China's NHC Eases Regulations on High-End Imaging Equipment, Paving the Way for Market Expansion

GE Hangwei

Medical Device R&D and Manufacturer

United Imaging

High-end Medical Device Developer

Neusoft

Comprehensive Solution Provider for Clinical Diagnosis and Treatment

In 2020, the emergence of the COVID-19 pandemic disrupted the steady growth trajectory of large-scale medical equipment. Focusing solely on CT scanners, over 7,000 new units were installed in hospitals within a single year, nearly doubling the figure from the same period in the previous year.

Beneath the market’s surge lies growing concern, particularly for manufacturers whose primary revenue stems from low-end CT scanners. Data from MedTech Study Club shows that approximately 4,000 CT units were sold in 2019, with 75% being mid- to low-end models featuring fewer than 64 slices. In 2020, despite a substantial increase in sales volume of mid- to low-end CT scanners amid the pandemic, their share of total sales declined to 64%. The years 2021 and 2022 proved even more challenging, marked by declines in both absolute sales volume and market share for mid- to low-end CT scanners, signaling signs of fatigue in this segment.

Recent Major Policy"Notice on the Catalogue for the Administration of Licensing for the Allocation of Large Medical Equipment (2023)"The release has further accelerated the polarization of the medical device market.

In the new edition of the configuration catalog, procurement restrictions on CT scanners with 64 slices or more and MR systems of 1.5T or higher have been removed; as long as the price does not exceed RMB 30 million, any medical institution may directly procure medical equipment not listed in the catalog without needing to apply for approval from provincial or municipal authorities. In other words, the unmet demand for mid-to-high-end imaging equipment at some secondary and tertiary hospitals, previously constrained by configuration permits, will be released over the next few years.

How Should Large Medical Equipment Companies Respond to the New Policy? VCBeat Discusses with Industry Experts, Analyzing Policy Changes to Explore Market Response Strategies.

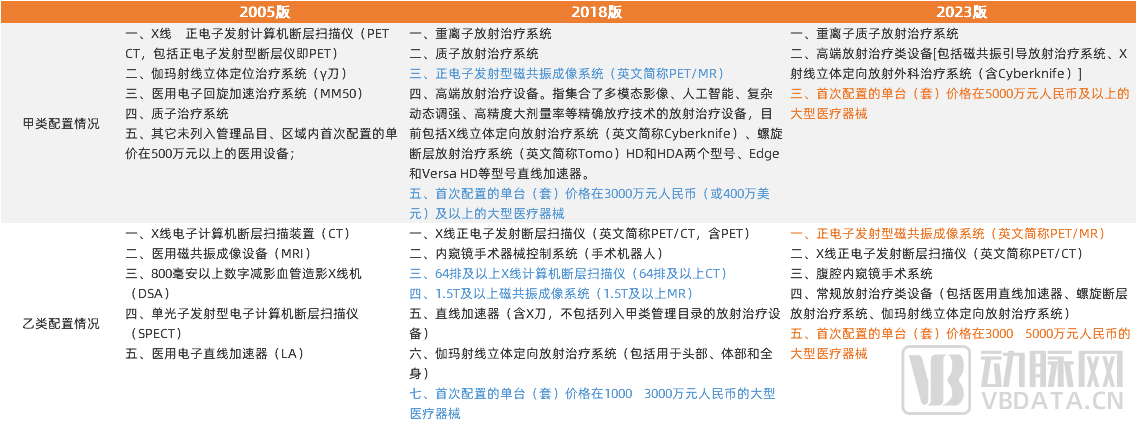

The original intent behind the introduction of the Catalogue for the Allocation of Medical Equipment was to curb hospitals’ blind investment in equipment, thereby optimizing the allocation of hospital assets. Since the formulation of the first Interim Measures for the Administration of Allocation and Application of Large-Scale Medical Equipment in 1995, China’s Catalogue for the Allocation of Medical Equipment has undergone several iterations.

Changes in the configuration catalog over the years reveal a clear trend: more frequent updates, narrower coverage, lower procurement thresholds, and the continuous decentralization of authority for configuring large medical equipment.

Policy Changes Over the Years (Blue sections indicate adjustments or reductions compared to the 2023 version; orange sections indicate adjustments or additions compared to the 2018 version)

Policy Changes Over the Years (Blue sections indicate adjustments or reductions compared to the 2023 version; orange sections indicate adjustments or additions compared to the 2018 version)

Compared with policy changes in previous years, the 2023 edition of the configuration catalog features relatively modest revisions; however, each amendment will reshape a massive niche market.

Deletions: 64-slice and above CT, 1.5T and above MR removed from the configuration catalog

In recent years, the implementation of the tiered diagnosis and treatment policy, coupled with the strong willingness of medical institutions to strengthen infrastructure, has led to a continuous increase in the annual procurement volume of CT scanners in China, with primary healthcare institutions beginning to drive sales. To break through the dominance of joint-venture enterprises, domestic CT manufacturers have been striving to improve quality while reducing costs, constantly exploring the lower price limits for CT systems. They have even compressed the price of 16-slice CT scanners to below RMB 1 million, making this equipment affordable for larger community health centers.

The combined efforts of supply and demand, coupled with the catalytic effect of the COVID-19 pandemic, have significantly accelerated the deployment of CT scanners in Chinese medical institutions, to the point where signs of market saturation are emerging. Data from MedTech Study Club shows that CT sales peaked in 2020 and began to decline in 2021. However, this decrease was entirely attributable to low- and mid-end CT systems with fewer than 64 slices, while sales of mid- to high-end CT scanners continued to grow.

The removal of restrictions on the procurement of mid-to-high-end CT scanners in the 2023 edition of the Configuration Catalog aligns well with the development trends of China’s CT industry. As domestic 64-slice CT technology matures and prices become increasingly controllable under full competition, healthcare institutions can gradually transition to 64-slice and higher-slice CT systems when replacing their equipment, thereby advancing toward higher-quality development.

It should be noted that the volume-releasing effect of allocation policies may be somewhat weakened by the widespread adoption of specialized equipment such as 60–63-slice CT scanners and 1.43T/1.49T MR systems, which serve as alternatives to “64-slice CT” and “1.5T MRI.” When the 2018 edition of the Allocation Catalog removed purchase restrictions for CT scanners with fewer than 64 slices, sales across various CT product lines did not see a significant increase in 2019; it was not until the emergence of COVID-19 in 2020 that the entire CT market began to surge. Therefore, policy changes primarily impact high-end CT scanners with more than 64 slices.

Compared to the mid- and low-end CT segments, demand in the high-end CT market is price-inelastic, leading to a lag in policy transmission and causing the volume growth effect to be dispersed over several future years. This lag primarily stems from hospitals’ equipment configuration planning: hospitals that had already planned to purchase high-end CT scanners will not alter their plans due to policy implementation, while for hospitals generating additional procurement needs due to catalog changes, current policies have relaxed purchasing restrictions on high-end CT scanners but have not guided manufacturers to lower prices. With equipment costs nearing ten million RMB, hospitals with insufficient patient flow and limited research capabilities can neither recover their costs within a few years nor fully leverage the equipment’s value through scientific research. Therefore, when acquiring mid- to high-end equipment, hospitals must simultaneously complete staffing and operational planning; otherwise, the expensive equipment they purchase will ultimately become a management burden lasting for several years.

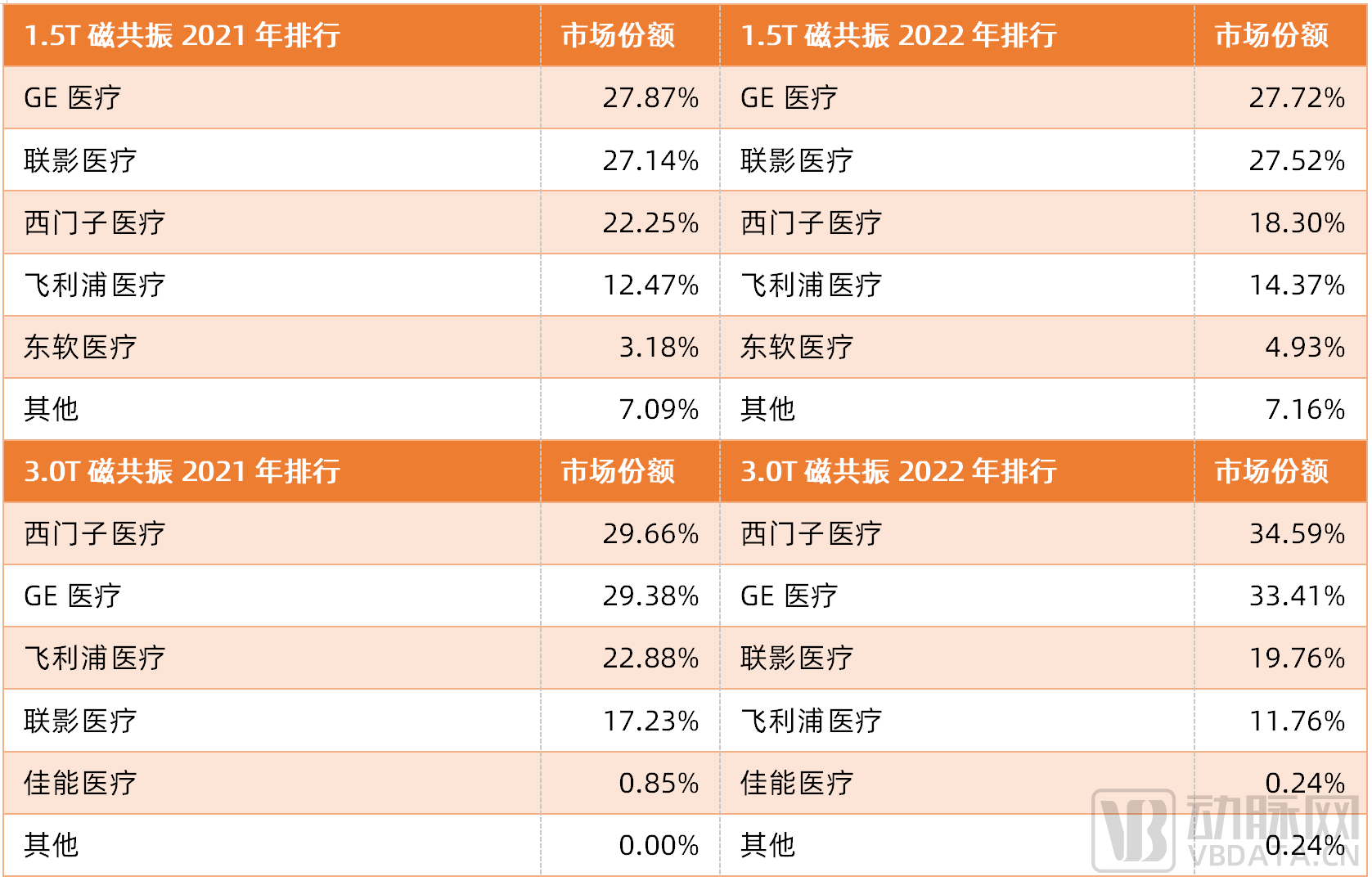

The situation with MR is similar to that of CT, but with slight differences. Currently, the 1.5T MR market, which serves as the primary workhorse, is still far from saturation. As a result, manufacturers are continuously reducing prices to compete for share in the 1.5T MRI market, with some companies selling 1.5T MR units at prices even below RMB 3 million. With recent policy decentralization, 1.5T MRI systems are now able to enter higher-tier hospitals, and to some extent, they will replace 1.43T and 1.49T MRI systems in the market.

The high-end and ultra-high-end MR markets will be more significantly affected. At present, a large number of hospitals have already deployed 3.0T MR systems to enable more precise diagnosis of diseases affecting the nervous, cardiovascular, and cerebrovascular systems, resulting in a market characterized by excess demand over supply. Once the authority for equipment procurement allocation is fully decentralized, sales volumes of high-end MRI scanners may rise more rapidly. After all, hospitals also expect to boost revenue while advancing scientific research by leveraging new equipment.

Overall, although the configuration directory sets 64-slice CT and 1.5T MR as the “threshold,” the high-end CT and MR segments have responded more strongly. Furthermore, MR is more sensitive to policy changes than CT, given the market dynamics of scarcer resources and greater demand.

As policy changes are primarily focused on the high-end medical imaging equipment sector, they are more beneficial to companies that have already established a strong presence in this field, such as GE Healthcare, Philips Healthcare, Siemens Healthineers, United Imaging, and Neusoft. Furthermore, due to the price differential, there is virtually no competition between high-end and low-end CT scanners; therefore, a market for mid-to-low-end CT systems will persist for several years. 16-slice CT scanners priced at approximately RMB 1 million, as well as 32-slice and 40-slice CT scanners priced between RMB 4 million and RMB 5 million, will remain the primary procurement choices for primary healthcare institutions. This implies that manufacturers with a focus on mid-to-low-end CT scanners still have ample time to undergo transformation.

2021–2022 MR Market Competitive Landscape (Data Source: Yizhaocai)

Adjustment: PET/MR is reclassified from Category A to Category B

Due to the relatively late market entry of PET/MR systems, there remains significant room for expansion in terms of clinical value and market awareness. Currently, only a very limited number of manufacturers are capable of producing PET/MR equipment, and systems integrating 1.5T or higher-field MRI are exceedingly rare.

United Imaging’s prospectus disclosed certain data: As of the end of 2020, there were approximately 200 PET/MR systems installed worldwide, primarily distributed across North America, Europe, and China. China accounted for around 40 installations, representing one-fifth of the global market. In 2020, among the PET/MR equipment purchased in China, United Imaging held a 50% market share, while GE Healthcare and Siemens Healthineers each held 25%.

Reclassifying PET/MR from Category A to Category B reflects, to some extent, official recognition of its clinical applications and development prospects, demonstrating a willingness to provide policy support to encourage more top-tier Grade 3A hospitals to acquire PET/MR systems and accelerate the bidirectional advancement of clinical practice and scientific research in PET/MR.

Given the limited number of players and high competitive barriers in this multi-billion-yuan market segment, the introduction of new policies will further intensify the competition between GPS and United Imaging. However, since the policy does not specify the magnetic field strength for the MRI component in PET/MR systems, low-field-strength PET/MR devices from companies such as ViewRay (under Fosun) are also poised for a surge in sales.

Adjustment: The threshold for configuring the first Class A medical equipment has been adjusted from over RMB 30 million to over RMB 50 million; the threshold for configuring the first Class B medical equipment has been adjusted from RMB 10–30 million to RMB 30–50 million.

Compared with the all-encompassing RMB 10–30 million range, the updated RMB 30–50 million tier in the configuration catalog is somewhat distinctive. In terms of unit price, common equipment such as 128-slice/256-layer CT scanners, 3.0T MR systems, PET/CT scanners, and surgical robots can be purchased for under RMB 30 million. Meanwhile, scarce, custom-built 7.0T MR systems and PET/MR systems integrating 3.0T MR technology are priced by manufacturers at well over RMB 50 million.

An industry insider told VCBeat: “The price range of RMB 30 million to 50 million is aligned with large-scale medical equipment procurement plans for the coming years. In particular, as photon-counting CT and 5T MRI systems enter the market, an appropriate mechanism is needed to regulate hospital equipment configurations. Overall, the adjustment of this ‘threshold’ reflects the National Health Commission’s supportive stance toward healthcare institutions acquiring more advanced medical equipment, which aligns with the future needs of high-quality hospital development.”

As the most valuable segment of the entire industry chain, the upgrading of large-scale medical equipment not only drives active innovation, enhances manufacturing processes, and reduces configuration costs in the upstream components sector, but also prompts downstream hospitals to shift their mindset, accelerate scientific research, elevate the status of relevant departments, establish more mature training systems, and recruit more talent adept at operating high-end medical devices.

Meanwhile, mid-tier medical AI enterprises will also experience rapid growth alongside the boom in large-scale medical equipment, striving to unlock the clinical potential of such devices and reduce their dependency on personnel expertise. The development of digital application platforms for medical equipment is likewise poised for opportunity; as hospitals’ equipment portfolios become increasingly diverse, there is a growing need to establish new platforms for intelligent, full-lifecycle device management.

Overall, the relaxation of configuration catalog requirements for medical devices will gradually impact the entire chain, enabling an upgrade across the full industrial chain.

Nevertheless, the relaxation of configuration planning policies also harbors concerns. In an era where centralized procurement has become widespread for medical devices, the majority of medical equipment still adheres to traditional sales models. However, in certain regions, calls for including imaging equipment in centralized procurement are growing louder. Concerns that once existed only in prospectuses have now partially become a reality.

Anhui Province had already established centralized procurement at a certain scale as early as 2016, purchasing a total of 43 CT scanners, 16 MR systems, 8 DSA units, and 8 LA devices. Fujian Province followed suit, launching provincial-level centralized procurement for large equipment such as CT and MRI in 2021, with average price reductions exceeding 50%; Suzhou Langerun’s 1.5T MR system was sold for only RMB 2.93 million. In October 2022, Fujian further expanded the scope of its provincial centralized procurement to cover 64-slice CT, 1.5T MR, high-end CT (256-slice and above), and high-end MR (3.0T and above).

An industry insider believes that the relaxation of configuration controls for CT and MR equipment in the allocation catalog has made manufacturers more susceptible to price reduction risks resulting from centralized procurement.

How to Mitigate These Risks? All Domestic Medical Device Manufacturers May Have No Choice but to Move in Unison Toward the “High-End” Market.