2023 Insight Report on Oral Healthcare Services: Digital Transformation Accelerates Driven by Supply-Demand Synergy

Meituan

E-commerce Platform Service Provider

Small Mouth, Big Health.

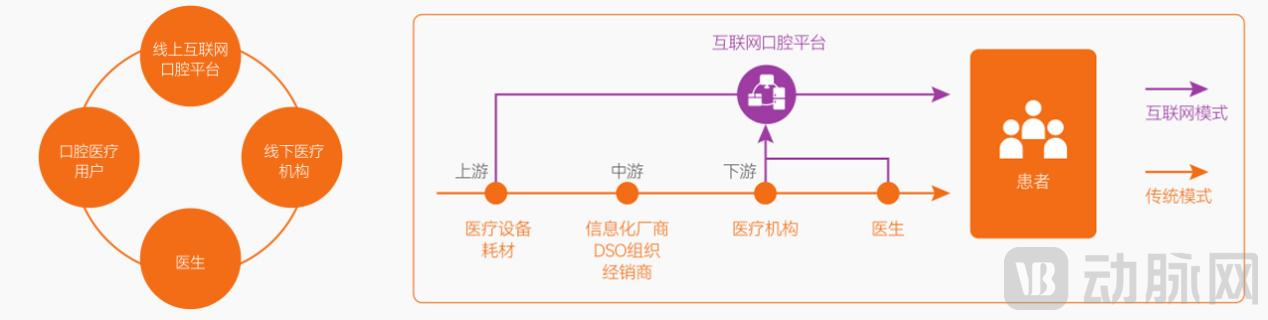

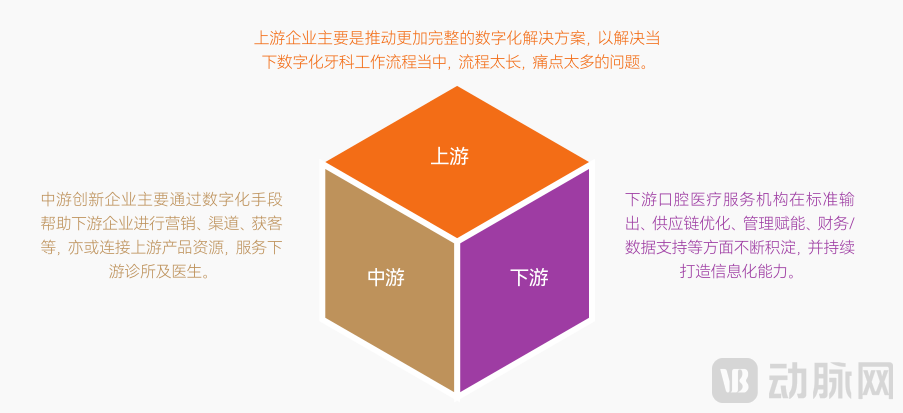

As a highly marketized vertical segment within the healthcare industry, the oral care industry encompasses an upstream sector dominated by manufacturers of consumables and equipment R&D; a midstream sector comprising distributors of dental medical equipment and consumables, providers of informational software, and Dental Support Organizations (DSOs); and a downstream sector consisting of various medical service institutions, internet platform operators, and consumers.

Amid the prevailing "appearance economy," China's dental industry is entering a new phase of rapid development, with the market size projected to reach RMB 300 billion by 2025. Both evolving consumer demands and advancements in new technologies and business models on the supply side are jointly driving the growth and transformation of the dental healthcare services sector.

In light of this, VCBeat and Meituan Healthcare jointly released the “2023 Insights Report on Dental Medical Services,” aiming to provide a comprehensive and systematic analysis of the current state of the dental services industry. By examining the development characteristics of dental consumers and dental institutions through emerging internet channels, as well as the underlying changes occurring across the industry chain, the report offers judgments and recommendations for the future development of the sector, thereby facilitating the continued advancement of the dental medical services industry.

Access the full report:

Method 1: Follow the “Meituan Hemei Merchant Home” official account and reply with the keyword “Oral Report” to obtain it.

Method 2: Scan the QR code to add the assistant and send a private message to obtain it.

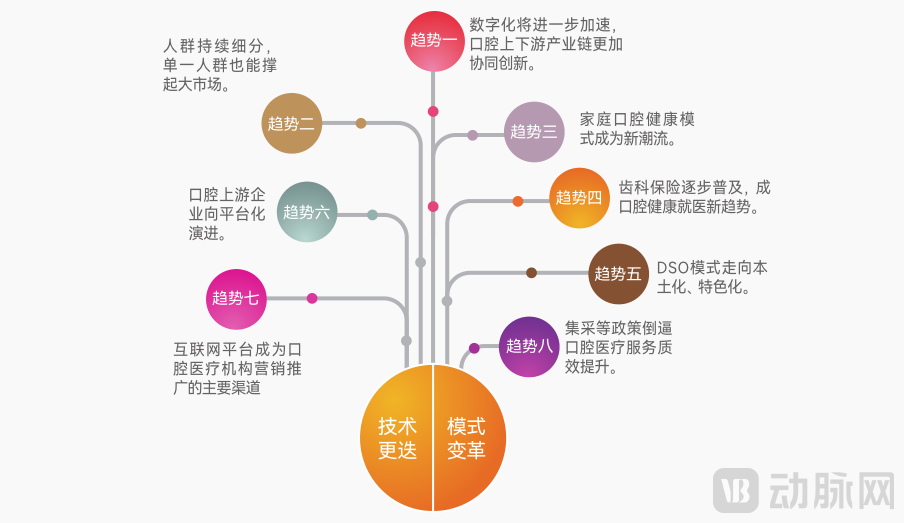

Core Trend Insights:

Trend 1: Digitalization will further accelerate, fostering more collaborative innovation across the upstream and downstream segments of the dental industry chain.

Trend 2: Continued Segmentation of Dental Care Consumers, with Single Demographics Capable of Sustaining Large Markets.

Trend 3: The Rise of Home Oral Health Models, Serving as a Key Channel for Primary Oral Care.

Trend 4: Dental insurance is gradually becoming widespread, emerging as a new trend in seeking oral healthcare.

Trend 5: The DSO Model Becomes a Key Evolutionary Direction for Dental Chains.

Trend 6: The upstream dental sector is heating up, with companies evolving toward platform-based models.

Trend 7: Internet platforms have become the primary channel for marketing and promotion by dental medical institutions.

Trend 8: The implementation of policies such as centralized procurement will compel the dental care service sector to accelerate improvements in quality and efficiency.

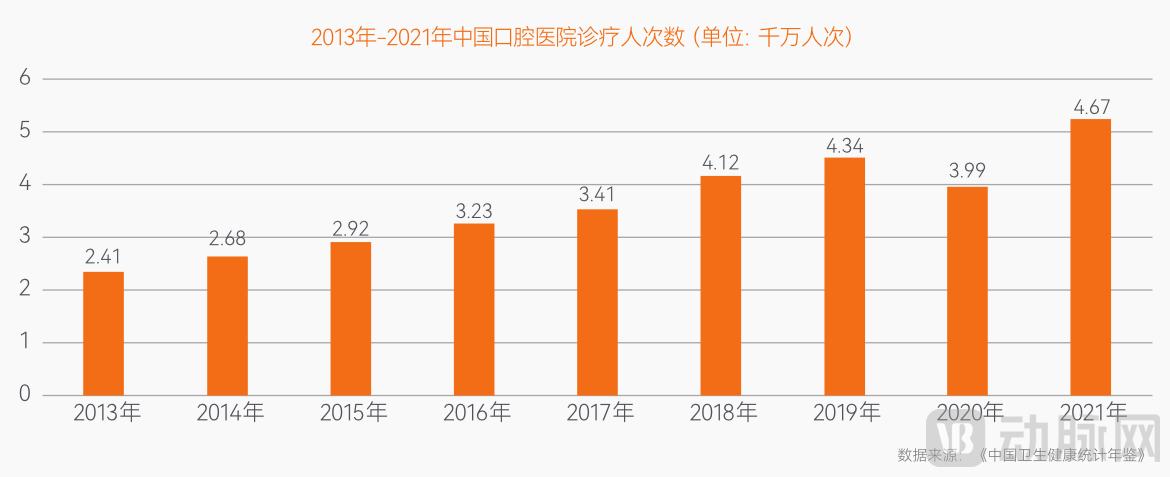

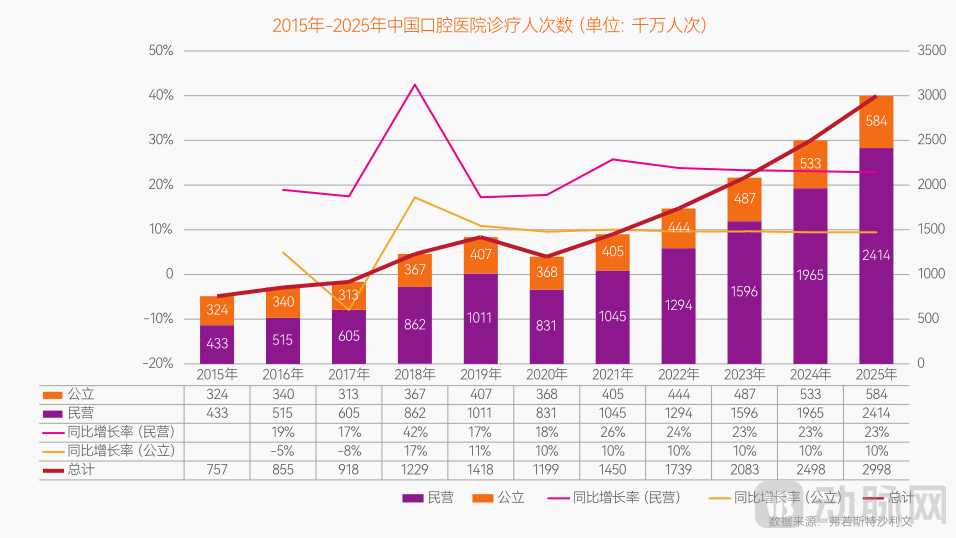

Current Status of the Demand Side in Oral Healthcare: Growing Attention to Oral Health Issues Has Led to a Year-on-Year Increase in Patient Visits, Exceeding 46 Million.

The "2021 National Health Insight Report" shows that among the top 10 health issues affecting Chinese residents in 2020, oral health problems ranked fifth, rising by one position from 2019. Oral health has become an issue that cannot be ignored in China.

Driven by the growing prevalence of oral diseases and heightened health awareness, the number of outpatient and emergency visits for dental care at hospitals has steadily increased. According to data published in the China Health Statistics Yearbook, the annual number of patient visits to specialized stomatological hospitals in China rose from less than 25 million in 2013 to nearly 45 million in 2019. It is estimated that this figure reached approximately 46.77 million in 2021.

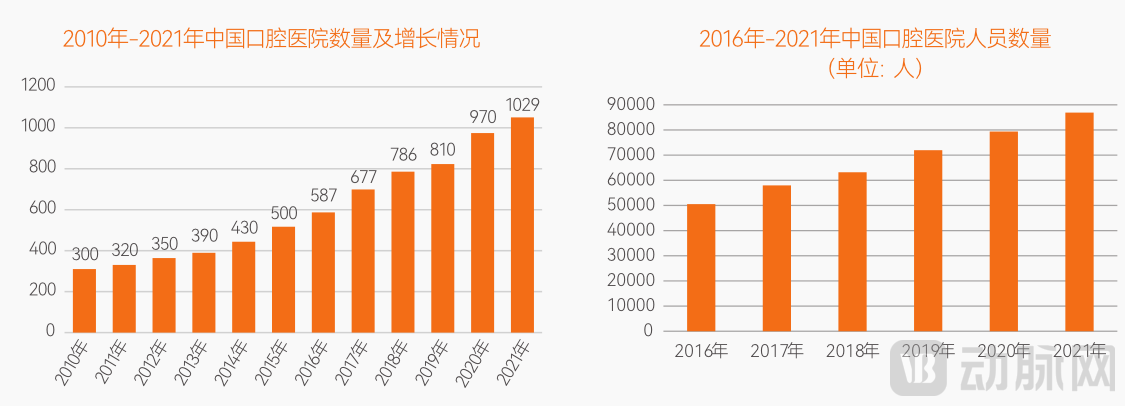

Current Status of the Supply Side in Oral Healthcare: The number of oral healthcare institutions and personnel has been increasing year by year, with supply capacity in a period of steady growth.

Driven by national policies and steady economic development, the number of dental healthcare institutions and dental professionals in China has grown steadily, leading to a continuous enhancement of dental care supply capacity.

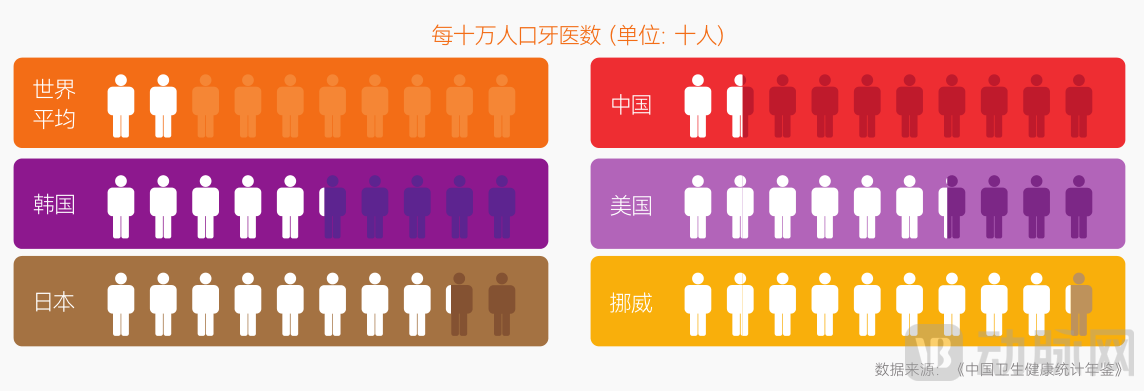

From the perspective of dental hospitals, data from the China Health Statistics Yearbook shows that the number of dental hospitals in China has maintained an overall growth trend, increasing from 300 in 2010 to 1,029 in 2021, with a compound annual growth rate (CAGR) of approximately 12%. From the perspective of medical personnel, the number of staff in China’s dental hospitals (including licensed assistant physicians, licensed physicians, and registered nurses) steadily increased from 2016 to 2021, reaching 85,900 in 2021. However, on the other hand, the supply of dentists in China remains insufficient. In 2020, there were only 15.7 dentists per 100,000 people in China, far lower than in countries such as the United States, South Korea, and Japan.

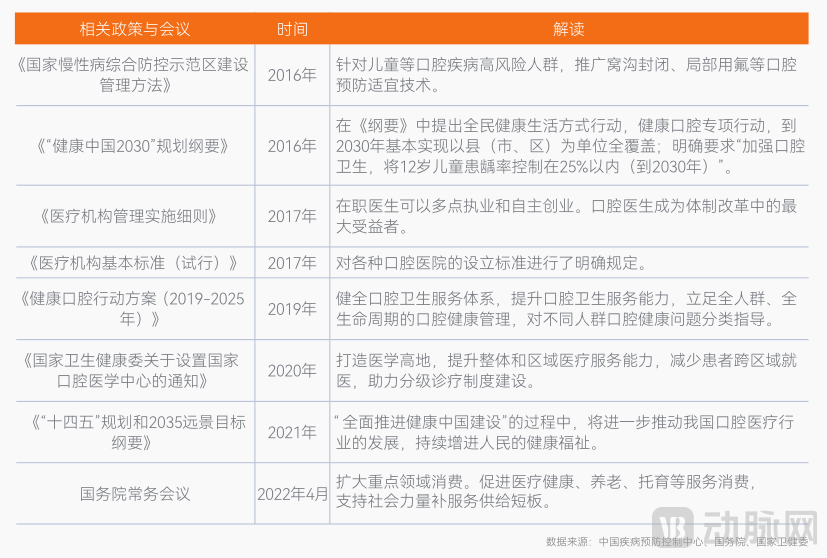

Current Status of Dental Healthcare Policy: Continuous Policy Intensification, with Oral Health Shifting from “Treatment” to “Prevention.”

Policy support for the oral health industry is being further strengthened. Since 2016, China has introduced multiple policies covering various aspects, including system development, industry standards, regulation of oral healthcare institutions, physician practice, patient education, and oral disease prevention and control. We have conducted a more in-depth analysis of the factors influencing policies related to oral healthcare services. Policies on the supply side primarily focus on establishing standards for the operational models, practice formats, and service specifications of medical institutions and physicians, thereby ensuring the quality of oral healthcare services. Policies on the demand side emphasize long-term planning for residents' oral health, with the core message indicating that such planning will shift from "treatment" toward "prevention."

Current Status of the Dental Care Services Market: Supply and Demand Jointly Propel the Industry Toward a RMB 300 Billion Market.

Driven by the combined forces of supply and demand, China's oral healthcare services market is ushering in new opportunities for growth. Based on terminal consumption data and Frost & Sullivan's report, we find that the market size of China's oral healthcare services reached RMB 145 billion in 2021, maintaining an average annual growth rate of 20%. It is projected to reach RMB 300 billion by 2025, indicating broad market prospects.

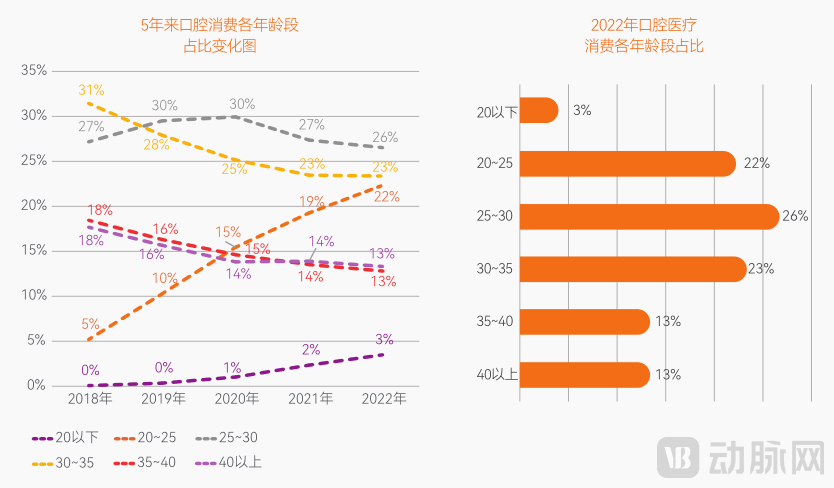

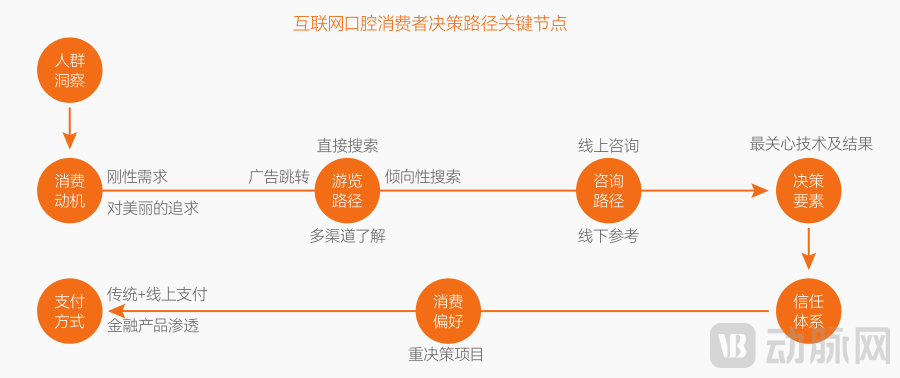

Consumer Profile of Dental Medical Services ①: The consumer base for dental medical services is continuing to skew younger, with individuals aged 20 to 35 constituting the core demographic.

Age Structure:Survey data indicates that young adults aged 20 to 35 constitute the core consumer group for dental medical services, accounting for approximately 70% of the market. Furthermore, the dental care consumer base is expanding year by year, with growing oral health awareness among younger generations. Consequently, meeting the dental healthcare consumption habits of young people, particularly Generation Z (those born between 1995 and 2010), has become a key consideration for dental healthcare providers in the near future.

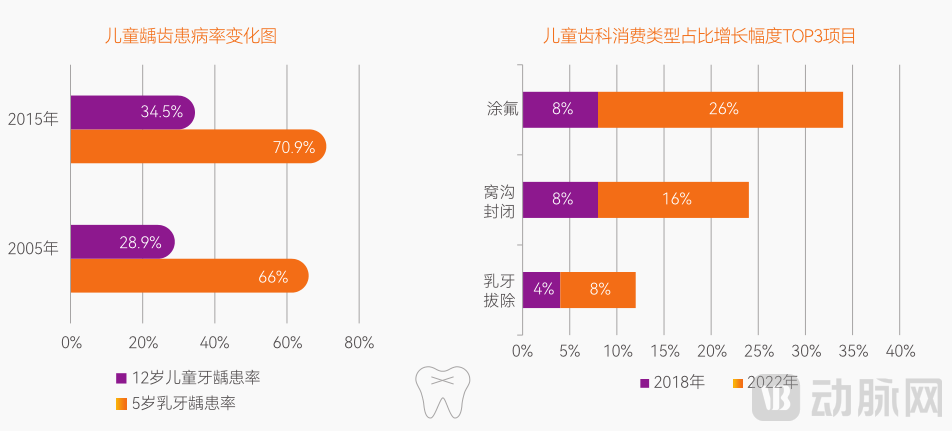

Oral Healthcare Consumer Profile ②: Significant Rise in Pediatric Caries Prevalence, with the Fastest Growth in Caries Prevention Services

Population Segmentation:Data from the "Report on the Fourth National Epidemiological Survey of Oral Health" shows that from 2005 to 2015, the prevalence of dental caries in children showed an upward trend, with an increase of more than 5%. In terms of population birth, the current number of children in China has reached 247 million, accounting for 17.5% of the total national population, nearly 20%. Based on the large population of children with dental caries, survey data shows that in the past five years, anti-caries projects such as fluoride application and pit and fissure sealing have increased by 18% and 8%, respectively, in the total consumption of children's dental projects.

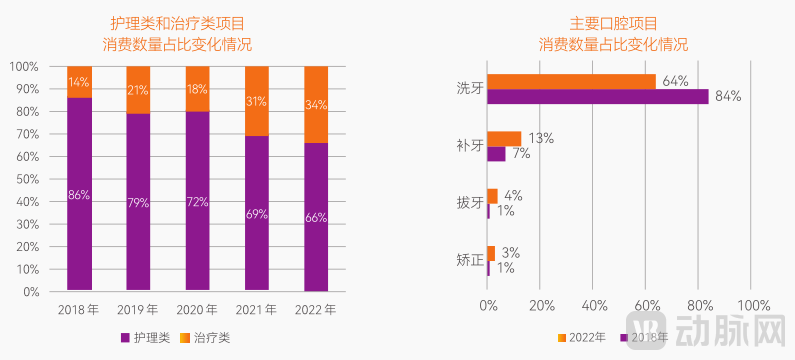

Consumer Profile ③: Dental Cleaning Becomes the Most Purchased Online Service, with Rapid Growth in Spending on Fillings and Extractions.

Charge Items:Survey data shows that dental scaling is currently the most purchased item in online consumption, but it has shown an overall decline between 2018 and 2022. In addition, restorative and extraction procedures have continued to rise, while increased consumption of therapeutic products is attributed to improved product offerings and standardized supply.

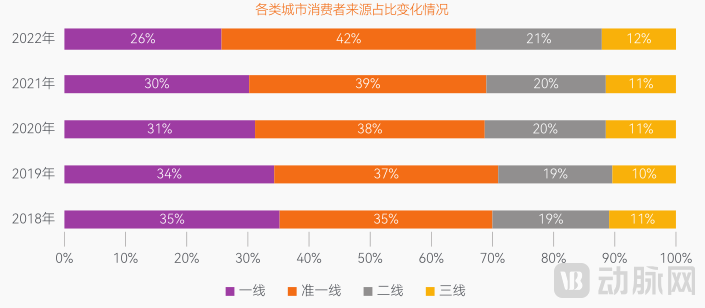

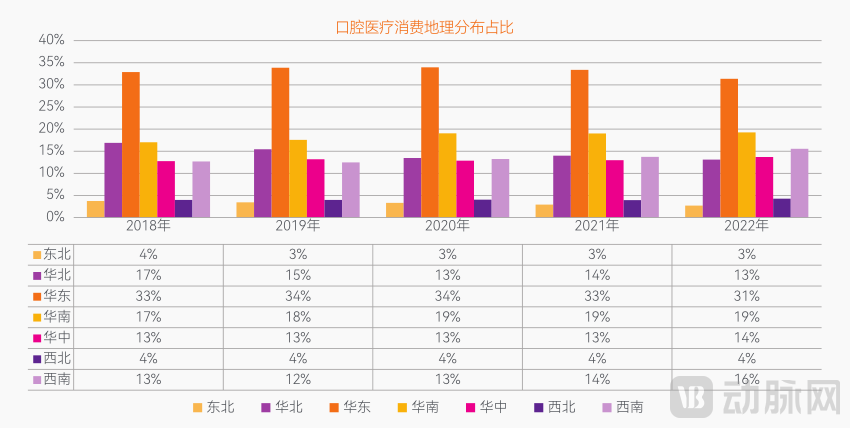

Consumer Profile ④: By city tier, new first-tier cities are the primary battleground for dental consumption; by region, the Southwest is experiencing rapid growth.

Geographic Distribution:Survey data indicates that with rising economic levels, dental healthcare consumption is gradually expanding to more cities, propelling quasi-first-tier cities to become the main force in dental consumption. Among these, the economically developed East China region accounts for the highest proportion, while the Southwest region is experiencing rapid growth. Notably, in 2022, the share of consumption in Beijing and Shanghai, two first-tier cities, declined significantly due to the impact of the pandemic.

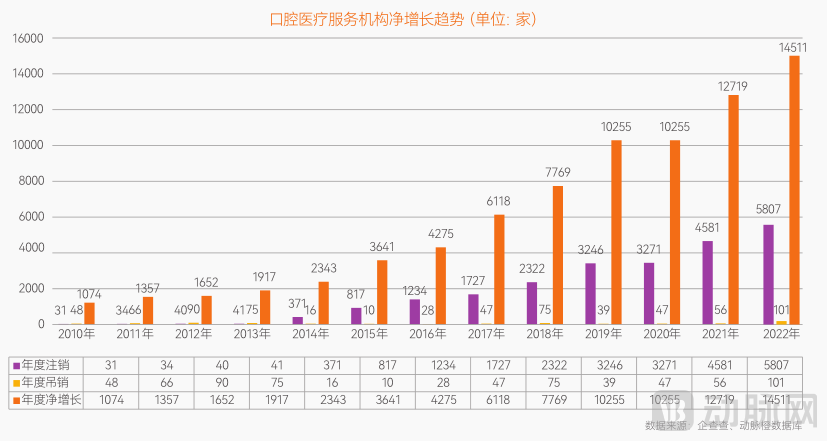

Supply-Side Status: Annual Cancellations Hit Record High, Dental Service Providers Undergo Market Consolidation.

In a market environment characterized by survival of the fittest, integrated data from Qichacha and the VCBeat Orange Database show that while the number of dental medical service institutions deregistered in 2022 reached a record high, the annual net growth peaked at 14,511 entities.

Profile of Dental Healthcare Institutions (I): Leading Enterprises Pursue Chain Operations and Scale, Starting from First-Tier Cities.

The chain business model of private specialized dental hospitals offers consumers more convenient, efficient, and personalized services than public hospitals, gaining favor in the mid-to-high-end market. It is expected that with the rise in per capita disposable income in first- and second-tier cities, more expansion opportunities will be created for mid-to-high-end chain private specialized dental hospitals in the future.

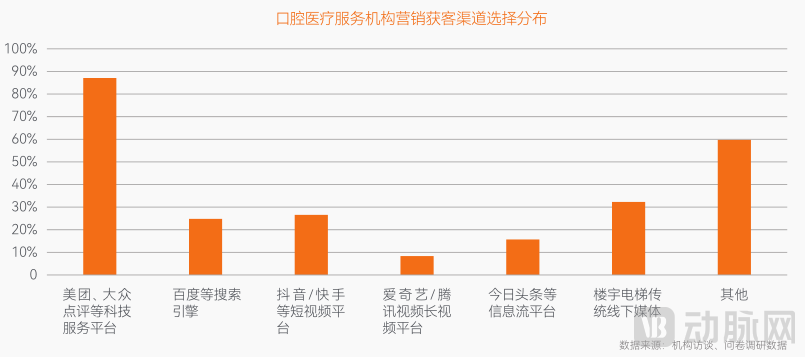

Profile of Dental Healthcare Institutions (II): The Vast Majority of Institutions Favor Online Channels for Marketing and Customer Acquisition, with Meituan and Dianping Being the Most Widely Used.

Surveys indicate that the vast majority of institutions favor online channels for marketing and customer acquisition, including tech platforms such as Meituan and Dianping, search engines like Baidu, and short-video platforms such as Kuaishou. Among these, tech platforms like Meituan and Dianping account for the highest proportion at 87.09%, while traditional offline channels, such as elevator advertisements in office buildings, account for 32.28%.

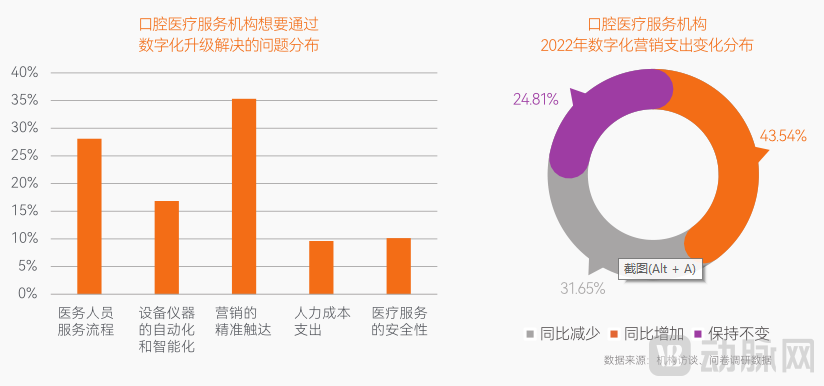

Profile of Dental Healthcare Institutions (III): 35% of institutions seek to leverage digitalization for precise marketing outreach, while 44% increased their digital marketing spending in 2022.

Surveyed institutions believe that digitalization primarily addresses issues such as precise marketing outreach, service workflows for medical personnel, automation and intelligence of medical equipment, safety of medical services, and labor cost expenditures. Among these, 35.32% of the institutions aim to leverage digitalization to achieve precise marketing outreach.

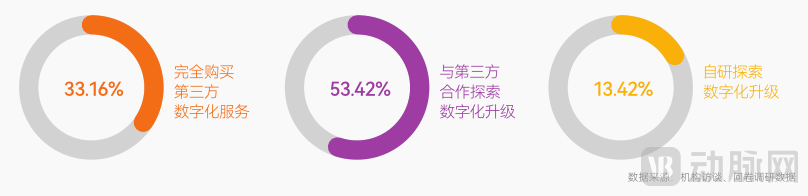

Profile of Dental Healthcare Institutions (IV): Over Half of Enterprises Seek Third-Party Collaboration to Explore Digital Transformation

According to the survey, 33.16% of institutions opt to fully purchase third-party digital services in their digital transformation journey, 53.42% collaborate with third parties to explore digital upgrades, and 13.42% pursue in-house development for digital transformation.

Platform Service Provider Status: Acting as a Bridge to Enhance Supply-Demand Matching Efficiency.

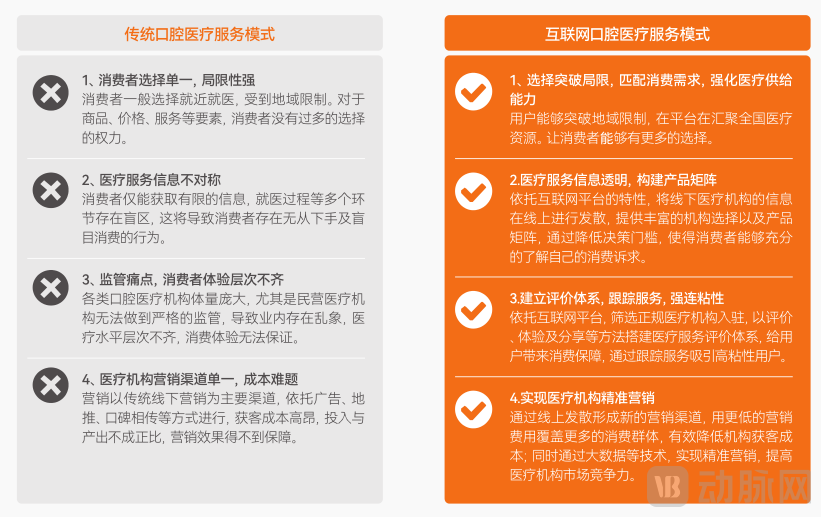

Traditional Dental Care Model: Healthcare institutions directly serve dental care consumers by providing them with medical services.

Internet-Based Dental Care Model: Integrating offline business opportunities with the internet, making the internet a platform for offline transactions. The core of the Internet-Based Dental Care Model is to use an online dental care platform as a bridge, connecting medical institutions and dental care users (primarily patients). B-side: By offering price discounts, providing information, and appointment services, it disseminates information about offline medical institutions online, thereby expanding their customer acquisition channels. C-side: It provides patients with more choices and richer product information.

Role of Platform Service Providers: Facilitating the Digital Transformation of Dental Care Services.

Internet Dental Platform: An internet-based ecosystem formed by reshaping and transforming the value chains of the industry chain and its various stakeholders, leveraging internet technologies and ecosystems. Internet dental platforms fully utilize the optimizing and integrating role of the internet in the allocation of production factors, achieving deep integration between the internet and the dental services industry.

Meituan Healthcare: Building an information and transaction platform for both supply and demand sides, delivering bilateral value.

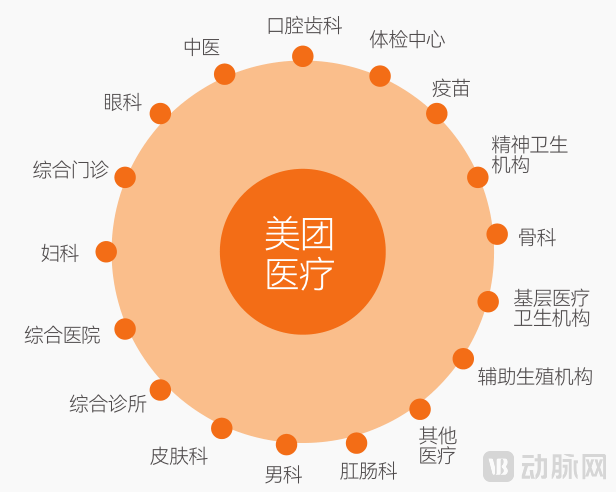

Meituan’s Consumer Healthcare segment was launched in 2019, providing users with information-driven decision support and service selection spanning health screening, preventive care, and management of minor ailments, covering 36 sectors including dentistry, medical check-ups, vaccination, Traditional Chinese Medicine (TCM), and ophthalmology.

Consumer Side: Offers a wide selection of stores and products, online doctor consultation services, and diverse purchasing scenarios such as group buying, pre-orders, appointments, and team purchases, providing users with convenient, professional, and guaranteed options for consumption decisions and medical consultations.

Merchant Platform: Centered on localized consumption, Meituan provides digital services—including LBS-based precision marketing, IT solutions, and operational support—to help merchants boost sales, accumulate online brand equity, and acquire customers through online marketing.

The Essential Business Platform for Building Brand Influence.

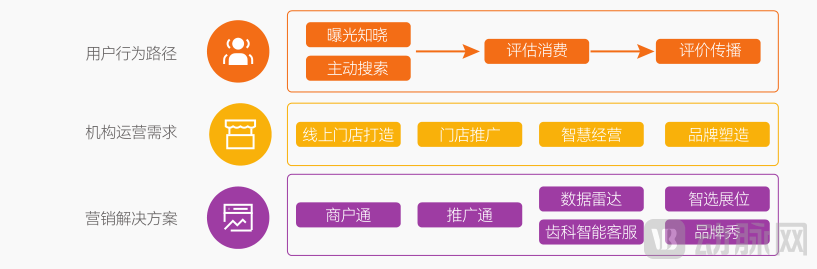

Meituan Healthcare: Six Digital Marketing Solutions to Boost Institutional Operational Efficiency.

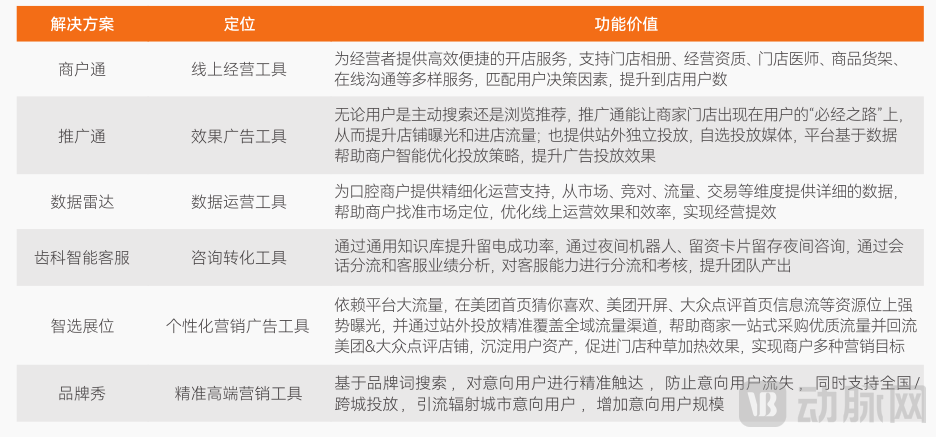

Meituan Healthcare offers a suite of digital marketing solutions—including Merchant Connect, Promotion Connect, Data Radar, Dental Intelligent Customer Service, Smart Select Ad Placements, and Brand Showcase—tailored to the operational needs of healthcare institutions. These solutions cover the entire lifecycle of institutional operations, empowering sustainable long-term growth.

Trend 1: Digitalization will further accelerate, fostering more collaborative innovation across the upstream and downstream segments of the oral care industry chain.

Currently, digitalization has become a consensus among innovative enterprises across the upstream and downstream sectors of China’s oral care industry, gradually driving internal digital transformation within these companies. For instance, internet platform providers and health informatics companies are actively attempting to integrate fragmented data from oral healthcare services to guide or empower downstream service institutions.

Trend 2: Dental insurance is gradually becoming widespread, emerging as a new trend in seeking oral healthcare.

In dental healthcare consumption, most medical services are primarily paid out-of-pocket, and complex dental treatments such as dental implants are considered high-cost expenses. The introduction of commercial insurance into dental care, which helps patients reduce treatment costs, undoubtedly meets the current substantial market demand.

Trend 3: Internet platforms have become the primary channel for dental institutions to operate and deliver services.

The pandemic has accelerated the digital transformation of dental healthcare. During this period, internet platforms emerged as the primary channel for marketing and promotion by dental institutions, making customer acquisition through online channels a prevailing trend. This shift is driven by the fact that digitalization represents the future direction of the dental industry; the pandemic hastened the emergence of demands such as online consultations, prompting numerous dental institutions to actively pursue digital transformation to ensure continuity in patient follow-up care.

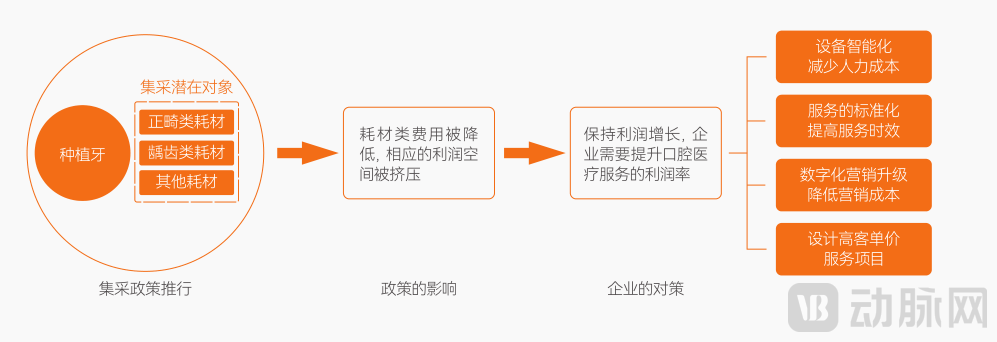

Trend 4: The implementation of policies such as centralized procurement will compel the dental healthcare service sector to accelerate improvements in quality and efficiency.

Centralized procurement of high-value dental consumables is an inevitable trend. Dental implants have already been included in the centralized procurement program, and more consumables are expected to be covered in the future. The implementation of centralized procurement will significantly reduce the cost of consumables. To maintain profit growth, companies must increase service margins by enhancing the quality and efficiency of their services through digital technological innovation, management innovation, and product innovation.

Table of Contents for the "2023 Oral Healthcare Services Insight Report"

Chapter 1: Current Status of the Oral Healthcare Services Market

1.1 Overview of Dental Healthcare

1.2 Current Status of the Demand Side in Oral Healthcare

1.3 Current Status of the Supply Side in Oral Healthcare

1.4 Current Status of Dental Healthcare Policies

1.5 Current Status of the Oral Healthcare Services Market (①-②)

Chapter 2: Insights into Consumer Demand for Oral Healthcare Services

2.1 Consumer Profile of Dental Medical Services (①-⑦)

2.2 Summary (①-②)

Chapter 3: Digital Transformation in the Supply of Oral Healthcare Services

3.1 Current Status of the Supply Side (①-③)

3.2 Profile of Dental Medical Institutions (①-⑨)

3.3 Domestic Cases of Digitalization Layout

3.4 The Digitalization Journey of Leading U.S. Enterprises

3.5 The Value of Digital Dentistry

3.6 Summary

Chapter 4: Platform Service Providers Facilitate the Digital Transformation of Dental Practice Operations

4.1 Status as a Platform Service Provider

4.2 Role of Platform Service Providers

4.3 Meituan Healthcare Case Study

Chapter 5: Future Trends in Oral Healthcare Services

5.1 Brief Overview of Development Trends for the Next Three Years

5.2 Industry Trend Insights (①-⑧)