How U.S. Venture Capitalists Make Decisions: Insights from a Survey of 885 Investors

Venture Capital (VC) is one of the most critical components of our industry. For years, venture capitalists have played a vital role in the industry and the broader economy by providing funding to high-growth startups.

Nevertheless, there is little understanding of what venture capital actually does and how it creates value. This is partly because venture capitalists themselves often prefer to stay behind the scenes, shrouded in mystery. What is certain is that most of us have a general sense that they fill a critical market need by connecting entrepreneurs with promising ideas but lacking funding to investors who have capital but lack ideas.

A U.S. study surveyed 885 venture capitalists from 681 venture capital firms, encompassing the vast majority of leading VC firms, and was followed by dozens of interviews. This study represents the most comprehensive and detailed investigation of the venture capitalist community to date.

The survey inquired about how they source deals, select and close investment transactions, manage portfolio companies post-investment, structure their work schedules, and maintain relationships with limited partners (LPs).

The survey results, backed by comprehensive data, corroborate some of our earlier general perceptions—for instance, that investors prioritize founders above all else when making investment decisions, and that venture capital firms allocate substantial resources across deal sourcing, deal selection, and post-investment value creation.

Other findings have updated outsiders’ conventional perceptions of the venture capital industry. For example, the survey found little evidence that venture capital firms use the standard financial analysis techniques taught in business schools to evaluate deals; indeed, a small number of venture capitalists do not even forecast companies’ cash flows at all.

In summary, these survey results are rich in detailed data and information, enabling a deeper understanding of investors’ working models and their values. Of course, these insights are based on research into U.S. venture capitalists (VCs); Chinese VCs exhibit distinct operational characteristics and styles. Nevertheless, we believe that many will resonate with the shared journey of identifying valuable innovative projects and supporting their growth to generate both economic and social benefits.

VBInsight has compiled the key findings of this article, hoping to provide insights for both investors and entrepreneurs.

The Daily Life of Venture Capitalists in Numbers

The Daily Life of Venture Capitalists in Numbers

Venture capital firms holding substantial capital have an average of only 14 employees, five of whom are senior partners in decision-making roles.

Venture capital firms have relatively few junior deal-making personnel, with an average of 1.3 venture partners. Other roles within VC firms include entrepreneurs in residence, analysts (typically found only in larger VC firms), back-office personnel, and logistics personnel. Early-stage VC firms are smaller in size, particularly having fewer junior deal-making personnel.

It is widely believed that investors work at a fast pace and put in long hours. While their working hours are indeed longer than those in traditional finance, most venture capitalists surveyed reported that their weekly working hours were not excessive. On average,They work 55 hours per week, spending 22 hours on networking and sourcing deals, and 18 hours engaging with portfolio companies.. During the COVID-19 pandemic, venture capitalists slowed their pace slightly, but their time allocation remained largely unchanged: sourcing new deals, conducting due diligence, closing transactions, and supporting portfolio companies.

Of course, venture capital firms have internal professional specialization. In 60% of the funds, partners focus on different tasks. We asked respondents what they specialized in, and they could choose multiple options. For those firms with specialized partners,44% of respondents are generalists, 52% are responsible for fundraising, and 55% and 53% of investors are responsible for sourcing deals and closing deals, respectively.Interestingly, nearly one-third of investors also stated that they specifically help startups organize social events.

Closing successful deals is crucial for investors.More than 30% of deals originate from the investors’ former colleagues or professional acquaintances; 20% come from referrals by other investors, and 8% from referrals by existing portfolio companies. Only 10% result from cold emails sent to company management. Notably, nearly 30% of venture capital investments are generated through proactive outreach by venture capital firms to entrepreneurs.

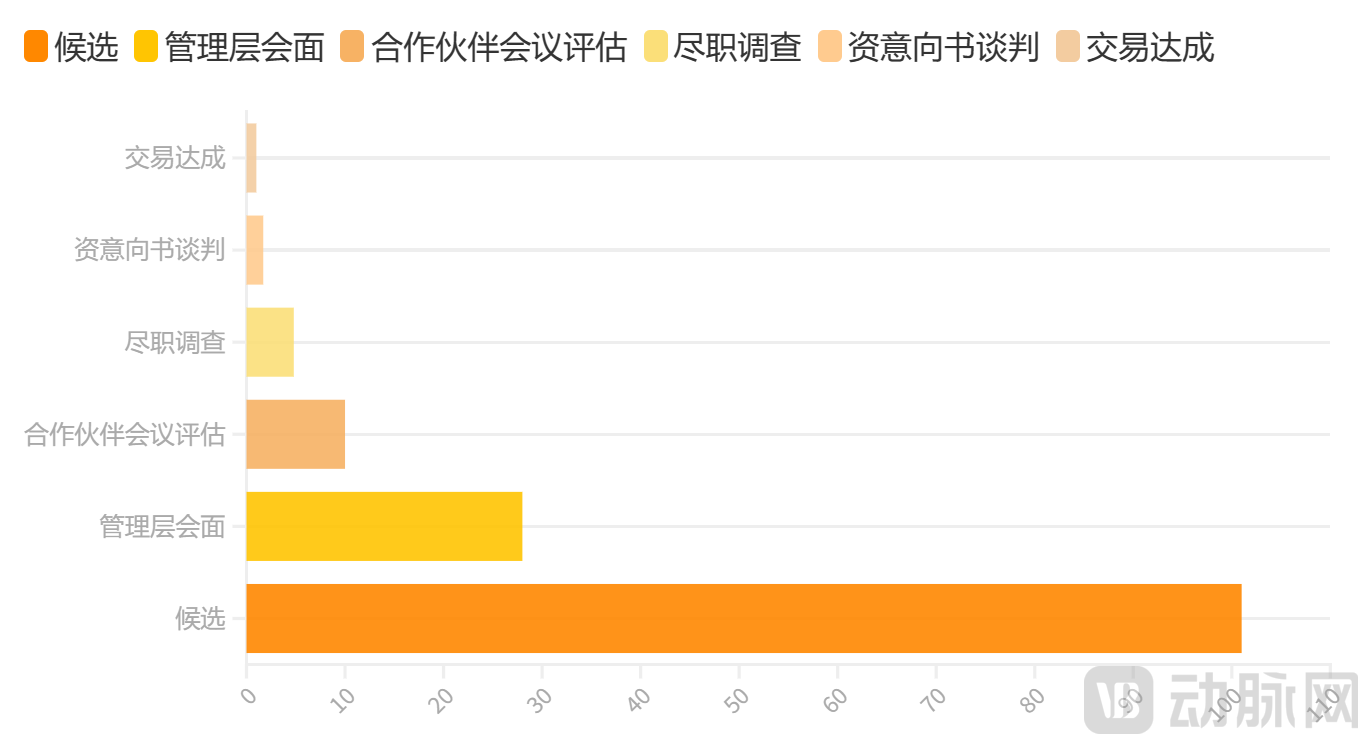

In general,For every deal ultimately closed by a venture capital firm, an average of 101 opportunities are considered. Of these, 28 lead to meetings with management; 10 are evaluated at partner meetings; 4.8 proceed to due diligence; 1.7 advance to the term sheet negotiation stage with startups; and finally, only one results in an investment.

Figure 1:Venture Capital Project Screening Funnel

Data Source: How Venture Capitalists Make Decisions

A typical transaction takes 83 days to complete, during which an average of 118 hours is spent on due diligence and an average of 10 references are contacted.

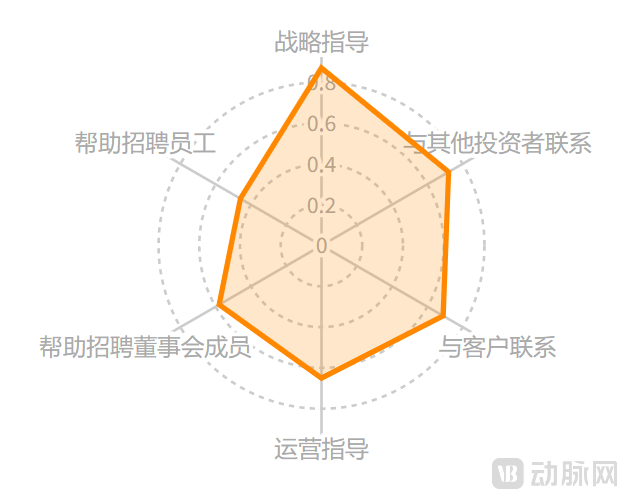

After completing the investment transaction,Venture capitalists engage in at least one “substantive interaction” per week with 60% of their portfolio companies, and have multiple interactions per week with 28% of them. They provide extensive post-investment services: offering strategic guidance to 87% of portfolio companies, connecting 72% with other investors, helping 69% secure customers, providing operational guidance to 65%, assisting 58% in recruiting board members, and even helping 46% hire employees.

Figure 2:Weekly Interaction Frequency Between Venture Capitalists and Portfolio Companies

Data Source: How Venture Capitalists Make Decisions

Given the substantial time and effort invested, how do partners at venture capital (VC) firms reap returns from investment deals? In 74% of VC firms, partners are rewarded based on individual performance. Interestingly, however, larger and more successful VC firms are less likely to tie compensation to individual success. In 44% of VC firms, particularly those managing early-stage funds, partners receive roughly equal shares of the carry. Closely aligned with this figure, in 49% of firms, partners have equal access to investible fund capital. These findings suggest that firms maintain consistency between collaborative contributions and rewards for individual success. Nevertheless, overall, VC firms vary in how they compensate their partners.

How Do Investment Firms Make Investment Decisions Internally? Approximately half of all funds—particularly smaller funds and healthcare-focused funds—require a unanimous vote from partners. Another 7% of funds require unanimity but allow for one dissenting vote. Around 20% of funds require consensus among partners, some of whom hold veto rights. Finally, 15% of funds operate based on a majority vote.

How Venture Capitalists Make Decisions

How Venture Capitalists Make Decisions

1. Seeking Transactions

The first task facing venture capitalists is to establish connections with startups seeking financing, a process known in the industry as “deal flow generation.” As previously mentioned, over 30% of deals come from VCs’ former colleagues or professional acquaintances. Twenty percent of deals stem from referrals by other investors, and 8% originate from recommendations by existing portfolio companies.

Jim Breyer, founder of Breyer Capital and Facebook’s first venture capital investor, believes that high-quality deal flow is crucial to generating substantial returns. “I have found that the best deals often come from my network of trusted investors, entrepreneurs, and professors,” said Jim Breyer. “My colleagues and partners help me quickly screen opportunities and prioritize those I should take seriously. Experts are immensely helpful in generating a large pool of potential investments and narrowing it down to the highest-quality candidates.”

Rick Heitzmann, founder of the venture capital firm FirstMark, believes that “the best opportunities do not always come to our office. We identify and study major trends and proactively reach out to entrepreneurs who share a common vision for the future direction of the world.”

These results indicate that entrepreneurs who lack connections to the right social and professional circles struggle to secure funding.Few deals are closed by founders who walk into venture capital firms’ doors without any prior connections. Indeed, some venture capital executives acknowledge the negative implications of this reality: the need to access certain networks can place entrepreneurs from specific groups—such as women and ethnic minorities—at a disadvantage, causing investment firms to miss out on talent and opportunities.Investment institutions should consider diversifying their partners and relationship networks.

2. ReviewEstimated Transaction Value

As previously mentioned, for every deal ultimately closed by a venture capital firm, an average of 101 opportunities are considered. This means that even if startups seeking financing establish contact with venture capitalists, their chances of securing investment remain very low.

What Factors Do Venture Capitalists Consider During the Screening Process? A framework suggests that investors either favor the “jockey” or the “horse.” The founding team represents the “jockey,” while the strategy and business model constitute the “horse.” Surveys indicate that although investors deem both the jockey and the horse essential, they ultimately regard the founding management team as more critical. As legendary venture capitalist Peter Thiel stated, “Our fate hinges on our founders.”

Investigations revealed that,95% of venture capital firms consider founders a critical factor in investment decisions, 74% regard business models as important, 68% view the market as a key factor, and 31% see the industry sector as significant.

Surprisingly, when ranking the core factors that investors focus on in their investment projects by citation frequency, company valuation ranks only fifth. In fact, while chief financial officers of large corporations typically use Discounted Cash Flow (DCF) to evaluate investment opportunities, few venture capitalists employ DCF or other standard financial analysis techniques to assess deals. Instead, the most commonly used metric to date is cash-on-cash return, or the Multiple Of Invested Capital (MOIC). The second most frequently used metric is the annual Internal Rate of Return (IRR) generated by the transaction. Hardly any venture capital firms adjust their target returns based on systematic (or market) risk.

More notably, the survey found that 9% of respondents did not use any quantitative metrics to evaluate transactions. Consistent with this finding, 20% of venture capitalists and 31% of early-stage venture capitalists stated that they do not forecast companies’ financial performance at all when making investment decisions.

In other words, few venture capital firms employ standard financial analysis techniques to evaluate a deal.

How can this disregard for traditional financial valuation be explained? Venture capitalists understand that their success stems from exits via mergers and acquisitions (M&A) and initial public offerings (IPOs), which are the true drivers of their returns. Although most investments yield minimal returns, a single successful exit can generate a 100-fold return. Given the volatility of IPO exits,Venture capital focuses on identifying companies with the potential for substantial exits, rather than estimating short-term cash flows.

As J.P. Gan, co-founder of INCE Capital, explained: “Successful venture capital deals take a long time to develop, mature, and exit. We focus heavily on potential return multiples rather than net present value or internal rate of return at the time of investment. The internal rate of return is only calculated when our limited partners have an exit.”

3. After the Handshake

Following the closing of a deal, a typical venture capital term sheet is generally structured to ensure that entrepreneurs receive financial rewards if they perform well, while granting investors control over the company if the entrepreneurs fail to deliver on their commitments.

Valuation is part of the negotiation process among new venture investors, existing investors, and founders. Other aspects involve complex contractual terms—cash flow, control, liquidation, and employment rights. Venture capital firms employ certain terminology and clauses that are critical to their interests. However, there is limited understanding among outsiders regarding which investment terms are most crucial to venture capitalists, which allow for flexibility, which are less negotiable, and how they trade off among these terms.

The investigation revealed that terms related to cash flow rights include anti-dilution protection, dividends, investment amount, option pool, ownership stake, and valuation; those related to control rights include board control and pro-rata rights; liquidation rights encompass liquidation preferences, participation rights, and redemption rights, along with certain employment-related provisions (such as equity incentives and vesting).

If a company raises its next round of financing at a lower valuation, anti-dilution protection grants venture capitalists additional shares. An option pool is a set of shares reserved for employee compensation and incentives. Pro-rata rights entitle investors to participate in subsequent financing rounds. Liquidation preference ensures that investors have priority in the event of liquidation. Participation rights allow venture investors to combine upside potential with downside protection (such that venture investors first receive downside protection and then share in the upside). Redemption rights grant investors the right to redeem their securities or require the company to repay the original investment amount. Equity clawback provisions mean that a portion of the shares held by founders or employees who leave the company will be forfeited.

Research on venture capital investment terms indicates that VCs achieve their objectives by carefully allocating cash flow rights, control rights, liquidation rights, and employment provisions (particularly equity incentives). Equity incentives provide entrepreneurs with the motivation to perform well and remain with the company. Generally, deal structures are designed to allow entrepreneurs who meet specific milestones to retain control and receive financial returns. However, if they miss these milestones, VCs can introduce new management and alter the company’s strategic direction.

Venture capitalists indicate that they are relatively inflexible regarding pro-rata investment rights, liquidation preferences, anti-dilution rights (which protect their potential economic interests), as well as founders’ equity incentives, company valuations, and board control (often regarded as the most critical control mechanism). As one venture capitalist stated, pro-rata rights—which allow VCs to purchase additional shares in a company—are crucial because “the greatest source of our returns is our ability to double down on winners.” VCs are more flexible on matters such as option pools, participation rights, investment amounts, redemption rights, and particularly dividends. Many of these terms have a smaller impact on the potential returns for venture capital, making them more open to negotiation.

In fact,Many venture capital firms, during negotiations with startups, strive not to focus too narrowly on financial terms, but instead place equal emphasis on how well the company fits into their investment portfolio and why their experience and expertise can benefit the founding management team.As Khosla explained to us, “To attract the best entrepreneurs, it is important to have a clear vision beyond just making money. As a venture capital firm, what do you intend to do? Does it align with the entrepreneur’s vision?”

4. Find Alpha

Outsiders know little about the inner workings of venture capital firms. Because VCs typically keep their internal organizational structures confidential, yet these structures may be relevant to venture capital investment decisions.

Once venture capitalists invest in a company, they roll up their sleeves and become active advisors. As previously mentioned: venture capitalists engage in “substantive interactions” with 60% of their portfolio companies at least once a week, and have multiple interactions per week with 28% of their portfolio companies. They provide extensive post-investment services.

Intensive advisory activities are a primary mechanism through which venture capitalists increase the value of their portfolio companies. Surveys indicate that private equity investment firms operate in a similar manner. Jon Callaghan, co-founder of True Ventures, stated that his firm considers advisory services to play a crucial role in attracting top-tier entrepreneurs, having invested 15 years and $10 million in developing these entrepreneurial ventures. He pointed out, “We do this because we have repeatedly recognized that founders are key to building and leading teams, thereby maximizing returns for venture capital investors.”

Top-tier venture capital funds can generate substantial profits. However, there is currently no clear explanation of how venture capital achieves “Alpha” (Alpha coefficient represents unsystematic risk in investment, referring to returns that investors obtain independently of market fluctuations). When asked to assess the relative importance of deal sourcing, deal selection, and post-investment actions in creating value within portfolios, most investors responded that while all three factors are critical, deal selection is the most crucial.

What is the most decisive factor in the success or failure of a portfolio company? In response to this question, the management team is considered the most critical factor to date. As Brian Jacobs, co-founder of Emerging Capital, told us: “I have never seen a venture capital success where one person took all the credit. The winners always seem to be founders who can build a strong team.”

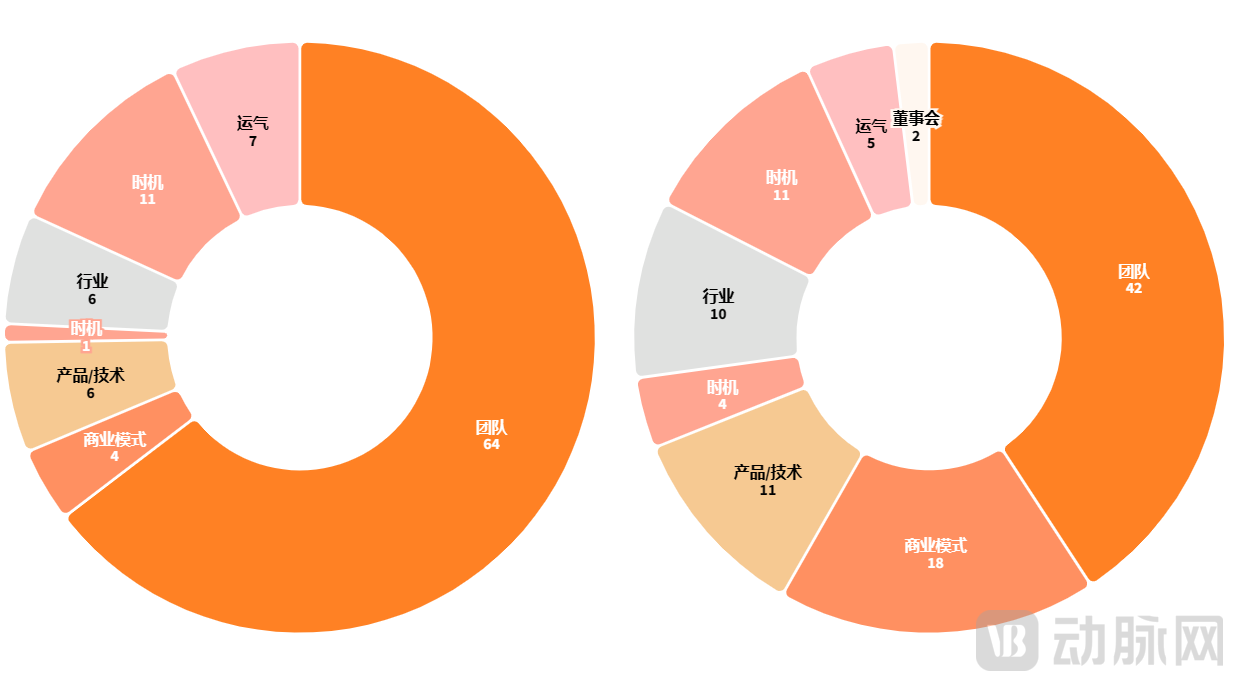

Compared with whether a deal can be closed, the factors determining the success of a transaction are more complex. Other factors cited by venture capitalists include timing, luck, technology, business model, and industry sector.In early-stage investing, the team remains the most significant factor influencing a project’s success; meanwhile, the importance of product/technology is outweighed by the timing of the investment. In late-stage investing, the significance of the business model and the industry sector increases.

Interestingly, timing and luck are considered to have a considerable impact on investment success.

Figure 3: Contribution Ratios of Factors Influencing Transaction Success

Data Source: How Venture Capitalists Make Decisions

Surprisingly,Whether in the early or late stages of a project, venture capitalists do not regard their contributions as the primary source of success.

These findings indicate that it is entrepreneurs, not venture capitalists, who create the greatest value for startups. As one VC executive stated, “Our firm devotes substantial resources to supporting our portfolio companies—ranging from assisting with recruitment to serving as a confidant for founders. Ultimately, however, the true success or failure of a business hinges on its founder.”

Other Interesting Findings

Other Interesting Findings

Certainly,Venture capitalists do not always adhere to a fixed pattern; when they encounter companies they favor, they can be highly aggressive.

Vinod Khosla, co-founder of Sun Microsystems and founder of Khosla Ventures, stated that when venture capital firms become excited about a startup, the power dynamics can shift rapidly, especially if the startup receives offers from other companies. He explained, “The best startups, led by inspiring entrepreneurs, face intense competition for funding. For venture capitalists, the key to winning such opportunities lies in clearly defining what they will and will not do, how they provide genuine value-added support, and how they help realize bold visions. These factors are crucial for fund returns.”

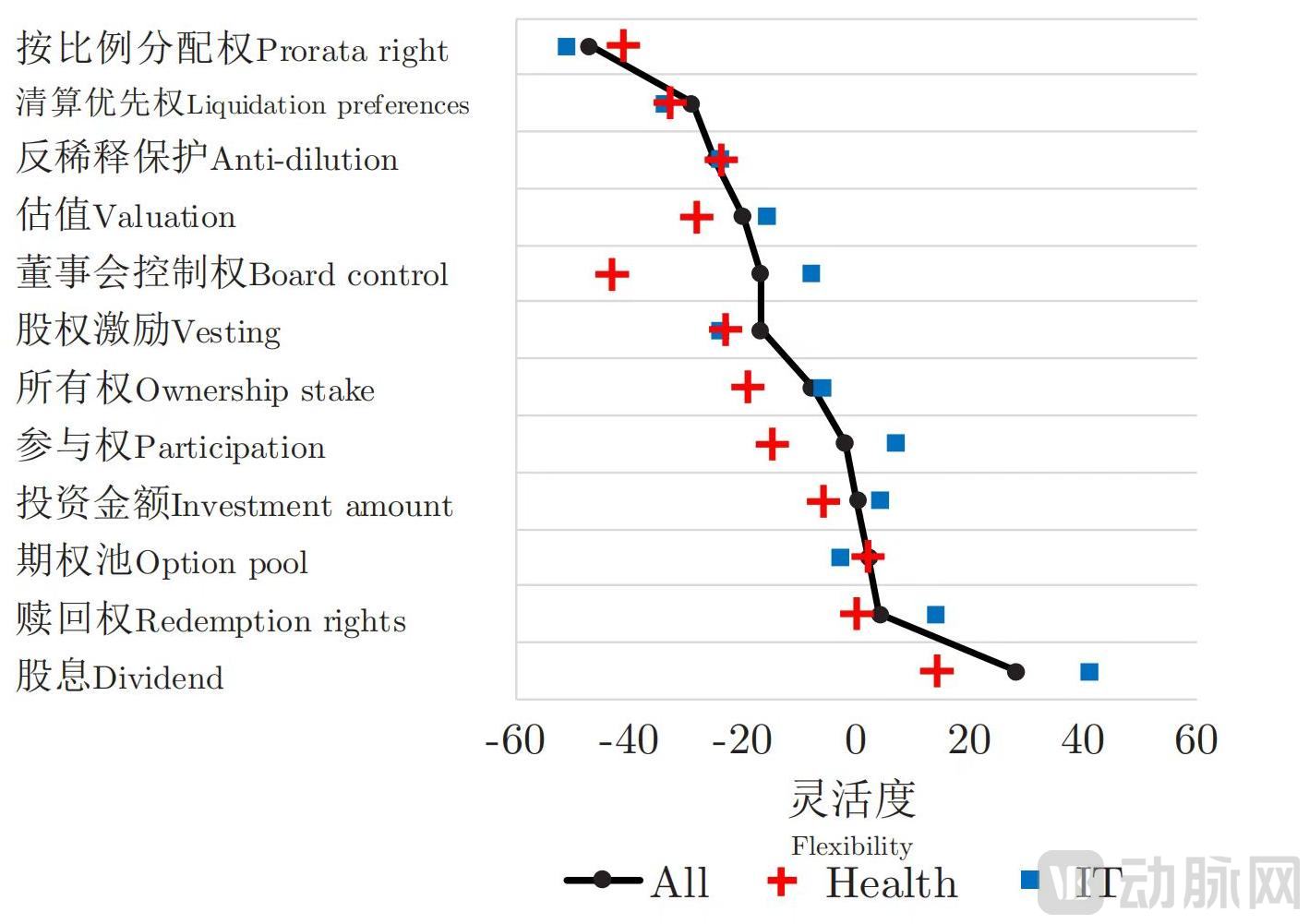

Furthermore, the survey reveals that venture capital firms investing in the healthcare sector are significantly less flexible on many terms compared to those investing in the IT industry. In addition to the pro-rata rights, liquidation preferences, anti-dilution rights, founder equity incentives, company valuations, and board control rights—which we have already discussed as being relatively rigid—VCs in the healthcare sector also demonstrate less flexibility regarding other control provisions, valuations, ownership stakes, and dividends. Board control provisions are particularly noteworthy, as healthcare VCs rank them as the least flexible term, whereas IT VCs are relatively more flexible. This is related to the fact that healthcare companies are more susceptible to internal risks, such as project selection.

Figure 4: Flexibility in Contractual Terms

Note: Average flexibility of respondents when negotiating contract terms on a scale from −100 to 100 (−100 indicates completely inflexible and investor-unfriendly, −50 indicates not very flexible, 0 indicates somewhat flexible, 50 indicates very flexible, and 100 indicates extremely flexible and founder-friendly).

Data source: How Venture Capitalists Make Decisions

We discuss how organization and structure relate to venture capital investment decisions. Venture capital firms in the healthcare sector are more likely to have risk partners, which may also be because investments in the healthcare and biotechnology industries require specialized expertise for evaluation.

Moreover, venture capitalists in the healthcare industry spend more time assisting their portfolio companies than their IT counterparts, despite holding fewer board seats.

Reference Article:

How Venture Capitalists Make Decisions,Paul Gompers, Will Gornall, Steven N. Kaplan, and Ilya A. Strebulaev,Journal of Financial Economics,2019

How Venture Capitalists Make Decisions,Paul Gompers, Will Gornall, Steven N. Kaplan, and Ilya A. Strebulaev,Harvard Business Review,2021