2023 Medical Endoscopy Industry Report: Disposable Endoscopes Are Not Simply Replacements—Domestic Innovation Accelerates to Capture a Blue Ocean Market

This industry survey focuses on two major segments of the endoscopy field: reusable endoscopes and single-use endoscopes.

Reusable endoscopes have a long development history and numerous domestic brands, yet there remains significant room for growth in their share of the domestic market. What is the current status of domestic substitution, and how will their future market share evolve?

The disposable endoscopy sector is still in its early stages of development, with numerous application scenarios yet to be explored and an urgent need for more mature products to achieve market commercialization. What is the current status of clinical application development, and how can companies rapidly establish a foothold and secure first-mover advantage in this blue-ocean market?

To clarify the current landscape and future development trends, this endoscopy industry research report was prepared based on interviews with 10 innovative companies, 3 investment firms, and 21 experts, company founders, and investors, aiming to provide insights for companies committed to the industry’s collective growth.

Core Viewpoints

Medical endoscopes have attracted significant attention from capital markets and policymakers, helping domestically produced products rapidly increase their market share. The market share of Chinese-made medical endoscopes rose from 10% in 2020 to 26% in 2022, with an average annual growth rate exceeding 60%.

It is only a matter of time before domestic alternatives achieve full import substitution, with multiple technologies gaining international influence. Traditional reusable endoscopes are transitioning from “me too” to “me better.” China’s technological capabilities in fluorescent endoscopy and confocal laser endomicroscopy are at the forefront globally.

Disposable endoscopes are positioned within the high-end manufacturing sector, where mass production capability and the ability to secure bulk orders constitute their core competitiveness; a mature reimbursement environment is urgently needed.

Currently, the penetration rate of minimally invasive surgery in China is less than 20%, leaving substantial unmet demand to be explored and satisfied. This necessitates collaborative innovation and advancement in medical endoscopes, endoscopic surgical instruments, equipment, and systems.

In the future, the company will continue to prioritize R&D and develop high-quality, differentiated products to avoid the “price wars” caused by product homogenization, thereby fostering a healthy environment for growth and advancing the fields of minimally invasive and non-invasive procedures.

>>>>

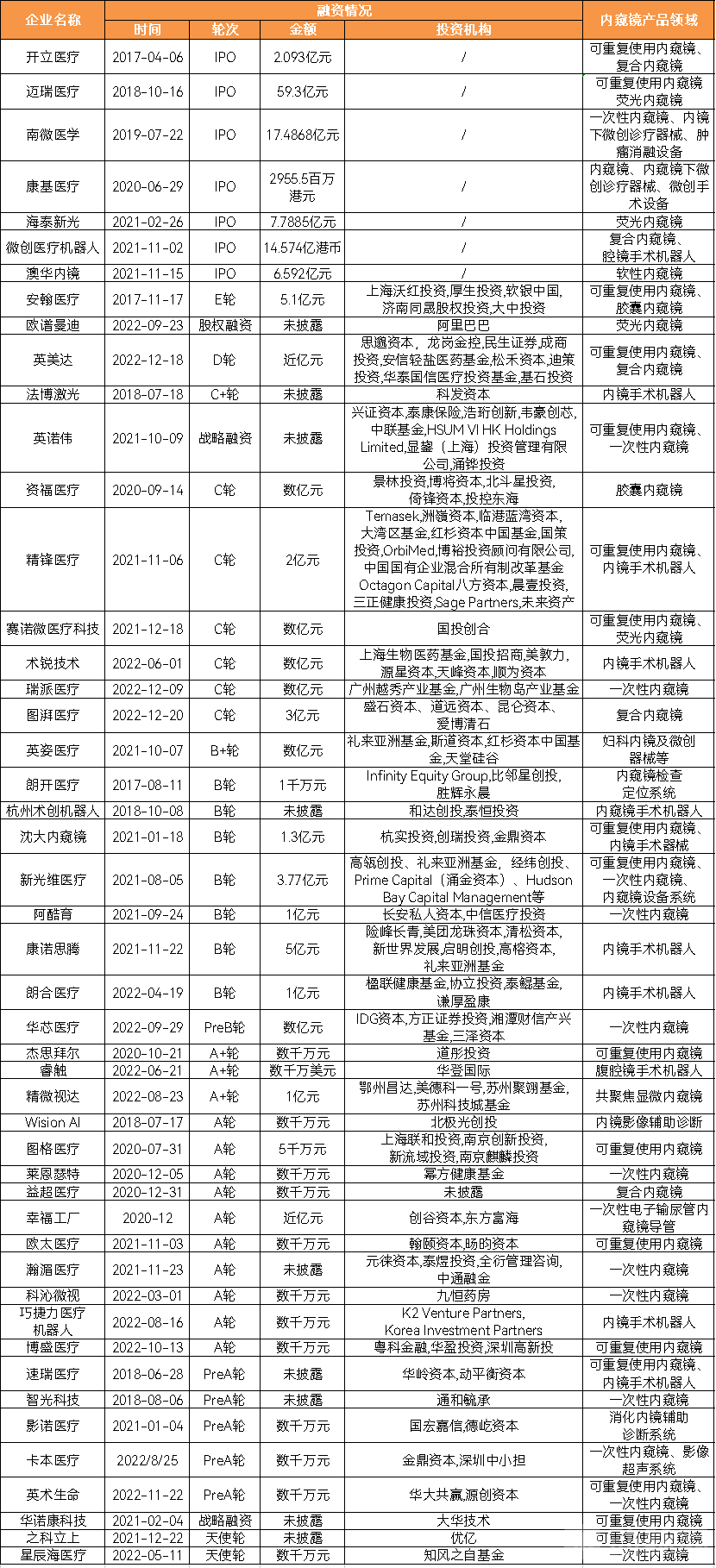

2021: Capital Activity in the Medical Endoscopy Sector Peaks as Leading Companies Emerge Across Sub-Segments

Financing frequency increased significantly in the past two years (2021 and 2022), with the total number of financing events nearly doubling the sum of the previous four years (2017–2020) and the total amount growing to nearly three times as much. In addition, the average size per financing round was substantial, ranging from tens of millions to hundreds of millions of yuan.

The reusable endoscope and associated medical device sector was the earliest to emerge, has reached the latest stages of financing, and exhibits the highest level of market maturity. Established companies such as Sonoscape Medical and Mindray Medical have long been publicly listed, while in the past three years, Kangji Medical, Haitai Xin Guang, and Aohua Endoscopy have also joined the ranks of listed enterprises.

Furthermore, companies focused on the research and development of minimally invasive surgical medical devices in niche sectors have also attracted favorable attention from investors. For instance, SinoMicro, which specializes in minimally invasive surgery, and Yingzi Medical, which focuses on minimally invasive gynecology, have both demonstrated strong fundraising performance.

Since their inception, single-use endoscopes have maintained strong revenue-generating potential. Following rapid development in recent years, the industry has seen the emergence of companies at later financing stages, such as Ruipai Medical and Huaxin Medical, with the competitive landscape beginning to take shape.

Meanwhile, companies engaged in the research and development of both reusable and disposable endoscopes have understandably attracted significant investor interest; for instance, Xin Guangwei successfully completed its Series A and Series B financing rounds consecutively within 2021.

In the earlier stages of technological innovation, capital has also placed significant emphasis on this track. For instance, Jingwei Shida, which specializes in confocal microscopy endoscopes, and Qiaojie Li Medical Robotics, which focuses on endoscopic surgical robots, both secured substantial early-stage financing ranging from tens of millions to hundreds of millions of yuan in 2022.

It is evident that in every niche segment of the endoscopy market, despite variations in overall financing rounds due to different starting times, capital has shown strong recognition and made significant investments, thereby driving rapid growth in each segment.

Review of Investment and Financing Activities in the Medical Endoscopy Industry from 2017 to 2022

Source: VBInsight (ranked by financing round; rounds of the same tier are sorted chronologically; only the most recent round is shown)

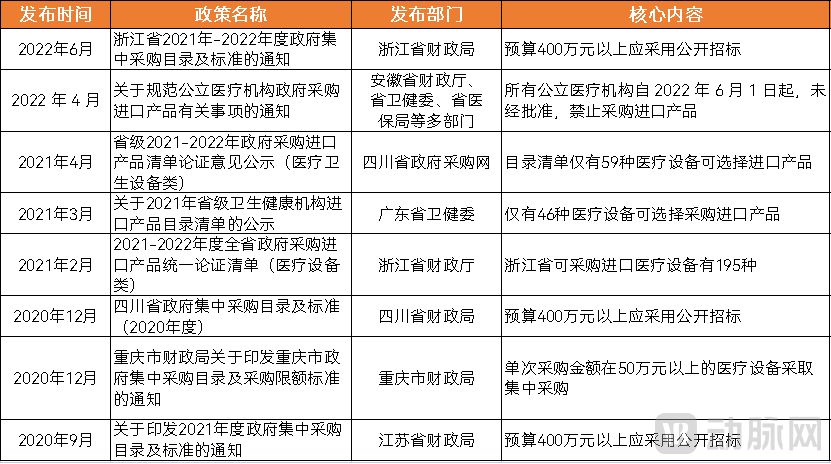

The State Increases Support for Domestic Substitution and Technological Innovation, While Local Governments Reduce the List of Imported Products

In recent years, as state-level support for the development of domestically produced medical endoscopes has continued to intensify, policies covering multiple dimensions—including R&D, regulatory approval, sales, and standardized use—have shown a trend toward progressive refinement and multidimensional expansion.

National-Level Policies Promoting the Development of Medical Endoscopes

Source: VBInsight

An analysis of the lists of imported products successively published by various regions since 2021 reveals that support for domestic substitution has been continuously strengthened, with explicit mandates to procure Chinese-made medical endoscopes.

Selected Local Policies Promoting the Development of Medical Endoscopes

Source: VBInsight

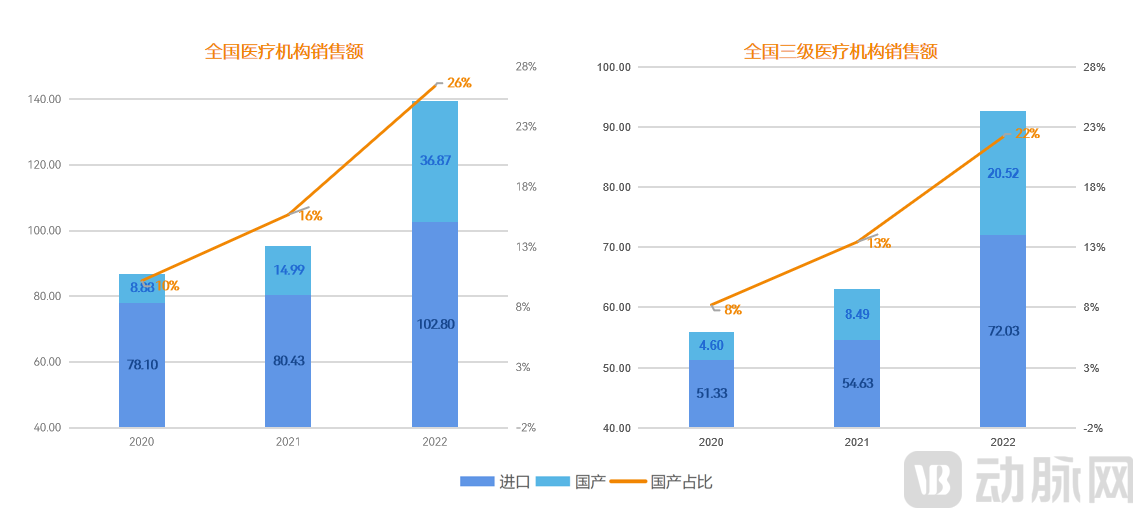

The Long-Standing Monopoly in the Domestic Market Has Been Broken, Accelerating the Pace of Import Substitution with Domestically Produced Alternatives

Breaking Monopolies with Quality: The Time Is Right for Domestic Substitution.Quality has served as a solid stepping stone for domestic enterprises, opening the door to clinical adoption and accelerating their growth with support from policies and other factors.

According to data from Zhongcheng Medical Device Research Institute, the total sales amount and market share of domestically produced medical endoscopes in healthcare institutions across China increased year by year from 2020 to 2022. The total sales revenue of domestically produced medical endoscopes reached nearly RMB 900 million in 2020 and grew to nearly RMB 3.7 billion in 2022; their market share also rose from 10% in 2020 to 26% in 2022.

2020–2022 Sales of Domestic and Imported Medical Endoscopes (RMB 100 million)

Source: Zhongcheng Medical Device Research Institute; Chart by VCBeat.

Furthermore, from 2020 to 2022, the total sales amount and market share of domestically produced medical endoscopes in tertiary healthcare institutions across China showed a year-on-year increase. The average annual growth rate was as high as 65%, surpassing the national sales growth rate. It is evident that domestic enterprises have broken the import monopoly through quality improvements, and the process of substituting imported medical endoscopes with domestically produced ones is progressing vigorously.

Product Strength and Market Capability Go Hand in Hand; Domestic Substitution Is Only a Matter of Time

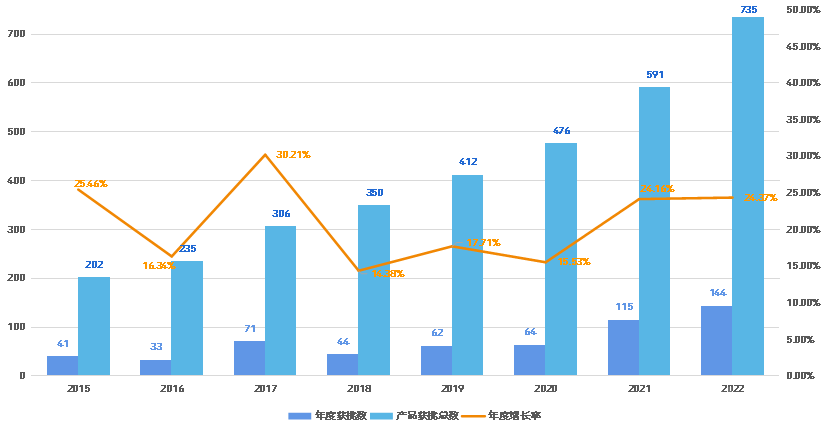

Product: The number of certified domestically produced medical endoscopes in China is growing rapidly.According to data from Zhongcheng Medical Device Research Institute, nearly 750 models of domestically produced reusable endoscopes have obtained NMPA medical device registration certificates, maintaining an annual growth rate of over 24% for two consecutive years.

Approval Status of Domestically Produced Reusable Endoscope Products, 2015–2022

Source: Zhongcheng Medical Device Research Institute; Graphic by VCBeat.

This signifies that domestically produced products can largely meet clinical demands in terms of quantity and variety, and also indicates that their quality has basically completed the “me too” phase, striving to enter the next “me better” stage.

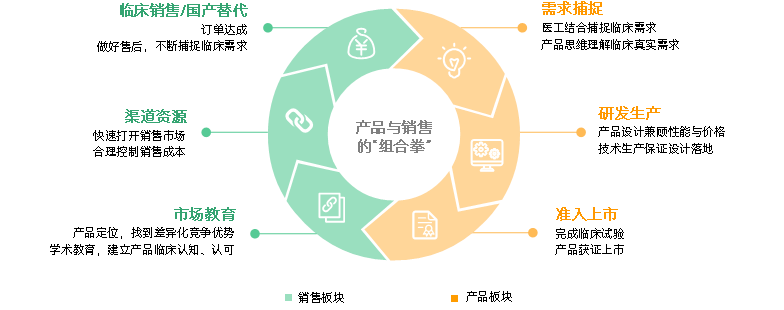

Sales: Market capabilities are increasingly valued.The path to domestic substitution is a systematic competitive process. Developing products that meet clinical needs is a necessary but insufficient condition for domestic substitution; it also requires professional and comprehensive marketing and sales strategies.

Domestic Substitution of Endoscopes Requires a “Combo Punch” of Product and Sales

In recent years, companies have begun to establish specialized marketing teams, striving to optimize product positioning and academic education to facilitate final sales achievement. Furthermore, after-sales service has received greater emphasis; beyond fulfilling corporate mandates to build a positive image in clinical settings, it serves as a valuable opportunity to capture clinical needs, providing essential real-world clinical insights to guide product research and development.

It is evident that, at the product level, domestic enterprises are continuously deepening their capture and understanding of clinical needs, while comprehensively enhancing their ability to translate these needs into products and solutions throughout the design and production processes. At the sales level, companies are beginning to focus on building professional market capabilities, leveraging a “combination strategy” of products and sales to strengthen their systemic competitiveness in the domestic substitution of reusable endoscopes. For Chinese enterprises that are simultaneously improving both product strength and market capabilities, achieving domestic substitution of reusable endoscopes in clinical practice is merely a matter of time.

Shouldering the Mission of “Exploration,” Focusing on Technological Breakthroughs and Integration

It is worth noting that in the field of reusable endoscopes, while domestic substitution remains the dominant trend, the industry has also witnessed numerous innovative breakthroughs.

Although China started later in the development of 4K endoscopes and 3D endoscopes, it has progressed rapidly, continuously narrowing the gap with overseas products. The capabilities of AI-assisted diagnostic systems for endoscopy are also at an international level, with comparable progress currently being made both domestically and abroad in this niche sector.

Taking 4K medical endoscopes as an example, this is currently a highly prominent niche segment within the medical endoscopy market, with companies such as Mindray Medical and Yuansai Medical having established their presence in this area. To deliver a genuine 4K experience in clinical practice, every component of the endoscopic system—including the light source, optical lenses, image sensors, data transmission, image processing, and display monitors—must meet 4K resolution standards. The failure to integrate any single link in this chain would hinder the realization of true 4K performance, making it a process that requires breakthroughs and effective synergy across multiple technological domains.

Encouragingly, in recent years, Chinese domestic enterprises have gradually broken through technological blockades and overcome critical “chokepoint” technologies, rapidly catching up with international standards. For instance, Yuansai Medical has leveraged its technical advantages in image processing to develop a full-chain 4K ultra-high-definition fluorescence endoscopic camera system that accurately reproduces colors. Its proprietary fluorescence management, combined with self-developed image enhancement algorithms, boundary segmentation, multi-mode image fusion, and color development algorithms, ensures clear visualization of tissues and lesions.

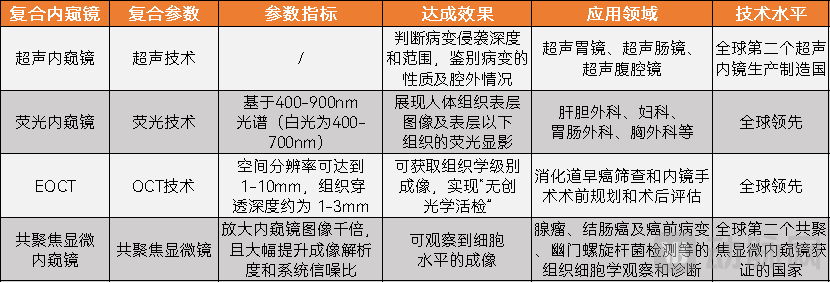

Hybrid endoscopes are showing strong development momentum, with multiple technologies leading globally.Composite endoscopes pose greater challenges for enterprises in terms of R&D and manufacturing compared to traditional reusable endoscopes.

China’s development of endoscopic ultrasound (EUS) started relatively late, but the momentum for domestic substitution is strong. In recent years, with the continuous improvement of R&D and manufacturing capabilities of Chinese enterprises, the industry has seen the first batch of domestically produced EUS systems obtain regulatory approval, breaking the monopoly of imported products. For example, Sonoscape’s radial array EUS scope EG-UR5 and curved linear array EUS scope EG-UC5T have successively received CE marking and NMPA device registration certificates, marking China as the second country in the world capable of producing EUS systems. Furthermore, in 2020, the company participated in the formulation of the People’s Republic of China Pharmaceutical Industry Standard YY/T 1676 “Endoscopic Ultrasound,” contributing to the independent R&D of high-end medical devices in China.

Analysis of the Application and Technical Level of Hybrid Endoscopes in Assisting Diagnosis

Furthermore, China’s technological capabilities in fluorescence endoscopy, EOCT, and confocal laser endomicroscopy are at the international forefront, granting it a certain degree of influence in the global market. Taking confocal laser endomicroscopy as an example, with Jingwei Shida’s independently developed and manufactured device—the first domestic confocal laser endomicroscope—obtaining NMPA registration approval in 2019, China became the second country in the world to have a certified confocal laser endomicroscope. This milestone signifies that China’s technical proficiency in laser confocal endomicroscopic imaging has reached an internationally leading level.

In the future, driven by the dual engines of “domestic substitution” and “technological innovation,” Chinese enterprises will steadily enhance their competitiveness and influence in the reusable endoscope market.

Disposable Endoscopes Gain Strong Foothold in Urology, with More Applications Yet to Be Explored

Domestic single-use endoscopes are developing rapidly, with a large number of products receiving approval.Around 2010, domestic companies specializing in single-use endoscopes began to emerge. According to incomplete statistics, as of February 14, 2023, nearly 80 domestically produced single-use endoscopes had received NMPA approval for market launch, whereas only a few imported single-use endoscopes were available.

Review of Approved Domestic Disposable Endoscopes

Source: Official Website of the National Medical Products Administration (as of February 14, 2023); Graphic by VCBeat.

In terms of approval timelines, 2022 marked the peak for approvals of domestically produced endoscopes in China, with at least 48 approved products accounting for over 60% of the total number of approvals. Furthermore, as of February 14, the number of approvals in 2023 had already reached nearly 30% of the full-year total for 2022, indicating that the number of certified single-use endoscope products is expected to experience explosive growth in 2023.

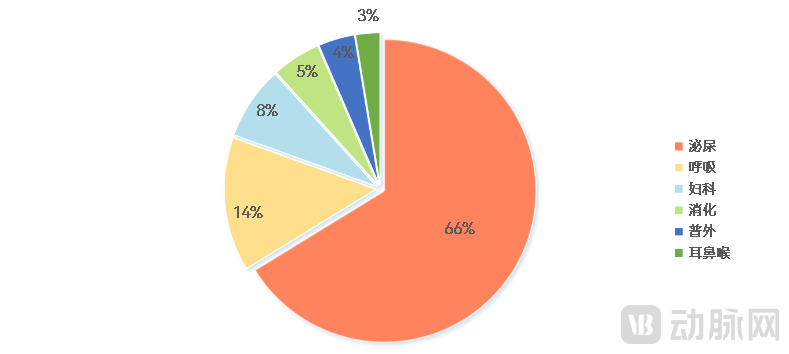

Commercialization pathways have been established, with more applications for single-use endoscopes awaiting exploration.The “essential” nature of single-use endoscopes in the field of urology is highly pronounced; consequently, many manufacturers of single-use endoscopes prioritize entering the urological application scenario with a precise market positioning centered on “infection prevention.”

Proportion of Approved Single-Use Endoscope Products by Application Scenario

Source: Official Website of the National Medical Products Administration (as of February 14, 2023); Graphic by VCBeat

However, the market positioning of “avoiding infection” alone is insufficient to explain the rapid development of disposable endoscopes in urology; this is also related to the existing reimbursement system.

On the one hand, traditional cystoscopy and ureteroscopy are relatively expensive, typically costing around RMB 1,000 to 2,000; whereas surgical procedures, such as those for kidney stones, cost approximately RMB 20,000. Therefore, the urology sector has greater capacity to pay for single-use consumables and offers a larger price differential to replace reusable devices. Furthermore, single-use endoscopes in urological applications can leverage existing medical insurance reimbursement catalogs, significantly accelerating the commercialization process.

As can be seen, disposable endoscopes have received a positive market response by entering through urological applications, marking a strong start to their commercialization. Building on this experience, more application scenarios will gradually streamline their commercialization processes once reimbursement issues are resolved.

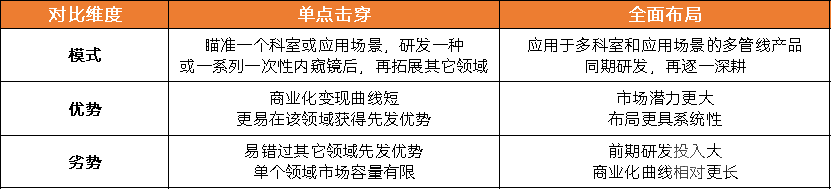

Balancing “single-point breakthrough” and “comprehensive layout” is crucial.Concentrating resources on a single domain appears to be a sound strategy for startups. Once a “blockbuster” product is launched and first-mover advantage is secured in that niche, the startup’s immediate “survival” concerns are effectively resolved. However, the company must then rapidly replicate this success across other domains to accelerate market coverage, thereby achieving more sustainable competitive advantages and broader growth prospects.

Comparison of the Advantages and Disadvantages Between Single-Point Breakthrough and Comprehensive Layout Models

A comprehensive layout from the outset places greater demands on a company’s financial strength and the speed at which it can achieve commercial validation; however, such companies may exhibit greater systematicity throughout the overall R&D phase, thereby laying the foundation for long-term, steady development.

For example, backed by a robust technical team and strong financial resources, Ruipai Medical implemented a comprehensive strategic layout from its inception, covering departments such as urology, gynecology, respiratory medicine, general surgery, and gastroenterology. Its product portfolio encompasses both flexible and rigid endoscopes, including major and minor endoscope types, providing clinicians with a total solution for single-use electronic endoscopy.

However, regardless of the development strategy chosen at inception, a common goal for disposable endoscope companies is to achieve comprehensive coverage across a wider range of application scenarios. Founders must strike a balance between deepening expertise in individual products and expanding the product pipeline, thereby leveraging their core competitive advantages to capture a larger market share.

Not as a replacement for reusable endoscopes, but to deliver superior clinical solutions through their respective unique characteristics

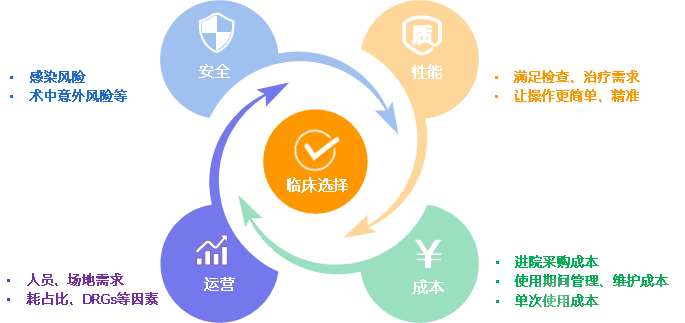

The selection of endoscopes for clinical use is a comprehensive decision involving multiple factors, including safety, product performance, operations, and cost.

Examples of Factors to Consider in the Clinical Selection of Endoscopes

Disposable endoscopes and reusable endoscopes will not have a substitutive relationship, nor is this the primary purpose behind the advent of disposable endoscopes. Instead, their combined use aims to provide better solutions for the diverse clinical application scenarios.

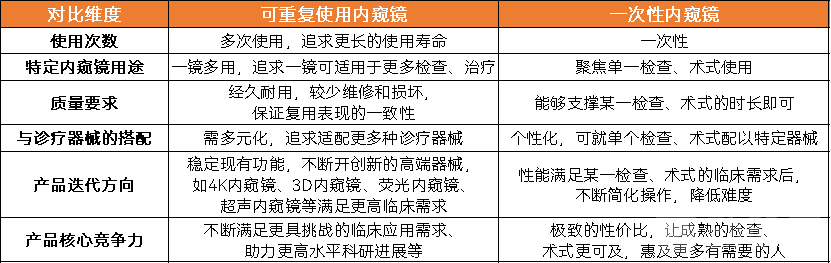

Leveraging their respective characteristics, they offer superior options for different application scenarios.Due to differences in materials, research and development, and manufacturing processes, reusable endoscopes and single-use endoscopes possess distinct characteristics to meet the clinical needs of various scenarios.

Comparison of Selected Performance Characteristics Between Reusable and Disposable Endoscopes

Our exploration of more and better treatment options must not cease; likewise, the path toward increased investment and high-end iteration for reusable endoscopes cannot stall. Meanwhile, it is crucial to ensure that the fruits of such advancements are accessible and affordable to those in need by reducing costs—a mission that may well be undertaken by single-use endoscopes.

Addressing pricing issues, focusing on specific surgical procedures, and mass production as the core competitive advantage

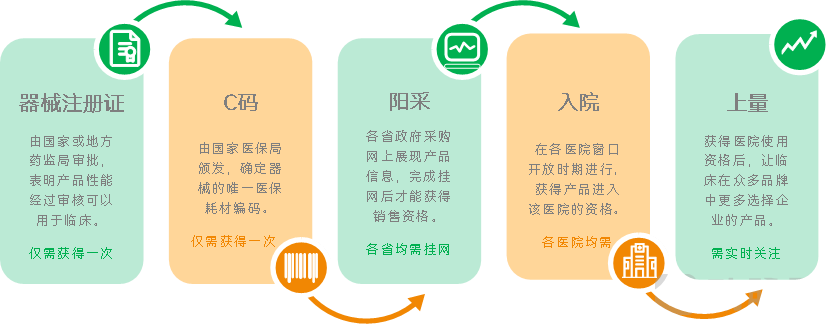

Resolving Fee Issues Requires Joint Efforts Across the IndustryAlthough dozens of disposable endoscopes have already obtained medical device certification from the National Medical Products Administration (NMPA), there remains a lengthy process of promotion and sales before they are widely adopted in clinical practice.

As a “novelty” in clinical practice, disposable endoscopes must obtain medical device registration certificates—akin to securing a “birth permit”—before they can achieve true market circulation with additional certifications such as the “birth certificate” and “ID card,” thereby extending the investment cycle for enterprises. Companies that are the first to navigate this process will gain a first-mover advantage, prioritizing the establishment of clinical usage habits and academic barriers.

Stages of Single-Use Endoscopes from Production to Clinical Use

Source: Huaxin Medical; Chart by VCBeat Institute

Currently, a significant portion of the sales market for domestically produced single-use endoscopes is overseas, partly due to the immature reimbursement environment in China. However, industry experts surveyed remain optimistic about the prospects of single-use endoscopes in certain application scenarios. They believe that once these devices fully demonstrate their clinical value, relevant policies will be optimized accordingly, a goal that requires collective efforts from the entire industry.

Positioned in the high-end manufacturing sector, mass production is its core competitive advantage.The key to the commercialization of single-use endoscopes lies in scaling up clinical adoption, where a large volume of market orders is crucial for amortizing costs, thereby testing manufacturers’ mass production capabilities. Our research reveals that more single-use endoscope companies are positioning themselves within the high-end manufacturing sector, with considerations of cost and mass production capability consistently integrated into the formulation of product strategies spanning R&D, market positioning, sales promotion, and other areas.

Huaxin Medical, for instance, has made substantial investments in product R&D by designing and commissioning an automated assembly line for endoscopes. This initiative has enabled an annual production capacity of 400,000 units while reducing the cost of single-use electronic bronchoscopes by nearly 30%, thereby better meeting demand across multiple clinical settings, including pulmonology, intensive care units (ICUs), and pediatrics.

In the future, on the starting line of meeting clinical demands, the core competitiveness of disposable endoscope companies will lie in their ability to secure larger clinical orders at lower costs and achieve automated mass production.

Overall, single-use endoscopes are currently experiencing strong momentum, gaining solid traction in urology by addressing the critical need for infection control. In the future, manufacturers of single-use endoscopes will need time to collectively foster a more favorable reimbursement environment in China. Meanwhile, these companies will leverage the high integration advantages of single-use endoscopes, focus on more specific surgical procedures, optimize cost control to the utmost, and enhance core competencies in mass production to lay a solid foundation for significant clinical adoption.

Medical Endoscopes and Associated Instruments and Equipment Jointly Drive the Development of Minimally Invasive Surgery

Performing endoscopic minimally invasive surgery requires not only the various types of medical endoscopes discussed in the previous two chapters, but also supporting minimally invasive surgical instruments and equipment. In recent years, the field of minimally invasive surgery has attracted numerous companies to enter this niche sector due to its substantial clinical demand, with these companies establishing comprehensive product portfolios that cover endoscopes, surgical instruments, and related equipment.

Development of a Full Product Line of Devices and Instruments to Drive the Advancement of Minimally Invasive Surgery.As device innovation continues, considerations such as safety validation and clinical-commercial barriers have led manufacturers to increasingly “proprietary” device interfaces, meaning that devices and instruments are paired one-to-one and can only interconnect within the same brand.

From a commercialization perspective, this trend offers certain advantages to companies that have established a full product portfolio for minimally invasive surgery, which is also why most product interfaces are not open to external parties. This trend is compelling capable companies focused on medical device R&D to expand their product layouts in equipment development.

However, beyond commercial considerations, such “commercial barriers” also offer certain advantages in terms of product performance and clinical outcomes. A fully integrated industry chain enables companies to unify planning and coordination from the initial stages of research and development, thereby better ensuring consistency between clinical performance and R&D testing results, and ultimately providing superior solutions for clinical practice.

For example, for this reason, Kangji Medical started with minimally invasive surgical instruments and consumables. After 18 years of development, it has become a comprehensive provider of minimally invasive surgical solutions, integrating endoscopes, surgical instruments, consumables, and equipment. Listed in 2020, the company now serves nearly 60 countries worldwide and more than 3,500 hospitals across China, including over 1,000 Grade III Class A hospitals.

Furthermore, many companies in the industry have adopted a comprehensive product-line strategy covering endoscopes, equipment, and instruments from the outset. These enterprises typically focus on deepening their expertise in a specific niche of minimally invasive surgery. For instance, Yingzi Medical, which specializes in women’s health, initially launched a series of products targeting the diagnosis of gynecological diseases as well as day-surgery and inpatient surgical treatment scenarios. Its aim is to increase the clinical adoption of electronic colposcopes, hysteroscopes, and endoscopic minimally invasive cold-knife technologies, thereby enhancing physicians’ diagnostic and surgical capabilities.

Driven by the co-evolution and innovation of endoscopes, endoscopic surgical instruments, and minimally invasive surgery-related equipment, an increasing number of surgical procedures are becoming minimally invasive, offering patients safer and more comfortable treatment.

Innovative Minimally Invasive Surgical Techniques Require a Solid Foundation of Product Technology

The clinical objectives of surgery remain fixed; however, continuous innovations in equipment and instruments are empowering clinicians with new surgical techniques that are safer and more precise, resulting in smaller incisions and easier postoperative recovery for patients.

The implementation of new surgical techniques requires not only endoscopes but also concurrent technological advancements and innovations in related supporting instruments.In procedures such as prostatectomy, traditional surgery demands sustained high-level concentration from surgeons, with outcomes heavily dependent on their experience and manual dexterity. The advent of the da Vinci Surgical System has significantly lowered the technical barriers for surgeons, shortened the learning curve, and enabled a broader range of physicians to perform these procedures through novel surgical approaches. This not only reduces the physical burden on surgeons but also enhances surgical precision.

According to research, purchased da Vinci surgical robots operate nearly 24/7 in healthcare institutions. On one hand, the high acquisition cost makes it difficult for hospitals to deploy multiple units; on the other hand, this underscores the substantial unmet clinical demand for surgical robots.

As the initial patent protections for the da Vinci Surgical System expire, numerous Chinese startups are entering the market, gradually introducing more affordable laparoscopic surgical robots to clinical practice; meanwhile, in the fields of natural orifice and pan-vascular robotic systems, there is an urgent need for domestically approved products to emerge.

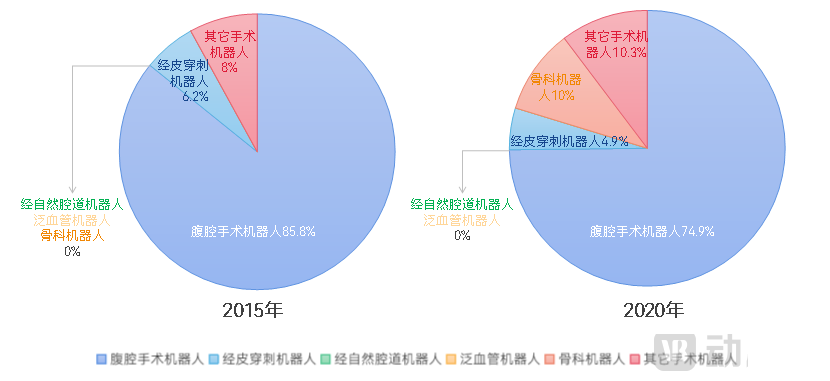

Proportion of Surgical Robots in Different Application Scenarios in China

Source: Kaiyuan Securities Research Institute; Chart by VCBeat.

According to forecasts by Kaiyuan Securities Research Institute, the market share of natural orifice surgical robots in China is expected to expand rapidly. The core technical barriers for natural orifice surgical robots include: surgical instruments must overcome the motion limitations imposed by rigid joint structures; and tool dimensions must be strictly controlled to achieve a balance between strength and flexibility within the narrow, tortuous natural cavities of the human body, thereby enabling smooth execution of diagnostic and therapeutic procedures such as biopsy and resection. Furthermore, the flexible robotic arms equipped on natural orifice surgical robots impose higher requirements on the interactivity between surgeons and the robotic system.

Notably, specialized technology companies have gradually emerged in this sector in China. For instance, Chokeli Medical Robotics, a healthcare technology company incubated by the University of Hong Kong, has developed breakthrough patented technology featuring a flexible robotic arm with a minimum diameter of just 2.5 mm. This device can pass through the working channels of conventional gastrointestinal and urethral endoscopes, thereby enabling flexible diagnostic and therapeutic procedures in narrow lumens such as the gastrointestinal tract and bladder.

It is believed that achieving regulatory approval for a pioneering product in fields such as natural orifice robotic surgery and pan-vascular robotics will confer a significant first-mover advantage.

Technological Innovation as the Foundation: The Emergence of New Surgical Procedures Through Close Medical-Engineering CollaborationThe emergence of a new surgical procedure requires a “two-way engagement” between the clinical and corporate sectors. Academic advancements made by physicians during clinical practice, or even just an initial idea, need to be communicated through unobstructed channels to relevant enterprises. These companies then evaluate the feasibility based on their R&D capabilities and ultimately realize the new surgical procedure through technological and product innovation.

Effective “integration of medicine and engineering” should span the entire product lifecycle, encompassing product design and R&D, testing and trials at various stages, and post-market clinical application. By continuously addressing identified clinical pain points through synchronized technological innovation and development in the fields of medical equipment and devices, this process serves as the “cradle” for the emergence of new surgical procedures.

Overall, the advent of endoscopy has opened the door to minimally invasive surgery, yet there remains a vast array of clinical scenarios for “minimally invasive” approaches that are yet to be fully explored. This calls for close collaboration between industry and clinical practice. On one hand, companies must continuously refine product innovation, design, and manufacturing capabilities, enhancing their ability to translate clinical needs into tangible products. On the other hand, the clinical community should actively share academic advancements and engage in robust dialogue with industry partners. Through this “two-way engagement,” an increasing number of surgical procedures will evolve into minimally invasive techniques that are safer for patients and more convenient for surgeons.

Clinical Needs Guide the Development Direction of Endoscopy: Focusing on Surgical Procedures

Exploring the “Optimal Solution” for the Synergistic Development of Reusable and Disposable Endoscopes

Chinese Endoscope Manufacturers Join Forces to Cultivate a Healthy Ecosystem and Drive Advancements in Minimally Invasive Procedures

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Chapter 1: Capital Support and Policy Protection Drive Diversification of Domestically Produced Medical Endoscopes

1.1 Capital Activity in the Medical Endoscope Sector Peaked in 2021, with Leading Companies Emerging in Each Sub-Segment

1.2 The state increases support for domestic substitution and technological innovation, while local governments reduce the list of imported products

1.3 Clinical Needs Drive the Gradual Diversification of Medical Endoscopes

Chapter 2: The Time is Ripe for Domestic Substitution of Reusable Endoscopes, with Parallel Technological Innovation

2.1 Long-term Domestic Monopoly Broken, Accelerating Import Substitution with Chinese-made Products

2.2 With Product Strength and Market Capability Advancing in Tandem, Domestic Substitution Is Only a Matter of Time

2.3 Shouldering the Mission of “Exploration,” Focusing on Technological Breakthroughs and Integration

Chapter 3: Disposable Endoscopes Focus on Specific Surgical Procedures, with Mass Production as the Core Competitiveness

3.1 Single-Use Endoscopes Gain Strong Foothold in Urology, with More Application Scenarios Yet to Be Explored

3.2 Not as a replacement for reusable endoscopes, but to provide superior clinical solutions based on their respective characteristics

3.3 Resolve Reimbursement Issues, Focus on Established Procedures, and Make Mass Production the Core Competitiveness

Chapter 4: Devices and Instruments Jointly Drive the Development of Minimally Invasive Surgery

4.1 Endoscopy Enriches Early Screening Methods, Opens the Door to the Minimally Invasive Era, and Leaves Significant Unmet Demand

4.2 Medical Endoscopes and Associated Instruments and Equipment Jointly Drive the Development of Minimally Invasive Surgery

4.3 Innovating Minimally Invasive Surgical Techniques Requires a Solid Foundation of Product Technology

Chapter 5 Future Trends

5.1 Clinical Needs Guide the Development Direction of Endoscopy: Focusing on Surgical Procedures

5.2 Exploring the “Optimal Solution” for the Coordinated Development of Reusable and Disposable Endoscopes

5.3 Chinese Endoscope Manufacturers Join Forces to Cultivate a Healthy Ecosystem and Drive Advancements in Minimally Invasive Procedures

Chapter 6 Corporate Case Studies

6.1 Huaxin Medical: Establishing a Foothold with Disposable Endoscopes, Saving More Lives Through Innovative Technology

6.2 Ruipai Medical – Full Range of Disposable Endoscopes, Providing High-Quality Total Solutions for Clinical Practice

6.3 Yingzi Medical – Leading the New Era of Cold Knife Technology, Safeguarding Women’s Health with Innovative Minimally Invasive Diagnostic and Therapeutic Techniques

6.4 Qiaojie Medical Robotics – Focusing on Natural Orifice Surgical Robots, Developing a 2.5mm Diameter Flexible Robotic Arm

6.5 Kangji Medical – Based in China, Providing Comprehensive Solutions for Minimally Invasive Surgery Worldwide

6.6 Yuansai Medical – A Provider of Innovative Integrated Minimally Invasive Diagnosis and Treatment Solutions Based on Digital Medical Technologies

6.7 Jingwei Shida – Building the “Chinese Brand” of Confocal Microendoscopy Technology to Facilitate Early Diagnosis and Treatment of Tumors

6.8 Sonoscape – Domestically Developed Technology, Providing High-End Diagnostic and Therapeutic Product Solutions for Early Diagnosis and Treatment Worldwide

Please scan the QR code to add our assistant and obtain the full report. If you have already added the assistant, please proactively request the report.

Special Acknowledgments (in the order of industry research):

Ms. Liu Haitao, Investment Director at Legend Capital; Ms. Li Jing, General Manager of Ruipai Medical; Dr. Zhou Zhenhua, Founder and Chairman of Huaxin Medical; Ms. Gao Ming, Deputy General Manager and Director of BD and Marketing at Yingzi Medical; Professor Guo Jiawei, Co-founder of Qiaojie Li Medical Robotics; Mr. Huang Shangmin, Senior System Manager at Qiaojie Li Medical Robotics; Dr. Chen Dong, Co-founder, General Manager, and Chief Technology Officer of New Optical Dimension Medical; Mr. Zhang Jindi, Founder of SinoMicro; Mr. Yue Jiqiang, Head of R&D at Kangji Medical; Ms. Wang Juan, General Manager of Yuansai Medical; and Mr. Wang Zixian, Marketing Director of Yuansai Medical.