Post-315 Exposure: Regulatory Crackdown on Injectable Aesthetics Drives Industry Standardization

Bloomage Biotech

Developer of bioactive substance products, producer of hyaluronic acid raw materials

At last night’s 3.15 Gala, irregularities in the medical aesthetics industry were once again exposed: cosmetic-grade products were used for medical aesthetic injections. This incident did not occur at some obscure clinic or beauty salon, but rather at a major exhibition.

Footage from the event showed that most participating companies at a major exhibition were manufacturers of aesthetic medical devices and cosmetics firms. Some exhibitors displayed injectable products for dermal filling, wrinkle reduction, weight loss, skin whitening, and hydration. These products, which should be regulated as Class III medical devices, were instead registered only as cosmetics. At numerous booths, staff members even administered injections to customers on-site.

Cosmetics company staff injecting “cosmetic-grade” products into consumers at an exhibition. Image source: screenshot from the 315 Gala

CCTV reporters discovered during their investigation that cosmetic injectables sold under the guise of cosmetics feature opaque pricing and yield exorbitant profits, drawing practitioners to them in droves.

On one hand, exhibitor staff stated that the price markup on product sales is “at least tenfold,” which clearly represents the profit margin for service providers. On the other hand, manufacturers of such cosmetics are also reaping market “dividends.” A representative from an exhibiting company noted that demand for cosmetic injectables has remained strong in recent years, with robust sales performance. As a result, the company is expanding its production capacity, increasing its operational footprint from three floors in its old factory to six floors in its new facility.

Historically, societal concern over irregularities in the medical aesthetics industry has focused primarily on the service end, including various beauty salons, medical aesthetic clinics, and even large plastic surgery hospitals. This time, however, the spotlight has shifted to the upstream sector, specifically the mid-to-upstream segments of injection-based medical aesthetics where chaotic practices are frequent. This development signals that the production end of the industry chain is poised for further purification, thereby promoting greater overall standardization within the medical aesthetics sector.

In fact, injectable medical aesthetics has already formed a huge market.

Injectable treatments have become a popular entry-level choice for many users due to their noticeable results, ease of administration, short recovery period, and relatively affordable price.

Meanwhile, injectable products are diverse in type and rich in efficacy, generally categorized into fillers, atrophy-inducing agents, and others. Fillers include injections such as collagen, hyaluronic acid, and regenerative materials, which can achieve a plump and three-dimensional effect on the skin. Atrophy-inducing agents are primarily represented by botulinum toxin, offering benefits such as wrinkle reduction, facial slimming, and body contouring. Consequently, these products can cater to a broad user base.

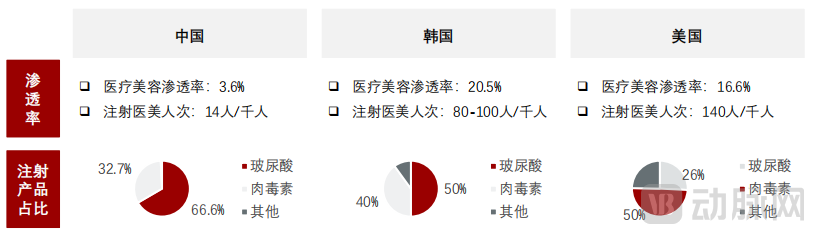

According to a report by LeadLeo Research Institute, China’s medical aesthetics industry is dominated by injectable treatments, which account for 57% of total consumption. However, compared with markets such as South Korea and the United States, the penetration rate of injectable medical aesthetics in China remains relatively low. In 2019, the number of injectable medical aesthetics procedures in China was only 14 per 1,000 people, significantly lower than that in other major countries. As the consumer base for medical aesthetics continues to expand, China’s injectable medical aesthetics sector holds substantial growth potential.

Comparison of Injectable Aesthetic Medicine Markets in Major Countries, Image Source: LeadLeo Research Institute

Meanwhile, in the existing market, China’s injectable medical aesthetics sector still holds substantial room for growth from its installed base, driven by rising penetration rates and repeat purchase frequencies among current users.

Bloomage Biotech, Imeik, and Haohai Biological Technology have long been established in the injectable medical aesthetics sector, with extensive portfolios of injectable products that have generated substantial revenue.

The latest annual report shows that in 2022, Imeik's revenue from both solution-based and gel-based injectable products increased. Specifically, revenue from solution-based injectable products reached RMB 1.293 billion, a year-on-year increase of 23.57%; revenue from gel-based injectable products amounted to RMB 638 million, representing a year-on-year growth of 65.61%.

As the penetration of injectable treatments among consumers expands, product sales volume is poised for further growth. According to estimates by Frost & Sullivan and Dongxing Securities, the market size of China’s injectable medical aesthetics sector is expected to reach RMB 125.5 billion by 2027.

Hyaluronic acid is one of the longest-standing “viral” products in the development of injectable medical aesthetics, widely recognized by consumers and potential consumers alike.

As of now, Haohai Biological Technology has developed its hyaluronic acid products to the fourth generation. Among them, the first-generation product, “Haiwei,” is the first monophasic cross-linked sodium hyaluronate gel for injection approved by China’s National Medical Products Administration (NMPA), primarily positioned as an entry-level hyaluronic acid for mass-market adoption. The second-generation product, “Jiaolan,” is targeted at the mid-to-high-end market, emphasizing its “dynamic filling” capability. The third-generation product, “Haimai,” features a linear, particle-free structure and is positioned as a high-end hyaluronic acid focused on “precise contouring.” In 2022, clinical trials for the fourth-generation organically cross-linked hyaluronic acid product were underway.

As a product nearly as renowned as hyaluronic acid, botulinum toxin has also attracted widespread strategic investment from industry participants.

CMS Pharmaceutical has entered into a licensing, collaboration, and distribution agreement with South Korea’s BMI for a 100U lyophilized powder injection of botulinum toxin type A. Meanwhile, Haohai Biological Technology has invested in Eirion to establish a product portfolio featuring “topical application + classic injection” botulinum toxin offerings.

In the startup sector, Junhemeng Biology completed a nearly RMB 100 million Series A+ financing round in January 2023. Its R&D pipeline is focused on frontier protein therapeutics in broad markets such as metabolism and medical aesthetics, with its lead product including recombinant botulinum toxin type A.

Currently, several botulinum toxin products, including Hengli, Botox, Dysport, and Letibot, have been approved in the Chinese domestic market. As more players enter the field, the industry is expected to become even more competitive.

Meanwhile, injectable medical aesthetics is entering the "regenerative era."

Regenerative materials are novel substances capable of stimulating the regeneration of human fibroblasts and collagen. Currently, mainstream regenerative materials in China’s medical aesthetics industry include poly-L-lactic acid (PLLA) and polycaprolactone (PCL). With advancements in production technologies, the application scenarios of regenerative materials have gradually expanded from the medical sector to the medical aesthetics sector, driving the diversification of injectable aesthetic products and the optimization of their efficacy.

Prior to this, PLLA-based “Youth Rejuvenation Injections” and PCL-based “Maiden Injections” had already been marketed and used for many years in the international medical aesthetics industry. According to survey reports released by the International Society of Aesthetic Plastic Surgery (ISAPS), among injectable medical aesthetic procedures from 2016 to 2020, PLLA dermal fillers experienced the fastest growth in treatment volume globally.

Since 2021, three domestically produced medical aesthetic products based on regenerative materials have been approved for market launch in China, including Sinocare’s Ellansé (Girl Needle), St. Bioma’s Avelan (Baby Face Needle), and Imeik’s Ru Bai Angel (Baby Face Needle).

As dermal fillers, regenerative materials deliver more natural and longer-lasting results than hyaluronic acid, propelling the field of medical aesthetics from the “filler era” into the “regenerative era” and meeting the urgent demands of aesthetic seekers.

The product portfolio formed from diverse materials has further enriched the efficacy of injectable treatments, contributing to the rapid growth of this market.

The vast market size, increasingly diverse product categories, and more refined product efficacies have enabled compliant enterprises to grow rapidly, while also alerting illicit manufacturers and merchants to “business opportunities.”

According to the regulations of the National Medical Products Administration (NMPA), injectable medical aesthetic products are regulated as Class III medical devices, including well-known treatments such as skin boosters. This means that a product must undergo a lengthy development cycle and significant financial investment from research and development initiation to market launch, and must pass clinical trials to verify its safety and efficacy. This is the primary distinction between products registered as “medical devices” and those registered as “cosmetics.”

For example, in 2022, Imeik’s R&D investment reached RMB 173 million, a year-on-year increase of 69.20%, accounting for 8.93% of its operating revenue. In the first half of 2022, Bloomage Biotech’s R&D investment amounted to RMB 179 million, representing 6.11% of its operating revenue; Haohai Biological Technology’s R&D investment was RMB 76.71 million, accounting for 7.93% of its operating revenue.

Continuously allocating a certain proportion of operating revenue to product research and development and expanding the product portfolio ensures that the company maintains a market-aligned product strategy. This is essential for sustaining corporate competitiveness within a compliant framework. From a macroeconomic perspective, healthy market competition should follow this same principle.

Clearly, using the guise of “cosmetic-grade” products to operate as “medical-device-grade” ones disrupts healthy market competition.

In fact, regulatory authorities have consistently attached great importance to the crackdown on non-compliant practices in injectable medical aesthetic procedures.

Consumer-Oriented: The National Medical Products Administration Has Issued "Consumer Risk Alerts for Injectable Medical Aesthetic Devices": In China, approved injectable dermal fillers such as cross-linked sodium hyaluronate gel and collagen implants must be administered into the dermis or subcutaneous tissue using medical devices like injection needles. In accordance with relevant regulations, such injections must be performed by licensed physicians with clinical experience in related specialties at qualified medical aesthetic institutions, strictly following the instructions for use provided with the medical device.

Targeting service providers, regulatory authorities have conducted multiple special rectification campaigns. In November 2022, 18 departments, including the Ministry of Industry and Information Technology, the State Administration for Market Regulation, and the Cyberspace Administration of China, jointly issued the Action Plan for Further Improving the Quality of Products, Engineering, and Services (2022–2025), which proposed to “set national medical quality and safety improvement targets on an annual basis to promote the continuous improvement of medical service quality, and strengthen comprehensive regulatory enforcement in medical aesthetics.”

In December 2022, the National Medical Products Administration announced seven cases of illegal activities involving drugs and medical devices for medical aesthetics, including one in which Jiaxing Baihui Medical Aesthetics Outpatient Department Co., Ltd. purchased drugs from illegal channels and used unregistered sodium hyaluronate gel for injection as a medical device.

The entities exposed in this year’s 3.15 Gala are primarily participants on the production and sales sides, which will prompt regulatory authorities to further extend the scope of supervision and intensify enforcement efforts.

According to media reports, on the evening of March 15, the Guangzhou Municipal Administration for Market Regulation issued a situation briefing stating that the CCTV “3·15” Gala had exposed complaints in the medical aesthetics industry, with the products involved linked to manufacturers in Guangzhou. The municipal and district-level market regulation authorities in Guangzhou immediately took action, rushing to the scene at the earliest opportunity to investigate and handle the enterprises involved, seal off the implicated products, and organize sampling inspections. Follow-up strict investigations and penalties will be carried out in accordance with laws and regulations, and timely updates will be provided to the public.

Only when the non-compliant industrial chain is thoroughly cleaned up from the service end to the production end can compliant enterprises and service agencies engaged in lawful production and operations secure greater market development opportunities, thereby fostering a healthier market ecosystem.