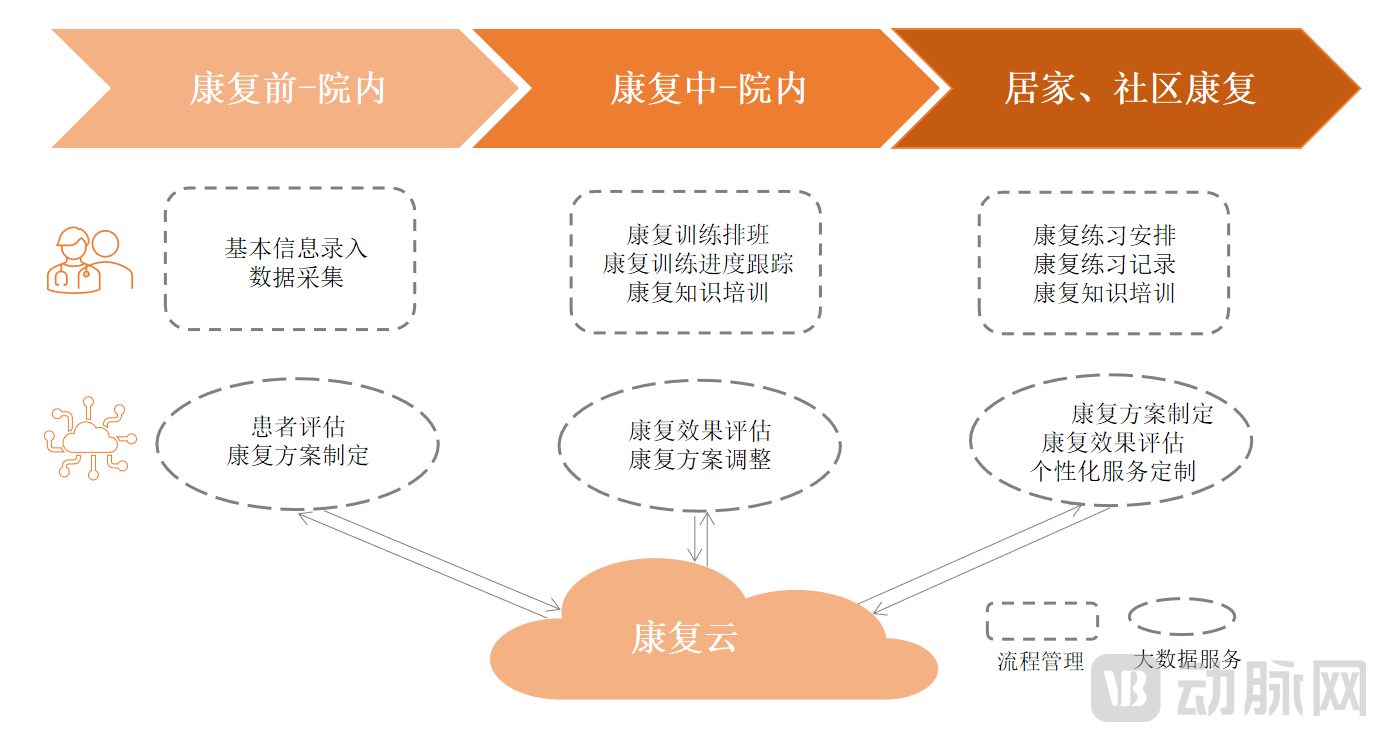

For enterprises, digitalization empowers end-to-end management of patient rehabilitation. Process management during the rehabilitation phase, data analysis and protocol formulation throughout rehabilitation, and remote home-based rehabilitation are all built upon a digital foundation. Here, process management encompasses patient administration tasks such as managing patients’ basic information and scheduling rehabilitation sessions.

Digitalization has played a significant role in pre-rehabilitation, during rehabilitation, and home-based rehabilitation, as detailed below:

Digital Empowerment for the Full Rehabilitation Cycle

Image source: VCBeat

Overall, the application of digitalization in the field of rehabilitation is still in its early stages. Although rehabilitation robots are attempting to incorporate digital technologies, the insufficient digital capabilities of other traditional equipment used in conjunction with them result in a relatively low level of overall digitalization, which depends on the comprehensive digital infrastructure development within the department.

Expanding Care Beyond the Hospital: Clinical Practice and Rehabilitation Move Toward Integration

Product innovation is being strengthened, with indications and functionalities set to expand. Currently, innovation in rehabilitation robotics is continuous, exemplified by single-lower-limb rehabilitation robots for hemiplegia and soft robotic devices for hand therapy. With accumulated technological expertise, the field of rehabilitation robotics is poised for an explosive period of innovation.

In addition, rehabilitation robots will expand in terms of indications and functionalities. Regarding indications, current rehabilitation robots primarily target the upper limbs, lower limbs, joints, and hands; future applications may extend to conditions such as spinal disorders and osteoporosis. Functionally, there will be expansion and integration, such as transitioning from rehabilitation to assistance, broadening the target population from patients requiring rehabilitative therapy to individuals with mobility impairments, and achieving integrated assessment and training capabilities in product design.

Technically, the direction lies in enhancing perception, creativity, execution, and comfort. Regarding the three major systems, the sensing system requires novel materials to improve perceptual capabilities. By integrating lighter and more comfortable materials with the human body and rationally arranging various modules, products can be made more lightweight; examples include non-contact visual sensors and non-invasive flexible epidermal sensors.

The control system needs to explore intent recognition technologies to enhance creativity, such as judging the user's movement intent through inertial measurements, interaction metrics, electroencephalography (EEG), and electromyography (EMG). By leveraging artificial intelligence, the system can identify adaptive patterns tailored to patients' personalized movement styles through data integration and machine learning.

The drive system requires high-power output actuators with fast response capabilities to enhance actuation performance. Currently, motor-driven systems are predominant, necessitating the exploration of lightweight, high-speed, and flexible actuators. Meanwhile, improving comfort is a key focus for next-generation rehabilitation robots, particularly those targeting consumer markets.

Let us imagine a future where rehabilitation robots possess warmth. During the prolonged rehabilitation journey, patients require encouragement. If rehabilitation robots can provide emotional companionship—such as encouraging patients and boosting their confidence—in addition to their core rehabilitative training functions, they will truly assume the role of professional rehabilitation therapists.

In terms of application scenarios, the focus is expanding from hospitals to communities and home settings. Rehabilitation is a prolonged process. Currently, rehabilitation robots are primarily deployed in hospital settings. After brief acute-phase and recovery-phase rehabilitation therapy within the hospital, most patients are discharged with varying degrees of sequelae, yet they still have needs for ongoing rehabilitation and assistance. Meanwhile, driven by the “9073” elderly care model, policy incentives, and increased capital investment, domestic companies are also beginning to establish their presence in community and home-based sectors, offering integrated rehabilitation therapy solutions.

Currently, capital is favoring the consumer-facing (C-end) market, which is rich with imaginative potential. In the future, as public awareness of rehabilitation strengthens, numerous products will be introduced for home use, making home and community rehabilitation centers a key battleground for large, comprehensive enterprises. For home-based scenarios, product diversification is inevitable; while safety remains fundamental, aesthetics, portability, and comfort will become primary focuses.

Digitalization Will Empower the Entire Rehabilitation Cycle. Currently, the application of digitalization in rehabilitation robotics primarily focuses on process management throughout the rehabilitation journey and data analysis during rehabilitation. While digital assessment prior to rehabilitation has been technically achieved, the current volume of accumulated data remains insufficient, and unified digital standards and clinical pathways have yet to be established. Furthermore, the low level of digitalization in related rehabilitation equipment hinders comprehensive assessments.

In the future, as data accumulates, the value of digitalization will become increasingly prominent. Beyond intelligent rehabilitation assessment, it will also play a significant role in formulating personalized treatment plans and enabling remote rehabilitation.

Early rehabilitation demonstrates superior health economic benefits. Early intervention in rehabilitation can effectively prevent the occurrence of disuse syndrome and misuse syndrome; initiating correct training during the early stages of illness can completely or partially prevent these abnormal manifestations. Previously, rehabilitation therapy was largely regarded as a follow-up measure after the completion of most clinical treatments, or positioned merely as one of the optional adjunctive methods during the acute phase of disease. This disconnect between rehabilitation and clinical treatment has significantly compromised therapeutic efficacy.

The integration of clinical care and rehabilitation enables the simultaneous delivery of clinical treatment and rehabilitative therapy, facilitating concurrent recovery from disease and restoration of function. This approach shortens treatment duration and enhances therapeutic outcomes, benefiting not only patients but also promoting the advancement of institutional medical standards.

Extending rehabilitation to the early stage is inevitable, and bedside rehabilitation presents an opportunity. With the release of the "Medical Quality Control Indicators for Rehabilitation Medicine (2022 Edition)" and its inclusion in the "Accreditation Standards for Tertiary Hospitals (2022 Edition)," the rate of early rehabilitation intervention has become a key performance indicator for tertiary hospitals. This will garner greater attention from hospitals and physicians, making collaboration between clinical and rehabilitation departments increasingly inevitable.

In February 2023, the “2023 National Goals for Improving Medical Quality and Safety” outlined core strategies to increase the rate of early rehabilitation intervention.In the future, key priorities will include how this policy is specifically implemented, how hospital performance evaluations are integrated with those of departments and physicians, how clinical and rehabilitation services will be coordinated, and how personnel and equipment will be allocated. For instance, will the rehabilitation department operate as a mobile unit, and how will it establish collaborative mechanisms with closely related specialties such as orthopedics?

In addition, products for early rehabilitation, such as bedside rehabilitation robots, present a significant opportunity. Currently, the adoption rate of bedside rehabilitation robots in tertiary hospitals is lower than that of upper- and lower-limb rehabilitation devices, and there are no adequate solutions addressing the differentiated early rehabilitation needs across various clinical departments. In the future, tailored early rehabilitation solutions must be developed for specific departments, including neurology, orthopedics, and the intensive care unit (ICU).

Chapter 1Overview: Favorable Policies Continue to Drive a Recovery in Financing

1.1 Policy: A Three-Pronged Approach Leveraging Technology, Resources, and Business Models

1.2 Market: CAGR of 57.5%, with faster growth in China

1.3 Financing: Industry Rebound, 2023 Financing Hits Record High

Chapter 2 Technology: Integration of Hardware and Software, Human-Computer Interaction

2.1 Core: Sensing Systems, Control Systems, and Drive Systems Are Becoming Intelligent

2.2 Applications: Novel Mirror Therapy Achieves Affected-Healthy Limb Coordination; VR Enhances Rehabilitation Engagement

2.3 Approvals: Expanding Anatomical Sites and Diversified Functional Capabilities

Chapter 3 Commercialization: Product Evolution, Diversified Models, and Hospital-Enterprise Collaboration

3.1 Current Status: Product Evolution, Enterprises Moving Toward Large-Scale and Comprehensive Operations

3.2 Model: Integration of Tertiary Healthcare Resources with Scenario-Specific Characteristics

3.3 Hospital Side: Early Rehabilitation Gains Attention, FRG Payment Model in Exploratory Phase

3.4 Enterprises: Digital Empowerment Across the Entire Rehabilitation Cycle

Chapter 4 Trends: Expansion of Scenarios Beyond Hospitals, and the Trend Toward Integration of Clinical Care and Rehabilitation

4.1 Technology: Enhancing Comfort, Advancing Toward Intelligence

4.2 Scenario: From Inside to Outside the Hospital, Digitalization Will Empower More

4.3 Hospital Side: Integration of Clinical Care and Rehabilitation, with Bedside Rehabilitation as an Opportunity

Chapter 5 Corporate Case Studies

5.1 Cheng Tian Technology – Leading Exoskeleton Robotics

5.2 AngelAI Technology – Intelligent Robots Focused on Brain Science Applications

5.3 Bangbang Robotics—Providing a New Smart Mobility Solution

5.4 Huaquejing Medical—Focused on Holistic Solutions for Smart Rehabilitation Medicine

5.5 Siyi Intelligence—Building an Integrated Smart Rehabilitation Solution

Please scan the QR code below to get the full report for free.

Special Acknowledgments (in order of research interviews):

Mr. Cao Xin, Investment Director at Shiyue Capital; Dr. Wang Tian, Founder of Chengtian Technology; Dr. Li Luya, Founder of Anjielai Technology; Mr. Wang Daoyu, Founder and CEO of Zhuodao Medical; Ms. Zhu Qi, CEO of Jiahu Medical; Mr. Li Jianguo, Founder and CEO of Bangbang Robotics; Dr. Wu Jianhuang, Founder of Huaquejing Medical; and Mr. Yin Ganggang, Founder and General Manager of Siyi Intelligence.