The Future and Emerging Opportunities of Aesthetic Photonics Amid Exponential Growth

Fumeilei Medical

R&D Developer of Medical Aesthetic Devices

Amid the strong tailwinds of the “light medical aesthetics” trend, the energy-based device sector in medical aesthetics has experienced explosive growth.

According to research data from the Huajing Industry Research Institute, the global number of non-surgical aesthetic medicine procedures reached 23.59 million in 2020, with energy-based devices accounting for 17.32% of the total.

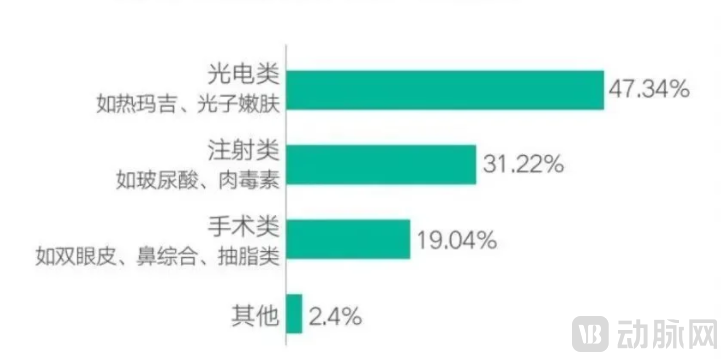

Focusing on the domestic market, photoelectric medical aesthetics has experienced explosive growth. The latest data released by So-Young indicates that in 2022, among the medical aesthetic procedures most favored or most desired by consumers in China, 47.34% of surveyed users identified photoelectric treatments as their top choice.

▲ Proportions of Aesthetic Medical Procedures Most Loved/Most Desired by Consumers Source: SoYoung

▲ Proportions of Aesthetic Medical Procedures Most Loved/Most Desired by Consumers Source: SoYoung

It is evident that photoelectric medical aesthetics is on the verge of an explosive boom.

However, alongside the booming growth of the optoelectronic medical aesthetics industry, numerous irregularities have emerged. To promote healthy and orderly development within this sector, the Chinese government has introduced a series of policies. For instance, the Guiding Opinions on Further Strengthening the Comprehensive Regulatory System for Medical Aesthetics specifically address existing irregularities in the medical aesthetics industry by calling for standardized medical aesthetic services, regulated production, distribution, and use of pharmaceuticals and medical devices, and controlled dissemination of medical aesthetic advertisements. These measures create a more favorable market environment, opening up broader opportunities for compliant products.

On the supply side, a cohort of high-quality innovative enterprises in the field of medical aesthetic optoelectronics is currently emerging in China, such as Suzhou Fumeilei Medical Technology, which recently secured Pre-A series financing. The rise of domestic manufacturers of high-end equipment will gradually reverse the import monopoly in China’s optoelectronic medical aesthetics sector, thereby creating new possibilities and opportunities.

How Will the Photoelectric Medical Aesthetics Industry Evolve Under the Combined Forces of Supply and Demand? What Are the Emerging Trends? VCBeat Will Provide a Detailed Analysis Below.

This article is an excerpt from the “White Paper on Energy-Based Devices in Medical Aesthetics.” To gain insights into the industry landscape, development logic, and potential opportunities for energy-based devices in medical aesthetics, please scan the QR code to contact our assistant and request the full report.

01 Rising Penetration Rates Will Gradually Popularize Light- and Energy-Based Aesthetic Procedures

Currently, public acceptance of medical aesthetics has significantly increased, with preferences shifting toward natural-looking results, thereby driving the continuous rise in the penetration rate of energy-based medical aesthetic treatments.

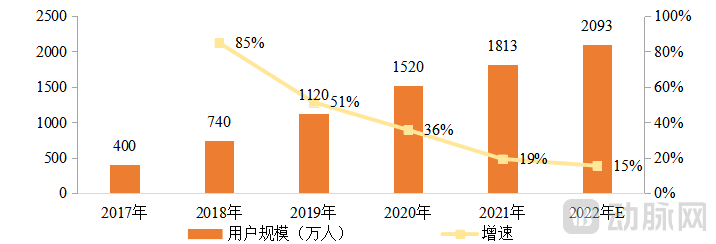

Looking at the industry's development, when private medical enterprises began to enter the plastic surgery and aesthetic medicine market in 1997, market awareness was relatively low. In recent years, however, medical aesthetic procedures such as European-style double eyelids, high nasal bridges, V-shaped faces, hyaluronic acid fillers, and skin boosters have significantly advanced market education, propelling China's medical aesthetics industry into a phase of rapid growth. According to statistics, the number of medical aesthetics consumers in China grew from 4 million in 2017 to 19.13 million in 2021, and is projected to exceed 20 million in 2022.

Notably, aesthetic preferences among medical aesthetics consumers in China are maturing, shifting from the earlier trend of standardized, “assembly-line” surgical faces toward natural beauty that aligns with individual styles, with greater attention paid to side effects and long-term sequelae. Compared with surgical and injectable procedures, non-invasive energy-based devices (EBD) treatments carry virtually no risk of disfigurement due to procedural failure, yield more natural-looking results, and can significantly boost consumer confidence. It is reasonable to anticipate that the penetration rate of EBD-based medical aesthetics treatments will continue to rise in the future.

▲User Base Size and Growth Trends in China's Medical Aesthetics Industry, 2017–2022

Source: Qianzhan Industry Research Institute; compiled by VCBeat

The trend of market penetration into lower-tier cities is becoming increasingly evident, with cost-effective and user-friendly projects gaining widespread adoption first.Currently, the primary consumer group for medical aesthetics in China consists of post-95s in first-tier cities with a monthly income of RMB 20,000–50,000. Penetration remains insufficient in second- and third-tier cities, with medical aesthetics users accounting for less than 0.5% of the population in third-tier cities and below, indicating substantial room for expansion.

From 2018 to 2020, the number of newly registered enterprises related to “medical aesthetics” in lower-tier markets remained above 500 annually, marking a significant increase compared with 2016 and substantially improving the accessibility of China’s medical aesthetics industry in these markets. Meanwhile, enhanced information coverage in lower-tier markets has strengthened the industry’s influence and rapidly raised consumer awareness of medical aesthetic services.

In 2016, So-Young launched its “market penetration into lower-tier cities” strategy, expanding into third- and fourth-tier cities. Currently, So-Young’s platform services cover more than 350 cities, with significant user growth observed in these lower-tier markets. Furthermore, internet platforms such as Pinduoduo, Douyin, and Kuaishou have allocated more resources to the medical aesthetics category. The proliferation of short-form videos and live-streaming content related to medical aesthetics has greatly stimulated the rise of aesthetic awareness among users in lower-tier markets.

There is a gap in income levels between residents in lower-tier markets and those in developed regions. Aesthetic medicine consumers in these markets are more price-sensitive; thus, light- and energy-based procedures, which offer high cost-effectiveness and safety, are more readily accepted and tried by this demographic. Furthermore, current technologies for light- and energy-based aesthetic devices are relatively mature, posing lower overall risks and requiring less stringent operator expertise. Given the severe shortage of qualified aesthetic medicine professionals in China, such procedures are easier to promote, thereby achieving higher market penetration.

Intensified market competition creates the possibility for lower end-user prices, while standardized industry development is transforming photoelectric treatments into mainstream daily maintenance procedures.

On the one hand, as domestically produced devices in the optoelectronic field rapidly emerge in China over the coming years, and excellent innovative foreign products continue to enter the Chinese market, intense competition will ultimately compel aesthetic medicine device manufacturers to adjust their pricing strategies. This may even involve a shift from a high-consumables model to a low-consumables model, thereby creating room for downstream aesthetic clinics to reduce service prices. Currently, significant price reductions have already been observed for many optoelectronic treatments on the market. For instance, since 2016, the end-user price of IPL (Intense Pulsed Light) treatments has dropped by nearly two-thirds, while Thermolift has decreased from its initial launch price of tens of thousands of yuan per session to just several thousand yuan per session.

On the other hand, against the backdrop of increasingly stringent regulations in China’s medical aesthetics sector and growing consumer sophistication, operational strategies within the beauty industry will gradually shift from marketing-driven inducement to a consumer-demand-led model. Service package designs will align more closely with the actual efficacy of products, and, provided pricing remains reasonable, energy-based device treatments will ultimately evolve into mainstream, routine maintenance procedures.

02 Energy-Based Medical Aesthetic Devices Are in a Window of Opportunity for Domestic Substitution

It is precisely against the backdrop of the rapid development of China’s photoelectric medical aesthetics industry that energy-based aesthetic devices are in a window of opportunity for domestic substitution.

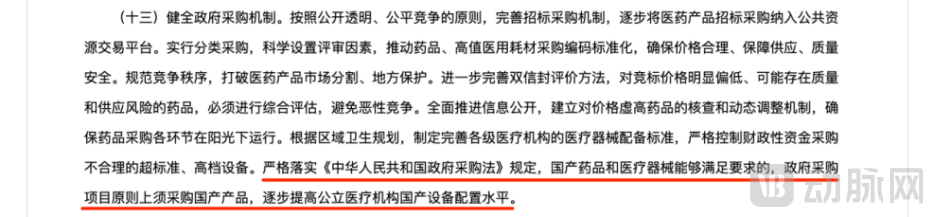

First, it benefits from policy-driven initiatives.For instance, according to the "2022 Departmental Budget of the National Health Commission" released by the National Health Commission, the budget allocation for public hospitals under health expenditures further decreased, dropping by 9.0% compared to 2021. Consequently, for general public hospitals, the budget for medical equipment procurement is typically the first to be cut following a reduction in fiscal appropriations. It is foreseeable that as national fiscal tightening continues, public hospitals will exercise greater caution in purchasing imported medical devices in the future, and domestically produced equipment with more competitive pricing and higher cost-effectiveness is likely to be favored.

Furthermore, policies explicitly restrict the procurement of imported medical devices and encourage the purchase of domestically produced medical equipment. According to Article 13 of the "Guiding Opinions of the General Office of the State Council on Promoting the Healthy Development of the Pharmaceutical Industry" (Guo Ban Fa [2016] No. 11), government procurement projects shall, in principle, procure domestic products if domestically produced drugs and medical devices can meet the requirements, thereby gradually improving the configuration level of domestic equipment in public medical institutions.

Second, domestic high-end brands are on the rise.It is worth noting that imported photoelectric medical aesthetic devices account for as high as 80% of the market share, reflecting substantial technical barriers. The photoelectric medical aesthetic device industry is a technology-intensive sector characterized by multidisciplinary integration and exceptionally high technical barriers.

Currently, nearly all mid-to-high-end photoelectric medical aesthetic devices used by licensed medical aesthetic institutions in China are imported products. Although the overall market share of imported manufacturers in China’s compliant market has declined slightly in recent years, it remains above 80%, constituting a near-monopoly. This is due to the relative scarcity of specialized talent in the field of photoelectric medical aesthetics, particularly for high-end equipment, and the fact that core technologies are still in a catch-up phase.

Amid vast market substitution opportunities, an increasing number of enterprises, capital investors, and R&D and management talents are entering the field of photoelectric medical aesthetic devices. In China, there is a large number of small-scale photoelectric medical aesthetic companies characterized by severe product homogenization, low technological value-added, and consequently low market concentration. Furthermore, these products generally rank low in terms of safety and efficacy. Facing market consolidation and substitution opportunities, more enterprises, capital investors, and R&D and management professionals are flocking to the photoelectric medical aesthetics sector.

For example, as a new entrant in the field of medical aesthetic optoelectronic devices, Fumeilei Medical was established in Suzhou in September 2021. Committed to the research and development and manufacturing of high-end optoelectronic equipment, the company aims to become a global leader in medical aesthetic optoelectronic devices. Its flagship product, the ForePico multi-wavelength picosecond laser therapeutic apparatus, is about to enter the clinical trial phase.

▲ForePico Product Image Source: Fumeilei Medical Official Account

▲ForePico Product Image Source: Fumeilei Medical Official Account

In the foreseeable future, as mid-to-high-end domestic medical aesthetic optoelectronic devices are successively launched, Chinese-made equipment will rapidly capture market share through superior product quality and relative price competitiveness, thereby achieving import substitution.

03 The Future of Photoelectric Medical Aesthetics and Greater Possibilities

High-energy photoelectric treatments carry safety risks, underscoring the importance of post-procedure care and repair. Due to the high energy density of photoelectric energy-based devices, they can easily cause epidermal damage, leading to side effects such as hyperpigmentation, erythema, bruising, and crusting. This is particularly relevant for individuals with sensitive skin, who are more susceptible to external light and thermal stimuli. They may experience immediate symptoms such as redness, swelling, and burning sensations, and face a higher risk of subsequent skin barrier impairment following the procedure.

Furthermore, as the visualization systems for energy-based devices remain immature, truly personalized treatment is not yet achievable. Variations in individual skin types can easily lead to adverse effects such as subcutaneous scarring and nerve damage due to improper operation, often necessitating subsequent corrective procedures for affected patients.

Therefore,Post-procedure care and repair are essential for photoelectric treatments, and the combination of pharmaceuticals and medical devices is clinically recognized as an effective approach.On the one hand, it can effectively prevent adverse reactions, alleviate immediate postoperative discomfort, and enhance clinical acceptance.

Taking laser therapy as an example, persistent erythema is a predictable outcome following treatment with most laser devices. The erythema typically lasts for 24–72 hours, causing psychological stress and mild burning discomfort for patients. Post-procedure application of specific topical vasoconstrictive agents can effectively shorten the duration of erythema or even prevent its occurrence, thereby facilitating the broader clinical adoption of laser therapies.

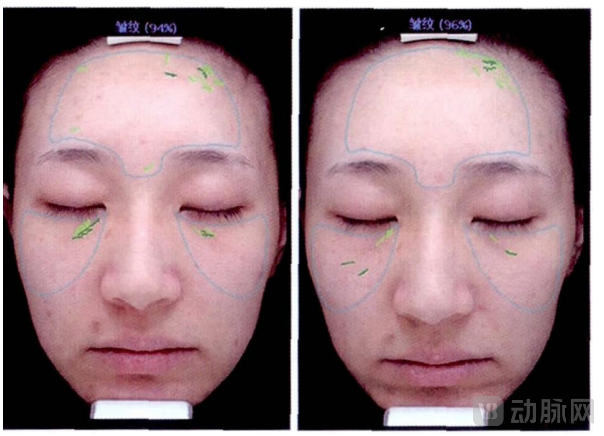

▲Visia analysis images before treatment (left) and after treatment (right)

Botulinum toxin was sprayed around the left eye. As shown in the post-treatment image on the right, wrinkle improvement was more pronounced in the left eye compared to the right.

Source: Chinese Journal of Aesthetic Medicine, compiled by VCBeat

On the other hand, the combination of pharmaceuticals and medical devices can enhance therapeutic efficacy and improve patient satisfaction. Following photoelectric therapy, the skin barrier is disrupted, leading to increased transdermal absorption of drugs. This allows therapeutic agents to reach the target treatment layer directly, thereby reinforcing treatment outcomes.

However,High Barriers to the Industrialization of Combined Drug-Device Products: China Remains in a Very Early Stage, Offering Significant Growth Potential。

First, due to the differing R&D logics of pharmaceuticals and medical devices, their effective integration still faces multiple challenges, including market demand analysis, industrial convergence, and business model experimentation, and thus remains in an exploratory stage.

Overall, as the development of medical aesthetic drugs by domestic Chinese enterprises remains in its early stages and lacks industrialization experience, identifying high-quality medical aesthetic drugs presents a significant challenge. In summary, the drug-device combination model is an inevitable path for photoelectric equipment to break through their current market capitalization scale, although it is still in its early stages.

For medical device manufacturers, proactively entering the pharmaceutical sector and exploring combination product approaches can effectively strengthen competitive barriers and create greater growth potential.

Undoubtedly, under the sweeping tide of minimally invasive aesthetic medicine, the photoelectric aesthetics sector will continue to unfold even more compelling narratives.