ICU Capacity Tripled in Three Years Amid Sustained Expansion; CRRT Manufacturer Shanyuanshan Hits Record High Share Price

SWS MEDICAL

Blood Purification Equipment R&D and Manufacturer

Edan Instruments

Developer, manufacturer, and service provider of medical electronic equipment products

Mindray

Medical Device R&D Manufacturer

ICU: The Last Line of Defense for Patients’ Lives. Here, the rhythmic beeping of ventilators, monitors, and various other medical devices intertwines with the hurried footsteps of healthcare workers, composing the main theme of this critical frontline.

According to the paper “Prediction of Short-Term Allocation of Hospital Health Resources in China” published by Wang Xiling and colleagues from the School of Public Health at Fudan University, in 2021, China had 4.37 comprehensive ICU beds per 100,000 permanent residents. Even in Beijing and Shanghai, which have the most abundant medical resources, there were only 6.25 and 6.14 ICU beds per 100,000 population, respectively.

As the pandemic evolved, the national government began to prioritize the expansion of ICU bed capacity, creating significant growth opportunities for a wide range of ICU medical devices. This growth has not abruptly ceased with the relaxation of pandemic control measures but continues to gain momentum. SWS MEDICAL, a manufacturer of CRRT (Continuous Renal Replacement Therapy) equipment commonly used in ICUs, has seen its stock price rise from RMB 25 at its IPO late last year to a high of nearly RMB 45, almost doubling in value. This demonstrates that the market remains optimistic about the substantial incremental potential driven by the ongoing expansion of ICU capacity.

The Three Years of the Pandemic: A Three-Year Catch-Up Period for ICU Development in China

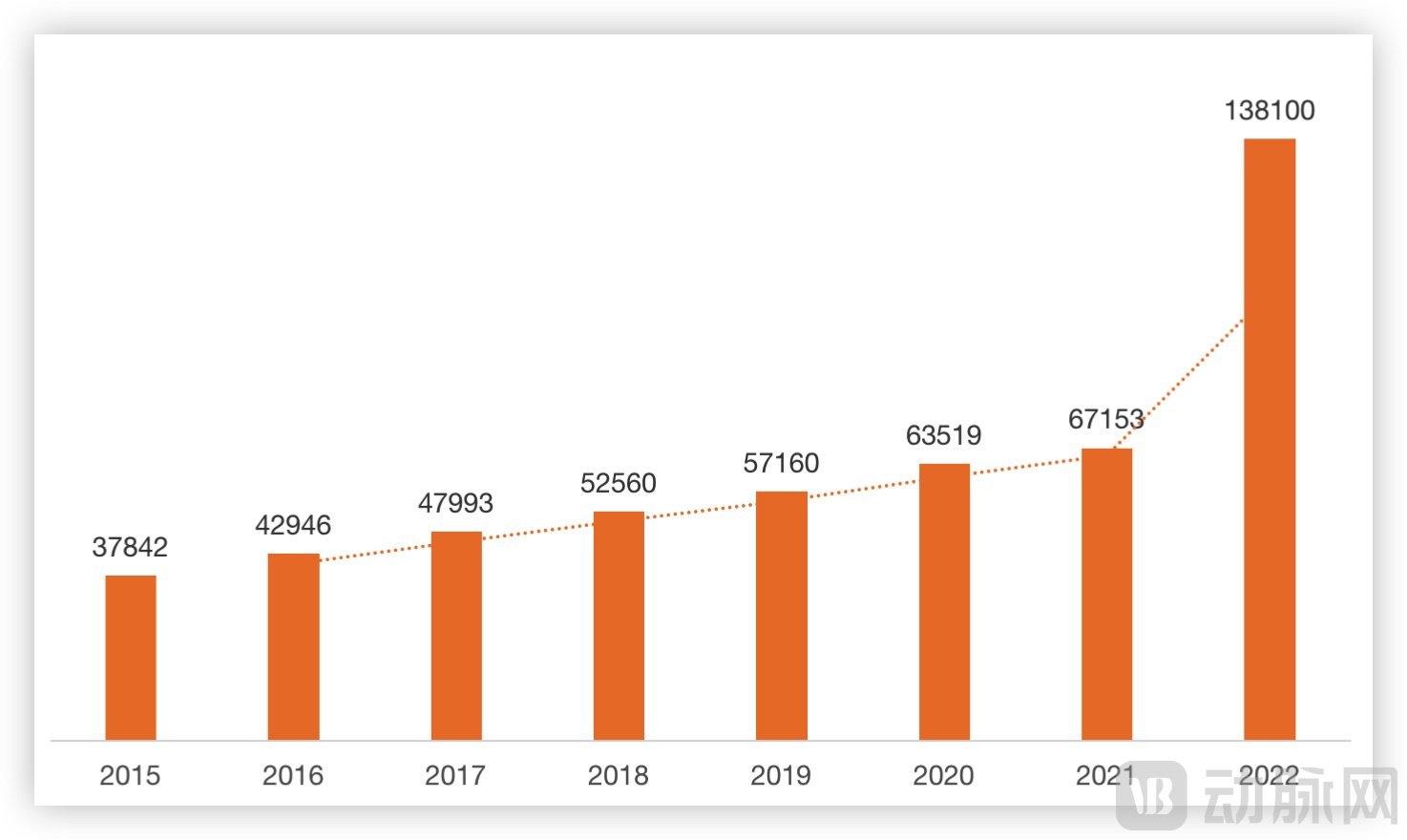

Since the outbreak of the pandemic, the shortage of ICU beds in China has been exposed, leading to a frantic effort to “catch up” over the past three years. According to data from the 2020 China Health and Health Statistical Yearbook, by the end of 2019, there were 57,160 beds in critical care medicine departments nationwide, while the total number of beds in medical and health institutions across the country was 8.807 million, meaning that ICU beds accounted for less than 1%.

By early December 2022, three years later, the National Health Commission revealed at a press conference that the total number of critical care beds nationwide was 138,100, with 106,500 ICU beds in tertiary medical institutions—an increase of over 80,000 beds in three years. Compared to the baseline three years prior, this figure was 2.4 times that of 2019, but this was only the beginning.

ICU Bed Count in China by Year; Data Source: "China Health Statistics Yearbook" and the National Health Commission

To cope with the relaxation of pandemic control measures, the National Health Commission stipulated that comprehensive intensive care unit (ICU) beds in tertiary hospitals should account for 4% of the total number of hospital beds. It further required an additional 4% of beds to be constructed as backup capacity, subject to equally stringent standards mandating their rapid conversion into critical care ICU resources within 24 hours. In other words, the combined capacity of comprehensive ICUs and convertible ICUs must meet the requirement of 8% of the total hospital beds, with completion mandated by the end of December 2022.

According to data from the "China Health and Health Statistical Yearbook," there were approximately 3.23 million hospital beds in tertiary hospitals in China in 2021. Based on a calculation of 4% for regular ICU beds plus 4% for reserve capacity, the number of regular ICU beds in tertiary hospitals should reach 129,000, with an additional 129,000 convertible ward beds.

According to the announcement by the National Health Commission, as of December 25, 2022, the number of critical care beds in tertiary medical institutions reached 133,400, with 104,800 standby ICU beds, totaling approximately 240,000 available beds, basically achieving the “4+4” construction target. Meanwhile,China’s combined total of conventional ICU beds in secondary and tertiary hospitals has reached 181,000, three times the 2019 figure.。

Compared with 2019, the number of ICU beds has increased by as many as 130,000. Moreover, this expansion is not limited to tertiary hospitals; as early as 2021, the National Health Commission formulated the “Work Plan for Enhancing the Comprehensive Capabilities of County Hospitals under the ‘Thousand Counties Project’ (2021–2025),” which specifically highlightedEnhancing the Comprehensive Capabilities of County-Level Hospitals, with a Particular Focus on Investment in Critical Care Medicine. We hope to seize the opportunity presented by the “Thousand County Project” to further strengthen critical care disciplines, elevate the level of critical care treatment capabilities in county-level regions to a new height, and truly achieve the goal of retaining critically ill patients within county-level hospitals.

The outbreak of the epidemic has exposed the shortcomings of insufficient medical resources, kicking off a new wave of infrastructure development in the healthcare sector, primarily focused on expanding public hospitals, and rolling it out across China.

Despite significant progress over the past three years, a substantial gap remains compared with developed countries. According to OECD data, Germany has 28.2 ICU beds per 100,000 population, and the United States has 21.6. In China, based on a population of 1.412 billion and 181,000 ICU beds,The number of ICU beds per 100,000 people is approximately 12.8, less than half that of developed countries., there is still significant room for catch-up.

From a long-term development perspective, the expansion of the overall number of ICUs in China will continue.

Data from the China Health and Health Statistical Yearbook shows that in 2021, tertiary and secondary hospitals in China had a total of approximately 5.97 million beds. Based on the Guidelines for the Construction and Management of Intensive Care Units (Trial), which stipulate that ICU beds should account for 2% to 8% of the total number of hospital beds, calculations can be made accordingly.China should be equipped with 119,400 to 477,600 ICU beds.. In February this year, the National Health Commission also stated at a press conference that the number of intensive care unit (ICU) beds would be expanded to 404,000. The market offers substantial room for growth.

Furthermore, according to data from the National Health Commission of China, as of December 25, 2022, in terms of critical care rescue equipment, intensive care unit (ICU) beds across the country were equipped with a total of 167,000 hemodialysis units, 24,000 continuous renal replacement therapy (CRRT) machines, over 2,600 extracorporeal membrane oxygenation (ECMO) systems, 131,000 invasive ventilators, 157,000 non-invasive ventilators, 1.09 million patient monitors, and 58,000 high-flow nasal cannula (HFNC) oxygen therapy devices.

The ongoing expansion of ICU infrastructure will further drive growth in the sales of related medical equipment.

The ICU is the final line of defense in hospitals for treating critically ill patients, a defense that relies on the support of various medical devices.

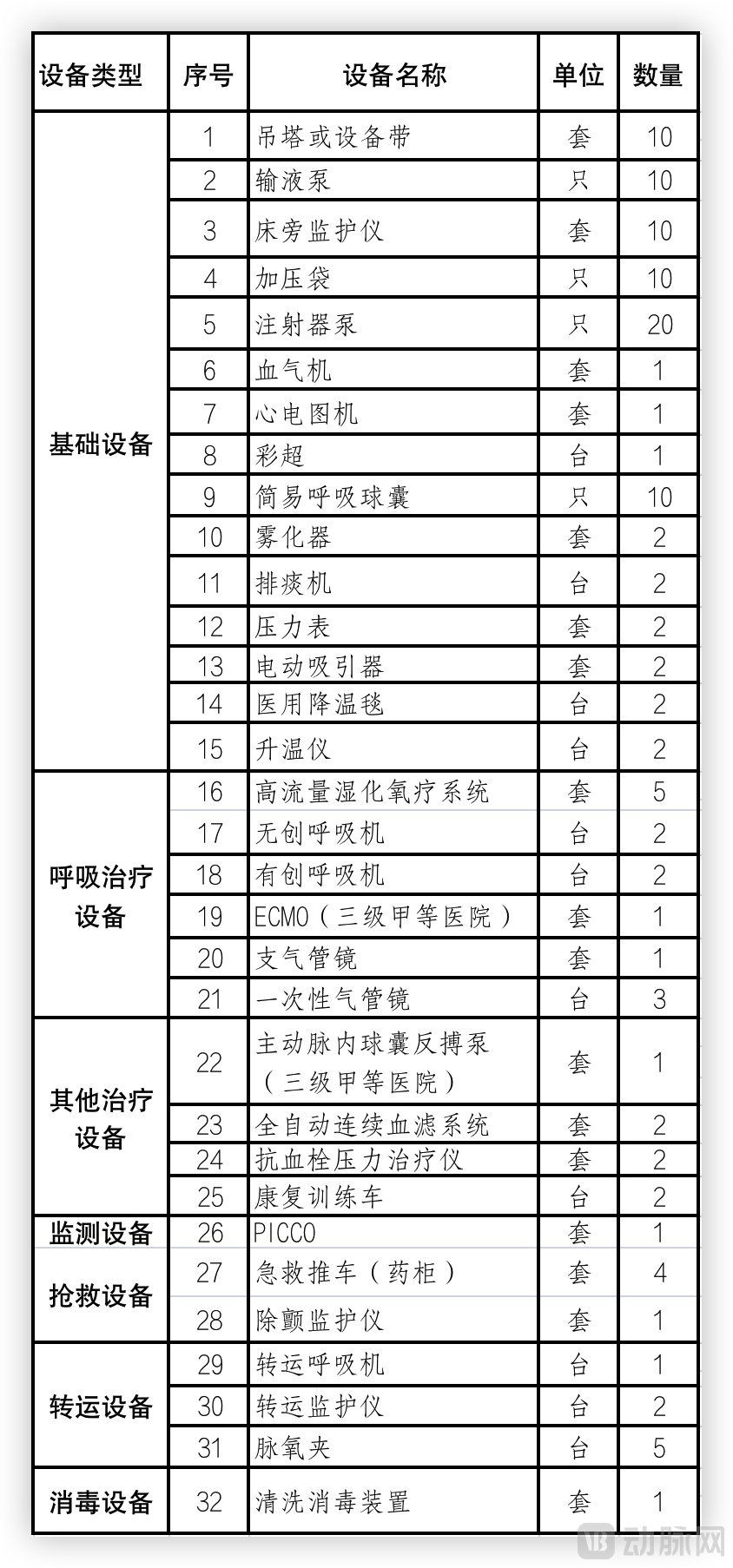

The National Health Commission explicitly stated in the "Operational Guidelines for the Expansion and Renovation of Critical Care Beds" that tertiary hospitals must strengthen their preparedness of critical care medical resources, ensuring that general intensive care unit (ICU) monitoring units are readily available at all times. Hospitals are required to accelerate the construction and upgrading of general ICU monitoring units in accordance with general ICU standards to ensure that all critical care units are immediately operational. The concurrently released "Reference Standards for Equipment Configuration in General ICUs" also stipulates the equipment configuration requirements for general ICU wards.

Equipment Configuration per 10 ICU Beds, Source: “Reference Standards for Comprehensive ICU Equipment Configuration”

According to public data, the construction cost of a single ICU bed ranges from approximately RMB 400,000 to RMB 1 million. Based on a median estimate of RMB 700,000, the construction expenses for the 130,000 new ICU beds added in China over the past three years amount to nearly RMB 100 billion.Based on a target of 400,000 ICU beds, nearly 200,000 additional ICU beds need to be constructed in the future., related medical devices have significant growth potential.

In late February, Chongqing Shanwaishan Science&Technology Co.,Ltd. (hereinafter referred to as “SWS MEDICAL”) released its 2022 annual performance flash report, showing a year-on-year increase of over 200% in net profit attributable to shareholders of the parent company. Since the beginning of this year, SWS MEDICAL’s stock price has surged by 80%, nearly doubling, with a peak gain of close to 20% in the first week of April alone. On April 17, the stock price hit a new high.

Behind the outstanding revenue lies the sustained growth in market demand for ICU equipment.

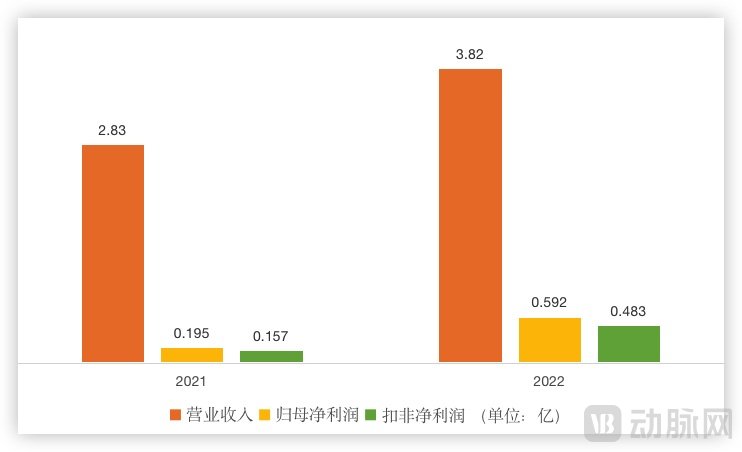

SWS MEDICAL released its 2022 annual report on the evening of April 2. The company achieved a revenue of RMB 382 million in 2022, a year-on-year increase of 34.85%; net profit attributable to shareholders of the parent company was RMB 59.237 million, up 204.2% year on year; and net profit after deducting non-recurring gains and losses was RMB 48.2595 million, up 207.37% year on year.

SWS MEDICAL’s revenue is primarily composed of three major segments: equipment, consumables, and medical services. Regarding the reasons for its performance growth, SWS MEDICAL stated in its annual report that this was mainly due to the year-on-year increase in recognition of its blood purification equipment by hospitals both domestically and internationally, the continuous expansion of its distribution coverage, and the rapid growth of its blood purification equipment business.

Key Financial Data of SWS MEDICAL in the Past Two Years, Sourced from Company Announcements

Revenue from blood purification equipment, the company’s core business, reached RMB 242 million in 2022, a year-on-year increase of 41.32%. According to SWS MEDICAL’s annual report, the company sold 3,071 units of blood purification equipment in 2022, representing a 60.2% year-on-year increase. As equipment coverage expanded, the company’s brand gained increasing market recognition, which in turn drove a consumption materials sales growth rate exceeding 100%, with dialysis powder sales surging by 330.36% year on year.

Notably, SWS MEDICAL’s continuous renal replacement therapy (CRRT) equipment, developed based on proprietary core technologies for original blood purification devices, has gained recognition from ICU professionals for its high stability and clinical adaptability in the treatment of critically ill COVID-19 patients. Furthermore, SWS MEDICAL’s CRRT systems integrate multiple therapeutic modes and offer a variety of functional configurations and models, allowing for customization to meet clients’ personalized needs.

Continuous Renal Replacement Therapy (CRRT) has a broad spectrum of clinical applications. It demonstrates promising utility in conditions ranging from severe acute renal failure to multiple organ dysfunction syndrome (MODS), systemic inflammatory response syndrome (SIRS), acute respiratory distress syndrome (ARDS), acute necrotizing pancreatitis, crush syndrome, drug and toxin poisoning, and severe heart failure. CRRT represents one of the most significant advancements in intensive care unit (ICU) treatment in recent years.

Although SWS MEDICAL did not disclose the specific sales volume of its Continuous Renal Replacement Therapy (CRRT) devices in its annual report, the company explicitly stated during investor meetings that CRRT device sales in 2022 saw a significant increase compared to 2020 and 2021, driven by increased procurement following the relaxation of pandemic control measures. A large number of Grade A tertiary hospitals in major cities across China have extensively purchased and deployed SWS MEDICAL’s CRRT devices.

Meanwhile, SWS MEDICAL stated that with increased support from national policies, the acceleration of critical care capacity building and the substitution of domestic products for imports, as well as the demand driven by new healthcare infrastructure development, CRRT will continue to maintain a high level of market demand for a considerable period in the future.

The outbreak of the epidemic has boosted the development of critical care medicine in China and indirectly driven the growth of equipment in related fields.

In the “14th Five-Year Plan” for the Development of the Medical Equipment Industry, released in 2021 by ten departments including the Ministry of Industry and Information Technology of China, various medical equipment types—including CRRT—were identified as “key areas for development.” Multiple provinces, such as Zhejiang, Guangdong, and Sichuan, have signaled support for the development of domestically produced medical equipment, thereby laying a solid foundation for the domestic substitution of imported products in the hemodialysis industry.

Certainly, it is not only CRRT that will benefit; related ICU equipment such as monitoring systems, ventilators, infusion pumps, X-ray machines, electrocardiographs, blood gas analyzers, and defibrillators will also see robust demand.

ICU treatment capabilities are closely tied to the configuration of medical equipment.

Incremental Medical Equipment Driven by ICU Construction; Data Sourced from "Reference Standards for Comprehensive ICU Equipment Configuration" and the China Government Procurement Network

Undoubtedly, the incremental demand for medical devices driven by ICU construction will be substantial. Using the equipment ratio requirements specified in the "Reference Standards for Equipment Configuration in Comprehensive ICUs" as a baseline, we selected certain essential medical devices and calculated the costs based on the addition of 100,000 new ICU beds. The prices were derived from recent bid award announcements published on the China Government Procurement Network.

As shown in the table above, every addition of 100,000 ICU beds creates an incremental market space of approximately RMB 43 billion for medical devices. Among these, respiratory therapy equipment, represented by ventilators and high-flow humidified oxygen therapy systems, accounts for nearly RMB 15 billion, excluding ECMO, which is only required to be equipped in Grade A tertiary hospitals. In addition, the incremental market space for patient monitors exceeds RMB 8 billion, while that for CRRT reaches RMB 7.7 billion. This may explain why SWS MEDICAL is viewed favorably in the secondary market.

Between the 181,000 beds already built in 2022 and the target of 400,000 beds under construction, there remains a gap of over 200,000 beds. This implies that nearly RMB 100 billion in incremental market space for medical devices will be created in the future. In particular, essential ICU equipment such as patient monitors and ventilators will see substantial growth potential.

Patient Monitor

As an essential vital signs monitor (hereinafter referred to as "monitor") in the ICU, it can continuously monitor patients' physiological parameters 24 hours a day, detect changing trends, predict changes in condition, and provide doctors with emergency handling. In the current domestic monitor market, Mindray is the industry leader. According to its annual report, its life information and support business, represented by monitors, covers nearly 110,000 medical institutions in China and more than 99% of tertiary hospitals.

Mindray also disclosed in its Q3 2022 report that revenue reached RMB 23.296 billion, representing a year-on-year increase of 20.13%. The Patient Monitoring & Life Support segment benefited from the continued advancement of new healthcare infrastructure projects in China, with its growth rate accelerating quarter over quarter during the reporting period. Additionally, at an investor meeting, Mindray revealed that in the first three quarters, the Patient Monitoring & Life Support product line secured 270 new high-end hospital clients previously not served by the company and expanded its reach to 350 existing clients through cross-selling.

Meanwhile, leveraging its comprehensive portfolio of patient monitors, ventilators, defibrillators, anesthesia machines, operating tables, surgical lights, ceiling pendants and bridges, infusion pumps, and ECG machines, as well as its holistic solutions for operating rooms (OR) and intensive care units (ICU), Mindray has launched the “M-Connect” ecosystem • Smart Monitoring+. This system seamlessly integrates data and waveforms from patient monitors, ventilators, and other devices into the ultrasound imaging interface, enabling synchronized, real-time visualization of dynamic changes on a single screen. This facilitates better integration, analysis, and utilization of clinical information, allowing healthcare professionals to clearly and comprehensively assess the trajectory of patients’ condition changes, thereby enhancing diagnostic and therapeutic efficiency and quality.

As of the first half of 2022, the “Rui Zhi Lian” IT solution had cumulatively secured contracts with nearly 300 hospitals, including over 80 new additions in the first half of 2022. The system has been installed at numerous top-tier hospitals in China, such as Peking Union Medical College Hospital, Beijing Tiantan Hospital, Beijing Jishuitan Hospital, China-Japan Friendship Hospital, Zhongshan Hospital Fudan University, Tongji Hospital in Wuhan, Xiangya Hospital of Central South University, and The First Affiliated Hospital of Sun Yat-sen University.

Edan Instruments and BaolaiTe, second-tier domestic manufacturers, have also reaped significant benefits from the expansion of ICU capacity.

According to Edan Instruments’ annual report, the company achieved revenue of RMB 1.74 billion in 2022, representing a year-on-year increase of 6.48%. The advanced parameter monitoring modules equipped in Edan’s self-developed plug-in patient monitors—including EtCO₂, anesthesia, neuromuscular blockade, and EEG modules—have all achieved import substitution for core technologies. Edan independently developed the CNBP (Continuous Non-Invasive Blood Pressure) measurement technology, an industry first for patient monitors, which provides comprehensive data monitoring and a more comfortable measurement experience. Meanwhile, at an investor conference, Edan stated that ICU critical care construction is a systematic and long-term process. To support this, the company has launched multiple new products aimed at enriching ICU application solutions.

As one of the earliest domestic enterprises to engage in the R&D and manufacturing of medical patient monitors, Baolait boasts a comprehensive product portfolio comprising three major series: all-in-one patient monitors, modular patient monitors, and handheld patient monitors. These products cover a wide range of clinical applications, including critical care, sub-intensive care, surgical and anesthesia monitoring, neonatal and obstetric monitoring, and routine departmental monitoring. In the first half of 2022, the company achieved revenue of RMB 558 million, representing a year-on-year increase of 10.16%. Furthermore, Baolait drives innovation by closely addressing key clinical needs. Its newly launched P-series information-enabled modular patient monitor is a high-end intelligent monitoring solution designed specifically for critical care departments. By integrating modern artificial intelligence, internet, and Internet of Things (IoT) technologies, this product has been widely adopted in hospital ICUs, operating rooms, and various special care wards.

Ventilator

The outbreak has provided domestic ventilator manufacturers with an opportunity to gain prominence and even achieve overtaking on a bend.

Ventilator manufacturing features high entry barriers, stringent technical requirements, significant complexity, and a highly concentrated market. In the ICU segment, three international brands—Getinge, Hamilton Medical, and Dräger—dominate the market with a combined share exceeding 50%, followed by companies such as GE HealthCare, Medtronic, Vyaire, and Mindray. Among them, Dräger has long held the leading market position in China due to its early entry into the country.

Prior to the pandemic, medical device giants such as Dräger, Philips, and Maquet led the domestic sales rankings for medical ventilators, while domestic brands included Mindray, Shenzhen Comen, and Beijing Aeonmed. The outbreak prompted European and American countries to relax access requirements; for instance, ventilators from Mindray and Yuwell obtained Emergency Use Authorization (EUA) certification from the U.S. Food and Drug Administration (FDA).

With the entry ticket to overseas markets, not only has there been a surge in sales, but technological breakthroughs have also followed. Hangzhou Beifeng Technology Co., Ltd. launched the turbine motor, a key hardware component for the localization of ventilators, enabling independent control over critical parts and making significant contributions to the stable production of domestically manufactured ventilators. Aerospace Changfeng has also introduced an adult ventilator equipped with the internationally mainstream “differential pressure” flow sensor.

With the rise of domestic ventilator manufacturers, China’s invasive ventilator industry is also experiencing rapid development.

Since launching its first ventilator in 2012, Mindray has undergone multiple iterations and upgrades, enabling its products to compete with international brands. For instance, the SV300 is China’s first electric turbine-driven ventilator, achieving precise and stable flow control while resolving the conflict between noise and heat dissipation. The SynoVent E series features a design with separate gas and electrical circuits to ensure operational safety; its expiratory valve is fully detachable and sterilizable, thereby preventing nosocomial cross-infections. The SV800/SV600 are critical care ventilators equipped with Adaptive Mechanical Ventilation (AMV) mode and Intelligent Cycle (Intellicycle) technology. These systems automatically adjust ventilator parameters by monitoring changes in patients’ respiratory physiology and waveforms, thereby implementing lung-protective strategies.

Aeonmed is a leading domestic R&D and manufacturing enterprise in anesthesia and respiratory medical equipment, with products covering six major business segments: Respiratory & ICU, Anesthesia & Operating Room, Emergency & Response, Laminar Flow & Hospital Engineering, Sleep & Respiratory Diseases, and IVD. Among them, the VG70, as its flagship product, is a turbine-based therapeutic ventilator integrating invasive and non-invasive ventilation functions. Its built-in turbine features oxidation resistance, low noise, and long service life, capable of high-speed operation in oxygen-enriched environments with a lifespan exceeding 30,000 hours, representing the latest generation of turbines internationally.

Amid a surge in bulk procurement orders from health commissions and key hospitals across multiple provinces and cities at the end of 2022, Aeonmed Medical rapidly coordinated resources across departments, delivering and putting into use over 3,000 units of equipment in the Beijing market within one week. Before the Spring Festival, the company successfully delivered more than 20,000 units of invasive ventilators, non-invasive ventilators, transport ventilators, and high-flow respiratory humidification therapy devices nationwide, with over 10,000 units of its flagship VG70 ventilator delivered.

Of course, there is the indispensable ECMO. As a life-saving device that can partially replace heart and lung functions, allowing them brief rest and adequate oxygenation, reducing ventilator-induced lung injury, promoting systemic blood circulation, maintaining basic physiological stability, and buying critical time for patient rescue, each ECMO unit costs between 1 million and 3 million RMB. Currently, only more than 200 hospitals in China are equipped with ECMO.

Although the domestic market for ECMO is still dominated by foreign brands, three domestically produced ECMO systems were launched in Q1 of this year.

On January 5, the National Medical Products Administration (NMPA) announced on its official website that Hannuo Lifemotion, China’s first ECMO product, had been approved for market launch. On January 17, HuiSheng-I, developed by Changzheng Medical, became the second ECMO device approved for marketing in China following review and approval by the NMPA. On February 23, the NMPA granted conditional emergency approval to an ECMO device developed by Jiangsu Suiteng Medical Technology Co., Ltd., marking it as the third domestically produced ECMO product to receive approval.

Although the three approved domestically produced ECMO devices were granted emergency approval, this also indirectly reflects the substantial market demand.

Medical devices, represented by patient monitors, ventilators, and ECMO systems, serve as a critical foundation for ICU development and constitute a key target of public health infrastructure within China’s new wave of healthcare infrastructure initiatives.

The nearly RMB 100 billion incremental market space for medical devices has instilled greater confidence in related companies.

Since the end of last year, the pace of ICU equipment procurement across China has significantly accelerated.

Guangzhou will invest 895 million yuan to procure 22,000 units of 23 types of medical equipment, including infusion pumps, ventilators, and high-flow nasal cannula therapy devices. Hefei had previously announced that it had prepared 1,000 ICU beds and would urgently purchase medical supplies worth over 100 million yuan.

A search for “ventilators” on the Chinese Government Procurement Network by VCBeat revealed 514 related entries in December 2022, with over 600 entries in Q1 of this year, compared to only slightly more than 300 in Q1 2019, before the pandemic. A similar trend was observed for “patient monitors,” with 376 related entries in December last year, 460 in Q1 of this year, and merely 200 in Q1 2019. This indicates that procurement of ICU-related equipment did not come to an abrupt halt after December but has continued to gain momentum.

Since the outbreak of the pandemic, the Chinese government has implemented a series of measures to address weaknesses in the healthcare system. These initiatives range from the “Thousand-County Plan” for new healthcare infrastructure, to over RMB 300 billion in special-purpose healthcare bonds, and subsidized loan policies. They cover the upgrading, supplementation, and expansion of existing hospital equipment, with a particular emphasis on strengthening critical care departments. The expansion of ICU beds in hospitals will drive increased demand for equipment related to intensive care units. As certainty on the demand side grows, it will provide greater momentum for the development of relevant enterprises.