Photonic Aesthetic Medicine Enters the Golden Era of Domestic Substitution

Fumeilei Medical

R&D Developer of Medical Aesthetic Devices

The curtain is rising on the medical aesthetics industry.

In recent years, driven by substantial demand from consumers seeking aesthetic enhancements, China’s medical aesthetics industry has been thriving. According to a 2021 survey by the So-Young Data Yanjiuyuan, over 80% of respondents expressed a relatively accepting attitude toward medical aesthetic procedures,The growing openness of public attitudes has become one of the key drivers behind the growth in the number of medical aesthetics consumers.

How Rapid Is the Growth? Data from So-Young indicates that from 2016 to 2022, the year-on-year growth rate of the number of users in China’s medical aesthetics market remained above 20%, with the growth rate exceeding 80% in 2018, highlighting the market’s substantial size.

On the other hand, the development of the medical aesthetics industry has been widely criticized, with illegal “black market” medical aesthetic practices emerging endlessly. Behind this,Beyond issues such as industry self-regulation and talent shortages, the core challenge lies in the de facto “lack of autonomy” within China’s medical aesthetics industry.

How should this be understood? Specifically, China lacks domestic manufacturing capabilities for many medical aesthetic devices and consumables. This situation forces manufacturers to either opt for "high-priced, compliant imported equipment" or enables unscrupulous vendors to use "counterfeit, low-cost, non-compliant devices." Furthermore, given consumers’ current limited understanding of the industry, they are highly susceptible to deception.

To address this dilemma, one effective solution is to promote the rise of reputable domestic manufacturers of medical aesthetic devices and consumables in China, enabling Chinese consumers to confidently enjoy “safe and cost-effective” medical aesthetic services.

And this inflection point is now arriving.

This article is an excerpt from the White Paper on Energy-Based Devices in Medical Aesthetics. To learn about the industry landscape, development logic, and potential opportunities for energy-based devices in medical aesthetics, please scan the QR code to contact our assistant and request the full report.

For a long time, China’s upstream medical aesthetics equipment sector has been dominated by imported brands, particularly in the high-end segment.

Taking photoelectric medical aesthetics as an example, imported devices account for as high as 80% of the market share. The underlying reason is that the photoelectric medical aesthetic device industry is a technology-intensive sector characterized by multidisciplinary integration, with exceptionally high technical barriers.

Furthermore, in the field of photoelectric medical aesthetics, particularly with regard to high-end equipment, China still faces a shortage of relevant talent, and its core technologies remain in a catch-up phase.

“Two ‘Major Hurdles’ Facing the R&D of High-End Photoelectric Medical Aesthetic Devices in China.” a senior investor in consumer healthcare told VCBeat.

· First, China remains relatively weak in fundamental research; for instance, the specific mechanisms and effects of various energy-based technologies in aesthetic dermatology require further academic investigation.

· Second, in terms of application development, the industry requires more interdisciplinary talent, as optoelectronic medical aesthetics involves the intersection of multiple disciplines, including physics, engineering, and medicine. An excellent optoelectronic device must not only address technical issues such as lasers and wavelengths but also resolve challenges related to product design and clinical efficacy.

This presents both challenges and opportunities. In China, there is a large number of small enterprises in the photoelectric medical aesthetics sector. Their products suffer from serious homogenization and low technological value-added, resulting in low market concentration. Furthermore, these products generally rank low in terms of safety and efficacy.

Amid the vast market substitution opportunities, an increasing number of enterprises, capital investors, and R&D and management talents are entering the field of photoelectric medical aesthetic devices.

An increasing number of players are entering the field of photoelectric medical aesthetics, gradually exploring two pathways: one is mergers and acquisitions, and the other is independent research and development.

Most of the companies implementing M&A strategies are leading enterprises in the pharmaceutical sector, with their expansion into medical aesthetics primarily aimed at identifying second and third growth curves for their businesses.

Taking Huadong Medicine as an example, as a pharmaceutical R&D enterprise, it acquired a 26.6% equity stake in the U.S.-based company R2 in 2019, thereby securing exclusive Asia-Pacific distribution rights for R2’s aesthetic light-based devices F1 (for cryo-pigment removal) and F2 (for full-body skin whitening), which marked its formal entry into the energy-based medical aesthetics sector. Subsequently, in February 2021, Huadong Medicine acquired 100% of High Tech’s equity, gaining control over its cryolipolysis products (Cooltech, Cooltech Define, and Crystile) and laser hair removal systems (Elysion and Primelase).

In February 2022, Huadong Medicine announced that its wholly-owned subsidiary, Sinclair, would acquire 100% of the equity of Viora, an Israeli energy-based medical aesthetics device company. Viora is an international medical aesthetics company specializing in non-invasive and minimally invasive energy-based devices, with products applied in areas such as anti-aging, body contouring, and facial shaping. Upon completion of this transaction, Huadong Medicine will have more than thirty products in the non-invasive and minimally invasive medical aesthetics field globally, with a product portfolio covering mainstream non-surgical medical aesthetics areas including facial fillers, thread lifts, skin management, body contouring, hair removal, and intimate rejuvenation.

Domestic enterprises pursuing independent R&D are also on the rise, continuously breaking through technical barriers, forging ahead with innovation, and highlighting their cost advantages.

For example, as a new entrant in the field of medical aesthetic optoelectronic devices, Fumeilei Medical was established in Suzhou in September 2021, dedicated to the research, development, and manufacturing of high-end optoelectronic equipment, with the ambition of becoming a global leader in medical aesthetic optoelectronic devices. The core founding team hails from Peking University and prestigious overseas universities, boasting many years of deep engagement in the medical aesthetic optoelectronics industry, along with robust technical expertise and profound industry insights. Notably, R&D personnel constitute two-thirds of the company’s workforce. It is reported that the company’s flagship product, the ForePico multi-wavelength picosecond laser therapeutic device, is poised to enter clinical trials.

▲ ForePico Product Image

Source: Fumeilei Medical Official Account

As the ultimate solution for pigmentary disorders, picosecond laser devices can be used to treat benign cutaneous pigmented lesions, remove tattoos, and achieve facial rejuvenation. Currently, only one domestically produced picosecond laser device has been approved for market launch in China, indicating substantial market potential. Meanwhile, high-cost imported products fail to meet the continuously growing domestic demand for medical aesthetic services.

In the foreseeable future, as mid-to-high-end domestic medical aesthetic optoelectronic devices are successively launched, Chinese-made equipment will rapidly capture market share through superior product quality and relative price competitiveness, thereby achieving import substitution.

Therefore, it is evident that driven by immense market potential, the increasing involvement of enterprises, capital, and talent will break down the technical barriers in photoelectric medical aesthetic devices, enabling domestically produced products to gain momentum and exert a significant impact on imported alternatives.

As the Golden Age of Domestic Substitution Arrives, What Should Chinese Innovative Enterprises Prioritize Besides Technology?

VCBeat believes that as the current medical aesthetics market trends toward a return to its core essence, product efficacy is becoming more important than conceptual marketing. It is evident that, in the short term, some manufacturers will still resort to malicious marketing or hype to package their products through conceptual branding, thereby capturing consumer attention and ultimately driving sales.

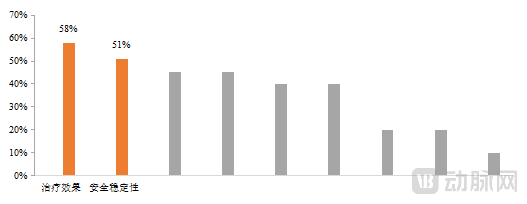

According to a survey conducted by Allergan Aesthetics among medical aesthetic institutions, the primary factors considered in product selection and service strategy formulation are “treatment efficacy” and “safety and stability.” As market education continues to deepen, consumers’ demands for medical aesthetic services are evolving from entry-level to more advanced offerings. If a treatment fails to deliver the advertised results, consumers will likely discontinue use after one or two sessions, causing significant harm to the product itself. Loss of consumer trust consequently shortens the product’s lifecycle. Hence, the current medical aesthetics market is characterized by a frequent turnover of preferences, with the typical lifecycle of aesthetic devices lasting approximately 2–3 years.

In the foreseeable future, the medical aesthetics market will inevitably return to its medical essence—namely, selecting appropriate treatments based on consumers’ needs. Phenomena such as conceptual hype and excessive marketing that mislead consumers will gradually diminish.

The future trend is clear: only high-quality enterprises with independent R&D capabilities that develop safe and effective products will be able to secure a stable and invincible position in market competition.

▲ Primary Considerations for Institutional Product Selection

Source: Allergan Aesthetics, compiled by VCBeat

Furthermore, domestic manufacturers must not only prioritize product quality assurance but also deliver comprehensive full-lifecycle services to gradually establish their brand advantage in the market.

Currently, given the high value of optoelectronic devices, most medical aesthetic institutions will carefully consider their procurement choices if after-sales service cannot be adequately guaranteed. To some extent, satisfaction with after-sales service carries significant weight in institutional procurement decisions and determines whether a company’s products can achieve strong sales among downstream medical aesthetic institutions.

For example, imported brands such as Lumenis and Cynosure, which were among the first to enter the Chinese market, offer free maintenance during the first year after equipment sale, requiring no additional expenditure from customers. However, beyond the first year, paid maintenance becomes necessary. On one hand, warranty services are particularly expensive; on the other hand, medical institutions must pay an upfront fee for on-site maintenance by after-sales service engineers. Another significant issue is that these imported manufacturers currently lack R&D and production departments in China. Consequently, once complex after-sales issues arise, the equipment must be shipped abroad for factory repair, resulting in exorbitant repair costs and excessively long waiting periods.

Therefore, the vast majority of small and medium-sized institutions currently opt for third-party maintenance services rather than original equipment manufacturer (OEM) after-sales support when their devices encounter issues. However, due to the uneven technical expertise and service capabilities among third-party providers, downstream institutions often experience subpar after-sales service quality.

Currently, in the Chinese market, Alma Lasers from Israel stands out for its relatively superior after-sales service. This service comprises two key components: first, training services, which have fostered strong collaborative relationships with medical aesthetic institutions through continuous and in-depth product training and communication; second, on-site engineering support and routine visits, ensuring that daily operational issues and maintenance needs are addressed promptly—essentially on call—thereby alleviating institutional concerns and achieving high customer satisfaction. Correspondingly, Alma Lasers’ high market share is largely attributable to its robust after-sales service, which has bolstered its market reputation.

Based on the development experience of other medical device manufacturers,The competitive advantage of high-quality domestic manufacturers must initially stem from superior pre-sales and after-sales services.As we can see, leading domestic medical equipment manufacturers such as Mindray and United Imaging, during their early development stages when their product competitiveness was not yet advantageous, facilitated sales adoption and strengthened brand recognition among healthcare institutions by providing services superior to those of imported brands. Similarly, in the rise of domestically produced aesthetic optoelectronic devices, delivering comprehensive lifecycle services, including both pre-sales and after-sales support, constitutes the core competitive advantage for Chinese manufacturers.

Next, the wave of rapid development in China’s domestically produced photoelectric medical aesthetics industry is bound to grow increasingly powerful.