Is the Multi-Billion-Yuan Acid Suppression Market Undergoing a Generational Shift? It May Be Too Early to Conclude

Acid-suppressing drugs are medications that inhibit gastric acid secretion. Excessive gastric acid production in the human body may lead to discomforting symptoms such as stomach pain and heartburn. Currently, acid-suppressing drugs available on the market are primarily categorized into the following major classes: proton pump inhibitors (PPIs), H2 receptor antagonists (H2RAs), and alkaline antacids.

Among them, proton pump inhibitors (PPIs), as high-quality drugs for treating acid-related disorders, have dominated the acid-suppression market for over three decades. However, the multi-billion-dollar oral acid-suppressant market appears to be welcoming new competitors. With the launch of a new class of acid-suppressing agents—potassium-competitive acid blockers (P-CABs)—their potent and rapid acid-suppressing effects have attracted widespread market attention. There is much speculation about how much market share P-CABs will ultimately capture, and even whether they will replace PPIs to become the new dominant force in the acid-suppressant market.

Judging from the developmental trajectory of acid-suppressive medications, progressing from H2 receptor antagonists (H2RAs) to proton pump inhibitors (PPIs) and then to potassium-competitive acid blockers (P-CABs), their acid-suppressing potency has steadily increased. It may appear that enhanced acid suppression is the hallmark of newer generations of acid suppressants. However, this is not the case.

According to the epidemiology of gastroesophageal reflux disease (GERD), approximately 87% of patients in China are classified as Los Angeles Classification Grades A and B (mild to moderate mucosal injury), while 13% are classified as Grades C and D (severe mucosal injury). Currently, standard-dose proton pump inhibitor (PPI) therapy is effective for treating patients with mild to moderate disease, and double-dose PPI therapy can also achieve favorable outcomes in patients with severe disease. In addition to its rapid onset of action and potent acid suppression, potassium-competitive acid blocker (P-CAB) therapy is less affected by food intake and provides sustained drug effects, enabling rapid control of disease in critically ill patients.

However, P-CABs are rarely prescribed for ordinary patients. Studies indicate that Asians have fewer gastric parietal cells and lower levels of acid secretion compared to Westerners. Excessively potent and inappropriate acid suppression can disrupt normal gastric acid secretion and alter the gastric environment, leading to symptoms such as dyspepsia. Long-term, high-intensity, and inappropriate acid suppression may also result in deficiencies in minerals and nutrients such as calcium, iron, and vitamin B12. In this light, PPIs and P-CABs are not in competition or serving as substitutes for one another; rather, they represent a progressive and complementary relationship.

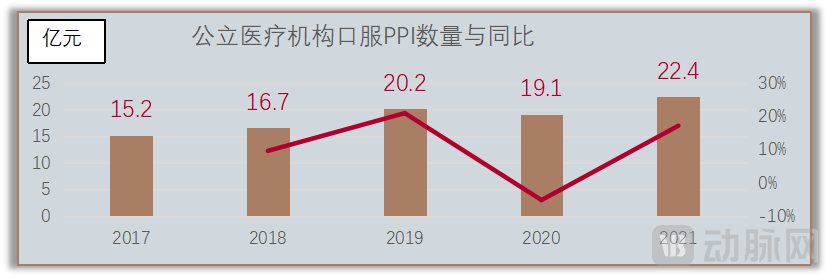

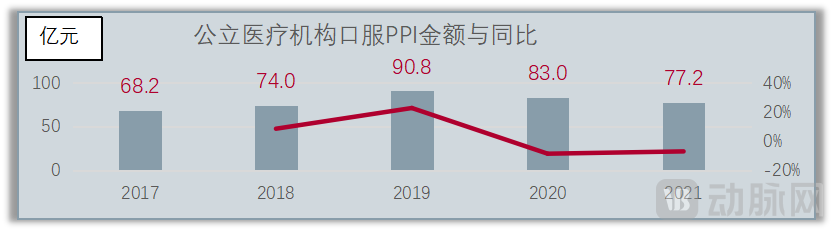

From a market perspective, the number of patients with gastrointestinal diseases in China is increasing annually, driven by deepening population aging and urbanization. According to IQVIA data, the sales volume of oral proton pump inhibitors (PPIs) has shown sustained overall growth, with only a slight decline in 2020 due to the sudden outbreak of the pandemic. In contrast, sales revenue has decreased year by year since 2019, primarily influenced by the national centralized procurement policy and the Key Monitoring Drug List.

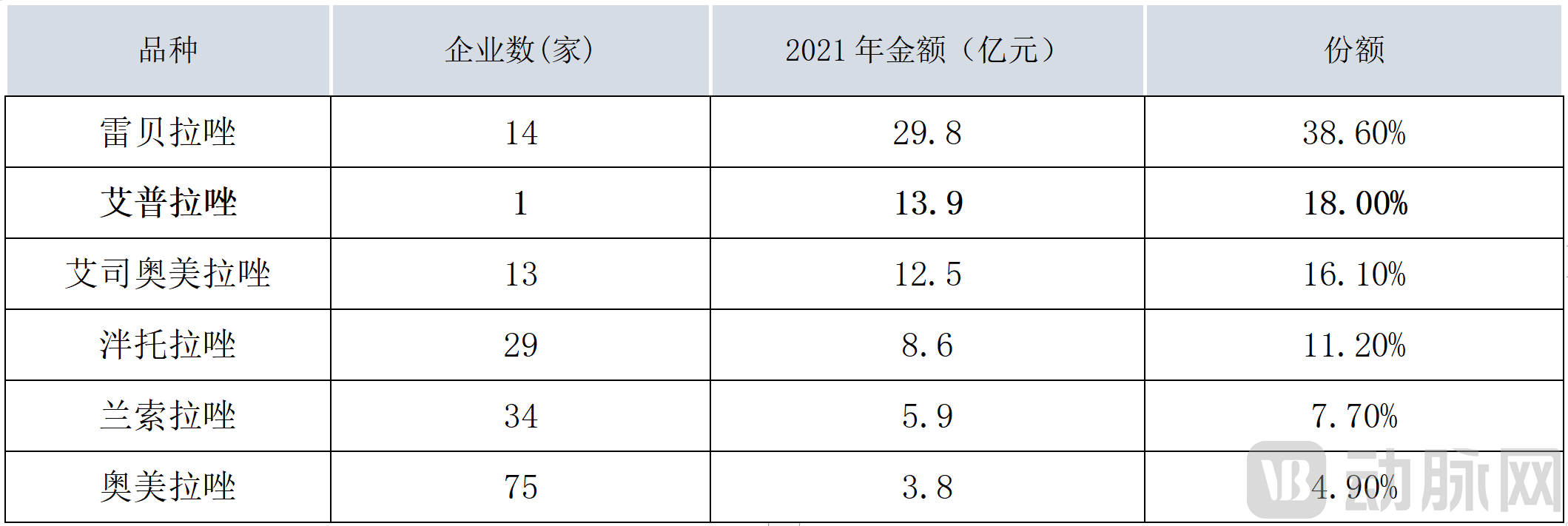

Currently, the PPI market is saturated with a wide variety of drugs, forcing generic manufacturers to compete for survival by lowering prices and squeezing profit margins. In contrast, pharmaceutical companies with exclusive products and patented technologies can easily stand out, rapidly capture market share, and achieve substantial investment returns. For instance, Ilaprazole, which faces no risk of inclusion in volume-based procurement and was not listed in the Second Batch of National Key Monitoring List for Rational Drug Use, captured an 18% market share in 2021 as a single-source product.

Market demand for acid-suppressing drugs is growing, while profits from generic versions continue to shrink. This is why Chinese pharmaceutical companies are continuously developing new acid-suppressing medications. It can be said that the normalization of national centralized procurement and the implementation of the key monitoring list have set a significant hurdle for PPI generics: cross it and survive, fail to do so and perish. Who will take over the vacated market share may depend on which company’s innovative drug can seize the initiative first. Although P-CABs appear to be gaining strong momentum, they still require close monitoring for long-term risks in clinical practice, meaning there is a long road ahead. Furthermore, given the vast difference in the magnitude of eligible patient populations, it seems premature to assert that P-CABs will become the dominant force in the next generation of the acid-suppressing drug market.