China's Radiopharmaceutical Sector Enters 2.0 Era Amid Shifting Competitive Landscape

During the Two Sessions, nuclear medicine became a hot topic of discussion. CPPCC members Li Sijin and Yang Jiancheng, as well as NPC deputy Luo Qi, offered their insights and recommendations to promote the innovative development of nuclear medicine in China.

On March 8, the People’s Daily Health Client’s “Two Sessions Health Strategy” column, featuring a segment on Innovation and High-Quality Development in Nuclear Medicine, hosted a live-streamed event across all major platforms. The event featured National Committee Member of the Chinese People’s Political Consultative Conference Li Sijin; Wang Jing, Director of the Department of Nuclear Medicine at Xijing Hospital; Shi Hongcheng, Director of the Department of Nuclear Medicine at Zhongshan Hospital Fudan University; and Wang Chao, President of the Molecular Imaging Business Unit at United Imaging Healthcare. The discussion focused on the collaborative innovation among government, industry, academia, research institutions, and medical practitioners in China’s nuclear medicine sector, offering recommendations for building a collaborative innovation system tailored to the characteristics of nuclear medicine development in China. The live stream garnered a total of 2.017 million views across all platforms, demonstrating widespread public interest in nuclear medicine.

Nuclear medicine is an independent discipline that utilizes radiation emitted by radionuclides for the diagnosis, treatment, and study of diseases. Its most distinguishing features are early diagnosis and targeted therapy. Radiopharmaceuticals (radioactive drugs) are the cornerstone of nuclear medicine; this field relies on various radiopharmaceuticals to diagnose and treat complex and refractory conditions. Furthermore, the operation of equipment such as PET/CT and SPECT/CT is inherently dependent on these radiopharmaceuticals.

In layman's terms, by labeling with different radionuclides, radiopharmaceuticals can achieve early visual diagnosis (using gamma-emitting radionuclides) and precisely locate lesions like a GPS system. They then exert potent, tumor-destroying effects akin to a "nuclear strike," selectively eradicating the target while minimizing damage to surrounding healthy tissues (using alpha- or beta-emitting radionuclides). In recent years, the therapeutic and diagnostic roles of radiopharmaceuticals in cardiovascular diseases, oncology, and neurodegenerative disorders have become increasingly prominent, driving substantial clinical demand.

Nuclear medicine enterprises, which bear the responsibility for the research, development, and production of radiopharmaceuticals, constitute a crucial link in advancing the development of nuclear medicine in China. What is the current state of development in China’s radiopharmaceutical sector? Which companies are competing in this arena? What does the competitive landscape look like? This article provides an in-depth analysis from multiple perspectives, including market entry timing, financing and mergers and acquisitions, and product pipelines.

The International Radiopharmaceutical Market Is Highly Prosperous

In the 1950s, Abbott launched its first commercial nuclear medicine product.131Radioiodinated Serum Albumin (RISA) pioneered the entry of radiopharmaceuticals into the healthcare market, giving rise to the global radiopharmaceutical industry.

In recent years, as multinational pharmaceutical companies such as Bayer and Novartis have entered the field of radiopharmaceuticals, the industry has been thrust into the spotlight and hit the “accelerator button,” with frequent large-scale mergers and acquisitions and a highly active market.

Table 1: M&A Events in the Field of Radiopharmaceuticals

According to incomplete statistics, there are approximately 80 nuclear medicine companies in Europe and the United States, primarily operating in four niche sectors: radioisotopes, API and equipment supply; innovative radiopharmaceutical R&D; radiopharmaceutical manufacturing (including CMO and CDMO services); and radiopharmaceutical CRO services.

The subsector with the highest number of participants and the most active financing is innovative radiopharmaceutical R&D, which mainly includes: (1) companies primarily engaged in the R&D of diagnostic radiopharmaceuticals, such as Lantheus, ImaginAb, and Avid; (2) companies engaged in the R&D of both therapeutic and diagnostic radiopharmaceuticals, such as Fusion, ITM, and Telix; (3) companies focused on the R&D of therapeutic radiopharmaceuticals, such as Alpha Tau, Aktis, and POINT; and (4) a small number of companies originally engaged in conventional innovative drug R&D that have initiated therapeutic radiopharmaceutical R&D through in-house development or mergers and acquisitions, such as IPSEN, Novartis, Bayer, and CellPoint.

The prosperity of the nuclear medicine market in Europe and the United States is also reflected in its continuously updated product pipeline. As of the end of March 2022, 60 nuclear medicines (covering 18 radioactive isotopes) had been approved for marketing by the U.S. FDA. According to a report by MEDraysintell, the global nuclear medicine market size was $4.8 billion in 2017 and is projected to reach $26 billion by 2030.

Early Signs of Shifting Competitive Landscape in China’s Radiopharmaceutical Industry

In contrast, China incorporated radioisotope technology into the “1956–1967 National Program for Long-Range Development of Science and Technology,” marking the beginning of vigorous growth in its isotope industry, particularly during the 1960s and 1970s.131I、125I、32P、99MO-99mMore than ten types of radionuclides and their products, including Tc generators, were successively developed and supplied to the market in bulk, addressing the urgent needs of clinical nuclear medicine applications in China at that time.

However, since the beginning of the 21st century, China has suffered from a severe lack of momentum in the research and development of innovative radiopharmaceuticals, with very few new products brought to market. Driven by growing clinical demand and reliance on traditional products, China Isotope & Radiation Corporation (CIRC) and Dongcheng Pharmaceutical have captured the majority of the domestic radiopharmaceutical market, maintaining a duopoly for an extended period.

China Isotope & Radiation Corporation (CIRC) is a subsidiary controlled by China National Nuclear Corporation (CNNC). Its predecessor, China Isotope Co., Ltd., was established in 1983. In 2011, through the acquisition of Atom High-Tech and CNNC GaoTong, both also under CNNC, its business scope expanded from primarily importing isotope products to the research, development, manufacturing, and sales of such products. Currently, its business primarily covers five major areas: radiopharmaceuticals, radioactive source products, irradiation applications, independent medical laboratory services, and radiotherapy equipment. The radiopharmaceuticals business is mainly operated by its subsidiaries Atom High-Tech, CNNC GaoTong, and Ningbo Jun’an.

Compared with China Isotope & Radiation Corporation, Dongcheng Pharmaceutical, which started with active pharmaceutical ingredients such as sodium heparin and chondroitin sulfate, entered the nuclear medicine field later, only beginning its foray into radiopharmaceuticals in 2015 through the acquisition of Chengdu Yunke Pharmaceutical. Since then, it has successively acquired Shanghai Yitai Pharmaceutical, GMS (China), and Nanjing Jiangyuan Andike, further expanding its radiopharmaceutical product pipeline.

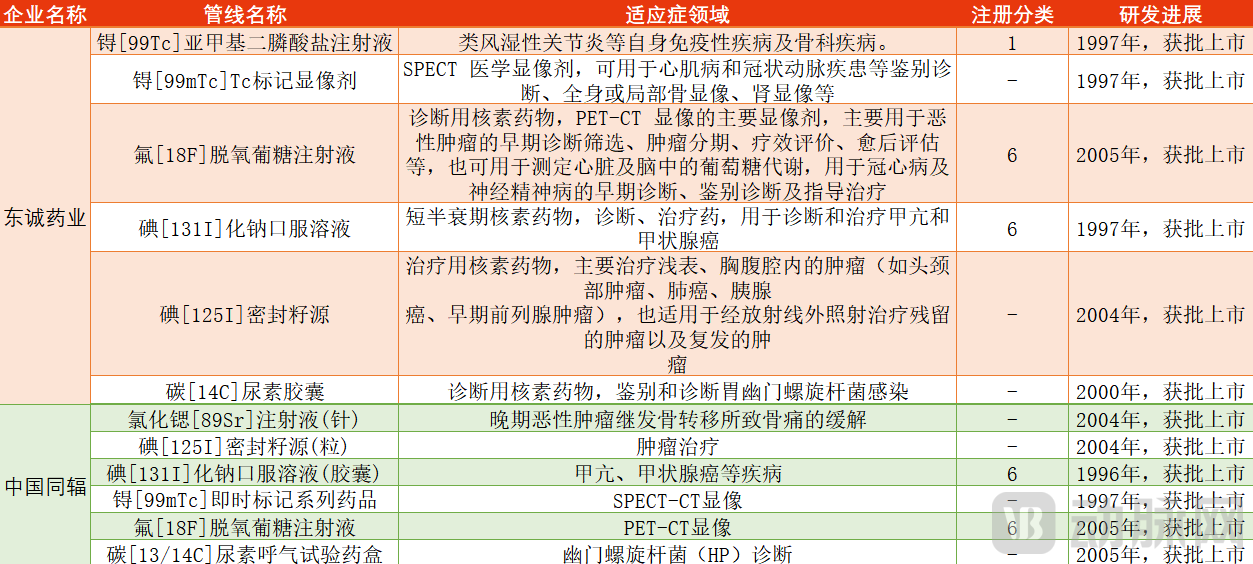

Although radiopharmaceuticals have generated substantial revenue for China Isotope & Radiation Corporation and Dongcheng Pharmaceutical, as shown in Table 2, their currently marketed radiopharmaceutical products are highly homogeneous. Moreover, these products were approved relatively early and are mostly generics of drugs that have been marketed abroad for many years, resulting in an aging product portfolio with narrow indications.

Table2: Marketed Products of China Isotope & Radiation Corporation and Dongcheng Pharmaceutical

Table2: Marketed Products of China Isotope & Radiation Corporation and Dongcheng Pharmaceutical

Meanwhile, overseas radiopharmaceuticals continue to be updated. In the area of diagnostic radiopharmaceuticals, in addition to18In addition to ¹⁸F-FDG, other agents have been approved for marketing abroad, including18F-florbetapir、18F-flutemetamol、18Multiple diagnostic agents for Alzheimer’s disease, including ¹⁸F-florbetaben. In 2020, the U.S. FDA approved64The market launch of Cu-DOTATATE injection has enriched the variety of radionuclides available for NETs imaging agents. With the68Ge/68The increasing maturity and widespread adoption of Ga generator and related targeted drug development technologies,68Ga-labeled drugs have also been successively launched. In 2016, the FDA approved an imaging agent for somatostatin receptor (SSTR)-positive neuroendocrine tumors.68Ga-DOTA-TATE (brand name Netspot), an imaging agent for the same indication to be approved shortly thereafter68Ga-DOTA-TOC was approved for marketing in the European Union in 2016 and in the United States in 2019; in December 2021 and March 2022, two additional companies’ products were respectively approved.68Ga-PSMA-11, for the diagnosis of prostate-specific membrane antigen-positive prostate cancer.

In the field of therapeutic radiopharmaceuticals, numerous products have also been successively launched in international markets. For instance, Xofigo (radium-223 dichloride), indicated for patients with metastatic castration-resistant prostate cancer (mCRPC) and bone metastases,223Ra] injection), Lutathera (for the treatment of gastroenteropancreatic neuroendocrine tumors (GEP-NETs)177Lu-DOTATATE), Pluvicto (for the treatment of patients with PSMA-positive metastatic castration-resistant prostate cancer (mCRPC)177Lu-PSMA-617), with their significant imaging results and therapeutic efficacy, as well as the substantial clinical demand for treatment, have made therapeutic radiopharmaceuticals and theranostic agents the latest development direction in the radiopharmaceutical market.68Ga、177Lu、225Ac、90With radionuclides such as Yttrium gaining prominence, and targets like SSTR, PSMA, CXCR4, and FAP emerging as key focuses, the radiopharmaceutical market has entered a new era.

Radiopharmaceuticals, particularly diagnostic agents, generally have short half-lives, precluding long-term storage and imposing strict requirements on distribution distance and timeframes. Consequently, their operation must adopt a model of on-site labeling and immediate delivery to hospitals. To expand the supply reach of these products and enhance clinical accessibility, China Isotope & Radiation Corporation and Dongcheng Pharmaceutical have both undertaken large-scale nationwide deployments of radiopharmacies over the past decade.

As of June 30, 2022, China Isotope & Radiation Corporation had seven radiopharmaceutical products under development, two of which were in the clinical trial stage (131I-MIBG injection, fluorine[18F] Sodium Chloride Injection), 1 IND pending approval (palladium[103Pd]-sealed seed sources), with four candidates in preclinical stages. Dongcheng Pharmaceutical established Shanghai Lannacheng Biotechnology Co., Ltd. in 2021, focusing on innovative radiopharmaceutical R&D; currently, several of its products have received Investigational New Drug (IND) approval in China and the United States.

However, Grand Pharma's SIR-Spheres®Yttrium [90Y] Microspheres Injection Approved for Market Launch; Xiantong Medicine’s Neuraceq®Fluorine[18F] Bi Ta Ban Injection has submitted an NDA, and Lutetium [177Lu] Lutetium-177 oxodotreotide injection is currently undergoing Phase III clinical trials. Numerous other companies newly entering the radiopharmaceutical sector are also rapidly advancing their pipelines of innovative products. In contrast, China Isotope & Radiation Corporation and Dongcheng Pharmaceutical have fallen behind, with early signs of a shifting landscape in China’s radiopharmaceutical market beginning to emerge.

More Than 20 Nuclear Medicine Companies Compete as the First Tier Poised for an IPO Surge

The Radiopharmaceutical Industry Chain: Upstream involves the supply of medical isotopes; midstream encompasses radiopharmaceutical R&D, manufacturing, sales, and distribution; downstream pertains to clinical applications in nuclear medicine departments. Market-driven radiopharmaceutical R&D and manufacturing enterprises play a pivotal connecting role throughout the industry chain. Only when these midstream companies possess a robust pipeline of products under development and on the market, along with capacity for stable, large-scale production, can they continuously meet clinical demands and, in turn, stimulate the upstream sector’s capability to achieve stable, large-scale production and supply of medical isotopes.

According to incomplete statistics, there are currently more than 20 radiopharmaceutical R&D enterprises in China’s market. Compared with the small-molecule and large-molecule drug sectors, the number of companies entering the radiopharmaceutical market is relatively small. This is mainly due to the high barriers to entry in the radiopharmaceutical industry: on the one hand, the construction cycle for radiopharmacies is long and requires substantial investment; on the other hand, obtaining the necessary qualifications to operate a radiopharmacy involves numerous requirements and certain thresholds; additionally, there is a relative shortage of specialized technical talent in China. Companies that possess sufficient capital and have entered the market early are often able to leverage their first-mover advantage to capture a certain share of the market.

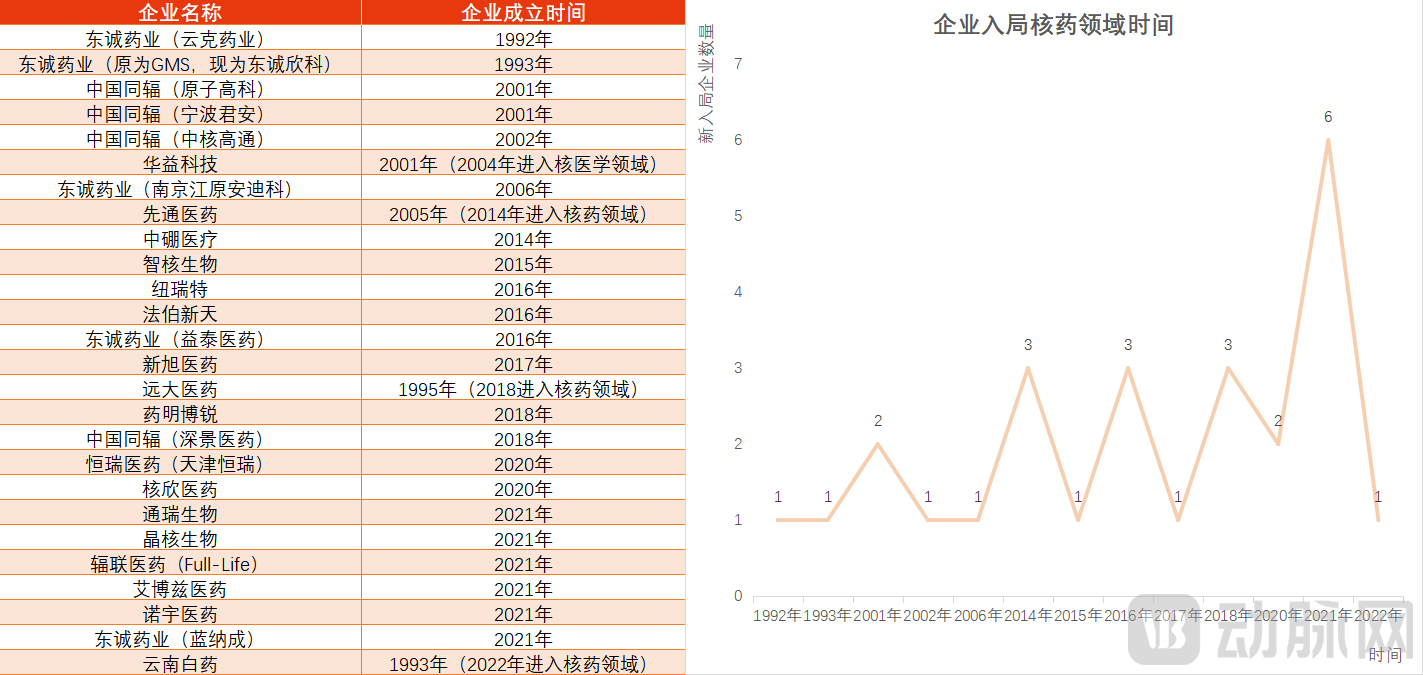

Table 3: Timeline of Domestic Companies’ Establishment or Entry into the Radiopharmaceutical Sector

Table 3: Timeline of Domestic Companies’ Establishment or Entry into the Radiopharmaceutical Sector

As shown in Table 3, apart from China Isotope & Radiation Corporation and Dongcheng Pharmaceutical, companies such as Huayi Technology and Xiantong Medicine entered the radiopharmaceutical industry relatively early and thus possess deeper industry expertise.

Furthermore, Table 3 shows that three established pharmaceutical companies—Grand Pharma, Yunnan Baiyao, and Hengrui Medicine—have all entered the radiopharmaceutical sector. In 2021, China witnessed a surge in the establishment of radiopharmaceutical companies, with six new entrants founded that year. This indicates that, driven by increasing investments of capital, technology, and talent, as well as the introduction of favorable policies such as the Medium- and Long-Term Development Plan for Medical Isotopes (2021–2035), the radiopharmaceutical industry has gradually moved beyond its niche and gained mainstream recognition.

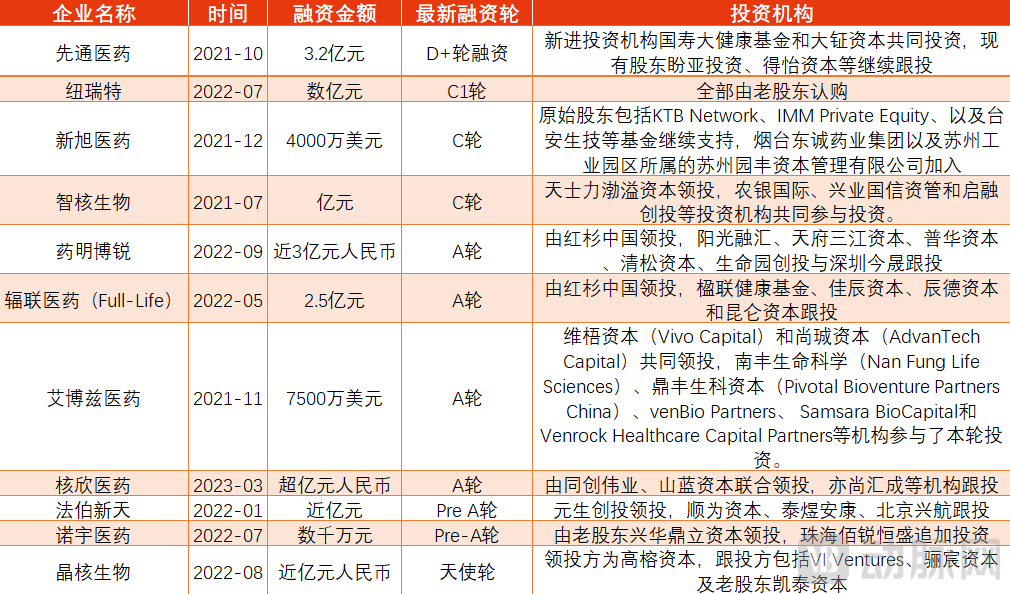

Table 4: Financing Status of Radiopharmaceutical Companies

As shown in Table 4, the nuclear medicine industry has secured substantial financing, with amounts generally exceeding RMB 100 million. Currently, financing rounds for domestic nuclear medicine companies are concentrated at Series A and earlier stages. Only Xiantong Medicine has advanced to Series D, while NuoRuiTe Medical, XinXu Medicine, and ZhiHe Biotechnology have subsequently entered Series C. The nuclear medicine sector as a whole remains in a phase of rapid development. Characterized by its asset-heavy nature, the level of financing in this industry significantly influences the pace of R&D investment, product pipeline layout, talent acquisition, capacity building, and product commercialization.

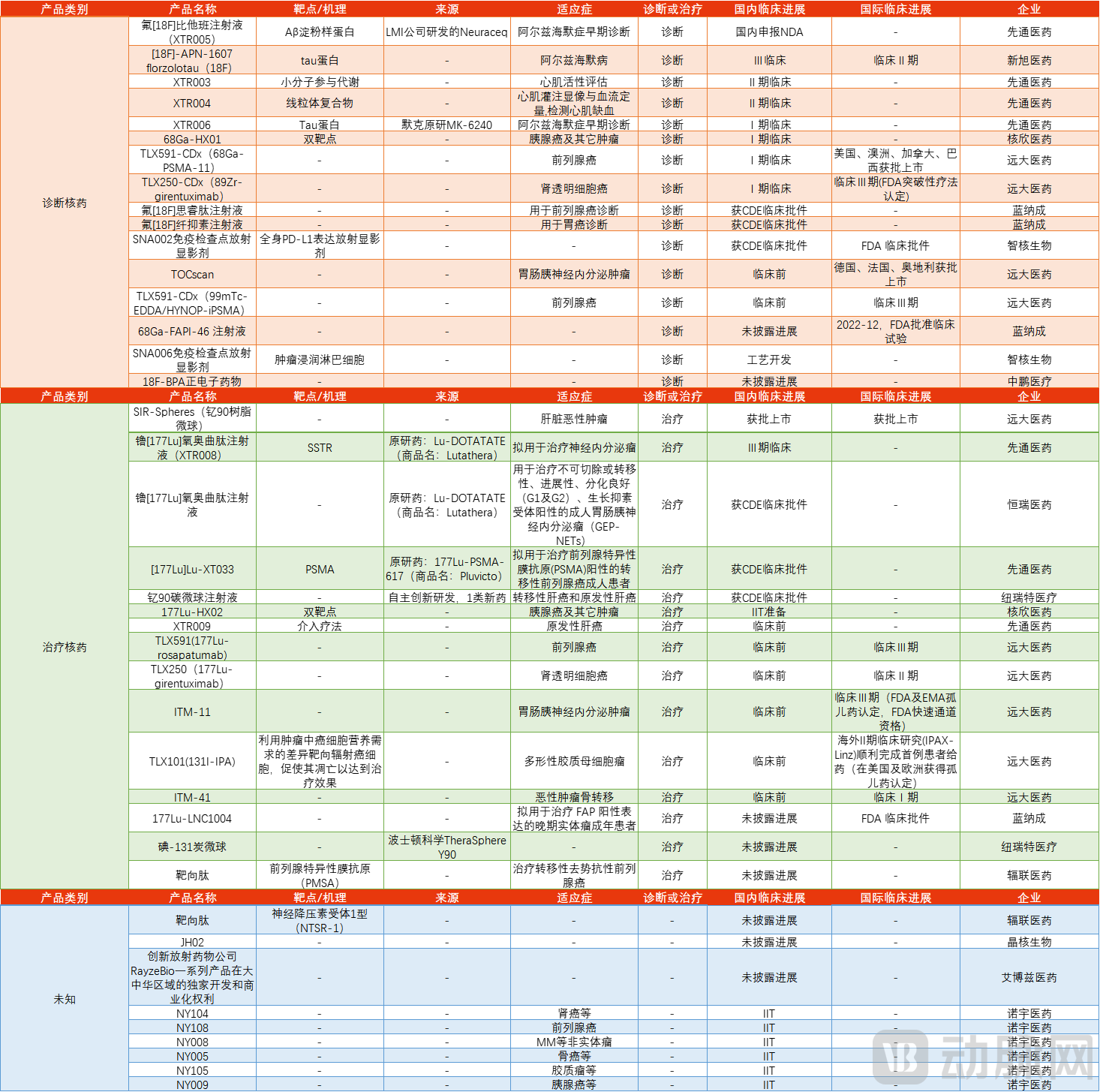

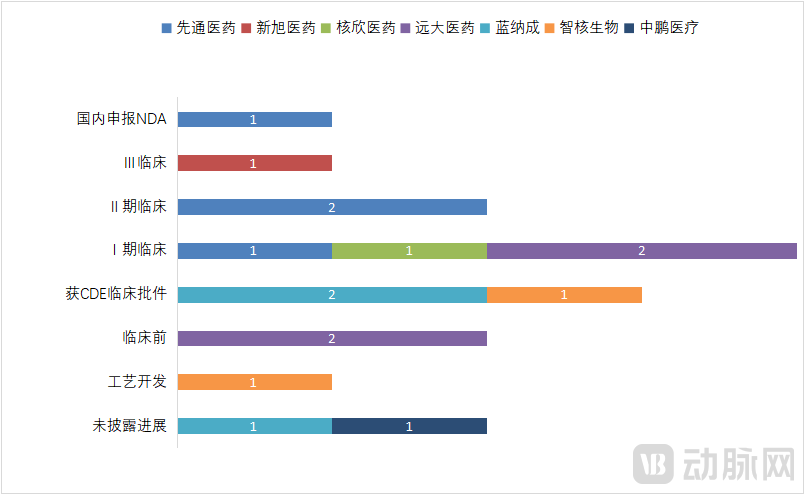

Table 5: Latest Progress in Product Pipeline

Table 5: Latest Progress in Product Pipeline

Currently, innovative diagnostic radiopharmaceuticals under development are primarily indicated for the early diagnosis of Alzheimer’s disease, myocardial perfusion imaging, and tumor diagnosis. At present, Xiantong Medicine (with an NDA submission) and XinXu Medicine (in Phase III clinical trials) are leading domestic R&D progress in China. Notably, Xiantong Medicine has disclosed a pipeline of four products, accounting for nearly half of the post-clinical R&D pipeline in China, demonstrating a significant competitive advantage.

In addition to the domestic market, Zhihe Biopharma and Lannacheng are among the few companies with nuclear medicine pipelines deployed in the United States, while Grand Pharma conducts related clinical trials simultaneously in China and internationally through Sirtex, Telix, and ITM.

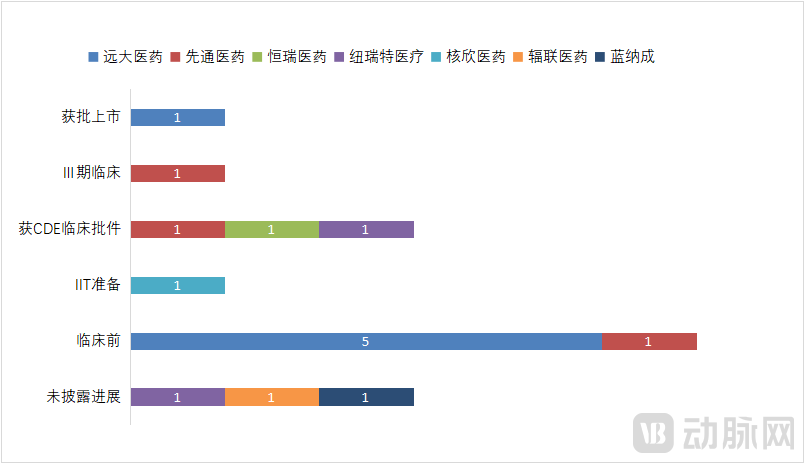

Table 6: Domestic Progress in the Diagnostic Radiopharmaceutical Pipeline

In the field of therapeutic radiopharmaceuticals, four products have been approved for clinical trials in China, including two from Xiantong Medicine, and one each from Hengrui Medicine and Newreat.

Among Xiantong Medicine’s products, one is benchmarked against Lutathera, a targeted radiopharmaceutical approved by Novartis in 2018 as the world’s first of its kind. Currently, Xiantong Medicine is making the fastest progress, having initiated Phase III clinical trials, while Hengrui Medicine successfully obtained an Investigational New Drug (IND) approval for clinical trials earlier this year.

Xiantong Medicine has another product that targets the same mechanism as Pluvicto, the world’s second targeted radiopharmaceutical approved by Novartis in 2022. Since its launch, Pluvicto’s strong sales have far exceeded Novartis’ expectations, leading to supply shortages. Novartis is currently accelerating capacity expansion, which will enable an annual production capacity worth $8 billion upon completion.

Nurite’s products are independently developed yttrium [90Y] Carbon Microsphere Injection, following Yttrium [90Y] Glass microspheres, Yttrium [90Yttrium-90 resin microspheres, the third generation of yttrium-90 products globally approved by drug regulatory authorities for clinical use or clinical research90Y] microspheres. Currently, this product is about to initiate clinical trials for two indications: metastatic liver cancer and primary liver cancer.

Table 7: Domestic Progress in the Therapeutic Radiopharmaceutical Pipeline

In recent years, with the influx of resources such as policy support, capital, and talent, the radiopharmaceutical sector has become increasingly vibrant. Established pharmaceutical companies such as Grand Pharma, Yunnan Baiyao, and Hengrui Medicine have entered the field, while newly founded biotech firms like Lannacheng, Aibozhi Pharmaceutical, and Fulian Pharmaceutical have also joined the race. However, the radiopharmaceutical industry is characterized by high regulatory barriers, significant asset intensity, and a strong reliance on R&D experience. Therefore, the layout of product pipelines and progress in research and development often better reflect a company’s value. In the fields of diagnostic and therapeutic radiopharmaceuticals, companies with extensive pipeline accumulations and advanced R&D progress, such as Xiantong Medicine, Hengrui Medicine, and Grand Pharma, hold a more prominent leading advantage.

Conclusion

In the 1950s, the nuclear medicine industry formally took off in China, ushering in a wave of development. However, since the turn of the 21st century, the severe lack of momentum in innovative radiopharmaceutical R&D has resulted in few new product launches. Now, as the sector enters its “2.0 era,” it is experiencing rapid growth. The introduction of newer radiopharmaceutical agents, broader indications, expanded market potential, and an increasing number of market participants are driving a renaissance in nuclear medicine, bringing about new changes in the competitive landscape.

Traditional radiopharmaceutical companies are increasingly unable to meet the urgent clinical development needs or adapt to new market dynamics. We believe that the future of the radiopharmaceutical sector will belong to those competitors who combine deep industry expertise with a proactive commitment to innovation, thereby delivering greater benefits to patients.