Global Medical Health Industry Capital Report Q1 2023: Signs of Market Recovery Amid Shifting Investment Hotspots

Core Viewpoints

I. In Q1 2023, both the number of financing deals and the total financing amount experienced a quarter-on-quarter decline, falling significantly short of the capital surge seen in 2021 and showing only modest growth compared to the same period in 2020. However, unlike 2020, when funding was heavily concentrated among top-tier enterprises, Q1 2023 offered greater room for development for startups.

II. The capital market shows signs of recovery, yet the structure of hot sectors has shifted: digital therapeutics have cooled down, while overseas virtual care has maintained its momentum following an initial surge, with care services progressively moving toward specialization and refinement; in biopharmaceuticals, CXO has faced a downturn, but innovative drugs related to ophthalmology, dermatology, geriatrics, and rare diseases have ushered in new development opportunities; in medical devices, previously heated fields such as IVD, AI-enabled devices, and brain science have witnessed a dual decline in both financing amounts and the number of financing deals, whereas emerging companies in orthopedic surgical robots and endoscopic robots demonstrated active performance in the first quarter.

III. Overseas investment institutions are heavily betting on the gene therapy sector, repeatedly increasing their stakes in innovative pharmaceutical companies; domestic investment institutions are exhibiting a more cautious approach, favoring the CXO, innovative drug, and upstream medical device sectors.

IV. European Countries Increase R&D Investment in Biomedicine, While the Jiangsu-Zhejiang-Shanghai Region Accounts for Half of Domestic Financing Deals.

V. Top 10 Most-Funded Companies in Q1 2023: Sono Bello Secures Over $500 Million to Claim the Top Spot, with Chinese CDMO Companies Making the List.

VI. The implementation of a full-market registration-based IPO system in China’s A-share market is expected to attract more companies to go public; overseas benchmark digital therapeutics companies have faced setbacks after their listings, prompting companies in this sector to adjust their strategic directions.

I. Trends in Global Healthcare Industry Financing Changes in Q1 2023

1.1 Decreasing Capital Concentration: The Capital Market Continues to Leave Room for Startups

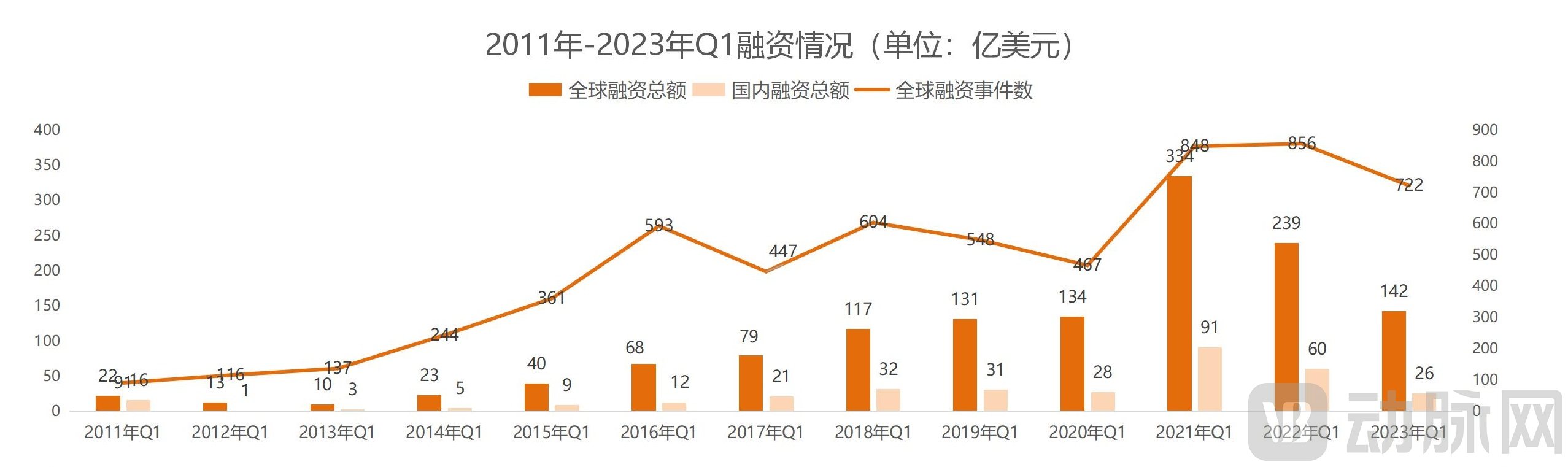

In Q1 2023, there were a total of 722 financing events in the global primary healthcare market, with the total financing amount reaching approximately $14.2 billion. Compared to the capital surge throughout 2021 and the lingering momentum from Q1 2022, the situation in Q1 2023 was more akin to that of Q1 2020. It achieved stable, marginal growth over Q1 2020, which had exceeded expectations. Notably, the impact of the black swan event—the COVID-19 pandemic—barely dampened investment enthusiasm in the foreign primary healthcare market during Q1 2020. In fact, following severe turbulence in overseas capital markets, financing demands in sectors such as telemedicine, in vitro diagnostics (IVD), and vaccine R&D were met with even faster responses. Nevertheless, compared to the high capital concentration observed in 2020, Q1 2023 still retained market space for startups to complete their initial financing rounds.

1.2 Million-Dollar Projects Overtake; Biopharma’s Multi-Million-Dollar Financing Advantages Stand Out

In Q1 2023, the global healthcare industry saw 35 financing deals exceeding $100 million each, accounting for approximately 42% of the total financing amount in Q1, indicating that the “top-heavy effect” continues to persist.

Although it had already pulled ahead of other sectors through large-scale financing, the biopharmaceutical sector’s advantage in the tens-of-millions-of-dollars funding bracket became even more pronounced in Q1 2023, amounting to roughly twice that of digital health, which ranked second.

Unlike the landscape since 2020, which was dominated by projects with financing in the tens of millions of dollars, Q1 2023 saw a predominance of deals in the single-digit millions, primarily involving startups in the medical device and digital health sectors.

II. Hot Sectors in Global Healthcare Investment and Financing in Q1 2023

2.1 Medical Devices and Digital Health Sector Cools Down as Capital Adopts a Wait-and-See Stance

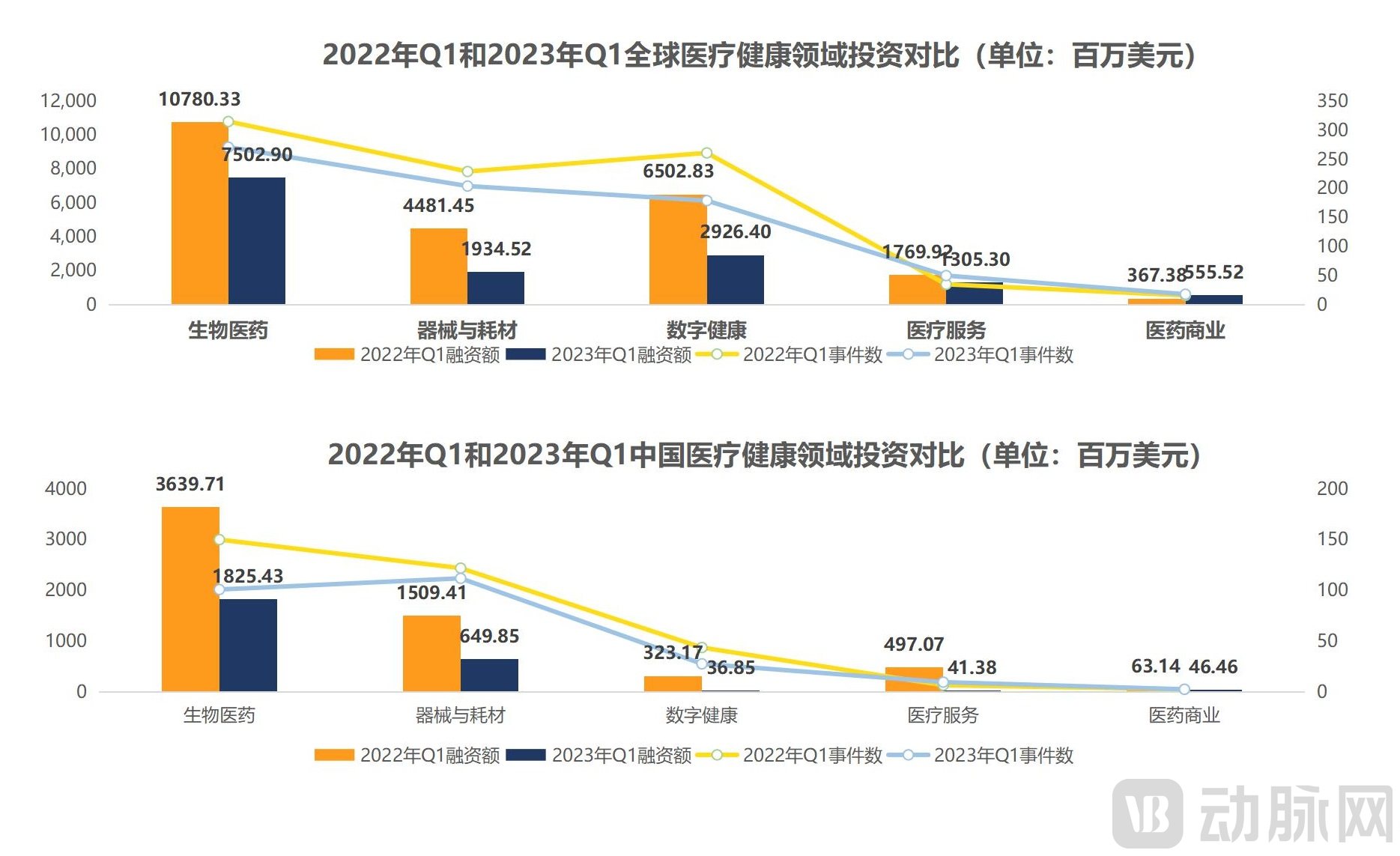

In Q1 2023, total global financing across all sectors except pharmaceutical distribution declined compared to the same period in 2022. The medical devices and digital health sectors cooled significantly in the first quarter of 2023, with total financing dropping by more than 50% quarter-over-quarter.

In the medical device sector, investment firms have exercised caution, resulting in smaller individual financing rounds, with only a few high-barrier subsectors securing substantial funding. In Q1 2023, the total financing amount in the device sector decreased by 57% quarter-on-quarter, while the number of financing events declined by only 10. There were just two deals exceeding $100 million. Financing amounts were predominantly in the millions-of-dollars range. Companies that secured large-scale funding were concentrated in high-barrier fields such as heart failure treatment, brain-computer interfaces (BCI), and regenerative medicine. Notable examples include Yongrenxin, an artificial heart developer that completed a Series A financing round of nearly $100 million, and Ruitai Biologics, a developer of regenerative repair materials that raised RMB 100 million in its Series A+ round.

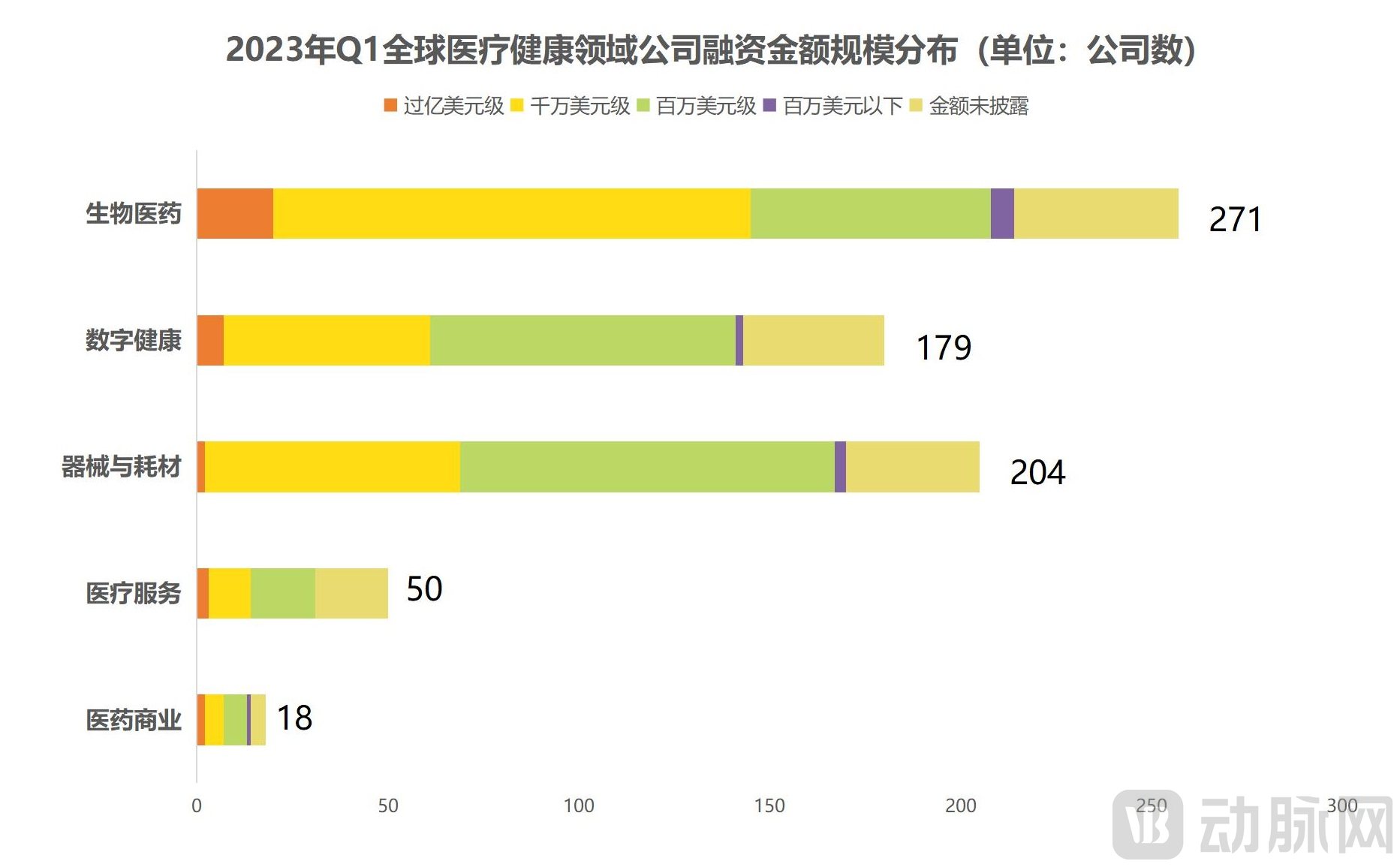

2.2 Hot Global Financing Tags: Biopharmaceuticals, Internet + Healthcare, Other Consumables

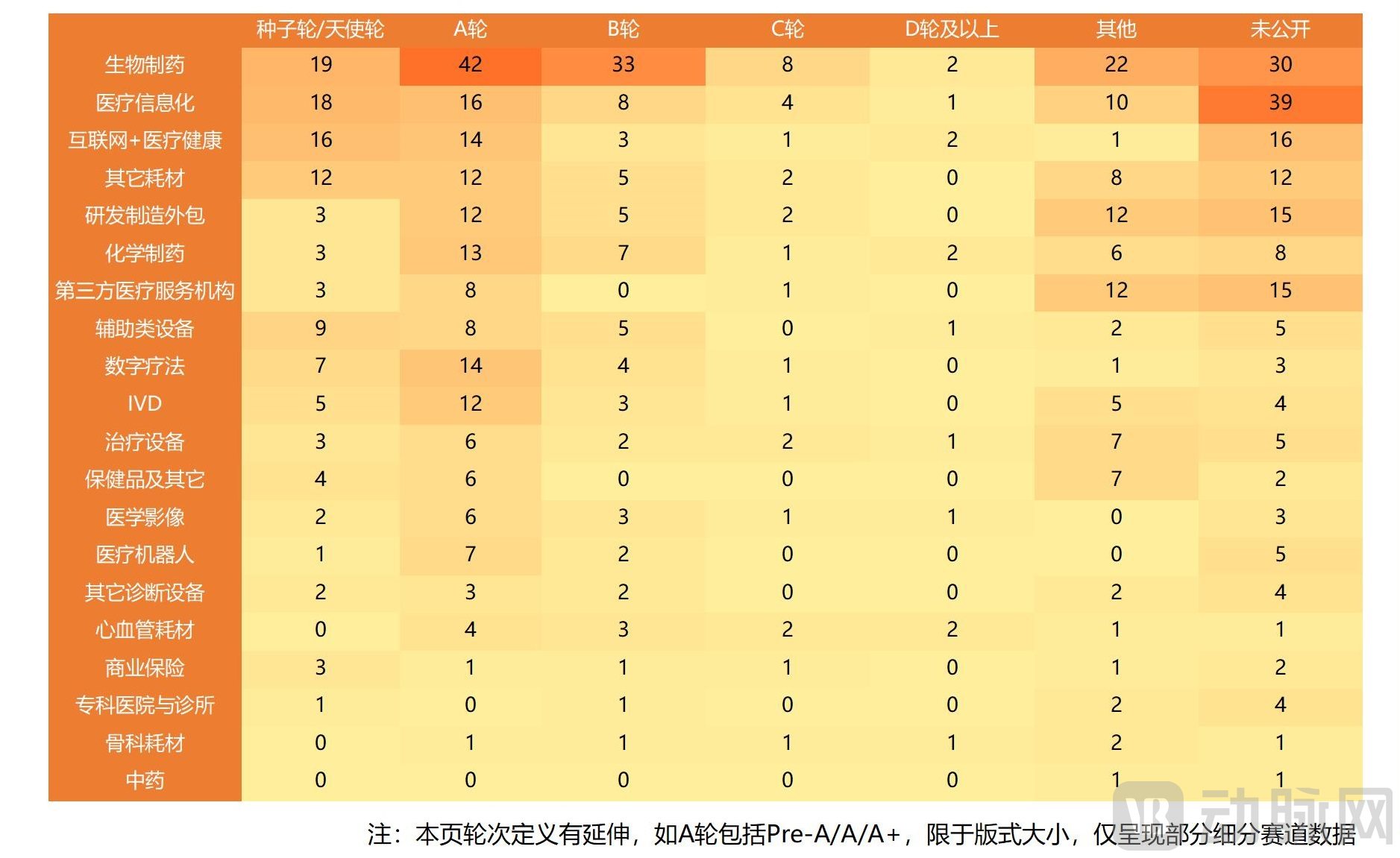

In Q1 2023, tags such as biopharmaceuticals, healthcare informatics, Internet + Healthcare, and other consumables exhibited high popularity.

From the perspective of funding rounds, investment institutions continue to favor early-stage projects. There were 298 financing events before Series A, accounting for 41% of the total number of transactions. Only a small fraction of companies have progressed beyond Series D; these enterprises either possess or are on the verge of launching commercially viable products. For instance, Hemei Pharmaceutical completed a Series D financing round of nearly RMB 300 million, with two drug candidates covering three indications currently in Phase III clinical trials. Haijieya Medical’s self-developed combined cryo-ablation device, Kangbo Knife, has entered China’s Green Channel for Special Review of Innovative Medical Devices. This indicates that investment institutions are currently focusing on early-stage projects while simultaneously increasing their bets on companies with proven commercialization capabilities.

2.3 Cell and Gene Therapy Gains Momentum, with CGT CDMOs Riding the Wave

Compared with Q1 2022, both the number of financing deals and the total disclosed financing amount in the biopharmaceutical sector declined. However, amidst the sluggish financing market, cell and gene therapy emerged as a bright spot, attracting significant attention from investors. Financing rounds this quarter were primarily concentrated at Series A, accounting for 23%, while Seed/Angel and Series B rounds remained at similar levels.

This quarter has seen a succession of breakthroughs in China’s cell and gene therapy (CGT) sector, with Huayi Lejian, Jiayin Biologics, Huida Gene, Bendao Gene, Anlong Biologics, and Nuowei Technology successively receiving Investigational New Drug (IND) approvals for their products. This signals that Chinese-made adeno-associated virus (AAV) gene therapies are entering a fast track of mutually reinforcing and sustainable development across the industry chain. Due to the high production and R&D costs, as well as the complex manufacturing processes associated with CGT therapies, the CGT sector relies more heavily on contract development and manufacturing organizations (CDMOs) than traditional pharmaceuticals, with stronger sustained demand. The continued momentum and promising outlook of the CGT industry have further fueled market growth for CGT CDMOs.

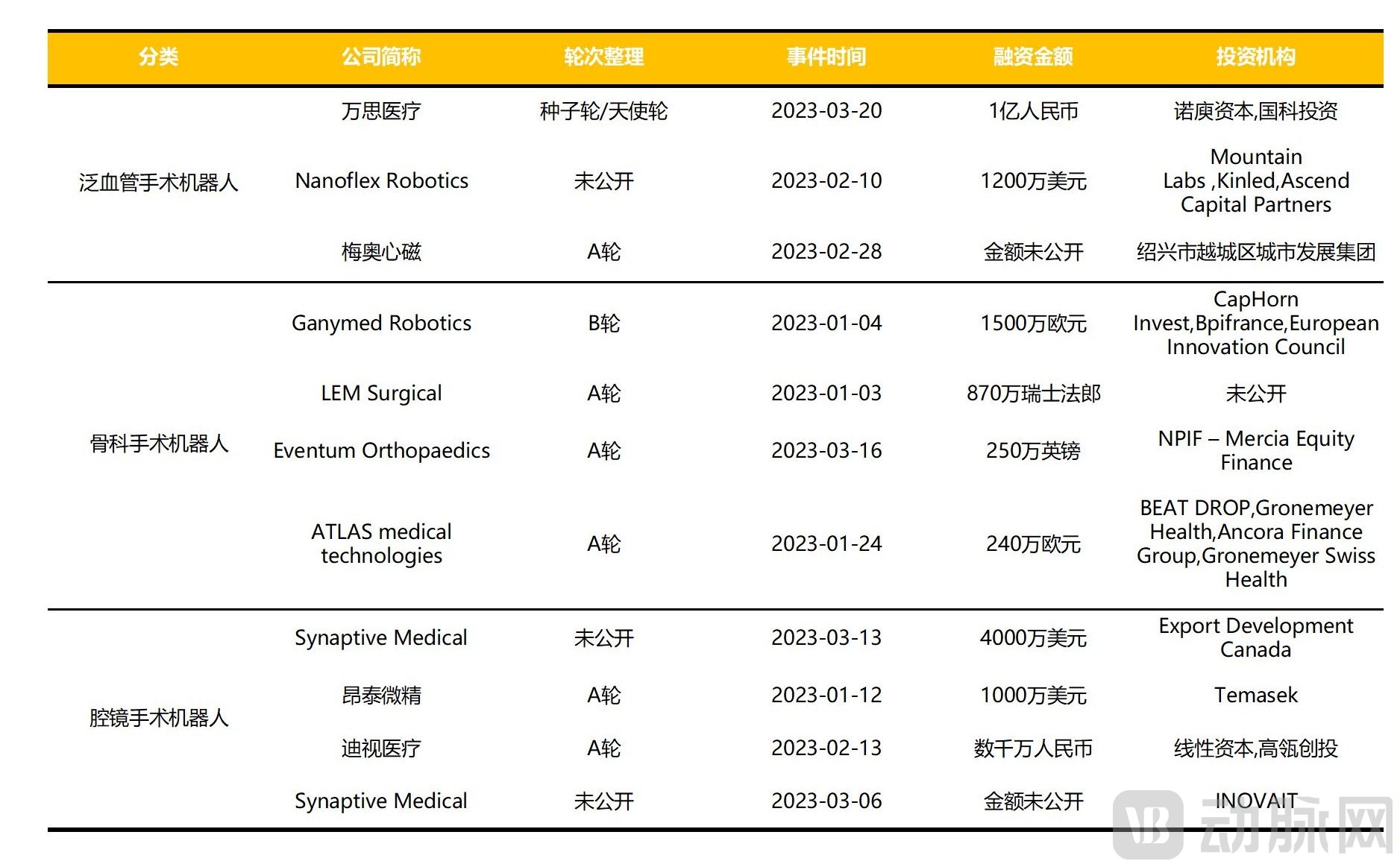

2.4 Surgical robot financing remains hot, with early-stage projects drawing significant attention

In Q1 2023, there were 11 financing deals in the global surgical robotics sector, each exceeding $100 million. Financing was concentrated in early-stage companies, with a higher number of recipients among orthopedic and laparoscopic surgical robotics firms.

In 2022, the surgical robotics sector secured over $800 million in financing, with momentum remaining strong in Q1 2023. The heightened investor interest in early-stage surgical robotics projects may be linked to product commercialization. According to data from the National Medical Products Administration (NMPA), 15 surgical robotic products received approval in 2022, and nine products obtained NMPA registration certificates in Q1 2023 alone.

The surgical robotics sector is expected to see sustained growth in financing activity. In March 2023, seventeen ministries and commissions, including the Ministry of Industry and Information Technology, the Ministry of Education, and the Ministry of Public Security, jointly issued the “Implementation Plan for the ‘Robotics+’ Application Initiative,” drawing significant attention from all sectors of society.

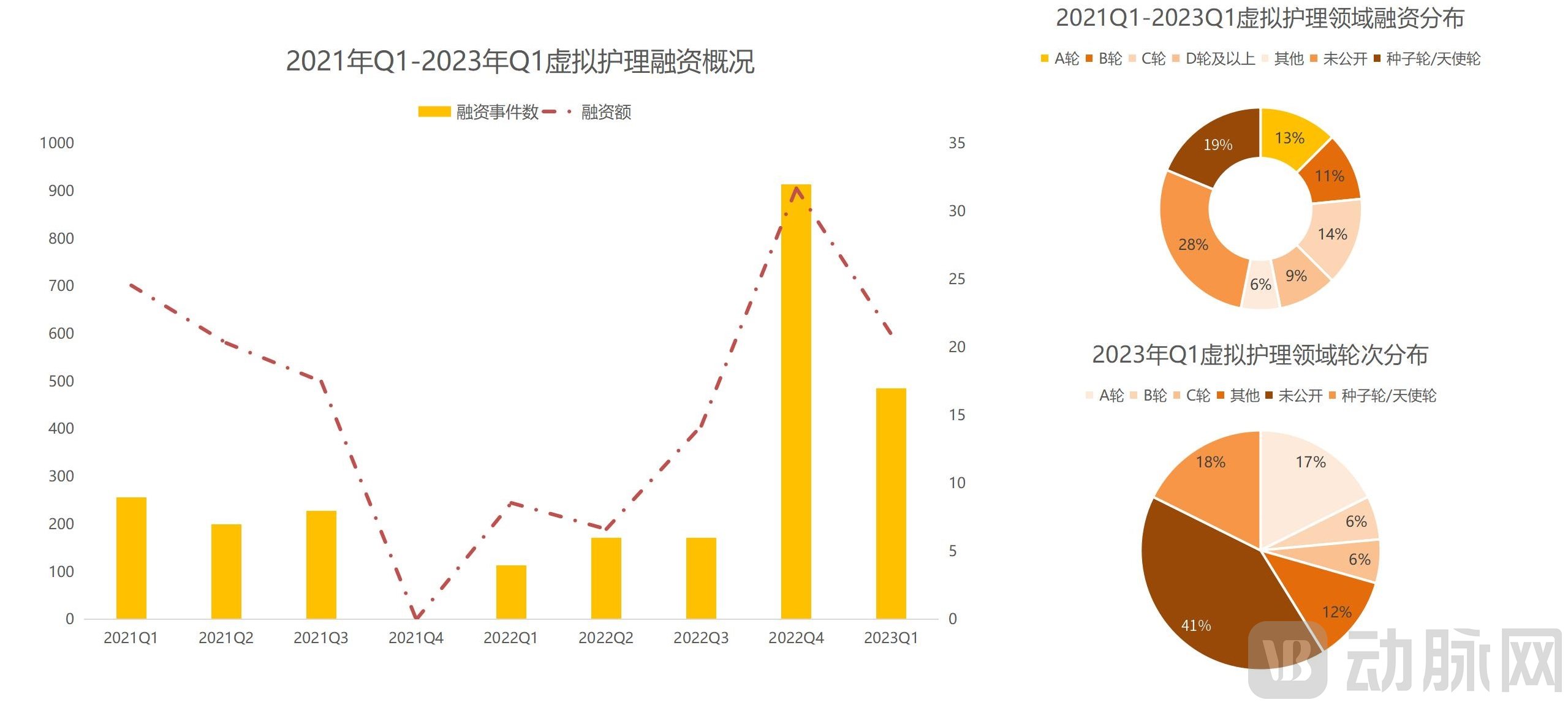

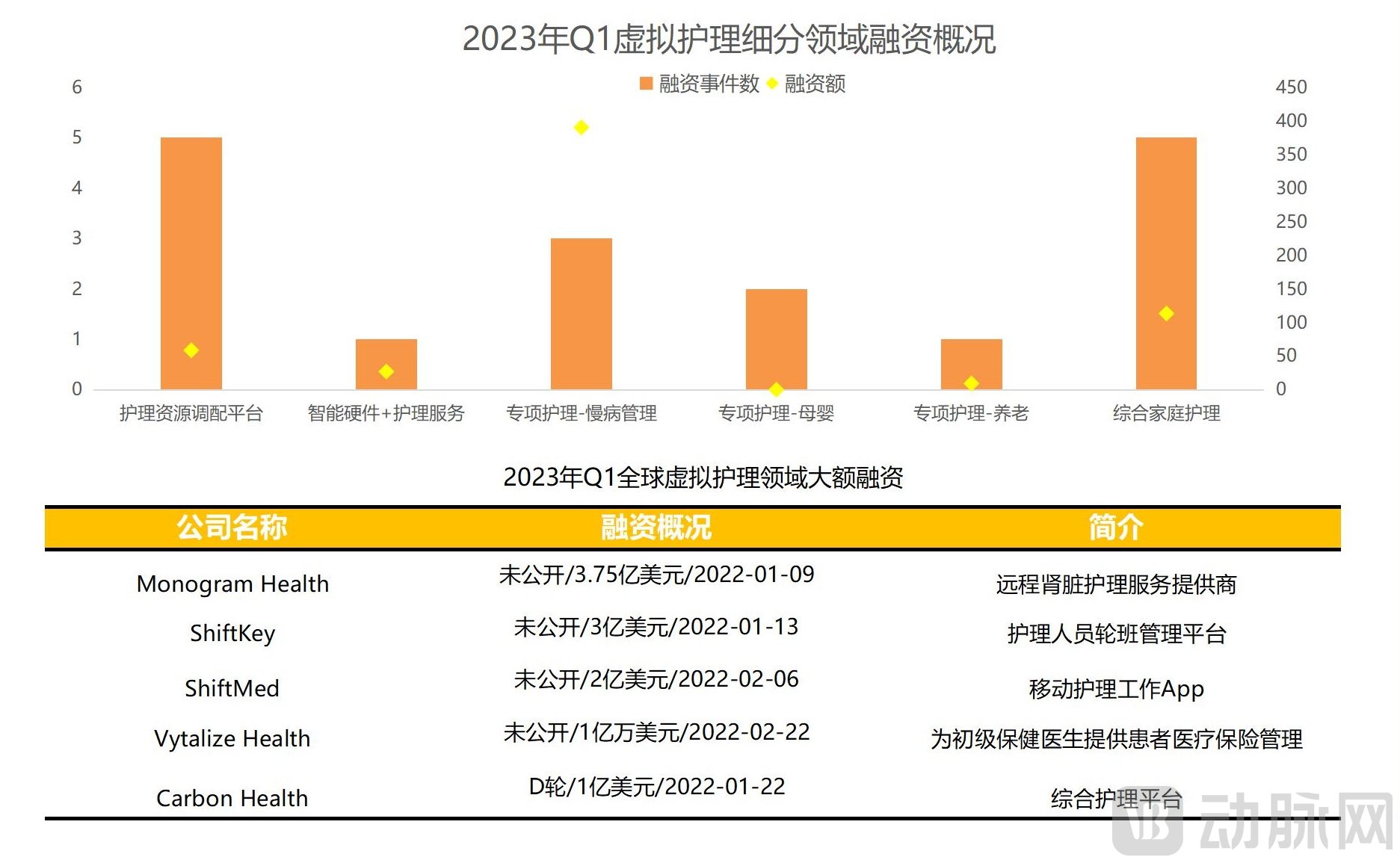

2.5 Enhanced Specialization and Refinement: Companies Continuously Fill Gaps in the Virtual Care Sector

The Ongoing Impact of the Healthcare Workforce Exodus, Exemplified by the United States: Data from the U.S. Department of Labor in 2022 showed that over 500,000 employees resigned from the healthcare and social assistance sector in September. Furthermore, a report released early in the year by the American Medical Association indicated that one in five physicians planned to leave the medical field within two years. Driven by these factors, the virtual care sector has experienced a surge in financing since the fourth quarter of 2022. Beyond the public’s growing adaptation to virtual technologies following the waning of the pandemic crisis, a more critical driver is the persistent shortage of professional healthcare resources. Major virtual care platforms can effectively bridge hospitals and home settings, delivering specialized services.

It is worth noting that since entering 2023, the businesses of relevant enterprises have become increasingly segmented. In addition to nursing resource allocation platforms and physician tools oriented toward hospitals, high-end services targeting specific niches—such as maternal and infant care, management of specific diseases rather than comprehensive chronic conditions, and home-based care for the elderly—have further developed and demonstrated strong revenue-generating capabilities.

III. Analysis of Active Healthcare Investment Institutions in Q1 2023

3.1 Foreign Investment Institutions Heavily Bet on the Gene Therapy Sector, Repeatedly Increasing Stakes in Innovative Pharmaceutical Companies

In Q1 2023, the most active investors in global healthcare were GV, the investment fund under Google, and OrbiMed, a vertical investment fund specializing in the healthcare industry.

Compared with Q1 2022, the total number of investments by foreign institutions remained stable, but domestic investment firms significantly slowed their pace in early 2023, with only Qiming Venture Partners and YS Capital making it into the global top 10 most active investors.

Specifically, foreign pharmaceutical companies specializing in gene therapy technologies have repeatedly received additional investments from prominent venture capital firms, with funding amounts concentrated at the hundred-million-dollar level. For example, Aera Therapeutics, a developer of gene editing technologies, has received two rounds of additional investment from GV since its inception. Its proprietary delivery technology platform is expected to precisely deliver various payloads—including gene therapies, mRNA, RNA interference (RNAi), antisense oligonucleotides (ASOs), and gene editing systems—to a wide range of human tissues and organs, significantly expanding the spectrum of diseases treatable by these therapies. Other pharmaceutical companies that have garnered favor from active institutional investors include Chroma Medicine, a developer of genetic medicines; Metagenomi, a gene technology research company; and Ensoma, a genomic medicine developer.

3.2 Domestic Investment Institutions Show a More Rational Approach, Favoring CXO, Innovative Drugs, and Upstream Medical Device Sectors

In Q1 2023, Qiming Venture Partners made nine investments, followed by Yansheng Venture Capital, Sequoia Capital China, and Yida Capital, which ranked second, third, and fourth with seven, six, and fewer investments, respectively.

Compared with Sequoia Capital China Fund’s 22 investments in Q1 2022, and Qiming Venture Partners’ and Hillhouse Investment’s 14 and 13 investments respectively, domestic investment institutions have shown a more restrained performance this quarter.

Specifically, active domestic investment institutions are favoring the CXO, innovative drug, and upstream medical device sectors. CDMO service provider Oli Biotech and CRO+CDMO service provider Pharmaron Biologics both received additional investments from two active institutions. Yuansheng Venture Capital invested twice in Boside, a company in the upstream imaging sector. Saipu Filtration, which provides filtration consumables to pharmaceutical companies, received additional investments from three active institutions: Yida Capital, Huimei Capital, and Hankang Capital. Additionally, several innovative pharmaceutical companies have attracted the attention of active investors, including small-molecule new drug developer Zhengxiang Pharmaceutical, tumor immune cell product developer Yuanqi Biotechnology, and drug development service provider Meinuo Pharmaceutical.

IV. Review of Healthcare IPOs Listed in Q1 2023

4.1 US stocks fail to rebound as expected; China’s market-wide registration-based IPO system is poised to attract more companies to list

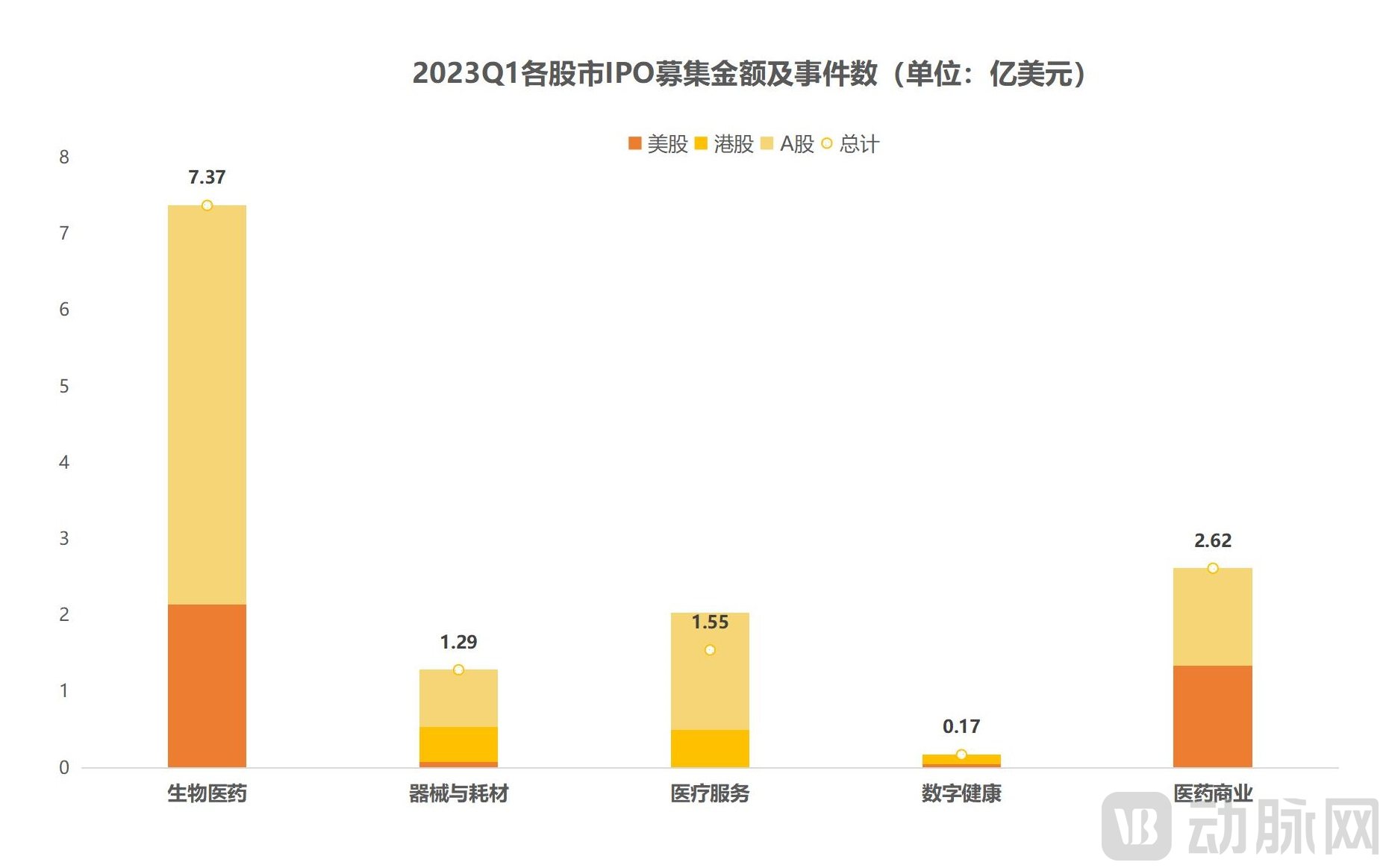

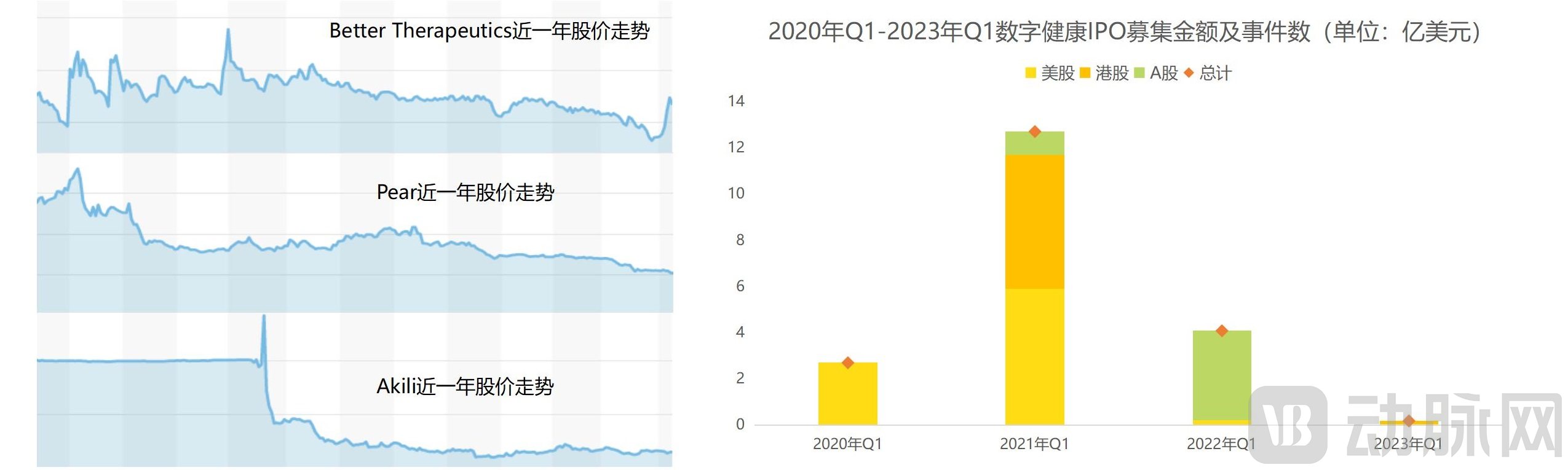

According to VBInsight, in Q1 2023, a total of 34 companies were listed on the A-share, U.S., and Hong Kong stock markets, which was lower than the same period in 2022; the total amount raised as publicly disclosed was approximately $1.3 billion, only about one-quarter of that in the same period in 2022.

Although the U.S. stock market has not rebounded as quickly as expected, a new trend has emerged in China: the China Securities Regulatory Commission (CSRC) has released for public comment the key institutional rules governing the comprehensive implementation of the registration-based IPO system (“Public Comment”). This marks the formal rollout of the registration-based system across the entire A-share market, and the more inclusive listing process on the Main Board is expected to attract a greater number of domestic healthcare companies.

4.2 Underperformance of Related Companies in the Secondary Market; Digital Health Firms Prioritize Primary Market Financing

In the digital health sector, which has been hit particularly hard, it is worth noting that the stock performance of three listed benchmark companies in digital therapeutics has been dismal. Akili’s shares experienced extreme volatility on their Nasdaq debut, triggering multiple trading halts, and had plummeted 81% from their peak by the first quarter of 2023. Better Therapeutics saw its share price drop by more than 87%. Meanwhile, prior to filing for bankruptcy liquidation in April 2023, Pear had incurred losses of $123.4 million against revenues of only $12.7 million.

This situation has also affected the growth expectations of a significant number of digital health companies. Some mature enterprises have prioritized continued fundraising over going public, while simultaneously restructuring their operations. However, although digital therapeutics have currently stumbled in the secondary market, the challenges they face—such as high pricing and unclear profitability models—provide valuable lessons for other emerging companies. In the future, the market is likely to see relevant enterprises exploring new directions.

V. Regional Distribution of Global Healthcare Investment and Financing Hotspots in Q1 2023

5.1 Global: The United States Leads Globally, with China and the US Accounting for 86% of Total Global Financing

In Q1 2023, the five countries with the highest number of global healthcare financing deals were the United States, China, the United Kingdom, France, and Germany.

In Q1 2023, the United States led globally with 295 financing deals totaling $9.563 billion (approximately RMB 65.8 billion), followed closely by China. Together, the U.S. and China accounted for 86% of the total global financing amount and 76% of all financing deals.

In addition, European countries have intensified their investments in the research, development, and production of biopharmaceuticals, leading to a strong growth trend in biopharmaceutical innovation. Notably, healthcare financing activity in France and Germany has surged significantly, propelling them into the ranks of the top five hotspot regions.

From the perspective of investment hotspots, biopharmaceuticals and medical devices are the sectors that have garnered global attention this quarter.

5.2 China: Jiangsu Takes the Lead, with Jiangsu, Zhejiang, and Shanghai Accounting for Half of All Financing Deals

In Q1 2023, the five regions in China with the highest concentration of healthcare and medical investment and financing activities were, in order, Jiangsu, Shanghai, Guangdong, Beijing, and Zhejiang.

Jiangsu has recorded a cumulative total of 59 financing events, raising $502 million (approximately RMB 3.5 billion), making it the city with the highest number of financing deals in the first half of the year. After surpassing Beijing in the number of financing events in 2020, Jiangsu has continued to outperform Shanghai this quarter.

The Jiangsu-Zhejiang-Shanghai region remains the backbone of healthcare innovation in China, with 134 financing deals accounting for half of the nation’s healthcare financing activity in Q1 2023.

VI. Top Financing Records of Healthcare Companies in Q1 2023