From Direct Entry to Behind-the-Scenes Investors: What Are Home Appliance Giants Really Competing for in the Medical Market?

Recently, two financing deals in the healthcare sector have drawn the attention of VCBeat. One isMicroRock Medicineannounced the completion of a Series B financing round worth hundreds of millions of yuan, and the other isChengyuan TechnologyAnnounced the completion of a pre-A financing round worth tens of millions of U.S. dollars. The reason for highlighting these two financing events among numerous others is mainly due to the distinctive nature of their investors, which are respectively under Haier GroupHaier Capitaland under the Gree GroupGree Industrial Investment。

Why, then, are these two institutions described as “special”? There are two main reasons: First, although Haier and Gree, as traditional home appliance manufacturers, have entered the medical field for some time,However, the role of an investor remains relatively unfamiliar., In addition, in their capacity as investors, both companies have shown a trend of continuously increasing their investments over the past two years. According to incomplete statistics,Haier and Gree have collectively invested in 17 companies in the medical sector over the past two years.

The second "special" reason lies inThe Nature of Medical Enterprises Invested in by Haier and Gree Is Undergoing Fundamental Changes. Based on past cases, home appliance companies' cross-sector investments in the medical field have mostly revolved around their core businesses, but this investment trend is currently changing. Taking the two investee companies mentioned earlier as examples,MicroRock Medicineis a provider of clinical testing services for infectious pathogenic microorganisms, andChengyuan Technologyis dedicated to accelerating the R&D of synthetic peptide drugs through AI empowerment, which has little relevance to the core businesses of Haier and Gree.

So, what exactly is the reason behind this?

Mega-Mergers and Venture Creation: Why Are Home Appliance Giants Obsessed with the Healthcare Market?

Before exploring the venture capital investments of home appliance giants in the medical sector, let us first clarify one point: why are these home appliance giants focusing their attention on the healthcare industry?

In fact, it is not new for non-medical enterprises to cross over into the healthcare sector, especially in the home appliance industry, where many major brands have rushed to enter the market. Globally, home appliance giants such as GE, Siemens, Philips, Panasonic, and Toshiba have been heavily investing in the healthcare industry. Over the past decade, several leading Chinese home appliance companies, including Haier, Midea, Gree, and Hisense, have also ventured into the medical field.

Taking Haier as an example, as early as 2005, Haier establishedHaier Biomedical, specializing in the field of low-temperature storage equipment for biomedical applications. In 2019, the company successfully listed on the STAR Market. It was also in that year that Haier Group acquired the listed company Xingpu Medical Technology for RMB 1.829 billion, which was later renamedYingkang Life, according to its latest annual report, Yingkang Life achieved a total revenue of RMB 1.156 billion in 2022, representing a year-on-year increase of 6.09%. Among this, the medical services segment generated RMB 997 million in revenue, while the medical devices business segment contributed RMB 160 million.

Compared with Haier, Gree entered the medical field relatively late, only announcing its foray into the healthcare industry in early 2020. Despite its late entry, Gree has made aggressive moves. After Dong Mingzhu, Chairman of Gree, announced that “the company will invest RMB 1 billion in the medical equipment sector,” Gree established, within less than half a year,Zhuhai Gejian Medical Technology, Chengdu Gree Xinhui Medical, Tianjin Gree Xinhui MedicalThree medical enterprises focus on the research and development of high-end medical equipment.

In addition, there is Midea. Although Midea is not the focus of this article, as a home appliance company, its layout in the medical field is also worth exploring. In 2017, Midea spent 29.2 billion to acquire the German robotics companyKuka Medical; In February 2021, Midea invested RMB 2.297 billion to take control of a long-established listed medical imaging companyWandong Medical; In March 2021, Midea was registered and establishedMidea Biomedical, Since then, Midea has completed a systematic layout in the medical field, establishing five major healthcare scenarios, including medical technology buildings, surgical departments, outpatient pharmacies, inpatient wards, and logistics command centers.

Looking back, it is not difficult to find that the ways in which home appliance companies have crossed over into the medical field are basically similar, namelyInvesting in or acquiring companies while simultaneously seizing opportunities to establish new enterprises, but regardless of the approach, the underlying efforts are immeasurable. In addition to substantial capital investment, commensurate human resources and energy must also be devoted. For instance, after Midea acquired Wandong Medical and became its largest shareholder, Midea Group appointed Hu Ziqiang, then CTO of Midea, as the legal representative and chairman of Wandong Medical. Additionally, Zhong Zheng, then CFO of Midea, and Liu Xiao, then Director of Strategic Development, underwent role adjustments and both assumed positions as non-independent directors on Wandong Medical’s board.

Therefore, one cannot help but ask,Why Are Home Appliance Giants Desperately Venturing into the Healthcare Sector?

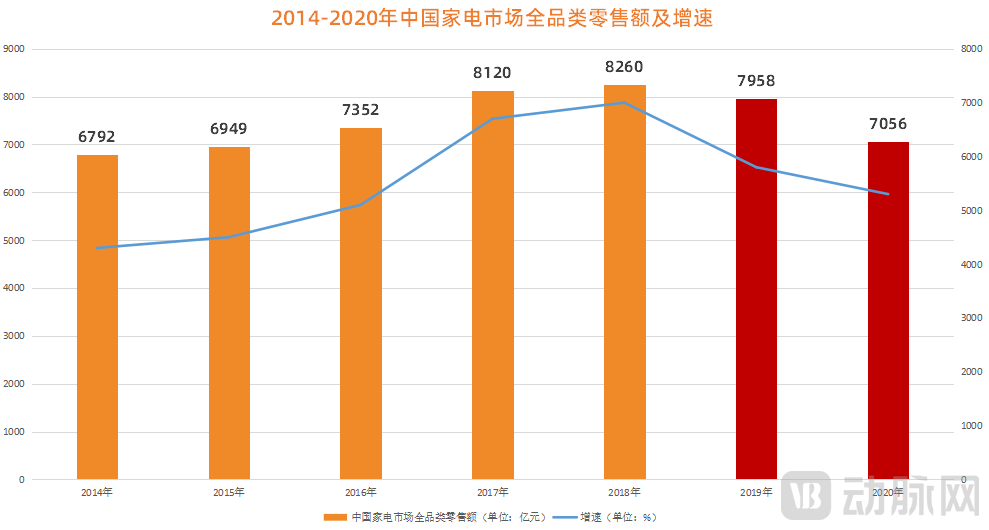

This is certainly not without reason. Currently, China's home appliance industry, having gone through a period of rapid growth, has achieved high product penetration rates,The market has shifted from a growth-driven market to a stock-based market.In addition, in recent years, affected by factors such as the slowdown in the growth of the real estate industry and pandemic control measures, the sales volume and growth rate of China's home appliance industry have declined. According to data from AVC (All View Cloud), the retail sales of China's home appliance market decreased by 3.6% year-on-year in 2019 and dropped by 11.3% year-on-year in 2020, representing a direct difference of RMB 120.4 billion compared with 2018.

Figure 1. Market Size and Growth Rate of China’s Home Appliance Industry (Data Source: AVC, CSC Financial)

Figure 1. Market Size and Growth Rate of China’s Home Appliance Industry (Data Source: AVC, CSC Financial)

This means that, against the backdrop of continued pressure on China’s home appliance industry,China’s Leading Home Appliance Giants, Growing Ever Larger, Need to Forge a Second Growth Curve, while medical devices boast higher gross profit margins, providing a strong stimulus to the overall business of home appliance enterprises. According to Wind data,In China, the gross profit margin for medical devices can exceed 80%, significantly higher than the average gross profit margin of 33% for home appliance products., the enormous profit potential makes it hard for home appliance giants to resist the temptation.

However, hidden behind these opportunities are risks. This is particularly true in the highly regulated medical sector, where numerous cross-industry giants have previously failed. Nevertheless, compared with companies from other sectors, home appliance giants possess unique advantages when entering the healthcare industry. Technologically, there is a certain degree of commonality between consumer appliances and medical devices. Furthermore, significant similarities exist in supply chains, sales channels, and assembly integration. These favorable factors have bolstered the confidence of home appliance giants in targeting the medical device market.

From Founding Companies to Pivoting to Venture Capital: Why Have Home Appliance Giants Changed Their Strategy?

As it is a blue-ocean market, home appliance giants are naturally going all out, with substantial investments in the medical sector.However, at present, its overall return remains relatively weak.. Taking Haier as an example, according to its financial reports, Haier Biomedical achieved sales revenue of RMB 2.864 billion in 2022, a year-on-year increase of 34.72%. Although the growth rate was substantial, its revenue accounted for less than 1% of Haier Group’s global revenue.Clearly, the healthcare industry has not yet become the second growth curve for home appliance giants.

This means that home appliance giants represented by Haier and Gree still need more room for imagination in the medical market, so they have started to bet on the field of medical venture capital again. It is reported that Haier Group currently has three venture capital institutions focusing on the medical field, namelyHaier Medical Industry Fund, Haier Venture CapitalandHaier Jinying, and there are also three from Gree, namelyGree Jintou, Gree Group Industrial InvestmentandGree Fund。

In fact, these financial institutions have been established for quite some time. Take the Haier Medical Industry Fund as an example: it was registered and incorporated as early as 2010, but did not make its first formal investment in a healthcare enterprise until 2015. In the subsequent years, its activities remained superficial, with limited substantive moves. It was only in the past two years that its investment frequency began to increase.

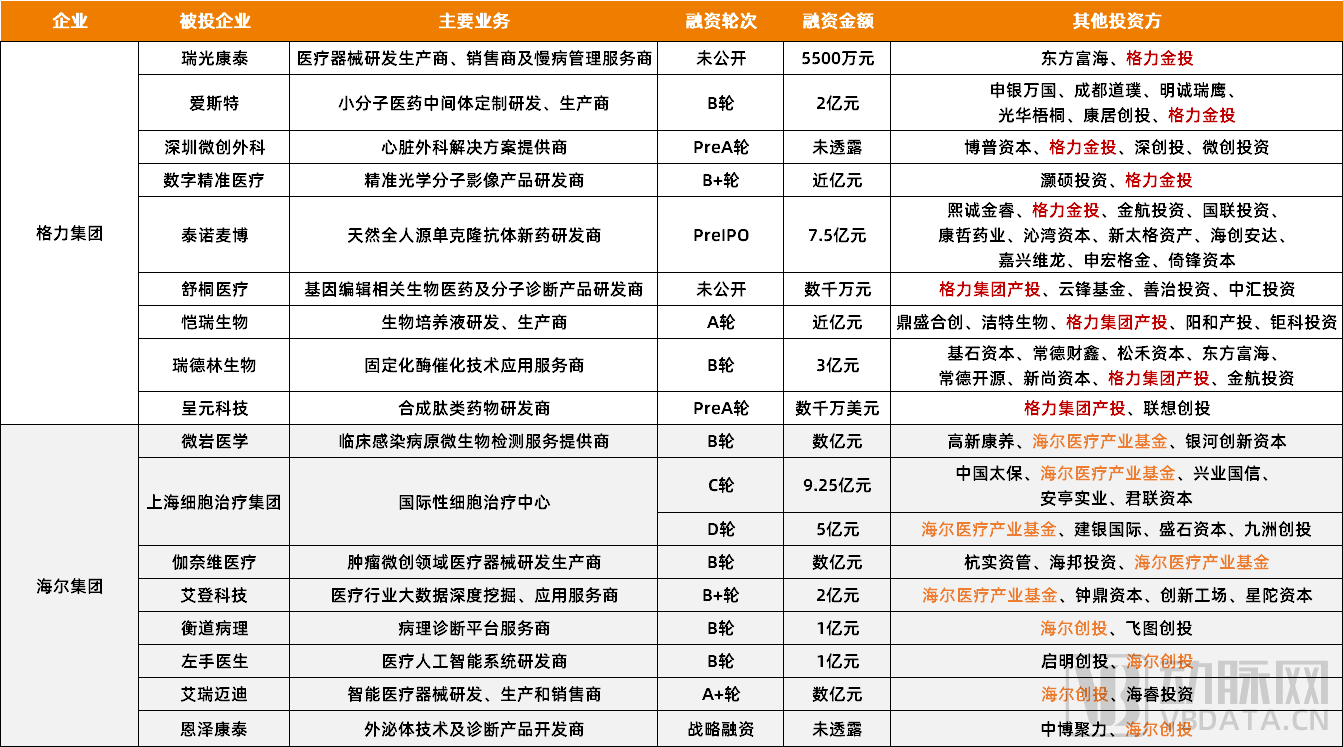

Figure 2. Investment Cases of Haier and Gree in the Healthcare Market Over the Past Two Years (Data Source: VCBeat Orange Database)

Figure 2. Investment Cases of Haier and Gree in the Healthcare Market Over the Past Two Years (Data Source: VCBeat Orange Database)

According to incomplete statistics from the VCBeat Orange Database,Over the past two years, Haier has completed nine financing rounds in the medical sector and invested in eight healthcare companies. Not to be outdone, its direct competitor GREE has also completed nine financing rounds and invested in nine healthcare companies during the same period.

So, who exactly did they invest in?

From the perspective of niche sectors, VCBeat has found that,Its investment targets are no longer limited to medical devices, but also extensively cover frontier fields such as innovative drugs and digital health.. Taking Gree as an example, its portfolio companies includeAiste, Kairui Biology, Ruidelin Biologypharmaceutical and healthcare companies, while Haier has its sights onAiden Techis a technology company focused on the in-depth mining and application of big data within the healthcare industry.

Certainly,Medical device companies remain the primary investment focus for Haier and GreeAccording to statistics, among the 17 portfolio companies, nine are medical device firms, accounting for more than half. However, their focus has expanded beyond imaging to include healthcare scenarios with significant unmet clinical needs, such as chronic disease management, oncology treatment, and minimally invasive cardiovascular procedures.

After examining the changes in the investment landscape, let us now turn our attention to investment rounds. According to compiled data, VCBeat has found thatHaier and Gree’s current investments in the medical sector are primarily concentrated in the mid-to-late stages., with Series B rounds being the most frequent, totaling 8 deals. In addition,Haier and Gree Are Also Focusing on Early-Stage Medical Investments, especially Geli, among the 9 financing events in the past two years, there were 3 before Series A, which respectively invested in cardiac surgery solution providersShenzhen Minimally Invasive Surgery, R&D and Manufacturer of Biological Culture MediaKairui Biotechand the synthetic peptide drug developer mentioned at the beginning of the articleChengyuan Technology。

Overall, Haier and Gree have seen significant changes in their investments in the medical sector over the past two years. First, the frequency of investment has increased substantially; second, the areas of investment have begun to diversify; and finally, while investments remain predominantly focused on mid-to-late stages, there is a gradual expansion into early-stage ventures. What, then, is the underlying logic behind these shifts?

Back to square one, home appliance giants are venturing into the healthcare sector in hopes of finding a second growth curve, and engaging in venture capital investment happens to meet this need.

From an intuitive perspective. In recent years, driven by the dual impetus of the pandemic and evolving clinical needs, the healthcare industry has experienced a significant boom. According to incomplete statistics from the VCBeat Orange Database, there have been 4,735 financing deals in China’s primary healthcare market from 2020 to present. Meanwhile, the secondary market has also been highly active; based on publicly available data, nearly 500 healthcare companies have successfully gone public in recent years.

Hidden within this series of data lies the immense opportunity in the healthcare venture capital market, especially in the current era where hard technology and achievement transformation are the central themes in the medical field. This investment potential is continuously expanding, which could represent the profit margins for home appliance giants entering the healthcare sector.

From a Microscopic Perspective, home appliance companies can leverage venture capital investment to facilitate horizontal industrial expansion and vertical industrial extension in the medical field. First, let us discussHorizontal Industrial Expansion, namely, home appliance giants expand their resource base in the medical sector through investment, thereby increasing their market share in existing industries. This is why Gree and Haier continue to ramp up their investments in the medical device sector.

andVertical Industry ExtensionThis refers to deepening industrial chain layout and extending customer demand, thereby integrating more industrial chain resources. This explains why home appliance giants are currently investing in pharmaceuticals and digital healthcare.Their core objective is to integrate the upstream and downstream segments of the healthcare industry chain, penetrate more deeply into core medical scenarios, and rapidly seize first-mover advantage in the market.

From Real Estate to Home Appliances: How Can “Outsiders” Break Through in the Healthcare Venture Capital Market?

In fact, whether they are institutions under Haier or Gree, they share a unified title in their capacity as healthcare investors—CVC (Corporate Venture Capital). Unlike traditional venture capital,CVC refers to an independent investment subsidiary or investment department established by a non-financial enterprise. Its funds are typically provided solely by the parent company and are not subject to the constraints of fixed fund terms. The establishment, development, and eventual closure of a CVC are closely aligned with the parent company’s long-term strategic development.

Figure 3. CVC Investment and Operation Model

Figure 3. CVC Investment and Operation Model

CVC originated in the United States in the early 20th century and was “introduced” to China around 2000. At that time, Alibaba, which had just been founded one year earlier, participated in investing in Haier’s smart brand “Haier Smart Home,” a move that can be regarded as the earliest attempt at CVC investment in China. After nearly two decades of exploration and development, CVC has now evolved into a highly mature model. Its investment focus is no longer confined to traditional manufacturing but has rapidly expanded into cutting-edge technology sectors, with healthcare being a prominent example.

By reviewing past investment cases, VCBeat found that,CVCs active in the healthcare investment market are primarily from the real estate, internet, home appliance sectors, and publicly listed healthcare companies.. One reason they are the ones is, of course, their pursuit of new incremental markets, as all hope to secure a share in the blue-ocean healthcare sector; another reason is their strong financial capacity. They not only have considerable disposable income but also possess robust external financing capabilities. Many banks proactively extend credit lines to them, often at interest rates below the benchmark rate. Moreover, they benefit from substantial policy support from local governments, including tax reductions and exemptions, various subsidies, and other industrial policy incentives.

The final point isTheir judgments on corporate investments tend to be more precise, with stronger contextual relevance and targeted focus.. Cai Zhengyuan, CEO of Haier Capital, once stated that unlike financial venture capital (VC) firms, corporate venture capital (CVC) investors often possess a deeper understanding of the business models behind cutting-edge technologies and demonstrate greater patience. Furthermore, by leveraging the entire industrial ecosystem and context, CVCs can cultivate areas of collaboration and co-creation with their portfolio companies, thereby providing enhanced synergies from their broader ecosystem resources.

Breaking down this passage, we can clearly see the two core advantages of CVC, namelyPossesses a profound understanding of the industry and robust post-investment service capabilities., these two points are extremely important in today's medical venture capital and investment market.

Currently, China’s healthcare sector is entering a critical phase that demands “genuine innovation.” As industry bubbles gradually dissipate and the industrial structure undergoes further realignment, investing early in hard-tech innovations has become a keyword for the healthcare industry at this stage. Against this broader trend, new requirements are being placed on investors: on one hand, they need a clearer understanding of the industry to identify stable growth opportunities amidst market variables; on the other hand, they must possess post-investment service capabilities to support the long-term growth of their portfolio companies.

Taking Haier as an example, according to Cai Zhengyuan, CEO of Haier Capital, Haier itself possesses a highly comprehensive industrial ecosystem. From home appliances, smart homes, and logistics to the Industrial Internet and healthcare, Haier has made in-depth strategic layouts. Coupled with its years of industrial accumulation in the medical field, this not only enables Haier to gain a clearer understanding of the logic behind transformations in the healthcare industry during the investment process but also allows it to better empower its portfolio companies with industrial resources.

However, everything has two sides, and CVC also has certain limitations when targeting the medical field.The first point is the high operational costs and long operating cycles., Due to the nature of the industry, Corporate Venture Capital (CVC) typically requires a decade-long operational cycle to mature and generate returns. However, many enterprises prefer quick-in, quick-out investment strategies. Faced with the lack of immediate tangible results and the dual pressures of financial and temporal uncertainty, tech giants often hesitate, choosing either to suspend or withdraw their investments.

The second point is how to balance independence and synergy with the group during CVC operations.As previously mentioned, a major advantage of corporate venture capital (CVC) when investing in the healthcare sector is its accumulated industry resources. However, these resources do not automatically transfer to the internal CVC unit; they are sometimes constrained by the parent company’s core business divisions, thereby placing the internal CVC in a passive position. Consequently, it must face a strategic choice: whether to prioritize the financial objectives of the CVC itself or to better support the parent company’s core business.

Addressing this issue, Cai Zhengyuan, CEO of Haier Capital, stated that independence and synergy are not contradictory; in fact, their ultimate objectives are aligned. Therefore, when establishing investment goals and frameworks, it is essential to base them on the group’s overall industrial and strategic objectives. Only in this way can a firm maximize its competitive advantages. Furthermore, it should strive to provide investment and industrial empowerment to portfolio companies within its own “sphere of influence.” This approach represents both a process of horizontal expansion and vertical accumulation across projects, as well as a synergistic process of mutual value creation.

Finally, let me share a story. One year, after Contemporary Amperex Technology Co., Limited (CATL) signaled its intention to raise funds in the market, venture capital firms across China flocked to it, with hundreds of VCs queuing up at its doorstep. Ultimately, TCL Capital became one of the few investment institutions selected by CATL. This decision was largely driven by CATL’s recognition of the industrial synergy and complementary capabilities between TCL and CATL. Notably, prior to investing in CATL, TCL Capital had already invested in numerous upstream companies in CATL’s supply chain.

This represents the current potential opportunities for corporate venture capital (CVC), exemplified by home appliance manufacturers, in the medical venture investment market.

· References:

1. “Haier Capital’s Cai Zhengyuan: Industrial Synergy, Co-Creation of Value—The Enduring Truth of CVC” – Sohu.com;

2. “Unveiling the Realities of CVC Investment” – Zero2IPO Research;

3. “Home Appliance Giants ‘Compete’ in Medical Devices” – MedDevice Innovation Network.