Plummeting Dental Implant Prices Spark 'Revenge Implantation' Trend?

MEI WEI DENTAL GROUP

Oral Health Service Provider

On April 20, Beijing, Guangdong, Shandong, and other regions officially began implementing the results of the centralized procurement of dental implant systems, while simultaneously enforcing price controls on dental crowns through competitive bidding and online listing, as well as regulating medical service fees.

Over the past two months, the outcomes of the centralized procurement for dental implants have been intensively implemented, signifying that the “most challenging centralized procurement in history” has achieved the entire process—from top-level design to procurement execution and finally to service delivery—within just six months.

As key players in the dental implant service sector, private dental institutions have long leveraged the volume-based procurement (VBP) initiative to launch sustained marketing campaigns. They promote low-priced packages using keywords such as “VBP price,” “additional discounts on top of VBP prices,” and “below VBP price,” or directly contact patients who had previously declined treatment due to high costs to inform them of the price reductions.

In the short term, the “price war” for dental implants among private dental clinics has already begun; in the long run, healthcare institutions should leverage both internal and external resources to build momentum.

Dental implants are hailed as the “most difficult centralized procurement in history” because the overall price structure of a single dental implant is complex, comprising the cost of the implant system (including the implant fixture, abutment, and other accessories), the cost of the crown, and medical service fees.

Reviewing the entire process of centralized procurement for dental implants, it was also divided into three parts: implant systems, crowns, and medical services, each advancing overall according to the characteristics of their respective fields.

Key Milestones in the Centralized Procurement of Dental Implants; Data Sources: National Healthcare Security Administration and Official Websites of Provincial Healthcare Security Administrations; Graphic by VCBeat

Regarding implant systems, 39 companies were selected in the centralized procurement, with an average price reduction of 55%.

In September 2022, the Sichuan Provincial Healthcare Security Administration established the Inter-Provincial Alliance Centralized Volume-Based Procurement Office and issued Procurement Announcement No. 1, officially launching the centralized procurement process.

In January 2023, the results of the centralized procurement for dental implant systems were announced: out of 55 participating companies, 39 were selected. The average winning bid price dropped to over RMB 900, representing a 55% decrease compared to the median procurement price prior to the centralized procurement.

According to data released by the Sichuan Provincial Healthcare Security Administration, this centralized procurement aggregated demand from nearly 18,000 medical institutions nationwide, totaling 2.87 million implant systems, which accounts for approximately 72% of the annual number of dental implants placed in China (4 million). It is expected to save patients around RMB 4 billion annually.

Regarding dental crowns, the healthcare security authorities have reduced overall prices through competitive bidding and online listing, taking into account factors such as product manufacturing and market demand.

Dental crowns account for approximately 10%–15% of the cost of dental implants. Previously, the mainstream market price ranged from RMB 300 to RMB 1,200, with the highest prices exceeding RMB 2,400.

Dental crowns are predominantly customized, non-standard consumables that must be manufactured according to the specific oral conditions of each patient. Therefore, after comprehensively considering factors such as the customized processing characteristics of dental crown products, the regionalized market landscape, and the differentiated usage requirements of medical institutions, the healthcare security authorities have opted for a more suitable approach of competitive bidding and online listing.

In March 2023, the Sichuan Provincial Healthcare Security Administration organized a competitive bidding and online listing process for dental crowns, specifically all-ceramic crowns for single-tooth implantation. Among the 110 companies that submitted bids, 107 were shortlisted. The shortlisted prices for single crowns ranged from RMB 100 to RMB 656, with an average shortlisted price of RMB 327. Notably, the shortlisted price for the most in-demand crown product dropped to RMB 150.

Following the announcement of the shortlisted results in Sichuan, provinces such as Shandong, Guangdong, Jiangsu, and Fujian organized local online bidding or linked listing processes for dental crowns in April 2023. Using Sichuan’s dental crown bidding as a reference, the overarching principle was to ensure that prices did not exceed the shortlisted prices in Sichuan.

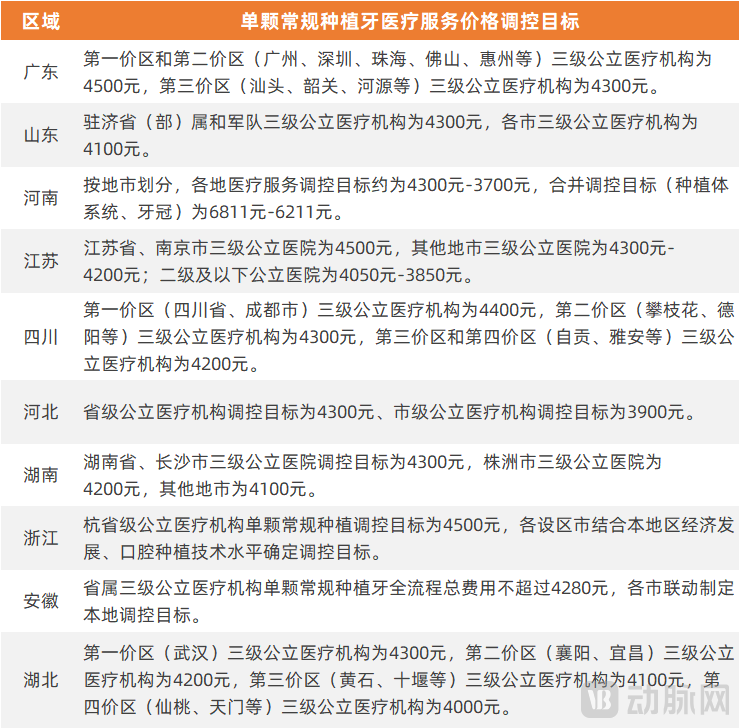

In terms of medical services, provinces and cities across China have successively formulated and implemented regulated prices for dental implant services.

Price regulation is primarily divided into two aspects: first, establishing price control targets for medical services related to single conventional dental implants, which include consultation fees, biochemical tests, imaging examination fees, implant placement fees, crown insertion fees, scanning, design and modeling fees, anesthesia fees, and medication costs throughout the entire implantation process; second, adjusting the current pricing items for oral implant medical services.

Among these, the medical service price for a single standard dental implant intuitively reflects the changes.

Previously, the average cost of the medical service component for a single conventional dental implant at tertiary public medical institutions exceeded 6,000 yuan. In accordance with the requirements of the National Healthcare Security Administration, the price control target for tertiary public medical institutions is set at 4,500 yuan.

On this basis, provinces and prefecture-level cities have established corresponding regulatory targets based on local economic conditions, labor costs, dental implant technology, and other factors.

Regulatory Measures for Medical Services in Selected Regions (Excluding Policy Relaxations); Source: Official Websites of Local Healthcare Security Administrations

Overall, the regulatory targets for tertiary public medical institutions in provincial capital cities range from approximately RMB 4,100 to RMB 4,500, while those for tertiary public medical institutions in prefecture-level cities are around RMB 3,700 to RMB 4,300. The regulated prices for secondary and lower-tier public medical institutions are correspondingly reduced, reflecting a predominant tone of “reduction” in the regulation of medical service prices.

The combined price governance measures for implant systems, crowns, and medical services have resulted in an overall reduction of approximately 50% in the cost of dental implants.

The implementation progress of the above-mentioned governance measures varies across provinces. Some regions adopt a step-by-step approach, implementing each measure as it is finalized, while others implement the “trinity” package simultaneously. On April 20, Beijing, Guangdong, Shandong, and other regions began the simultaneous rollout of the results from the centralized procurement of dental implants, the competitive bidding outcomes for dental crowns, and the regulated prices for dental medical services. According to publicly available information, the “trinity” price governance framework will be fully implemented nationwide before May.

Although the various measures of the centralized procurement program for dental implants are primarily targeted at public medical institutions, a large number of private dental clinics have participated in the program due to the significant market share held by private medical institutions.

It is reported that among the 18,000 medical institutions participating in the centralized procurement of implant systems, 14,000 are private; these private medical institutions have also simultaneously committed to responding to the regulation of medical service prices.

In terms of promotion and marketing, private medical institutions have been particularly proactive. Although the outcomes of volume-based procurement (VBP) are still being implemented gradually, private dental clinics have already seized the opportunity presented by VBP to launch high-profile marketing campaigns.

Currently, multiple enterprises, including Topchoice Medical, ByBo Oral Medical Group, and MEI WEI DENTAL GROUP, have announced that their affiliated medical institutions will implement local centralized procurement policies.

Offline, some medical institutions have announced in their lobbies through banners and display stands that they have begun implementing centralized procurement prices, emphasizing “lower prices without compromising quality.” Advertisements for “centrally procured dental implants” frequently appear in building advertisements.

On internet platforms, private medical institutions still offer dental implants priced at over RMB 10,000, while simultaneously launching bundled packages based on centralized procurement prices. Taking Beijing as an example, discounted Swiss-made dental implants are generally priced above RMB 6,500, with some institutions offering them for as low as RMB 5,980; the first Korean-made dental implant is priced at only RMB 2,080. Some packages are even labeled “below centralized procurement price” or “additional discounts on top of centralized procurement prices.” A dental chain in Beijing clearly lists its prices on an online platform, offering Nobel Biocare implants for RMB 1,800, whereas the centralized procurement price for the company’s products is RMB 1,855.

Direct price cuts, introductory low-price offers, and limited-quantity discounts are among the myriad marketing tactics being deployed. This wave of marketing extends beyond pricing to encompass services, with “complimentary pick-up and drop-off” becoming a value-added service offered by some medical institutions to attract patients. Other institutions are proactively reaching out to patients who previously hesitated due to high costs, informing them of the price reductions and gauging their interest.

In the past, dental implants were a high-margin service for private dental practices. Looking at the overall dental market, it is evident that a price war has been triggered, with volume-based procurement serving as the turning point.

“A short-term price war is inevitable,” said Chen Xizhu, founder of Hengmei Dental. Centralized procurement has indeed compressed the profit margins of private medical institutions to some extent; to survive, these institutions must increase their patient volume and service delivery. Even general clinics that previously stayed out of price wars may now be drawn into them.

Tian Li (pseudonym), a senior executive at a dental chain in Guangdong, told VCBeat that before the implementation of centralized procurement, prices at many private medical institutions were already relatively low. Consequently, there was limited room for further price reductions after centralized procurement, certainly not as significant as those seen in public medical institutions, with some having only a few hundred yuan of downward flexibility. “However, patients observe widespread publicity about reduced dental implant prices across society, with substantial discount margins, and thus naturally assume that private providers should also lower their prices. Therefore, these price cuts and promotions are largely marketing tactics.”

Regardless, centralized marketing has given patients a more intuitive perception of the implementation of volume-based procurement results.

In fact, since the National Healthcare Security Administration issued its directive in September 2022, healthcare security authorities at all levels, medical institutions, and media outlets have launched extensive publicity campaigns covering the centralized procurement of dental implants. Phrases such as “The era when a full set of dental implants cost as much as a BMW is now history,” “The end of the ten-thousand-yuan implant era; the arrival of the thousand-yuan era,” and “Dental implant prices halved” have frequently appeared online.

“For private medical institutions, the greatest benefit of centralized procurement lies in conducting a wave of extensive and sustained market education, enabling patients who previously had little or no understanding of dental implants to recognize that their own or their family members’ dental issues can be resolved through implant treatment,” said Xia Bin, CFO and COO of Youmu Dental. He believes that, in terms of overall trends, the number of patients opting for dental implants will continue to grow, with centralized procurement serving as an accelerator in this process.

Theoretically, price reductions can stimulate consumer demand. Under the influence of high-frequency policy promotion and marketing efforts, have medical institutions already seen a significant surge in patient numbers?

Chen Honghua, a member of the Management Committee of Taikang Insurance Group and CEO of Taikang ByBo Dental, stated that there has been a significant increase in outpatient consultations for dental implants recently, with the growth rate meeting expectations.

Multiple institutions also noted that although the number of dental implant patients in the past two months has exceeded the overall level from November 2022 to January 2023, it has not yet returned to the level seen in the same period of 2021. “On the patient side, the explosive growth many anticipated has not materialized.”

In some regions, the number of patients has decreased rather than increased.

According to media reports, a public dental hospital in Zhoushan, Zhejiang Province, has recently seen only follow-up patients, with just one new patient recorded during the first week of April; some private dental institutions have had no new patients seeking dental implants for several months.

Chen Xizhu believes that one of the reasons for these phenomena is that many patients remain in a wait-and-see stance. “Frequent policy publicity and marketing campaigns have indeed raised patient awareness of dental implants; however, the implementation progress of centralized procurement varies across institutions, and marketing packages are highly diverse. For the same brand of dental implant, significant price discrepancies exist among different providers, which instead causes patients to hesitate, unsure of how to choose, leading them to think it is better to wait.”

In fact, patients’ wait-and-see attitude of “dental implant prices will drop under centralized procurement, so I’ll wait before getting implants” began as soon as the National Healthcare Security Administration released its centralized procurement policy.

According to the annual reports released by multinational corporations such as Straumann and Dentsply Sirona, their business performance in China in 2022 was less than optimistic. This was due partly to the impact of the pandemic and partly to patients postponing treatment plans following the implementation of centralized volume-based procurement policies.

Currently, the phased suppression of patient demand has persisted for over half a year since September 2022 and has yet to recover.

According to Chen Xizhu’s forecast, with the full implementation of volume-based procurement from late April to May, once prices have stabilized and patients have more definitive information to guide their decision-making, the first peak may arrive in mid-May.

Xia Bin also stated that the underperformance in growth since 2023 may not be entirely attributable to centralized procurement. “It is also related to the overall economic environment; therefore, patient growth is likely to gradually materialize as the economy recovers.”

“Volume-based procurement for dental implants has had a certain impact on private dental practices, but it is not significant enough to alter the market landscape,” believes Tian Li.

Therefore, as comprehensive implementation takes effect, private dental practices need to attract patients through intensive marketing in the short term while patiently awaiting the arrival of the first growth peak. In the long run, how can they identify new profit margins and build new core competencies?

First, private dental practices need to optimize their customer acquisition methods and departmental structure.

Driven by market pressures, private dental practices are likely to shift their customer acquisition strategies in the future, moving from reliance on price differentials to building customer relationships and leveraging word-of-mouth referrals. Institutions will pivot from prioritizing major procedures such as dental implants to placing greater emphasis on preventive care departments, potentially developing new preventive service offerings that become key profit centers.

Secondly, to meet the diverse needs of patients, medical institutions can achieve tiered package offerings and differentiate themselves from public healthcare providers by offering premium implant brands and high-end services, in addition to those included in the centralized procurement program. Xia Bin introduced that the 14 clinics under Youmu Dental are generally positioned in the high-end market, with two of them participating in the centralized procurement.

Furthermore, volume-based procurement (VBP) has imposed stricter requirements on the cost control of management and operations in medical institutions. Following the implementation of VBP, there is limited room for further reduction in consumable costs, while labor costs associated with physicians cannot be significantly curtailed without risking talent attrition. Consequently, cost control in management and operational processes becomes particularly critical.

“Centralized volume-based procurement of dental implants helps promote a more open and transparent pricing system for implant procedures, and also facilitates the upgrading of operational management and customer service by dental institutions, thereby fostering a new development pattern in the oral healthcare industry characterized by fair competition, quality assurance, and innovation-driven growth,” said Chen Honghua.

In addition to out-of-pocket payments, leveraging commercial insurance to improve the accessibility of dental implants is another area where medical institutions can focus. For instance, ByBo Oral Medical Group has launched “Taikang Worry-Free Dental Implant Insurance” and “Good Teeth for Life,” a long-term dental insurance plan, which provides customers who receive implants from designated brands with coverage for free re-implantation.

It is worth noting that there is a fundamental logical difference between the centralized procurement of dental implants and that of pharmaceuticals and other medical consumables. The logic behind the latter is to squeeze out inefficiencies in the distribution chain, thereby benefiting patients on one hand, and raising medical service prices on the other to better reflect the value of physicians’ labor; alternatively, the savings generated from price reductions may be distributed to physicians as part of their insurance fund surplus, making their income more transparent and compliant. In contrast, the centralized procurement of dental implants is implemented alongside controls on medical service prices, which implies a decline in physicians’ income. To maintain or even increase their income levels, physicians must provide more labor and serve a larger number of patients.

Whether public or private, healthcare institutions need to leverage digital technologies to help physicians improve efficiency, optimize the allocation of medical resources for complex cases and routine dental implant procedures, and enable physicians to achieve more ideal income levels.

The centralized procurement of dental implants began with upstream consumables, and the transformation in the consumables sector also presents opportunities for downstream service providers.

In this centralized procurement of implant systems, the winning bidders include internationally renowned companies such as Straumann and Dentsply Sirona, high-demand South Korean brands like Osstem and Dentium, as well as domestic enterprises such as Weihai Weigao and Changzhou Baicaotec.

For companies that have already secured a certain market share and whose products have undergone long-term clinical validation, winning bids in centralized procurement can further expand the scope of product usage. These enterprises are also capable of adapting to the market environment under centralized procurement by adjusting their product portfolios and pricing structures. For companies that have yet to establish a significant market presence, centralized procurement offers a channel to rapidly enter hospitals with lower sales costs, facilitating faster growth, particularly for domestic brands.

Gao Jun, General Manager of Gaofeng Medical, believes that companies that were not selected or did not participate in the centralized procurement will establish clearer market positioning, such as focusing on high-end products and complex or difficult cases.

“Based on the market collaboration information we have gathered, once centralized procurement reaches a certain stage, it is not inconceivable that imported products with significant market share may be manufactured domestically through local production facilities, joint ventures, or contract manufacturing.” In Gao Jun’s view, if multinational corporations engage in deep cooperation with domestic enterprises, the former can reduce product costs, while the latter can enhance their capabilities in R&D, design, and manufacturing processes, thereby achieving mutual benefit and win-win outcomes.

Overall, upstream consumables represented by dental implants are expected to achieve clearer product and corporate positioning, thereby fostering a richer and more multi-tiered product ecosystem.

Amidst the transformation of the upstream market, healthcare institutions can select products that better align with their strategic objectives and local patients’ preferences and purchasing power, thereby establishing a differentiated service system—a key approach to seizing external opportunities.

The original intention of the centralized procurement of dental implants was to benefit the general public, and their feedback will quickly reflect this after full implementation; furthermore, public response will provide clearer guidance on the next steps for the industry.