Behind the Trillion-Dollar Market: Medical Device Investment Shifts Upstream

NovelBeam

Developer and Manufacturer of Medical Endoscopic Instruments and Optical Products

Early this year, more than ten medical device companies focused on hard-tech secured financing, including Huamu Medical (a medical device R&D firm), Sailuo Medical (specializing in the R&D and manufacturing of dental instruments), and Biolock (a developer of assisted reproductive technology devices). In the secondary market, several other companies, such as Shandong Baiduoan Medical Device and Harbin Sizerui Intelligent Medical Equipment, are queuing for initial public offerings (IPOs).

“Current Status and Trends of China’s Medical Device Industry” indicates that the market size of China’s medical device industry is expected to reach RMB 958.2 billion in 2022. In this nearly trillion-yuan market, domestically produced products have established a firm foothold in the low- to mid-end segments and are now making inroads into the mid- to high-end segments. The development of mid- to high-end products relies heavily on support from upstream industries, including electronics manufacturing, mechanical engineering, biochemistry, and materials. Without such upstream support, the move toward higher-end domestic medical devices would be nothing but an illusion. Consequently, there has been a growing trend of investment directed at upstream sectors in recent years.

The rise of investment in hard-tech medical innovations is an inevitable outcome driven by the logic of import substitution and the pursuit of self-reliance and controllability for domestically produced medical devices. Only by securing intellectual property rights over core technologies and components, while leveraging China’s manufacturing advantages, can we ensure supply chain security, reduce R&D costs for mid-stream enterprises, create a favorable environment for independent innovation, achieve self-reliance and controllability, and mitigate the risk of being “strangled” by external technological bottlenecks.

The upgrade of the medical device industry from “manufacturing” to “intelligent manufacturing” hinges on the upstream supply chain.

The Value of Upstream Medical Device Companies Is Becoming Increasingly Evident, Potentially Emerging as the Next Investment Hotspot.

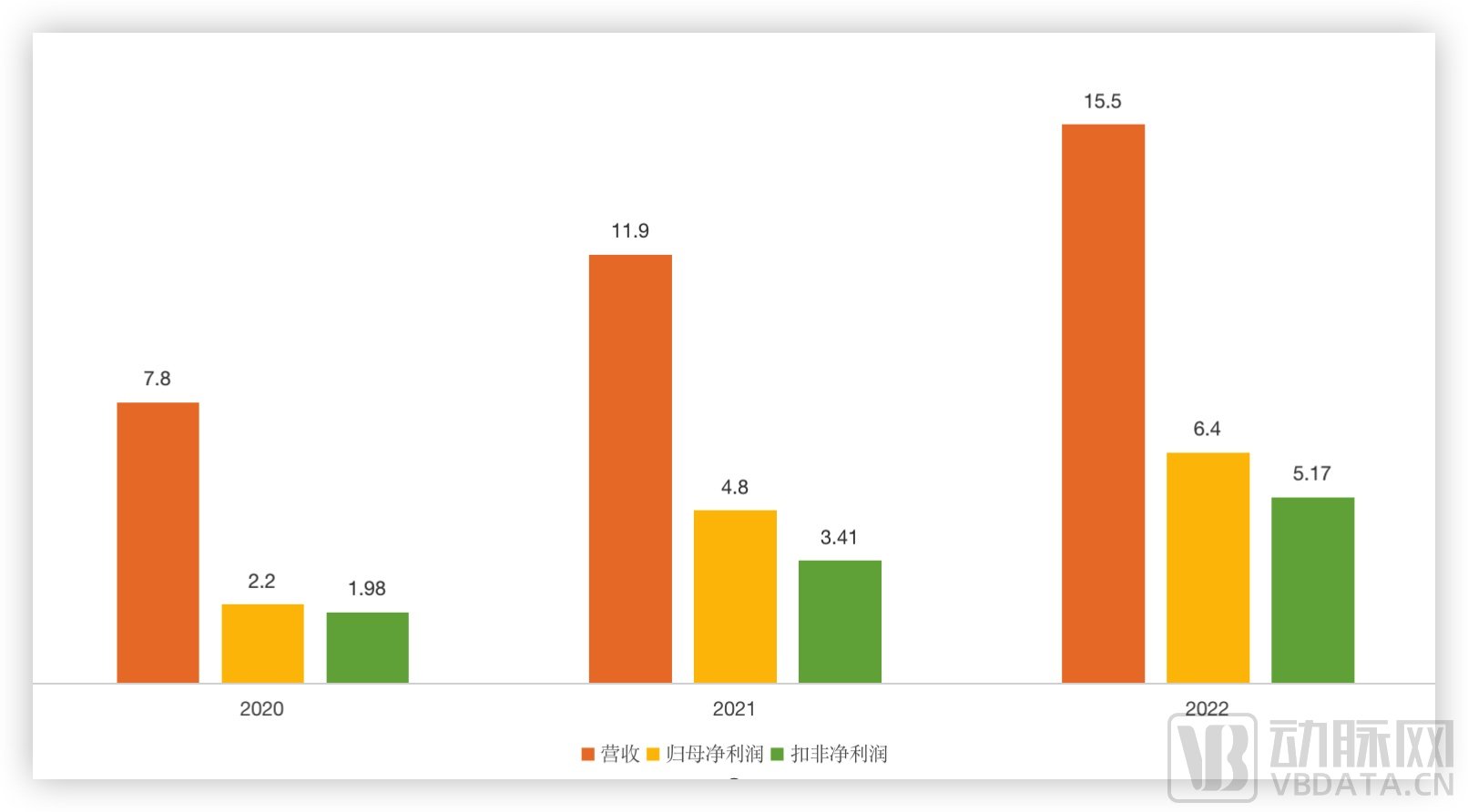

iRay Technology recently released its 2022 annual report. The company’s main business revenue reached RMB 1.549 billion, a year-on-year increase of 30.47%; net profit attributable to shareholders of the listed company was RMB 641 million, up 32.49% year on year; and net profit after deducting non-recurring gains and losses amounted to RMB 517 million, representing a year-on-year increase of 51.18%. Not only in 2022, but also looking at the data from the past three years, it is clear that iRay Technology’s business has shown a steady upward trend.

Key Financial Data of iRay Technology for the Past Three Years, Sourced from Corporate Announcements

iRay Technology’s core business is flat-panel detectors. In X-ray imaging equipment, when the X-ray source irradiates the human body, digital X-ray flat-panel detectors capture the attenuated X-ray photon signals that have passed through the body and convert them into digital images containing diagnostic information. The quality of flat-panel detectors directly affects image clarity and acquisition speed; they can be simply understood as the image sensors in digital cameras.

iRay Technology’s development coincided with the critical juncture when China’s medical imaging equipment industry was upgrading from traditional analog X-ray systems to digital ones. Market procurement of new equipment has spurred demand for upstream X-ray detectors.

Like many domestic brands, iRay Technology was not trusted by the market at its inception, with this distrust transmitting from the end-user market upstream. To reverse this situation, iRay adopted an outside-in strategy, initiating contacts with global brands such as Philips and Siemens starting in 2011. By around 2013, it had joined the supplier ranks of these multinational corporations, thereby gaining entry to numerous renowned international medical imaging equipment manufacturers.

By integrating into the supplier networks of multinational corporations, iRay Technology has accumulated substantial technical reserves. It is one of the few companies globally that simultaneously master four major sensor technologies—amorphous silicon (a-Si), IGZO, flexible substrates, and CMOS—and possess mass production capabilities for X-ray detectors. According to its 2022 annual report, iRay Technology had accumulated a total of 398 intellectual property rights, including 122 invention patents.

The development cycle for flat-panel detectors is long, requiring substantial capital investment, featuring high technical barriers, and involving complex manufacturing processes. Third-party suppliers like iRay Technology can effectively enhance the R&D efficiency of midstream imaging equipment manufacturers, representing the optimal solution under the current business model. iRay Technology’s steadily growing revenue over the past three years further corroborates its market position.

To achieve domestic substitution and autonomous control of medical devices, such upstream enterprises are indispensable.

The research and development of medical devices is highly dependent on the innovative advancement of upstream core materials and key components.

International cases have demonstrated that upstream enterprises play a pivotal role in driving the development of midstream and downstream equipment. Consequently, Chinese government authorities—ranging from the Ministry of Industry and Information Technology (MIIT) and the Ministry of Science and Technology (MOST) to various provincial departments—have issued multiple policy documents to encourage the coordinated development of core upstream components and materials.

Over the years, domestically produced medical devices have developed continuously from scratch, driving upstream component manufacturers to achieve a breakthrough from “0” to “1,” marking the first step for China’s upstream supply chain. As the logic of domestic substitution unfolds, domestically produced medical devices are expanding into more fields and launching an assault on the mid-to-high-end market from their base in low-end products.

For international giants, they are not waiting to be replaced; instead, they are seeking cooperation with domestic enterprises to establish local supply chains and localize production, thereby mitigating policy pressures. Against this backdrop, the upstream medical device supply chain has entered its second phase of development, providing domestically produced core components for multinational brands.

After entering the multinational brand supplier industry, domestic upstream companies have leveraged the engineer dividend and manufacturing advantages to gain an edge in differentiated design and cost control. This has made their products competitive on a global scale, thereby enabling them to capture global market share.

By integrating into the supply chains of more overseas brands, upstream enterprises have established the conditions for positive revenue growth. Furthermore, through collaboration with these international brands, they are continuously accumulating technical expertise to build scalable technology platforms, thereby extending their technological capabilities horizontally into broader fields. This strategy will enable companies to overcome the limitations of constrained market capacity and low growth ceilings inherent in individual niche segments of the upstream medical device industry, ushering in opportunities for rapid expansion.

In the endoscopy sector, where domestic products account for less than 10% of market penetration and industry giants dominate the mainstream market, there is a notable case of an upstream enterprise that has leveraged its technological accumulation to extend downstream, thereby unlocking new growth opportunities.

NovelBeam, established in 2003, has leveraged its accumulated expertise in optical technology to engage in the research and development of medical endoscope technologies. It ranks among the global leaders in the field of fluorescent rigid endoscopy and was successfully listed on the STAR Market in 2021.

Looking back at the development of NovelBeam, from 2003 to 2007, its business was primarily based on the OEM model. During this period, the company refined its industrial chain and strengthened technological innovation through contract manufacturing, thereby establishing comprehensive optical manufacturing capabilities. It also accumulated advanced technologies in LED application fields, such as LED/LD driver technology and multispectral illumination design, laying a solid foundation for its subsequent entry into the medical endoscopic device sector.

After 2007, NovelBeam continued to deepen its expertise in medical endoscopy technology. Relying on its independently developed LED endoscopic light source modules, the company successfully joined Stryker’s supplier base in 2008. In 2015, NovelBeam successfully developed high-definition fluorescence laparoscopes, fluorescence light source modules, and fluorescence camera adapter lenses for hepatobiliary surgery, gaining a first-mover advantage in the fluorescence application market.

NovelBeam’s primary revenue streams derive from component sales and its Original Design Manufacturer (ODM) collaborations with clients. NovelBeam’s fluorescence endoscopy products have been adopted by Stryker for use in the world’s first high-definition (HD) fluorescence laparoscopic system launched globally, making NovelBeam the exclusive design and manufacturing supplier of the system’s core components, including the HD fluorescence endoscope, HD fluorescence camera adapter lens, and fluorescence light source module.

Meanwhile, adhering to the strategic framework of “commercializing one generation, developing the next, and reserving the third,” NovelBeam has maintained sustained R&D investment over the years, thereby preserving its core competitiveness in the field of medical imaging devices. The development trajectory of NovelBeam serves as a textbook case of self-iteration and upgrading for an upstream enterprise in the medical device industry.

From an investment perspective, upstream enterprises like NovelBeam, which leverage engineering and industrialization techniques to drive the integrated development of medical engineering by enabling the intelligence and digitalization of medical devices and technologies, represent a key future investment direction.

As medical device companies expand overseas to compete globally, the development logic of the industry has shifted from mere domestic substitution to achieving autonomous and controllable capabilities, with a robust upstream supply chain being an indispensable component.

Throughout, in the niche segments of the medical device industry, investment institutions have favored sectors with room for innovation and low penetration rates of domestically produced products. However, the situation differs when it comes to upstream companies in the medical device supply chain. The core components at the upstream level face limited market space; as mentioned earlier, industries such as flat-panel detectors and light sources for rigid endoscopes each have relatively small individual market sizes. If NovelBeam were to supply components solely to Stryker, its revenue scale would be constrained, making it difficult to envision substantial growth potential.

Certainly, upstream enterprises are also leveraging their technological expertise to explore greater possibilities. For instance, in 2022, iRay Technology not only maintained a growth rate of over 10% in its flat-panel detector business but also actively expanded its dental product series, achieving a 55.9% growth rate. It successively completed supply chain integration with several well-known domestic CBCT equipment manufacturers, including Meyer Optoelectronic, LargeV, Fussen Technology, Born Dental, Sailuo Medical, and Woodpecker. The company will continue to expand its overseas customer base in the future.

Furthermore, iRay Technology has extended its technological applications to industrial products, successively launching a series of NDT products for industrial power battery inspection. In light of the rapid expansion of production capacity in China’s new energy sector, the company has also developed CMOS-based TDI detector prototypes tailored to the needs of new energy battery customers, with mass sales expected to commence in 2023.

NovelBeam is leveraging its foundational optical technologies to expand horizontally into fields such as biometric recognition and optical microscopy. Meanwhile, capitalizing on the absence of Stryker’s product sales in China, NovelBeam has developed its own complete medical devices and collaborates with Stryker through original equipment manufacturing (OEM) and private-label sales models to boost revenue.

The ability to leverage technological platforms to horizontally expand new product R&D capabilities is a key factor determining the value of upstream enterprises.

Furthermore, a holistic approach must be adopted at the level of industrial and supply chains. Sectors with low localization rates are currently the primary targets for industry breakthroughs, and upstream development must align with the needs of midstream and downstream segments. For instance, while domestic complete medical devices such as surgical robots have begun to enter the commercialization phase, core components associated with these products, including servo motors and reducers, remain monopolized by foreign brands. High-end medical devices rely heavily on components such as chips and sensors; without support from these underlying key technologies, achieving independent control and innovation is impossible.

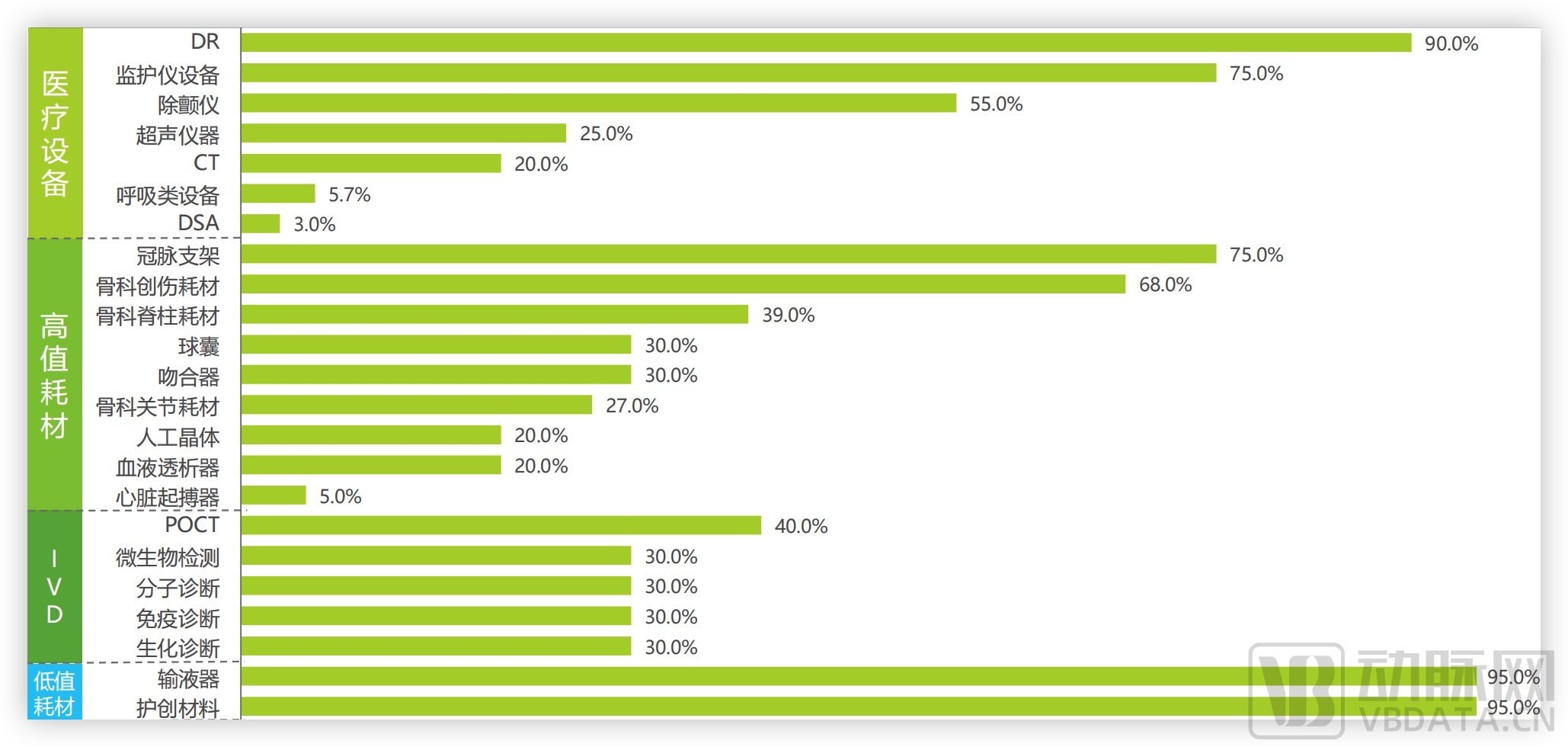

Domestic Production Rate in Major Fields of Medical Devices, Source: "Research Report on the Trend of Domestic Substitution of Medical Devices in China"

The logic of healthcare investment cannot bypass innovation. If innovation is broadly categorized into general innovation for import substitution, synchronous innovation to maintain international standards, and high-level innovation leading niche sectors, none of these can develop in isolation from the industrial chain; rather, they must align with the overall needs of industrial development.

In the field of medical imaging equipment, this includes core components of the imaging chain such as high-power CT X-ray tubes, high-voltage generators, and detectors, as well as electronic components like sensors and high-end chips; in the upstream supply chain of ventilators, it covers core parts such as solenoid valves, turbo compressors, and sensors; and for endoscopes, it encompasses image sensors, scopes, light source modules, and camera systems. These are all areas where China’s domestic industry urgently needs to achieve breakthroughs.

An investor stated, “When evaluating projects, we look beyond end products to examine upstream components. We deconstruct products to analyze the technical barriers surrounding their core components, assessing whether these can be addressed at the current stage. We also evaluate the scale of future market demand to determine if it warrants strategic investment. While many products have already achieved localization in China, the upstream sector—particularly core components and the instruments and equipment used for their R&D and design—remains largely untapped, presenting a significant market opportunity.”

Investment in the upstream segment of hard-core medical technology will become a key niche track in the industry. On one hand, this is driven by policy support, as the state has consistently encouraged various industries to break through core technological barriers and avoid being “strangled” by foreign dependencies. On the other hand, unlike midstream products, upstream component products do not require lengthy medical device registration cycles, offering richer commercialization scenarios for technology monetization. Furthermore, the upstream sector is less directly impacted by centralized volume-based procurement, making demand more inelastic from a payment perspective.

In essence, Chapter 18C is a continuation of the Chapter 18A policy.

In 2018, the Hong Kong Stock Exchange (HKEX) introduced Chapter 18A, a policy enabling pre-revenue biopharmaceutical companies to raise capital through IPOs. This initiative primarily targeted biotech firms focused on innovative drugs and medical devices, sparking significant growth in these sectors. On March 31, the HKEX implemented the new Chapter 18C regulations, which expand eligibility to include frontier technology fields not covered under Chapter 18A. Companies operating in healthcare-related information technology (such as AI-driven manufacturing, medical AI, SaaS, and healthcare digitalization), advanced manufacturing (including robotics), and new materials (such as synthetic biology and nanomaterials) can now apply for IPO fundraising under Chapter 18C.

Meanwhile, Chapter 18C does not close the door to companies outside the existing specialized and sophisticated technology industries. The Hong Kong Stock Exchange has stated that applicants demonstrating the following characteristics may still be accepted:

1. High growth potential;

2. Able to demonstrate that its core business employs new technologies and innovative techniques;

3. R&D investment reaches a certain proportion, among other conditions.

The upstream industrial chain, including innovative medical devices, will benefit from the Chapter 18C policy. Regarding the implementation of Chapter 18C, some investors have stated that it will further broaden exit channels for funds. Compared with the STAR Market, Chapter 18C has relaxed listing requirements, making it easier for companies to go public.

According to data from the "Development Report on National-Level Specialized, Refined, Differential, and Innovative 'Little Giant' Enterprises (2022)," as of December 31, 2022, the average age of national-level specialized, refined, differential, and innovative "Little Giant" enterprises was 16 years. Among them, the largest group consisted of enterprises established for 15 to 20 years, totaling 2,480 companies, accounting for 27.50%; followed by those established for 10 to 15 years, with 2,262 companies, representing 25.08%.

On a median basis, it takes approximately 13 years for a company to reach this stage of development. If investment institutions enter at the startup phase, the investment horizon—including the post-IPO lock-up period—may extend beyond 15 years, which misaligns with the typical lifespan of most funds and consequently impairs their capital efficiency. For numerous upstream hard-tech enterprises, continuous R&D funding is essential, resulting in persistent financing needs.

Both the Chapter 18C listing rules and the new fifth set of listing criteria introduced last year for the STAR Market have provided upstream companies with hard-tech attributes more convenient financing channels, ushering in significant development opportunities for the upstream industry chain.

According to data from Artery Orange, there were over 900 financing deals in China’s healthcare sector in the primary market in 2022, with total funding exceeding RMB 100 billion. Among these, the field of medical devices and core component R&D and manufacturing accounted for more than 200 deals, with funding surpassing RMB 20 billion. The rising investment热度 in upstream hard technologies in healthcare has been fueled by capital influx, with even internet giants participating in this trend.

Alibaba’s Yunfeng Capital has invested in multiple sectors, including high-end medical devices, medical robots, surgical equipment, innovative drugs, and vaccines. Tencent Investments has similarly covered areas such as high-end medical devices, surgical equipment, and novel vaccines.

This wave of investment in upstream hard tech has also swept into universities, as many key technologies are held by scientists. Whoever can “secure” scientists secures frontier technologies. Medical innovation in China is moving toward higher-end, more autonomous, and more internationalized development. In the next phase, the commercialization and translation of frontier technologies will inevitably be a critical link. With policy support and the combined forces of technology, capital, industry, and talent, the upstream hard tech sector is poised to reach new heights.