Global Biopharma Investment and Financing Report Q1 2023: Spring Has Yet to Arrive in the Capital Markets

I. In Q1 2023, both the number of global financing deals and the total amount raised declined significantly year-on-year, with a sharper drop in the Chinese market as capital markets cooled. The global capital market remained dominated by early- to mid-stage investments, while the IPO market chilled, leading to a precipitous decline in financing activity.

II. Small molecules, large molecules, and CXO lead the global popularity rankings, while capital investment in the CGT sector remains robust. In the domestic market, the CDMO sector serves as the primary driver, with synthetic biology drawing significant attention.

3. Nationwide biopharmaceutical investment and financing are primarily concentrated in the Jiangsu-Zhejiang-Shanghai region, with Guangzhou, Shenzhen, and Chengdu emerging as hotspots following the Yangtze River Delta. Government-funded capital has played a significant role in driving industry recovery, while market-oriented funds have remained cautious in their investments.

IV. Two Chinese enterprises made a strong showing in the top 10 global biopharmaceutical financing deals of Q1 2023; CXO emerged as a hot sector domestically, with early-stage companies rising to prominence and securing six of the top 10 spots in China.

01Trends in Global Biopharmaceutical Investment and Financing: Q1 2022–Q1 2023

1.1 The number of global financing events and total financing amount in Q1 2023 both decreased year-on-year, with a more pronounced cooling in the Chinese market

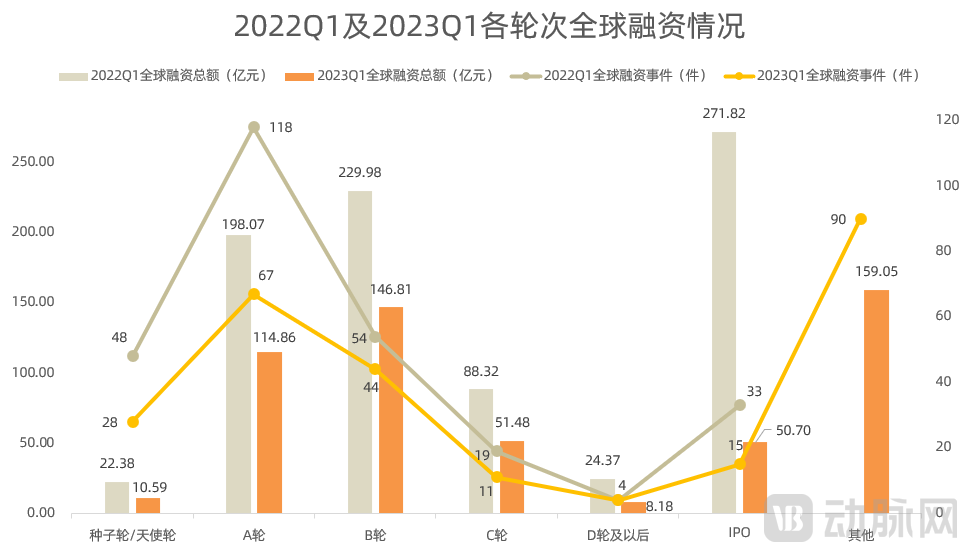

Comparison of the Number of Financing Events in Q1 2022 and Q1 2023, Data Source: Arterial Orange

Comparison of Total Financing Amounts in Q1 2022 and Q1 2023, Data Source: Artery Orange

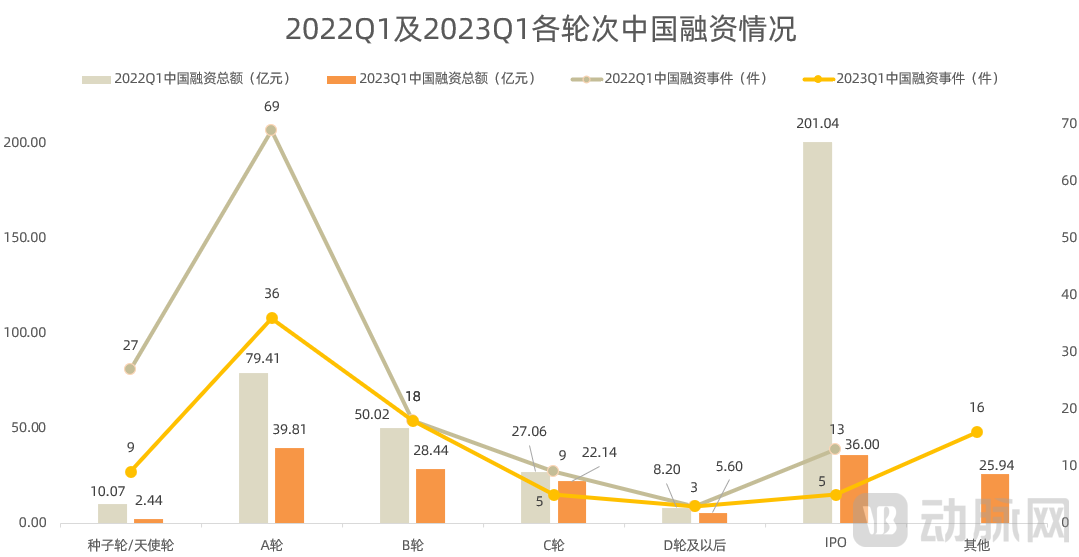

In Q1 2023, there were 259 financing events globally, averaging nearly three per day, a decrease of 17 from the same period last year, remaining largely flat. In China, there were 92 financing events in Q1 2023, averaging one per day, a decrease of 47 from the same period, representing a 30% decline, with a clear trend of contraction.

In terms of financing volume, the global total reached RMB 54.168 billion, a decrease of nearly RMB 30 billion year-on-year, representing a year-on-year decline of approximately 34%. The total domestic financing amounted to RMB 16.037 billion, down by about 57% year-on-year, indicating that the situation in China remains more severe than the global average.

Capital has become more restrained compared to the same period last year, with an overall decline in market sentiment and a significant drop in domestic activity. Biopharmaceutical companies are facing the challenge of “difficult financing.” Judging by the frequency and scale of investments, it is fair to say that the capital market remains in winter, with this chill being more pronounced domestically than overseas. This may reflect a lag in the Chinese market relative to the global trend.

1.2 Capital Markets Remain Dominated by Early-Stage Investment, While IPO Fundraising Experiences a Precipitous Decline

Data Source: VCBeat Orange

Examining the market by financing rounds, the cooling of the global funding landscape in Q1 2023 was primarily evident in the IPO stage. The number of financing deals was halved, while the total amount raised fell to less than 20% of the same period last year, with a significant decline in average deal size. With the secondary market failing to recover and the primary market unable to gain momentum, the linkage between the primary and secondary markets became stalled.

Investment and financing activities were primarily concentrated in Series A and Series B rounds. Although these figures declined compared to the same period last year, they still accounted for the majority of the investment market. Other financing types—including undisclosed rounds, strategic financing, equity financing, debt financing, and donations/crowdfunding—also secured a significant market share, driven by a high number of transactions and substantial total amounts. This indicates that during downturns in the conventional financing market, companies have adopted more diverse financing strategies to address capital constraints.

Data Source: VCBeat Orange

The broader trend in the Chinese market is aligned with the global market, with institutional investments primarily concentrated in early-to-mid-stage deals, and Series A financing accounting for the largest share. In contrast to the dismal performance of the global IPO market, although the average deal size in China’s IPO market has declined significantly year-over-year, its share of total domestic market financing remains second only to Series A and Series B rounds, indicating that the door to the IPO market remains relatively open.

02Hot Investment and Financing Sectors in the Global Biopharmaceutical Industry, Q1 2023

2.1 Small Molecules, Large Molecules, and CXO Lead the Global Popularity Rankings, with Gene Therapy Close Behind

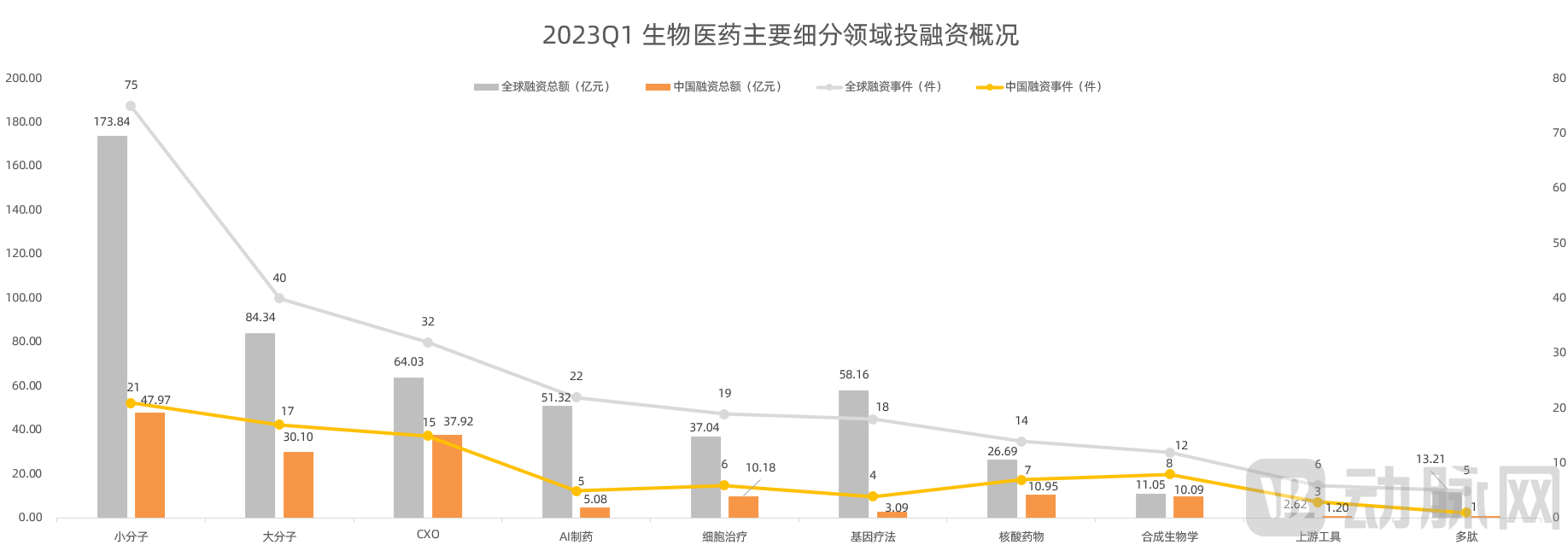

Data Source: VCBeat Orange

From a global perspective, small molecules, large molecules, and CXO were the three sectors most favored by capital in Q1 2023. Within the small molecule segment, oncology drugs remained the hottest area, recording the highest number of financing deals and the largest total funding amount. In addition, gene therapy stood out with high average deal sizes, following closely behind. This indicates that although cell and gene therapy (CGT) is often generalized in public discourse, investor activity has not cooled down, and the market remains optimistic about frontier innovations.

Compared with global trends, the domestic market shows a significantly higher preference for the CXO and nucleic acid sectors. The CXO sector remains hot, with the CDMO market contributing the majority of growth. In addition, companies such as Bluepha, Microfactory, Guangyue Biotechnology, and Enojikoco have achieved breakthroughs in synthetic biology, successfully attracting capital attention.

2.2 Focusing on Hot Sectors: A New Wave of “Low-Hanging Fruit” Harvesting

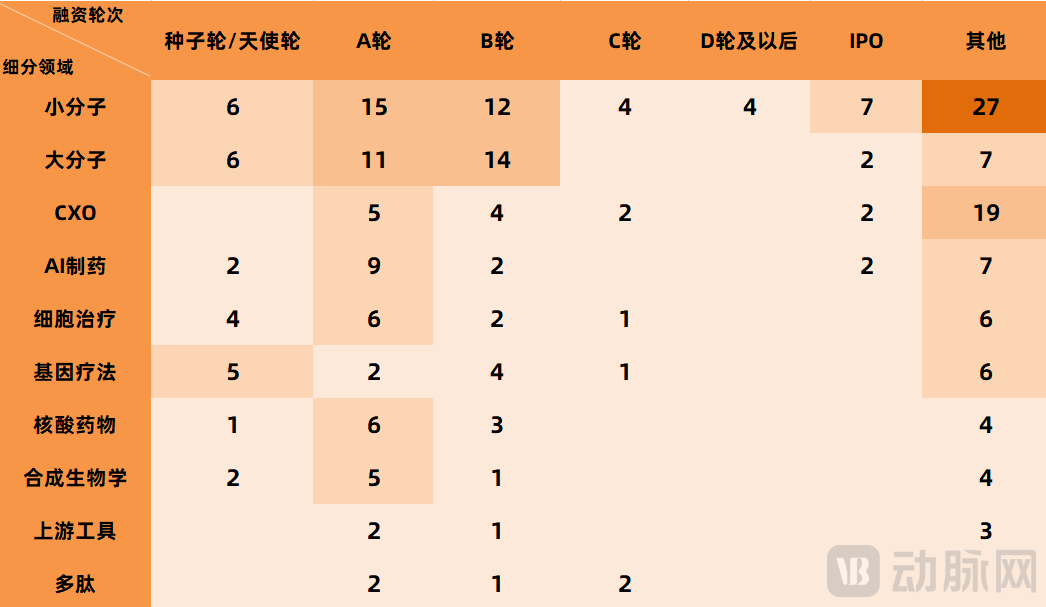

Distribution of Global Major Subsector Financing Rounds in Q1 2023, Data Source: Arterial Orange

Early-stage projects in frontier innovation sectors such as nucleic acid therapeutics, cell therapy, and gene therapy continue to attract strong interest, with sustained capital attention. In the more mature downstream processing sectors for small molecules and large molecules, financing rounds are widely distributed across all stages, with capital participation at each level, and a significant number of companies have successfully progressed to late-stage maturity. Furthermore, AI-driven drug discovery, as a prominent sector within the ITBT (Information Technology, Biotechnology) landscape, has garnered considerable attention; beyond the concentration of Series A companies, other financing stages have also attracted substantial capital interest.

03Top Cities for Biopharma Investment and Financing in China, Q1 2023

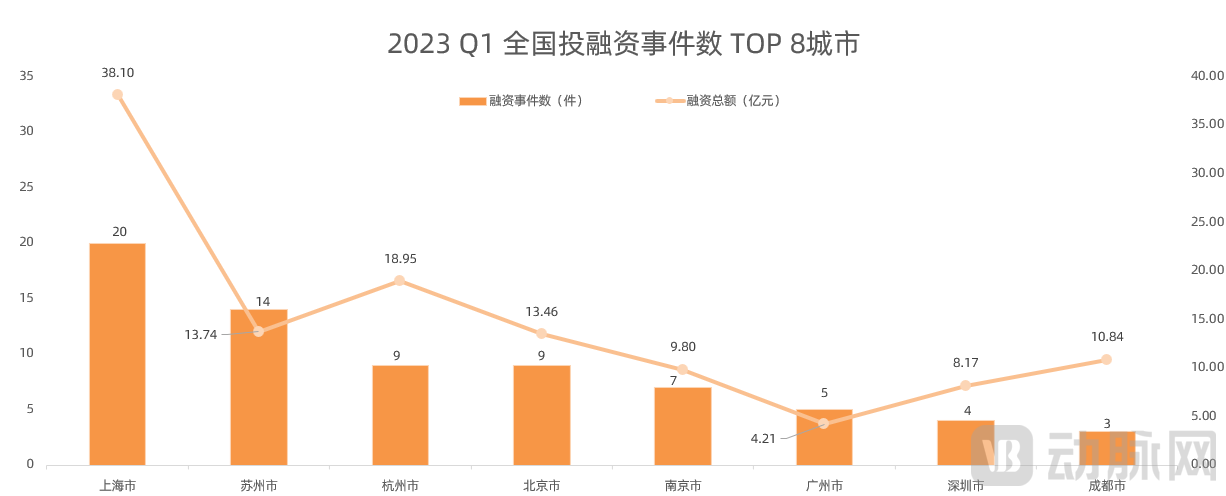

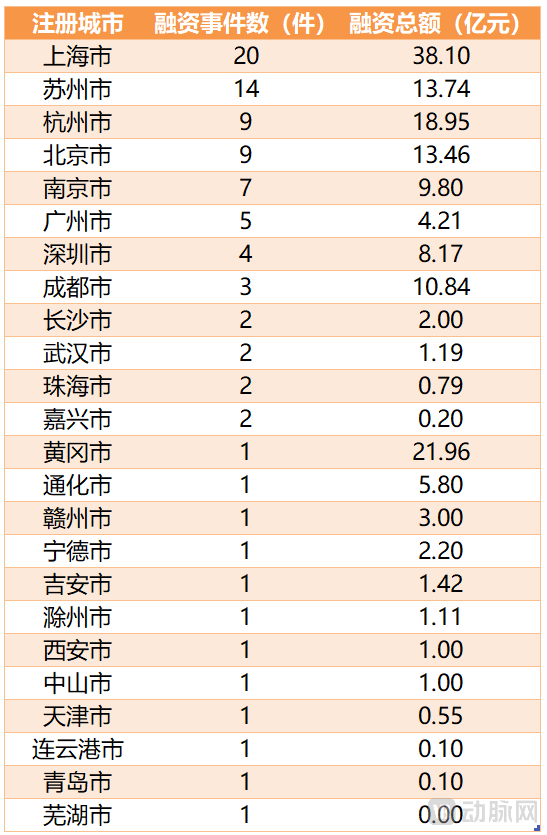

Distribution of Financing Across Chinese Cities in Q1 2023, Data Source: VBInsight

In Q1 2023, national biomedical financing and investment in China were primarily concentrated in the Jiangsu-Zhejiang-Shanghai region. Shanghai ranked first with 20 financing deals totaling RMB 3.81 billion, leading in both deal count and total amount, followed closely by Suzhou and Hangzhou. Notably, the average deal size in Hangzhou and Beijing exceeded that of Suzhou, suggesting that projects in these cities were at a more mature stage compared to those in Suzhou. Guangzhou, Shenzhen, and Chengdu emerged as hotspots after the Yangtze River Delta region. In particular, Chengdu surpassed Nanjing in total financing volume, driven by its high average deal size.

From the perspective of investment activities by institutions behind the top six cities, Sequoia Capital China Fund made four investments in Q1 2023, three of which were based in Beijing. These investments spanned four fields: small molecules, AI-driven drug discovery, synthetic biology, and nucleic acid therapeutics. Hillhouse also made four investments, primarily focusing on the CXO sector, with three out of its four deals being CXO projects; the portfolio companies were located in Shanghai and Hangzhou. Matrix Partners China has also been closely monitoring the CXO sector. Qiming Venture Partners invested in three projects across three distinct areas: small molecules, AI-driven drug discovery, and cell therapy.

Furthermore, it is worth noting that in addition to professional investment institutions continuously injecting vitality into the biopharmaceutical sector, government-backed capital has also stepped in to help revive the industry. For instance, Nanjing Jiangbei State-owned Assets and Nanjing Innovation Investment have participated in investing in cell therapy and small-molecule projects based in Nanjing, while the Guodiao Innovation Fund and Zheshang Venture Capital have jointly focused on nucleic acid drug R&D projects in Hangzhou.

04Top 10 Global Biopharma Companies by Q1 2023 Funding Amount (Excluding IPOs)

4.1 AI Drug Discovery Companies Top the List, with Two Chinese Firms Making a Strong Showing

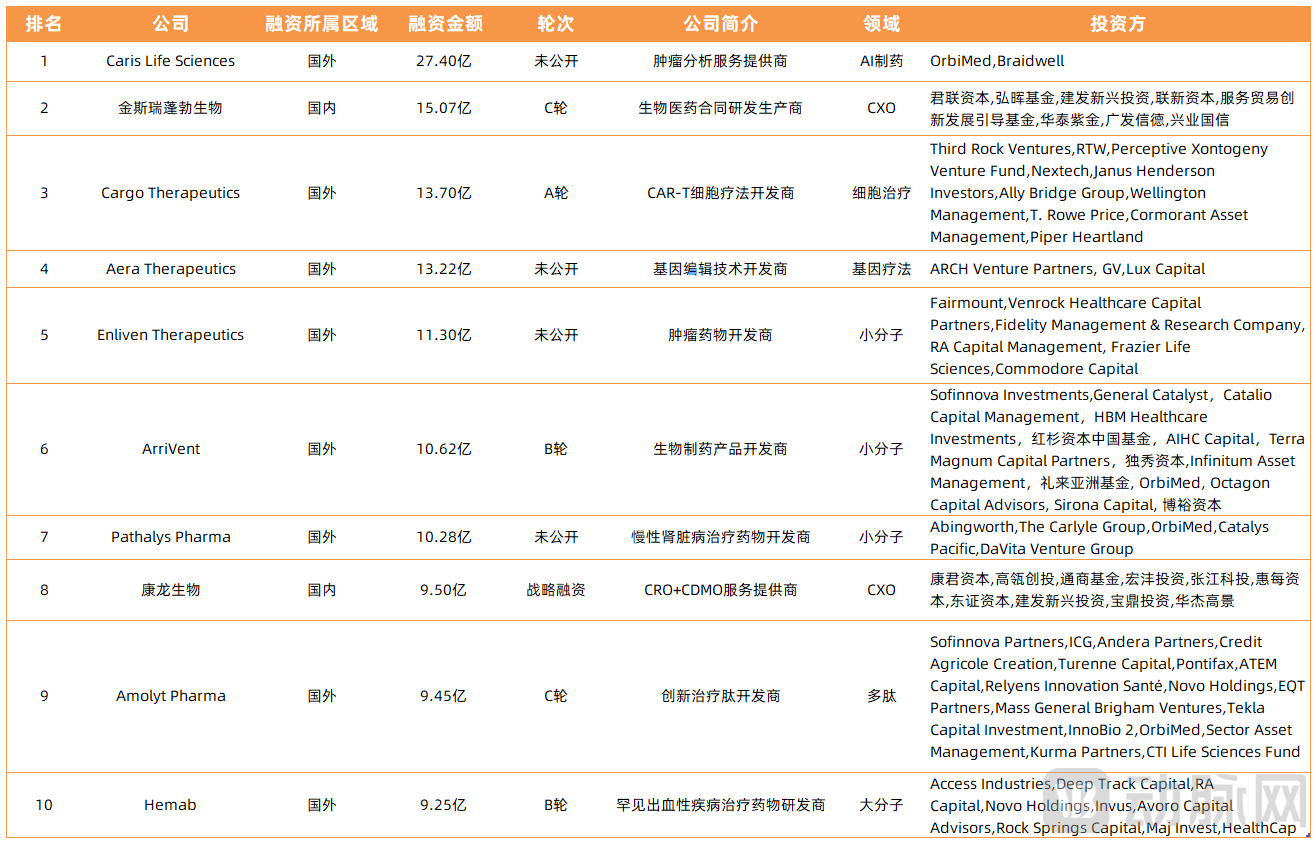

Overview of the Top 10 Companies by Global Biopharmaceutical Financing Amount in Q1 2023; Data Source: VCBeat Orange

In terms of drug modalities, small-molecule drugs still dominate among the global top 10 companies, accounting for three spots. Two CXO companies made the list, both Chinese firms: GenScript ProBio and Pharmaron ranked 2nd and 8th, respectively. Furthermore, we observe that substantial financing is increasingly directed toward AI-related enterprises, gene editing, cell therapy, and peptide-based therapeutics. Both drug modalities and disease areas have opportunities to secure significant funding, indicating that the market is not overwhelmingly concentrated on any single focus.

4.2 CXO Becomes a Hot Topic in China, with Early-Stage Companies Catching Up

Overview of the Top 10 Chinese Biopharmaceutical Companies by Financing Amount in Q1 2023; Data Source: VCBeat Orange

As expected, domestic companies with “stable assets” are more likely to secure larger financing rounds. This includes engineering-oriented sectors with positive cash flow, such as “CXO” (contract research, development, and manufacturing organizations) and “synthetic biology,” as well as enterprises backed by central state-owned brands like China Resources. The CXO sector in China remains hot, with the top three companies all belonging to this track: GenScript ProBio, Pharmaron, and ATLATL. Series A and B companies occupy six of the ten spots on the list. Notably, Jiachen Xihai, an mRNA vaccine and therapeutic drug developer at the Series A+ stage, tied for third place with ATLATL, each raising RMB 685 million.

Data Definition Rules

To facilitate statistical analysis, we adhere to the following principles when processing investment and financing data:

1. The financing events covered in this report include those from the angel round to IPO, excluding private placements and mergers and acquisitions;

2. In this report, angel rounds, seed rounds, and seed-stage VC investments are consolidated into the "Seed/Angel Round" category; all Series A rounds are consolidated into "Series A"; all Series B rounds into "Series B"; all Series C rounds into "Series C"; and all Series D rounds together with Pre-IPO rounds are consolidated into "Series D and Beyond." Other financing types include undisclosed rounds, strategic financing, equity financing, debt financing, and donations/crowdfunding.

2. All financing amounts are converted into RMB, using the following unified exchange rates: 1 USD = 6.85 RMB, 1 HKD = 0.87 RMB, 1 EUR = 7.40 RMB, 1 CHF = 7.45 RMB, 1 GBP = 8.4 RMB, and 1 SEK = 0.66 RMB;

3. Standardize financing amounts in the millions, tens of millions, or hundreds of millions to 1 million, 10 million, or 100 million, respectively;

4. The data in this report is current as of March 31, 2023; any data released after March 31, 2023, is not included in the statistical analysis of this report.The scope will be dynamically updated on the VCBeat Investment and Financing Channel.