Pear Therapeutics Bankruptcy Post-Mortem: Five Key Reasons Behind the Fall of the Digital Therapeutics Pioneer

Pear Therapeutics

Developer of Digital Healthcare Solutions

On April 7, digital therapeutics company Pear Therapeutics (hereinafter referred to as “Pear”) announced that it had filed a voluntary petition for Chapter 11 bankruptcy protection with the U.S. Bankruptcy Court for the District of Delaware. Pear laid off 170 employees, representing 92% of its workforce, including CEO and founder Corey McCann, retaining only a 15-member team to handle subsequent transition matters.

Thus, the former “first digital therapeutics stock” may fade into obscurity after its brief moment of listing glory. For those who have long followed the digital therapeutics sector, the phrase “watched him raise a grand mansion, watched him host lavish banquets, and watched his mansion collapse” perhaps best captures their current sentiments.

So, how did Pear reach its current state, what were the underlying causes, and what implications will this have for the future of digital therapeutics? VCBeat (WeChat ID: VCBeat), together with industry experts, has conducted a post-mortem analysis of its failure to provide reference for the sector.

Co-author: Dr. Fan Fangfang, Investment Partner at Guoke Longhui. Shanghai Guoke Private Equity Fund Management Co., Ltd. is an emerging private equity investment management platform that leverages strategic technological industry strengths and financial resources. Its investment focus primarily centers on semiconductors, artificial intelligence, 5G, and the Internet of Things (IoT). As an Investment Partner at Guoke Longhui, Dr. Fan Fangfang focuses on investment opportunities in medical devices, biopharmaceuticals, and digital health.

In 2013, Pear was founded in Boston, USA. This team, composed of interdisciplinary professionals from the biopharmaceutical, medical technology, and information technology sectors, is committed to redefining healthcare.

Corey McCann stated in an interview that during his tenure at McKinsey, he continued to pursue the interest and focus on neurological disorders that had characterized his academic career. However, as investment hotspots at the time were oncology and rare diseases, he grew increasingly frustrated by the inability to drive new therapies for brain-related conditions. Ultimately, he decided to found Pear Therapeutics, leveraging cognitive behavioral therapy as an innovative treatment approach.

Software, rather than pharmaceuticals, became the vehicle for this therapeutic approach, which later evolved into digital therapeutics. However, promoting public understanding and trust in software as a treatment modality required more robust evidence. This need drove the subsequent conceptualization of digital therapeutics: interventions or treatment measures provided to patients based on evidence-based medicine. These interventions are powered by high-quality software programs and are used for disease treatment (prevention, diagnosis, and control).

Since its inception, Pear has been a pioneer in digital therapeutics. At that time, the FDA was beginning to encourage innovation in digital health, and Pear quickly emerged as a benchmark in the field. In 2017, it was selected for the Software Pre-Certification Pilot Program, a new initiative aimed at developing regulatory approaches for medical software. In September of that year, it received the first De Novo clearance for a prescription digital therapeutic, ReSET.

This is a digital therapeutic for substance use disorders, designed to be used in conjunction with standard outpatient treatment for stimulant-, cannabis-, and cocaine-related substance use disorders. Leveraging the principles of cognitive behavioral therapy (CBT) and addressing the challenge of limited treatment access among patients with addiction, it transforms face-to-face treatment protocols into online, digital, and standardized interventions.

In the United States, addiction, a brain disease, can be described as an epidemic. In 2021, more than 46 million Americans struggled with addiction. The resulting economic burden was estimated to reach $700 billion annually (as of 2016). However, due to various factors, only 1.5% of individuals with substance use disorders receive treatment, representing a seemingly substantial market.

Compared with pharmacotherapy, digital therapeutics based on cognitive behavioral therapy and contingency management can avoid the side effects associated with medication, ensure treatment standardization and consistency, enhance accessibility through internet-based delivery, and prevent treatment discontinuation due to stigma related to face-to-face therapy.

Subsequently, Pear secured several additional approvals. In December 2018, ReSET-O, the world’s first digital therapeutic for opioid use disorder, received FDA approval for market launch. In March 2020, Somryst, indicated for chronic insomnia, was also approved for market launch. Notably, this product was the first prescription digital therapeutic submitted via the traditional 510(k) pathway and cleared through the Software Precertification Pilot Program, in which Pear participated as a developer.

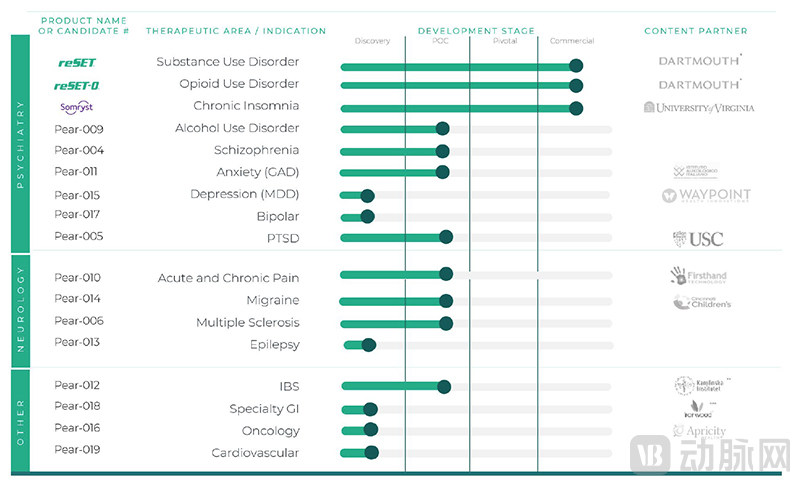

Pear Therapeutics rapidly replicated its validated product model across other indications, building an extensive product pipeline—in addition to the three approved products, its pipeline includes 14 other candidates.

Holding three FDA registrations and bearing the title of digital therapeutics leader, Pear achieved significant success in the primary market, completing eight rounds of public financing and raising a cumulative total of $409 million.

On June 22, 2021, Pear announced that it had entered into a definitive business combination agreement with the special purpose acquisition company (SPAC) Thimble Point Acquisition Corp. (“Thimble Point”) to go public via a SPAC merger. This milestone earned Pear the title of “the first digital therapeutics stock,” marking a highlight in the company’s history.

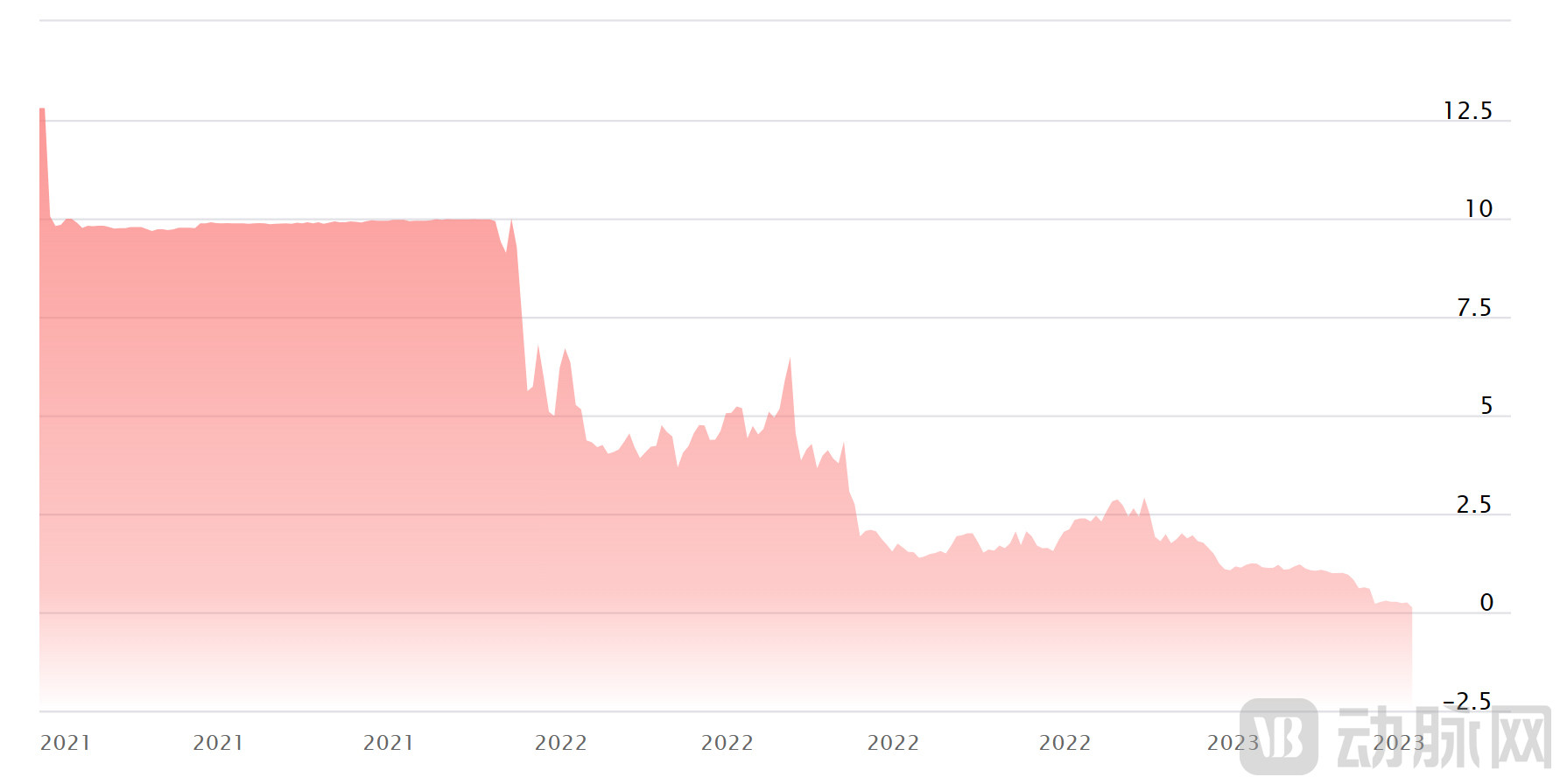

However, this moment in the spotlight did not last long. Pear, which had an initial valuation of $1.6 billion, began a “high-dive” plunge on its first day of official trading after the deal closed on December 3, with its stock price falling from $9 to under $2 in a very short period.

Pear’s stock price has plummeted rapidly since its IPO.

Just six months after its public listing, Pear began reducing operating costs through layoffs. First, in July 2022, it laid off 25 employees (9% of its total workforce). In November, Pear cut another 59 jobs (22% of its total workforce).

Since February 2023, the successive resignations of several senior executives have indicated that Pear is in a considerably difficult position. On March 17, Pear issued an announcement stating that it was exploring strategic alternatives, with the aim of securing additional financing through acquisitions, sale of the company, mergers, divestitures, licensing agreements, or other strategic transactions.

According to documents filed with the U.S. Bankruptcy Court, as of March 31, Pear’s engaged investment bank, MTS HealthPartner, had contacted more than 140 potential buyers, including pharmaceutical companies, insurers, healthcare providers, corporations, and pharmacies. Among them, 90 entities “participated or responded,” 24 were prepared to sign confidentiality agreements, and three submitted non-binding offers.

However, after considering all options, Pear ultimately decided to file for bankruptcy protection.

So, why did Pear, once a high-profile star, end up in such a dire situation? Drawing on multiple perspectives, we attribute Pear’s failure primarily to the following reasons.

Irrational Optimism: Inability of Revenue to Support Operations Is the Core Issue

The core issue is that Pear’s revenue was far too low. Prior to its IPO, Pear had issued optimistic projections, estimating that as three prescription digital therapeutics were gradually commercialized, it would achieve $22 million in revenue in 2022 and expand its revenue to $125 million in 2023.

The high growth in 2021 clearly misled Pear’s senior management, leading them to make irrationally optimistic judgments. Pear’s product sales revenue was $149,000 in 2020, but surged 24-fold to $3.748 million in 2021. This achievement was realized even though Somryst, its treatment for sleep disorders, had barely begun commercialization.

However, reality dealt a harsh blow to Pear’s senior management. Throughout 2022, Pear generated only $12.694 million in revenue (including $10.417 million from product sales), roughly half of the $22 million revenue target it had projected at the time of its IPO. Even compared with the full-year guidance of $14–16 million provided in mid-2022, there remained a significant shortfall.

Although Pear’s revenue is rising rapidly, it is unfortunately spending even more.

Although this represents a threefold increase compared to 2021, following this trend, the anticipated target of $125 million for 2023 at the time of listing is clearly wishful thinking.

As of February 2023, Pear had issued over 45,000 prescriptions, falling slightly short of the estimated 50,000–60,000 prescriptions projected for 2022 at the time of its market launch. Meanwhile, a comparison with the previous year’s semi-annual report reveals that prescription volumes actually declined in the second half of 2022. According to data available at that time, Pear had already issued more than 20,000 prescriptions in the first half of 2022, adding to the over 14,000 prescriptions written throughout all of 2021. This indicates that only 11,000 prescriptions were actually issued in the second half of the year.

Furthermore, the annual prescription fulfillment rate and payment rate have also gradually declined. According to the annual report, the full-year prescription fulfillment rate was 53%, and the payment rate was 41%. In last year’s semi-annual report, Pear Therapeutics publicly disclosed the prescription fulfillment and payment rates for the first two quarters: Q1 stood at 57% and 50%, respectively, while Q2 recorded 56% and 45%, reflecting a downward trend.

In mid-last year, Pear boldly claimed that it would raise both its fulfillment rate and payment rate to the level of 50-65%. Ultimately, the fulfillment rate managed to meet the target, but the key metric of payment rate fell significantly short of the goal.

Corey McCann expressed deep sentiment in his LinkedIn post: “We have demonstrated that clinicians can easily prescribe digital therapeutics. We have shown that patients engage with these products. We have proven that our products improve clinical outcomes. We have established that our products save payers money. Most importantly, we have shown that our products truly help patients and their clinicians. Yet this is not enough; payers retain the ability to deny reimbursement for therapies that are clinically necessary, effective, and cost-saving.”

For an emerging industry, it is not surprising to face skepticism. The key lies in improving products and services to alleviate payers’ concerns. However, Pear may have been constrained by circumstances and failed to refine its offerings as it should have.

Having been launched earlier, Pear’s digital therapeutics are now merely average. DynamiCare Health, which also develops digital therapeutics for addiction recovery, has directly compared Pear’s ReSET and ReSET-O with its own products, claiming superiority in terms of reward convenience, course duration, fidelity of contingency management, customer satisfaction, and compliance with federal anti-fraud scrutiny. While this assessment may not be entirely objective, it does indicate that Pear’s products are far from perfect.

In addition to the three products that have completed registration, Pear has as many as 14 products in its development pipeline.

It is worth noting that Pear’s R&D expenses are by no means low. In 2022, its R&D spending reached $48.31 million, more than four times its revenue. However, it is highly likely that little of this expenditure was allocated to its flagship products, given that all 14 of Pear’s pipelines under development require investment.

"All eggs in one basket": The business model is overly singular.

Dr. Fan Fangfang, Investment Partner at Guoke Longhui, believes that Pear previously collaborated with pharmaceutical companies to explore both B2B and B2C models; however, these efforts yielded only fleeting achievements, resulting in a business model overly reliant on in-hospital prescriptions.

On the B2B front, Pear once garnered favor from Novartis and partnered with it in March 2018 to develop prescription digital therapeutics for schizophrenia and multiple sclerosis (MS). However, the collaboration yielded limited results, and the agreement was terminated in June 2020. Nevertheless, this partnership generated $82.61 million in deferred revenue for Pear, substantially supporting its operations.

In the consumer segment, Pear entered into a collaboration and license agreement with Sandoz, a Novartis subsidiary, in April 2018, commercializing ReSET and ReSET-O for an upfront payment of $20 million. As no actual revenue was generated during the subsequent commercialization process, Sandoz terminated the agreement in October 2019, requiring Pear to refund the $20 million.

Perhaps due to overly optimistic expectations of the existing in-hospital prescription model, Pear did not pursue further exploration in either the B2B or B2C sectors thereafter, rendering its business model somewhat singular.

Misjudgment in direction: Would choosing another path be better?

On the other hand, the market potential for addiction withdrawal treatments may not be as optimistic as Pear had imagined. The prevalence of addictions to stimulants, marijuana, and cocaine, along with the associated opioid addiction, in the United States is not merely a medical issue but is rooted in complex social contexts. One contributing factor is the U.S. government’s relatively lax regulation of soft drugs.

Although the COVID-19 pandemic has exacerbated the severity of substance use disorders, U.S. government regulations have become increasingly lenient due to fiscal revenue considerations. Compared with pre-pandemic levels, drug overdose deaths nationwide increased by 18% in 2020, while cocaine-involved overdoses rose by 26%. As of June 2021, 18 U.S. states had legalized non-medical cannabis, and an additional 13 states had reduced criminal penalties for non-medical cannabis use—just a decade ago, non-medical cannabis was illegal in all 50 states.

Even more strikingly, in February 2021, Oregon became the first U.S. state to decriminalize the possession of “hard drugs” such as heroin, methamphetamine, and cocaine. Under this policy, possessing less than 1 gram of heroin or MDMA (ecstasy), or less than 2 grams of cocaine or methamphetamine, is no longer treated as a criminal offense; instead, individuals face a $100 fine or are required to undergo a health assessment. In November 2021, New York City became the first city in the United States to announce the establishment of “safe drug consumption sites,” where people are allowed to use drugs under the supervision of trained professionals.

Pear’s annual report reveals that its top three prescription sales customers are all state government agencies. Coupled with the fact that all support and service revenues also stem from a certain state’s Medicaid program, these sources collectively account for as much as 54% of its total revenue. Against this backdrop, achieving high-speed growth is clearly unrealistic.

In contrast, mental health conditions such as depression have emerged as a rapidly growing segment in telemedicine. Although the utilization of telemedicine has declined significantly in the United States following the end of the COVID-19 pandemic, dependence on telemedicine for psychiatric and psychological disorders, including depression, continues to rise, sustaining robust growth.

Take BetterHelp, Teladoc’s mental health-focused subsidiary, as an example: its revenue has grown rapidly over the past year, reaching the billion-dollar mark and becoming a key pillar for Teladoc, which has seen a significant decline.

Perhaps, if Pear had initially chosen a different indication, leveraging the authority of prescription digital therapeutics and capitalizing on the booming development of telemedicine for psychiatric and psychological disorders, it might have achieved a different outcome.

SPAC Listings: “Much Ado About Nothing”

Pear’s predicament was also caused by its adoption of a special-purpose acquisition company (SPAC) listing, which resulted in a failure to raise the anticipated capital.

In 2020, the pandemic disrupted many initial public offerings (IPOs), as valuations of IPO-bound companies failed to gain recognition in the capital markets, raising the risk of issuance failures. Against this backdrop, Special Purpose Acquisition Companies (SPACs) quietly emerged. A SPAC is first established in the United States as a special-purpose entity holding only cash and no actual business operations. It enables a target company to go public through a merger, while simultaneously providing access to the SPAC’s capital.

This model helps companies achieve dual assurances of going public and raising capital, while the target company only needs to meet the minimum listing requirements of NASDAQ. SPAC listings have a high success rate and are less affected by external regulatory factors; compared with traditional IPOs, the underwriting fee rate is lower, around 2%-5%; the lock-up period after listing is generally only six months, which is welcomed by institutional investors.

Pear raised approximately $400 million through its SPAC listing, comprising $276 million from the Thimble Point trust account and $125 million from an oversubscribed PIPE (Private Investment in Public Equity) transaction. However, as Pear went public during the waning phase of the SPAC boom when valuations were generally depressed, and with the global economy entering a downturn in the second half of 2022, its stock price plummeted shortly thereafter, resulting in secondary market fundraising that fell far short of expectations.

Dr. Fan Fangfang stated that, given Pear’s $1.6 billion high valuation at the time of its IPO and the oversubscription of its PIPE (Private Investment in Public Equity) offering, coupled with its high debt ratio over the past year, it is evident that senior management held irrational expectations about the market at the time of listing. They likely agreed to above-expectation “performance bet-on agreements” with the acquirer Thimble Point—namely, redemption clauses. However, a performance slump in the first year after going public triggered investors’ redemption clauses, which may be one of the reasons for its current predicament.

Spendthrift, spending money like water

Fundraising fell far short of expectations, and revenue performance was also disappointing. Under such circumstances, implementing austerity measures to navigate tough times should have been prioritized early on. However, a review of Pear’s annual report reveals its spending levels to be staggering. Research and development expenses rose by 30%, from $37.041 million in 2021 to $48.311 million; general sales and administrative expenses increased by 18%, from $67.619 million to $79.551 million. Total operating costs for the year reached as high as $123 million.

In comparison, Dario Health, a digital therapeutics company that went public as early as 2016, did not report high revenue for the full year 2022; however, its revenue of approximately $27 million was nearly three times that of Pear Therapeutics during the same period. Moreover, Dario Health maintained strict cost control, with R&D expenses of $19.649 million, general sales and administrative expenses of $46.816 million, and total annual operating costs of $66.465 million—only half of Pear Therapeutics’ level.

A comparison reveals Pear’s profligate spending. Had cost controls been strictly enforced from the outset, the company could have extended its runway. How the internal and external environments might have evolved during that period remains uncertain.

Nevertheless, Pear’s products retain their value. Despite mediocre prescription fulfillment and payment rates, the company still achieved a threefold revenue growth within one year; had it not encountered turbulence in the second half of the year, its performance might have been even stronger. This is further corroborated by the responses from entities contacted during the brief two-week period in which Pear explored strategic alternatives.

Jiang Tianjiao, Dean of VCBeat Institute, also noted that as a software-based medical device, digital therapeutics offer more stable output (compared to manual delivery), lower costs (with zero marginal cost), and more convenient real-world data collection (as product usage inherently generates feedback data). These represent unique value creation by digital therapeutics, constituting aspects that cannot be replaced by pharmaceuticals or traditional medical devices.

Pear’s failure was not solely attributable to issues with digital therapeutics; rather, it resulted from a confluence of internal and external factors. On one hand, its business model had inherent weaknesses that were exacerbated by the prevailing socioeconomic environment, coinciding with a downturn in financial markets that left the company unable to sustain operations until profitability. On the other hand, Pear held overly optimistic expectations for the future and failed to practice fiscal discipline from the outset. These factors collectively led to Pear’s ultimate demise.

We cannot deny the recent hype surrounding digital therapeutics, but this phenomenon is not unique to this field. From the perspective of Gartner’s Hype Cycle for Emerging Technologies, every industry undergoes value chain restructuring and consolidation. This is an inevitable stage in the development of new technologies. By drawing on past lessons and reintegrating core technologies and innovative resources, the digital therapeutics industry will enter a period of steady recovery, ultimately delivering genuine value to both physicians and patients.

References:

Li Zhiwei, People’s Daily International: “International Observation | Why Has the U.S. Government Legalized Marijuana?”

Katie Adams,Medcitynews.com:Telehealth visits for mental health continue to rise despite dropping in every other specialty