Organoids and Organ-on-a-Chip Industry White Paper: 49 Global Companies, CRO or Biotech?

Amid several major moves by the FDA, organoids and organ-on-a-chip technologies have attracted significant industry attention over the past two years. Given their strong relevance to traditional biological models, these technologies have sparked intense debate and discussion.

In the early stages of industry development, as most outsiders had limited understanding of the sector, a fervent aspiration had already taken root in their minds: “This new technology is poised to reshape the current industry landscape and will soon reveal a more humane vision of the world—‘enabling all necessary preclinical trials to assess the safety and efficacy of various substances without relying on animals.’”

Broad application prospects and immense development potential have suddenly made this sector red-hot. Behind the boundless imagination lies a surge of adrenaline. The rapid flow of capital reflects the market’s eagerness and expectations, even at a time when most people have yet to clearly distinguish between the concepts of organoids and organ-on-a-chip.

However, the realm of the ideal has never been easy to reach; the path forward is often spiral, accompanied by numerous difficulties and challenges.

To present the most authentic current state of development in the organoid and organ-on-a-chip industries, and to uncover the truth behind many conflicting narratives, we haveNearly 50 Leading Companies in the Global Organoid and Organ-on-a-Chip IndustryConducted in-depth research, meticulously outlining the background, origins, and developmental trajectory of the global organoid and organ-on-a-chip industry, andCore executives from nearly 30 domestic enterprises and multiple industry investorsWe engaged in in-depth dialogues and also handed the microphone to experts with relevant industry backgrounds but no current conflicts of interest, striving to present an objective and neutral overview of the industry’s current development landscape.

The following are the core insights of the report:

1. Organoids and organ-on-a-chip belong to different subfields, but their application scenarios and purposes are similar; therefore, they are often mentioned in parallel or even conflated. Organ-on-a-chip refers to the use of organoids as the cell source for organ chips to combine the advantages of both technologies.

2. China has a large and growing cancer patient population. Due to low awareness of early screening among Chinese patients, diagnoses are often made at intermediate or advanced stages. Tumor organoids hold significant promise for applications in drug sensitivity testing. The increasing complexity of requirements for new drug development models and treatment regimens is driving the rapid growth of the organoid and organ-on-a-chip industries, a trend further accelerated by the global movement toward replacing animal testing.

3. The organoid and organ-on-a-chip industry is still in its early stages of development, with demand in the mid- and downstream segments yet to scale up significantly. As the industry continues to advance and relevant policies and standards are implemented, upstream demand is expected to surge. Companies that have proactively established deep footholds in the upstream sector will enjoy a first-mover advantage.

4. More robust policy and funding support abroad, along with earlier initiation of research, has accelerated the overall development of the organoid and organ-on-a-chip industries compared to China. Specifically, some overseas organoid companies have already addressed compliance and ethical issues related to organoid culture and use. While China’s organoid industry is growing rapidly, its capabilities in quality control for organoid culture and sample compliance require further improvement. Overseas organ-on-a-chip companies hold a dominant position and capture the majority of the market share. Although research on organ-on-a-chip technology in China began around the same time as in the United States, technological accumulation has been slower, and industrialization lags behind.

5. In China, the organoid sector is gaining greater prominence, whereas abroad, a larger proportion of companies are focused on organ-on-a-chip technology. This disparity primarily stems from differences in foundational technological expertise and varying market demands driven by distinct national contexts.

6. Two primary business models in the global organoid and organ-on-a-chip industry: direct product sales and service provision. Three future development pathways for the industry: precision instrument and equipment manufacturers, CROs, and biotech companies.

7. The market for using organoids in drug sensitivity testing is booming, but certain developmental limitations must be viewed objectively. For instance, the high heterogeneity of tumors hinders the large-scale application of related products, and the proportion of cancer patients who truly need and can benefit from organoid-based precision medicine remains relatively limited among both existing and newly diagnosed patient populations.

8. Automation, high-throughput capabilities, real-time in vitro detection, precision, systematic approaches, and integration with technologies such as AI and gene editing are inevitable trends in industry development.

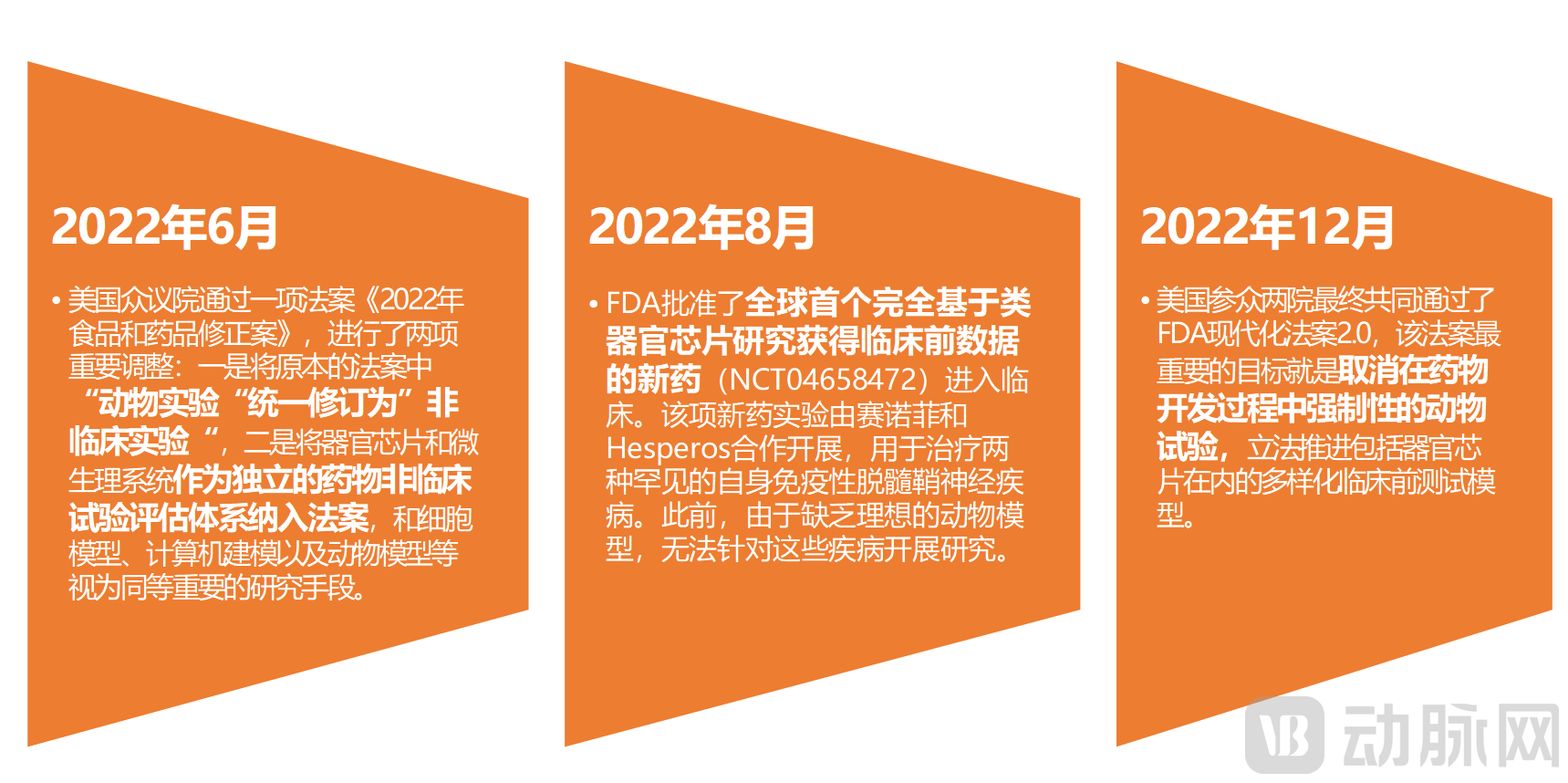

Driven by several major initiatives from the FDA, industry enthusiasm for organoids and organ-on-a-chip technologies has reached an all-time high in the past two years.

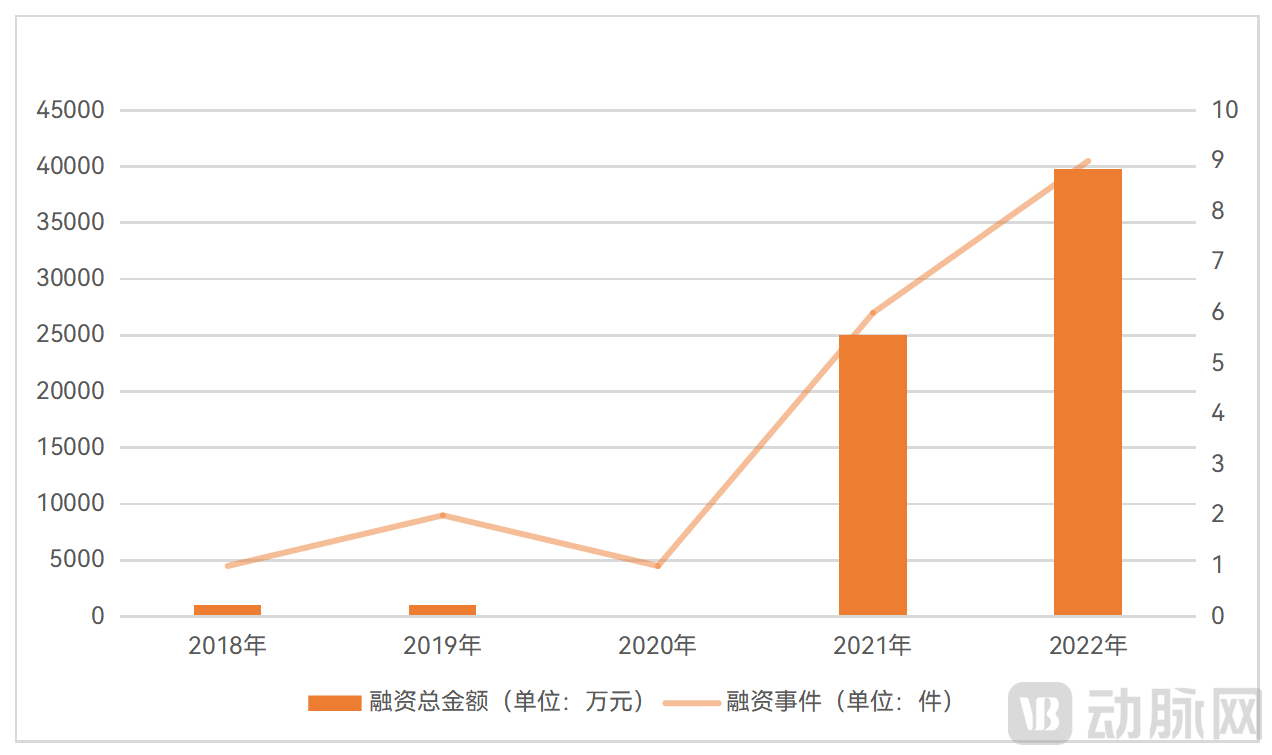

In 2021 and 2022, the organoid and organ-on-a-chip industry witnessed a surge in investment and financing growth, with both the number of funding rounds and the total amount raised hitting successive record highs.——In 2021, there were a total of six financing events in China’s organoid and organ-on-a-chip industry, with a total financing amount of RMB 250 million; in 2022, there were nine financing events, with a total financing amount of nearly RMB 400 million.

Over an extended timeframe, the financing and investment in China’s organoid and organ-on-a-chip industry have been steadily heating up over the past five years.

Financing Trends in China’s Organoid and Organ-on-a-Chip Sector Over the Past Five Years

Data source: Artery Orange Database; chart by VCBeat Research Institute

To help readers understand the current status of companies that are relatively active in the market, VCBeat has compiled the latest financing information for companies in China’s organoid and organ-on-a-chip industry as follows.

Latest Financing Landscape in China’s Organoid and Organ-on-a-Chip Sector

Data source: Artery Orange Database; chart by VCBeat.

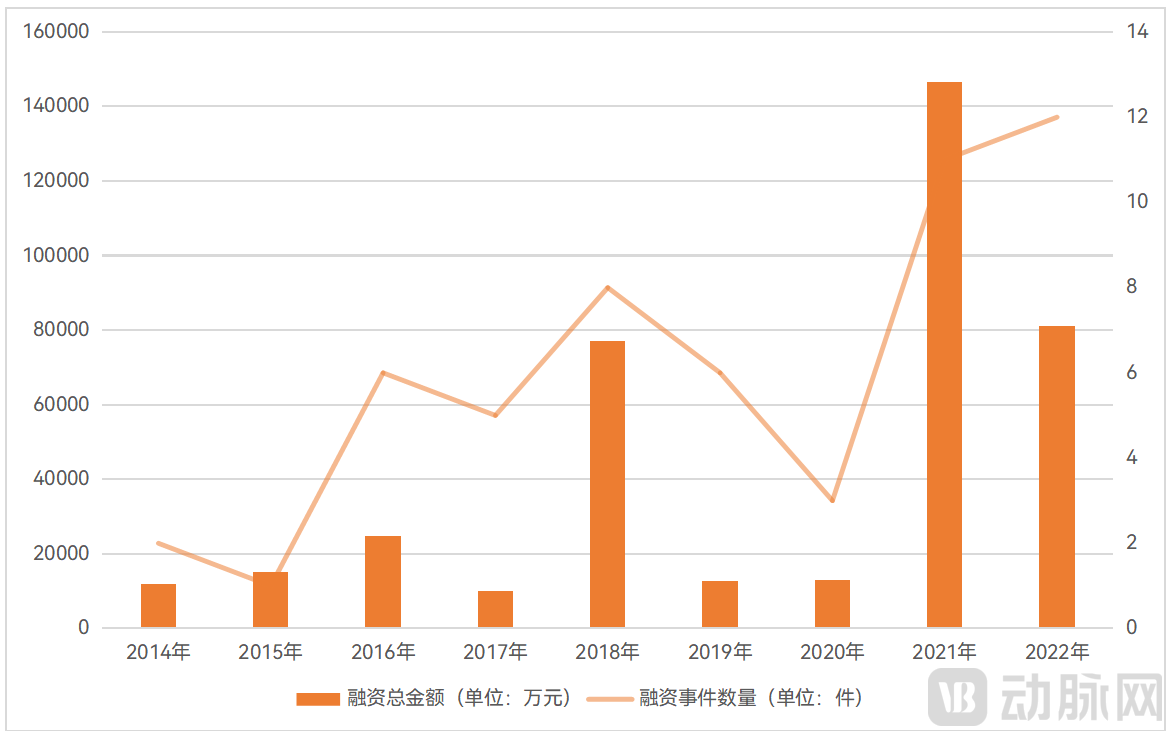

Widen the perspective, and then fromGlobal OverviewLet's take a look,Financing in the organoid and organ-on-a-chip sectors has experienced relatively significant fluctuations, yet it continues to demonstrate an upward trend.

Notably, the global organoid and organ-on-a-chip sector reached record highs in both the number of financing events and total funding amount in 2018 and 2021. In 2018, there were 8 financing events, with total funding reaching RMB 770 million; in 2021, there were 11 financing events, with total funding reaching RMB 1.46 billion.

Overview of Global Financing in the Organoid and Organ-on-a-Chip Industry, 2014–2022

Data source: Arterial Orange Database; Chart by VCBeat.

As the industry is in its early stages of development, global market financing performance is heavily influenced by the fundraising activities of individual star enterprises.

For example, the global field of organoids and organs-on-chipsTo date, the emergence of each new peak in investment and financing has been largely driven by the strong support of Emulate.—In 2016, Emulate completed a $28 million Series B financing round; in 2018, it completed a $36 million Series C financing round; and in 2021, it completed an $82 million Series E financing round.

Another star startup, founded in 2019,Xilis, has also become an important "combined force" driving the formation of new peaks in the investment and financing market. For instance, nearly half of the record-high global investment and financing in the organoid and organ-on-a-chip industry in 2021 was attributed to Xilis.

In terms of the frequency and amount of financing, both the organoid and organ-on-a-chip industries are still in their early stages of development, with competition just beginning to emerge.Enterprises that possess core technological advantages and a complete production chain, and have entered the industry early, undoubtedly enjoy first-mover advantage.

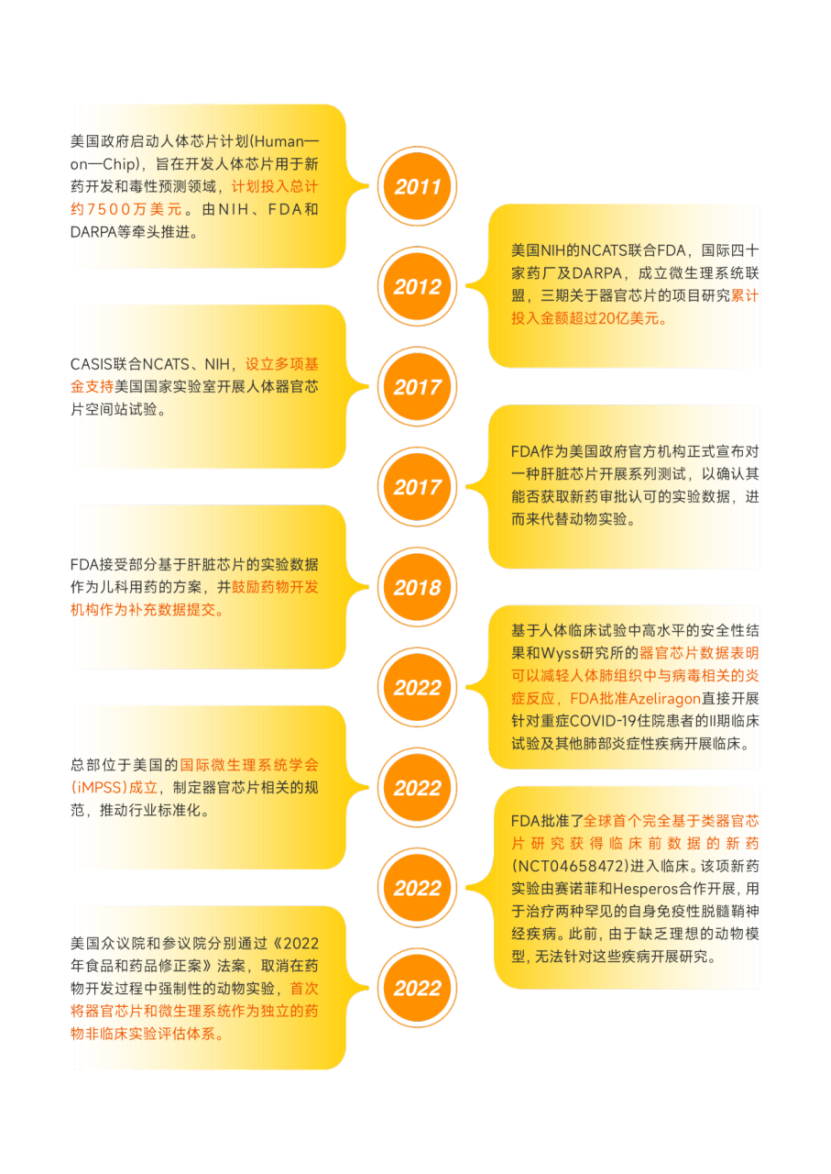

Given the broad application prospects and development potential of organoids and organ-on-a-chip technologies, governments worldwide are vigorously supporting and promoting industry growth. The U.S. government, in particular, places significant emphasis on the development of organ-on-a-chip technology, providing substantial research funding and practical support.

Significant U.S. Support for the Organ-on-a-Chip Industry

Data source: Artery Orange Database, Organ-on-a-Chip Network; graphic by VCBeat Institute

Since the announcement of the Human-on-Chip initiative in 2011, relevant U.S. government agencies have not only invested substantial research funding into the field of organ-on-a-chip technology but also encouraged and supported the establishment of industry consortia such as the International Microphysiological Systems Society (iMPSS) and the Innovation and Quality (IQ) Consortium. Furthermore, by setting up multiple organ-on-a-chip testing centers to advance the development of industry standards, and actively convening conferences and forums to strengthen cross-sector communication, these agencies have been promoting the industrialization of the organ-on-a-chip sector.

Introduction to the IQ Alliance and Its Key Members

As an affiliate of the IQ Consortium, IQ MPS is dedicated to advancing the development and standardized application of microphysiological systems in scientific research and pharmaceuticals, while providing a platform for cross-pharmaceutical collaboration and data sharing within the consortium.

Data source: Official websites of respective companies and the IQ Alliance; chart by VCBeat.

In recent years, the European Union has continuously increased its support for research on human organ-on-a-chip technologies, both in terms of concrete policy implementation and financial funding.For instance, the introduction of policies such as Europe’s ban on animal testing for cosmetics has significantly heightened industry attention to potential animal alternative technologies, including organoids and organ-on-a-chip systems.

In terms of financial support, the European Union’s most heavily funded global technological development initiative—the 7th Framework Programme (FP7), which was launched on January 1, 2007, with a total budget of €50.521 billion—included organ-on-a-chip projects. Additionally, initiatives such as the EU-ToxRisk project, which commenced in 2016, also provided funding for organ-on-a-chip research.

The Chinese government is currently placing greater emphasis on the development of the organoid field.In the past two years, with increasing government emphasis and intensified capital attention, a series of team standards and national standard drafts have been successively introduced, including “Human Colorectal Cancer Organoids,” “Human Intestinal Organoids,” “Technical Specifications for Culture of Human-Derived Lung Cancer Organoids,” “General Technical Requirements for Skin-on-a-Chip,” and “Operational Guidelines for Preparation, Cryopreservation, Thawing, and Identification of Human Normal Breast and Breast Cancer Organoids,” significantly accelerating the development of the industry.

Policies, Special Support Initiatives, and Standards Development for the Organoid and Organ-on-a-Chip Industry in China

Source: Artery Orange Database; Chart by VCBeat.

In addition, the active support in China in recent years for pilot programs of Laboratory Developed Tests (LDTs) has alsoIt has greatly stimulated the enthusiasm of organoid and organ-on-a-chip companies to apply their products in clinical development, enabling these enterprises to generate some cash flow during the early stages of product registration and approval, thereby supporting their survival and growth.Currently, some public medical institutions in cities such as Shanghai and Guangzhou have been designated as pilot comprehensive entities.

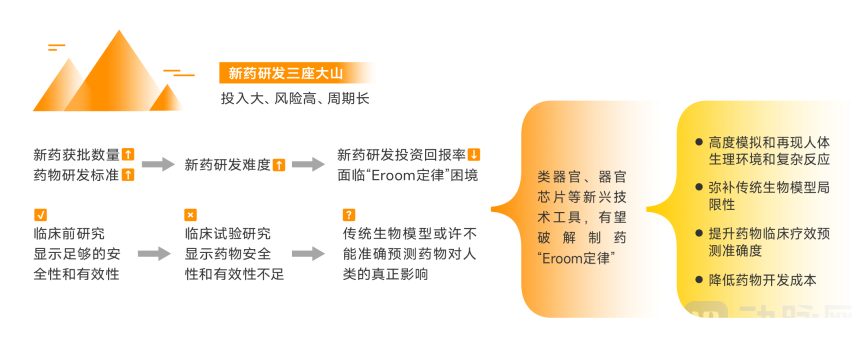

Every commercialized technology emerges in response to demand, and this holds true for organoids and organ-on-a-chip systems as well.Overcoming the current challenges in new drug development is a key driver promoting the growth of the organoid and organ-on-a-chip industries.

The Dilemma in New Drug Development Drives the Growth of the Organoid and Organ-on-a-Chip Industries

Source: Survey interviews; Chart by VCBeat

As more new drugs gain regulatory approval and enter the market, drug development standards are continuously being raised, leading to increasing complexity and costs in new drug R&D, diminishing returns on investment, and exacerbating the challenges faced by the industry. The pharmaceutical sector is urgently seeking new methods, paradigms, and tools to improve the success rate of new drug development.

In vitro biomimetic models, such as organoids and organ-on-a-chip systems, which can highly simulate and recapitulate human physiological environments and complex responses, have emerged as a promising new hope for breaking the impasse in the pharmaceutical industry.

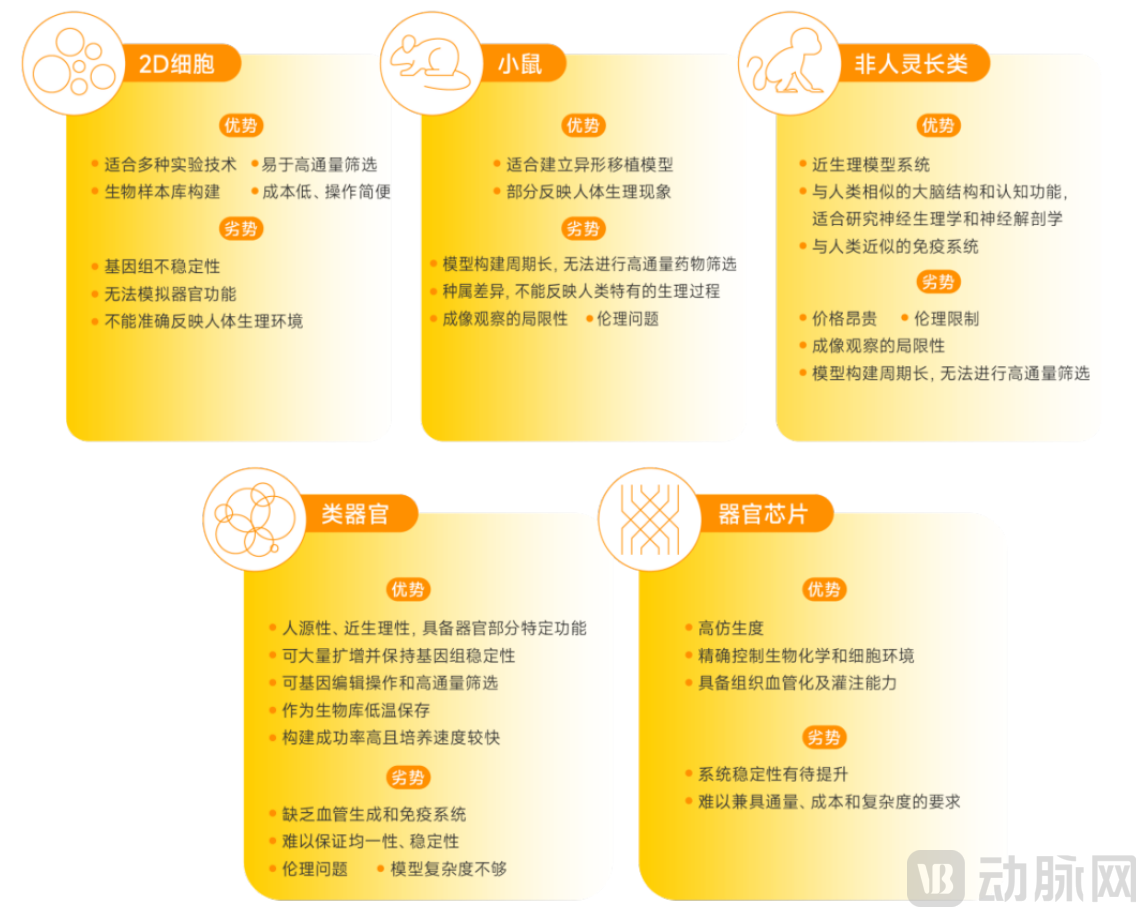

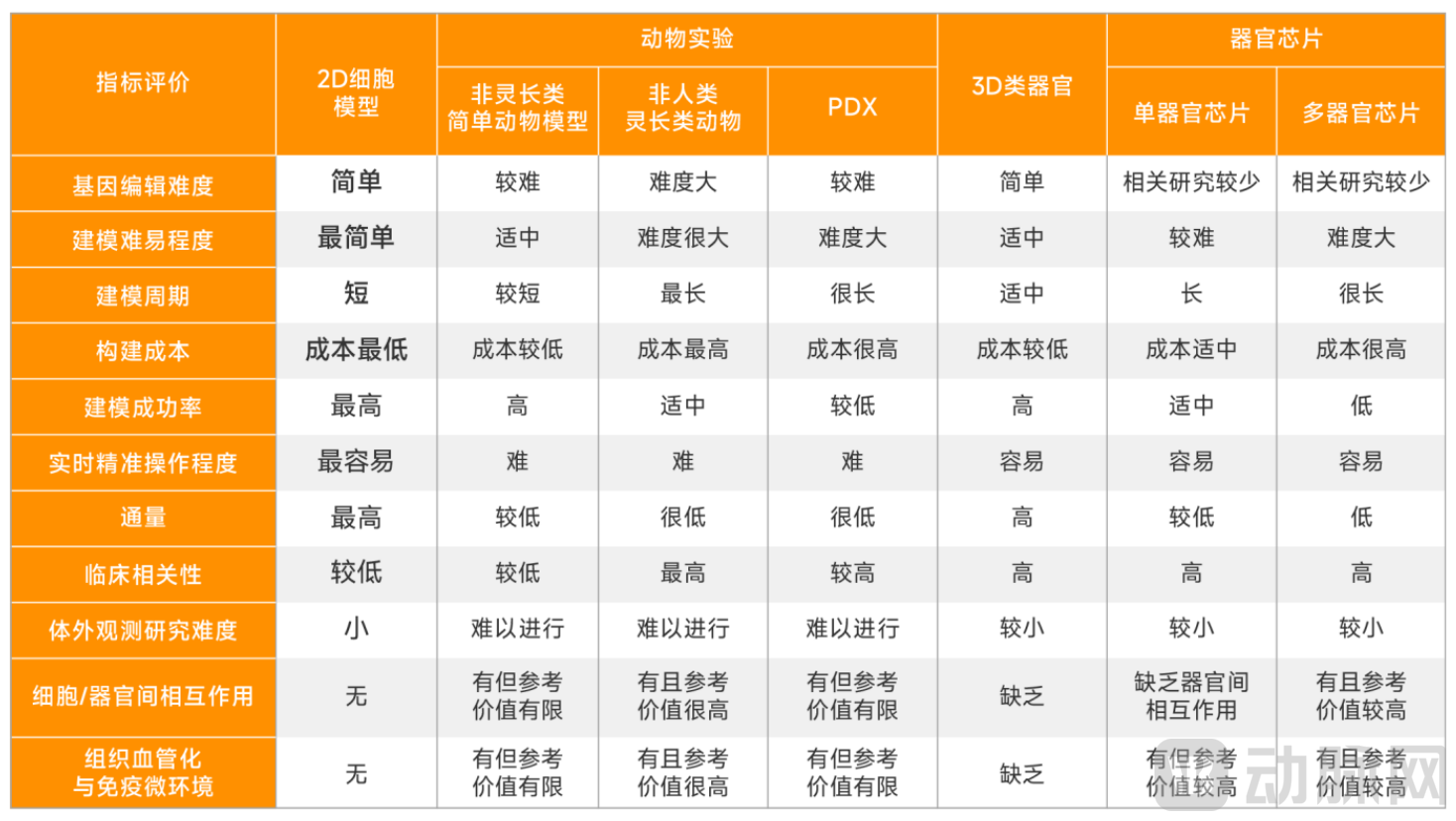

Advantages and Disadvantages of 2D Cell Cultures, Mouse Models, Non-Human Primates, Organoids, and Organ-on-a-Chip Applications

Data Source: Research interviews, chart by VCBeat

By leveraging in vitro biomimetic models such as organoids and organs-on-chips, the accuracy of predicting clinical drug efficacy can be effectively improved, thereby reducing drug development costs.

Comparison of the Advantages and Disadvantages of Traditional Biological Models, Organoids, and Organ-on-a-Chip Applications

Data Source: Survey interviews, chart by VCBeat.

Meanwhile, driven by continuous technological advancements, the advent of the precision medicine era, and the increasing complexity of new drug development, market demand for highly biomimetic human models such as organoids and organ-on-a-chip systems has further increased, ushering the industry into a period of robust growth.

Precision medicine has been a focal point of public attention in recent years.In the field of precision cancer therapy, the emergence of tumor organoids has created new opportunities for precision oncology.

Drug sensitivity testing using tumor organoids can accurately predict patient responses to anticancer drugs, guide patients to avoid ineffective medications with toxic side effects, select therapeutic regimens that effectively kill cancer cells, and reduce the risk of drug resistance and tumor recurrence.China has a large and continuously growing cancer patient population, which gives tumor organoids significant application prospects in the field of drug sensitivity testing.

On the other hand, the increasing complexity of new drug development models and therapeutic regimens has also driven the rapid growth of the organoid and organ-on-a-chip industry.

Traditional 2D cell models fail to simulate intercellular communication across different organs and the complex interactions among metabolites, hormones, and the immune system at the microenvironmental level; meanwhile, traditional animal models suffer from limitations such as interspecies differences, poor predictivity of actual human responses, ethical concerns, and constraints in imaging observation.For diseases with high human specificity, such as those involving immunology, metabolism, infection, the central nervous system (CNS), and rare disorders, traditional approaches like 2D cell models and model animals are inadequate for effective disease modeling.

In addition to the increasingly complex requirements for new drug development models, the growing complexity of treatment regimens has further driven demand for technologies such as organoids and organ-on-a-chip.

A decade ago, most pharmaceutical companies’ pipelines were dominated by small molecules. Today, they have expanded their portfolios to encompass a broad spectrum of innovative therapeutic modalities, ranging from small molecules to large molecules, and from traditional chemical drugs to monoclonal antibodies, bispecific antibodies, antibody-drug conjugates (ADCs), PROTACs, peptides, small nucleic acid drugs, gene therapy, and cell therapy.Since the mechanisms of action of most innovative therapeutic regimens primarily operate within the microenvironment (i.e., the intercellular space), addressing the challenges of multicellular co-culture is an imperative requirement.

Finally, the global trend toward animal-free practices is further accelerating rapid industry development.

With the strengthening of animal protection efforts, many countries and regions around the world have enacted laws and regulations prohibiting the use of animals for cosmetic testing. For instance, the European Union, Norway, New Zealand, Israel, and India have comprehensively banned animal testing for cosmetics and prohibited the market sale of cosmetics that have recently undergone animal testing.

Some European countries have even begun to implement bans on animal testing. China has also been gradually phasing out mandatory animal testing requirements for cosmetics.

In summary, the combined drive of technology, policy, and market factors has led to the current prosperity of the industry.

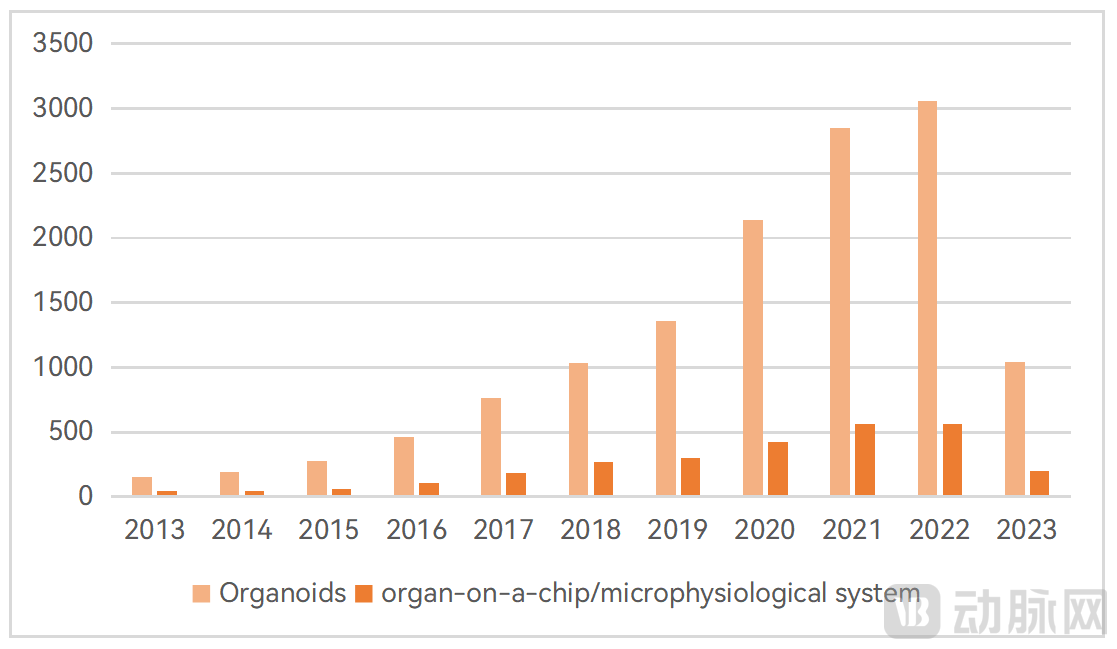

In scientific research, the number of publications related to organoids and organ-on-a-chip technologies is rapidly increasing.

Number of Global Scientific Publications on Organoids and Organs-on-Chips in the Past 10 Years

Data source: PubMed database; chart by VCBeat.

According to the PubMed database,Research involving organoid and organ-on-a-chip technologies has shown a linear upward trend over the past decade,Moreover, numerous articles have been published in top-tier journals such as CNS. The accumulation of research in basic science is further accelerating the industrialization of organoids and organ-on-a-chip technologies.

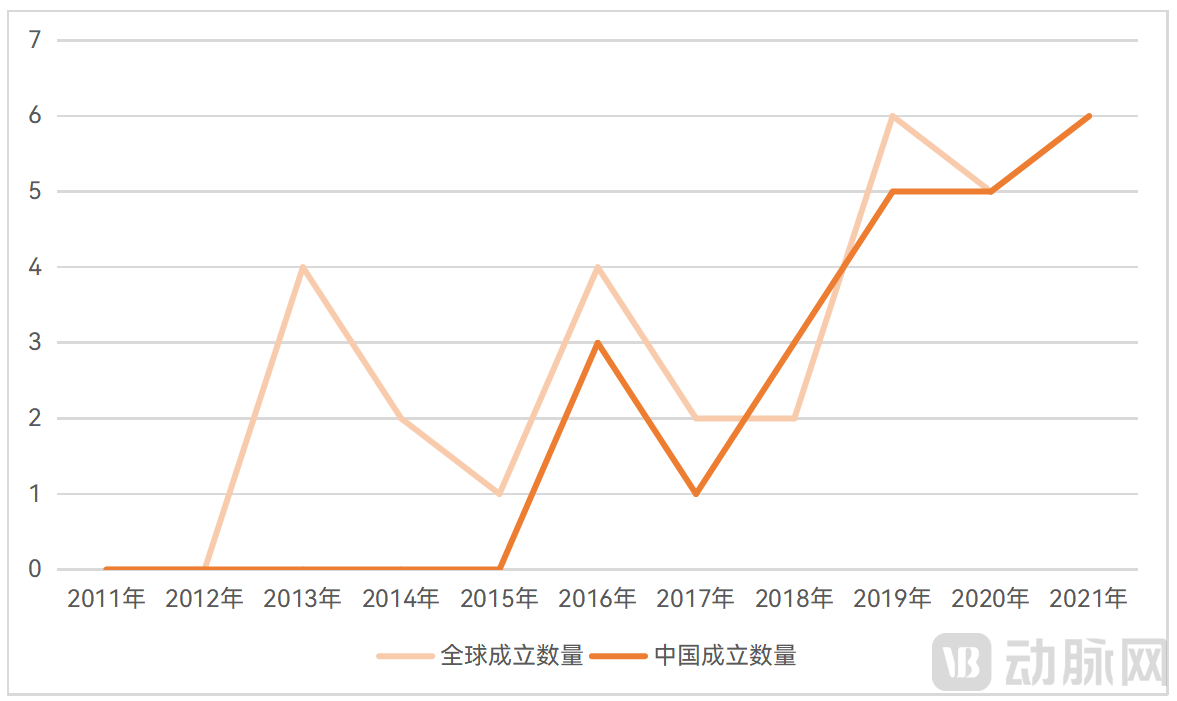

In terms of industry, multiple innovative enterprises have been established successively, and numerous companies have entered the organoid and organ-on-a-chip sectors through strategic innovation initiatives.According to incomplete statistics from VCBeat, there are currently over49These companies are strategically focusing on the organoid and organ-on-a-chip sectors.

Global Landscape of Company Foundings in the Organoid and Organ-on-a-Chip Sectors, 2011–2021

Source: Arterial Orange Database; Chart by VCBeat.

Before delving into an analysis of the current global landscape of organoids and organ-on-a-chip technologies, it may be necessary to first clarify the concepts of organoids and organ-on-a-chip.

As organoids and organs-on-chips are still in their early stages of development, there has been ambiguity in their definition and understanding within China. However,Clarifying and standardizing relevant concepts is undoubtedly important for fostering orderly competition and healthy development within the industry.

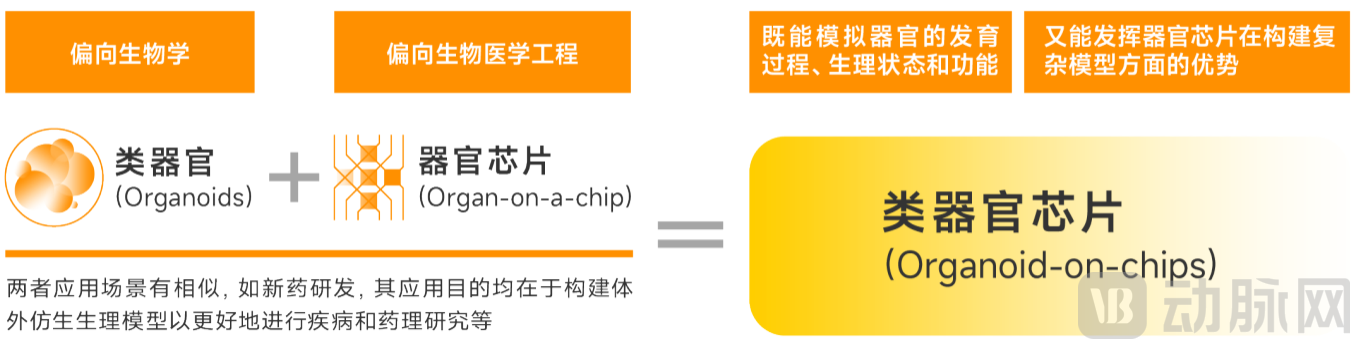

Based on prior interviews conducted by VCBeat New Medicine, Eggshell Institute conducted further research with additional industry professionals and reached the following conclusions:Organoids and organ-on-a-chip belong to different subfields, yet their application scenarios are similar.

The Relationship Between Organoids, Organs-on-Chips, and Organoid-on-Chip Systems

Data source: Interviews and surveys; chart by VCBeat.

Specifically,Organoids Leaning Toward Biology, belonging to the stem cell-related field, stem cells within organoids differentiate into various cell types during culture. The differentiated cells exhibit high similarity to human organs in terms of spatial organization and physiological function; however, they have limitations in controllability and reproducibility, with their complexity constrained by the differentiation capacity of the cells.

Organ-on-a-chip technology leans more toward biomedical engineering,The introduction of technologies such as microfluidics offers advantages in the controllability and standardization of modeling, enabling the construction of more complex models through co-culture techniques; however, it is often challenging to simultaneously meet the requirements for throughput, cost, and complexity.

Although organoids and organs-on-chips belong to distinct fields, they are frequently mentioned together or even conflated in China. The reasons for this includeBoth are alternative frontier technologies with certain synergies in application scenarios, and their shared objective is to construct in vitro biomimetic physiological models to facilitate disease and pharmacological research.

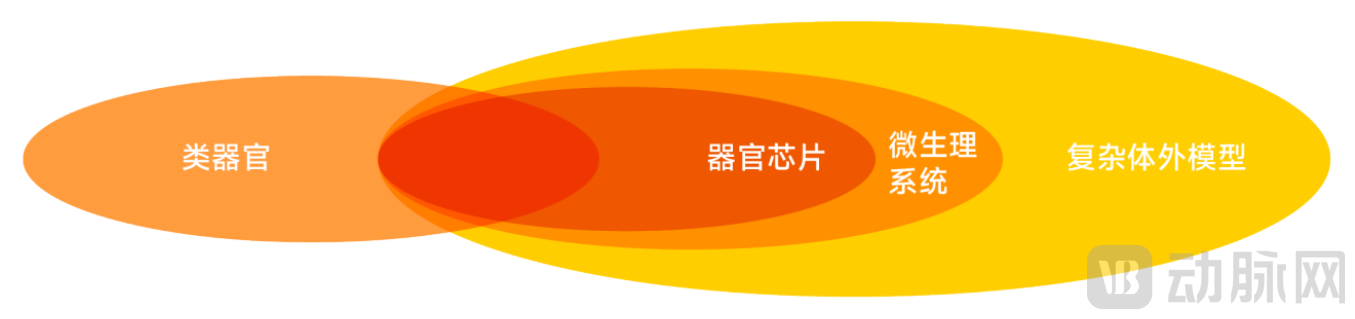

Organ-on-a-chip and microphysiological systems (MPS), as subsets of complex in vitro models (CIVMs), are often used interchangeably in the literature.

However, multiple industry experts unanimously agree thatMicrophysiological systems encompass a broader scope than organ-on-a-chip.The white paper provides clear and detailed explanations of the definitions related to various types of in vitro models; due to space limitations, these are not elaborated upon here.

Relationships Among Organoids, Organs-on-Chips, Microphysiological Systems, and Complex In Vitro Models

Data Source: Survey interviews, chart by VCBeat

Full Industry Chain Analysis: Midstream and Downstream Demand Has Yet to Scale Up, with 80% of Companies Also Engaged in Upstream Activities

Currently, the global organoid and organ-on-a-chip industry chainUpstreamIt primarily includes R&D and manufacturing enterprises for instruments and equipment, as well as for reagents and consumables. These companies provide the industry with automated high-throughput instrumentation for organoids and organ-on-a-chip applications, chip fabrication systems, and imaging equipment, along with reagents and consumables such as culture plates, assay kits, hydrogels, nanofibers, basement membrane matrix, synthetic scaffolds, proteins, specialized consumables, microfluidic chips, and substrates.

MidstreamA company providing organoids, organ-on-a-chip systems, and related technical services.DownstreamPrimarily including pharmaceutical and biotechnology companies (pharma companies), CROs, universities and other research institutions, cosmetics industry enterprises, hospitals, patients, etc.

Full Industry Chain Map of Organoids and Organs-on-Chips

Data sources: Official websites of various enterprises and research institutes; chart by VCBeat.

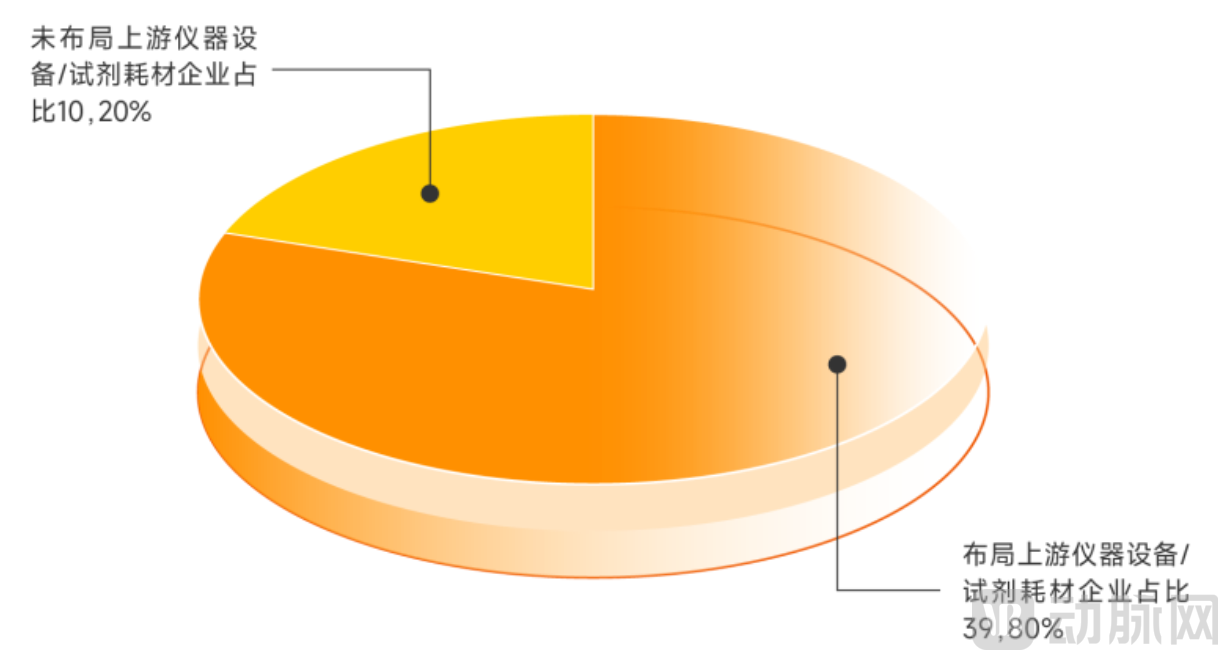

It is worth noting that, as the organoid and organ-on-a-chip industries are still in their early stages of development, demand in the mid- and downstream segments has yet to scale up; therefore,Many companies in the organoid and organ-on-a-chip sectors have, to some extent, assumed upstream roles by independently developing automated, high-throughput instrumentation and imaging equipment for organoids and organ-on-a-chip systems.

According to incomplete statistics from VCBeat,Up to 80% of global organoid and organ-on-a-chip companies are positioned in the upstream sector, focusing on instruments, equipment, reagents, or consumables.

Global Landscape of Upstream Operations in the Organoid and Organ-on-a-Chip Industry

Data source: VCBeat Orange Database; Chart by VCBeat.

As the industry continues to advance, the total demand from mid- and downstream sectors for upstream instruments, equipment, reagents, and consumables has further increased, giving rise to companies such as Bozhen Bio, which specialize in developing related instruments and equipment as well as researching, producing, and supplying reagents and consumables.

As the industry continues to develop in the future and relevant policies and standards are implemented,The surge in industry demand for upstream products will foster the emergence of more specialized upstream enterprises and drive business transformations among certain organoid and organ-on-a-chip companies. Enterprises that proactively and deeply establish their presence in the upstream sector will undoubtedly enjoy a first-mover advantage.

Industry Status Analysis: Overseas Development Progresses Faster Than in China, Showing Significant Development Disparities

Due to more robust foreign policies and funding support, as well as earlier initiation of research, the overall industrial development of organoids and organ-on-a-chip technologies abroad is ahead of that in China.

From the perspective of industrial applications, some overseas organoid companies have already addressed compliance and ethical issues related to organoid culture and use.For instance, HUB, an organoid technology incubator co-founded by Hans Clevers, has established a biobank of organoid models with substantial scale and diversity. This enables on-demand retrieval of specific organoid lines for targeted expansion and cryopreservation, thereby facilitating focused scientific research or serving downstream clients such as pharmaceutical companies.

such as InSphero, OcellO (acquired by CrownBio), and CellesceOverseas organoid companies have addressed key challenges in organoid culture, including high-throughput processing, reproducibility, and the lack of standardization associated with manual culture methods, thereby successfully applying this technology to drug development. Their primary customer base consists of pharmaceutical companies and research institutions.

The domestic organoid industry is developing rapidly, but capabilities in quality control for organoid culture and sample compliance need to be further enhanced.For instance, efforts to ensure the compliance and ethical integrity of organoid samples remain inadequate; furthermore, models in certain organoid banks have not yet met applicable standards due to a lack of relevant quality control criteria.

In the field of organ-on-a-chip,The core manufacturers of organ-on-a-chip technology are primarily distributed across North America and Europe, with leading companies such as Emulate, TissUse, Hesperos, and CN Bio accounting for over 50% of the global market share.Foreign organ-on-a-chip companies currently hold a dominant position, while China's industrialization process lags behind.

The reason lies in the fact that organ-on-a-chip is a highly interdisciplinary, cutting-edge technology with significant technical barriers. Furthermore, as countries at different stages of development prioritize different challenges, China’s organ-on-a-chip industry lacks the comprehensive financial backing and systematic government support seen in Europe and the United States.

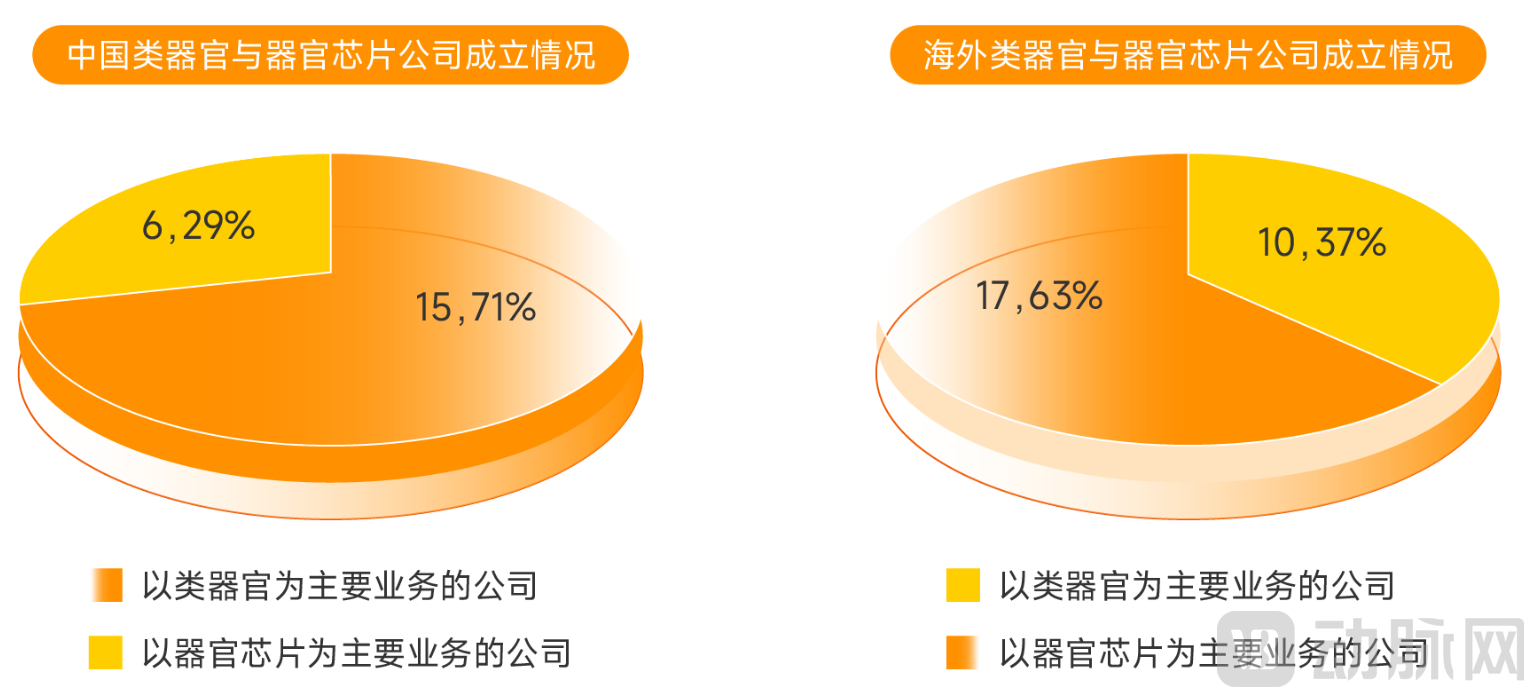

The momentum for organoid industry development is stronger in China, while foreign markets account for a larger proportion of companies focused on organ-on-a-chip technology; the developmental priorities in the fields of organoids and organ-on-a-chip are nearly opposite between domestic and international markets.

According to incomplete statistics from VCBeat, companies in China whose primary business is the development of organoids currently account for [percentage] of the total number of enterprises in the domestic organoid and organ-on-a-chip sector.71%, the proportion of overseas companies whose primary business is the development of organ-on-a-chip technology accounts for [a certain percentage] of the total number of enterprises in the overseas organoid and organ-on-a-chip sector.63%。

Differences in the Establishment of Organoid and Organ-on-a-Chip Enterprises: Domestic vs. International

Data Source: VCBeat Orange Database; Chart by VCBeat

We believe that there are two main factors contributing to this phenomenon:First, the foundations of technological accumulation differ; second, market demand development varies due to differing national conditions.

First, in the field of organoids, the reasons behind the statement that “the momentum of domestic industry development in organoids is even stronger” include some technical issues and obstacles mentioned above, as well as the imperfect regulatory approval guidance policies in China. In addition,Due to differing national contexts, the application of organoids in clinical settings for drug sensitivity screening—a key component of precision oncology—is a market demand in China that distinguishes it from overseas markets.

As a country with a high cancer burden, China has an enormous base of total cancer patients and a vast number of new cases each year, while the five-year survival rate for cancer patients is significantly lower than that in developed countries overseas. In addition to treatment modalities themselves, a critical factor influencing the five-year survival rate is early screening and early diagnosis.

Chinese people have weak awareness of early cancer screening, and most patients often seek diagnosis and treatment only when the disease has progressed to a stage with very obvious symptoms.Since a large number of cancer patients are asymptomatic in the early stages of the disease, diagnoses are more frequently made at the intermediate to advanced stages. Consequently, most Chinese cancer patients are already at an intermediate or advanced stage upon diagnosis. At this point, rapidly identifying an appropriate medication regimen for the patient would undoubtedly be of significant benefit.The large and continuously growing cancer patient population in China presents significant application prospects for tumor organoids in the field of drug sensitivity testing.

In addition to the expectations of China's capital market for the precision medicine market,The interest shown by overseas capital in the organoid company Xilis also indicates, to some extent, its recognition of applying tumor organoids to drug sensitivity screening for precision cancer medicine.

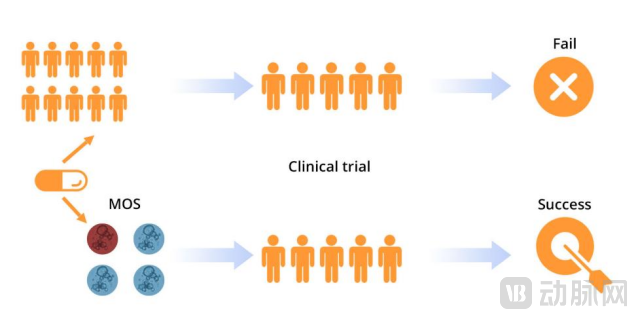

Advantages of the Xilis Enterprise MOS Platform

Data Source: Xilis Official Website

Founded in 2019, Xilis has raised over $89 million in its Series A financing alone, emerging as a hot new player in the current market. Its proprietary MicroOrganoSphere™ (MOS) platform is a scalable, patient-derived organoid model for drug discovery.By integrating AI-powered imaging analysis tools, Xilis can rapidly and accurately predict patient treatment responses based on tumor organoids, helping clinicians develop targeted, personalized cancer treatment strategies.

Of course, the reason overseas capital favors Xilis is not limited to cancer precision medicine; assisting pharmaceutical companies in new drug development is also an important business segment for Xilis, reflecting its technological strength.

A larger proportion of organ-on-a-chip companies are based overseas,We hypothesize that the primary reasons also lie in two aspects.

First, foreign countries are more advanced in drug development, leading to a more urgent market demand for organ-on-a-chip technology.

As mentioned earlier in the report, the R&D focus of pharmaceutical companies is shifting from small molecules to large molecules, and from chemical drugs to antibody drugs, PROTACs, peptides, small nucleic acid drugs, and gene and cell therapies. Traditional biological models can no longer meet the current R&D needs of pharmaceutical enterprises.

In addition, Dr. Yin Xiushan, founder of Kunshi Biotechnology, pointed out thatIn conducting animal experiments, foreign countries face greater ethical pressures and higher time costs compared to China.

For example, animal experiments involving gene editing require the use of primates. However, given the current policy environment and availability of animal resources in Europe, researchers may face a waiting period of more than four years to conduct such experiments, along with significant hurdles in obtaining ethical approvals. In contrast, in China, relevant experiments can potentially commence within three months, provided that funding and resources are in place.

Currently, the volume of animal experiments conducted by many European research institutes has declined sharply. Some companies, such as T-knife Therapeutics, have completely relocated their animal testing-related operations to the United States.

Secondly, the organ-on-a-chip industry started earlier in the United States, and government agencies have provided greater support for related research.

Currently, China’s organ-on-a-chip technology remains in its early stages of development. Few teams have mastered the core technologies, with most still focusing on relatively simple or specific types of organ chips, indicating substantial room for growth.

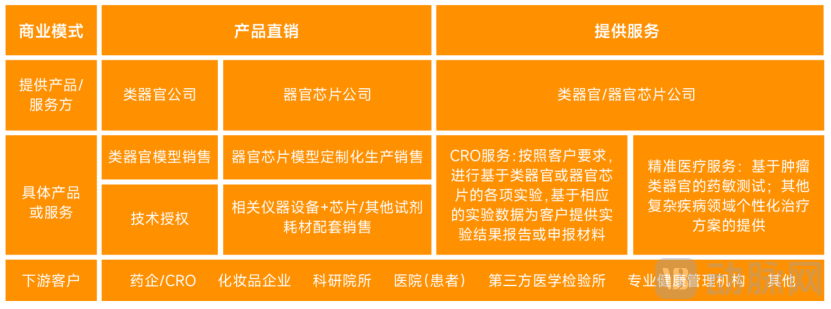

According to research and interviews conducted by VCBeat Institute,The global organoid and organ-on-a-chip industry currently features two primary business models: direct product sales and service provision.There are slight differences in the performance of the organoid and organ-on-a-chip industries.

Major Business Models of Organoid and Organ-on-a-Chip Companies

Source: Research interviews; chart by VCBeat

Direct Product SalesThis generally refers to organoid or organ-on-a-chip companies directly providing organoid models or organ-on-a-chip models to customers as standardized products, with various sales formats available depending on the specific requirements of different customers.

For organoids, the most mainstream direct sales model is the sale of standard organoid models.Organoid providers supply specific types of organoids to customers (primarily B-end clients such as pharmaceutical companies, CROs, cosmetics companies, and research institutes) to meet their R&D requirements.

However, Dr. Lu Zhenghao, R&D Director of Organoids at Jingke Biologics, pointed out that “this model still requires further exploration, particularly for patient-derived organoids. Beyond regulatory policy considerations, greater emphasis is placed on the application value associated with organoids. Therefore, organoid companies primarily deliver the research value of specific types of organoids to clients in the form of technical services.”

Another Profit Model for the Organoid IndustryIt refers to enterprises licensing their technology externally in the form of technical licenses, thereby generating IP licensing fees.For instance, HUB has facilitated the establishment and development of companies such as Epistem, Cellesce, and Crown Biosciences through technology licensing.

In the field of organ-on-a-chip, the most prevalent direct sales model is customized production and distribution.Specifically, organ-on-a-chip companies carry out customized design and manufacturing of organ chips according to customer requirements and provide the corresponding equipment and devices to customers.Another Profit ModelIt is a bundled sales model in which companies offer organ-on-a-chip instruments and equipment, chips, and other reagents and consumables as an integrated package:The company provides customers with the necessary equipment for operations through various models, including sales, leasing, or gifting, while also selling chips and other reagents and consumables to them.

Service ModelThis generally refers to organoid or organ-on-a-chip companies leveraging their proprietary models to directly provide corresponding support services based on customer requirements, primarily encompassing two types of services.

Among them,CRO ServicesRefers to organoid or organ-on-a-chip companies conducting various experiments based on organoids or organ-on-a-chip technologies according to customer requirements, and then providing experimental result reports or application materials to customers based on the corresponding experimental data.Precision Medicine ServicesPrimarily refers to drug sensitivity testing based on tumor organoids, providing personalized medication regimens for cancer patients in need.

It is worth noting that,The channels for precision medicine services differ slightly from the aforementioned profit models.The service delivery entities are primarily hospitals, third-party medical laboratories, or professional health management institutions.Therefore, it is evident that many organoid companies have established independent third-party clinical laboratories as part of their strategic layout, such as Jingke Biotechnology, Ketu Medicine, Chuangxin International, and Danwang Medical.

Currently, no company globally focused on organoids and organ-on-a-chip technologies has gone public. The fastest-growing player is Emulate, an organ-on-a-chip company that has secured Series E financing. Many other companies in the industry, such as Epistem, OcellO, and TARA Biosystems, have achieved their next stage of development through acquisitions. What are the potential future development paths for companies in the organoid and organ-on-a-chip sector?

Three Potential Future Development Paths for the Industry: Precision Instrument and Equipment Manufacturers, CROs, and Biotech Companies

Data source: Survey interviews; chart by VCBeat.

Regarding the future development path of organoid and organ-on-a-chip companies, some industry experts believe that,Companies such as Emulate may gradually transition into precision instrument and equipment manufacturers in the future.(Equipment and reagents are its core)Development, which is evident from its business layout.

A review of Emulate’s product portfolio reveals that the company is currently developing various types of organ-on-a-chip models. Industry insiders have pointed out, “Emulate is expanding the variety of its organ-chip models to drive sales of its equipment.” This strategy is also partially reflected in the company’s personnel appointments and transfers over the past two years.

Other industry experts believe that,Fundamentally, organoids and organs-on-chips constitute a technological platform primarily designed to serve specific stages of the new drug development process; their mainstream future development should be positioned within the contract research organization (CRO) sector.For instance, some investors believe that the organoid sector falls within the broader category of life science tools, and its future industry development logic will resemble that of the CRO industry, with both featuring a “gold digger” and “water seller” dynamic.

Furthermore, based on interviews and surveys conducted by VCBeat with numerous industry veterans, we have also identified another business model that is likely to become widespread in the future, namelyA biotech company developing new drugs based on organoids or organ-on-a-chip technology.Teams with drug development capabilities can independently develop new drug pipelines by leveraging their strengths in constructing organoid or organ-on-a-chip models. Future development pathways may draw reference from the business model of “AI Biotech” enterprises in the AI-driven new drug sector.

Currently, the primary application scenarios in the organoid and organ-on-a-chip industry includeDisease modeling, toxicity testing, high-throughput drug screening, drug evaluation, drug indication expansion, precision cancer therapy, regenerative medicine, aerospace medicine, etc.

Current Main Application Scenarios of Organoids and Organs-on-Chips

Source: Research interviews; chart by VCBeat

Among them,Precision cancer therapy is currently the most dynamic market for organoid technology applications in China.Industry practitioners have estimated to VCBeat that the annual number of samples collected for organoid-based precision medicine in China has exceeded 10,000. Hospitals such as Nanfang Hospital, Changhai Hospital, West China Hospital, and Fudan University Shanghai Cancer Center have already launched corresponding clinical studies.

Currently, organoid technology covers more than 20 types of cancer-derived organoids, including those for lung cancer, breast cancer, cholangiocarcinoma, gastric cancer, and colorectal cancer, with in vitro culture success rates for certain tumor organoids reaching as high as 95%.Combining with next-generation sequencing can further enhance the precision treatment outcomes for cancer patients.Currently, organoids are primarily used for chemosensitivity testing; with technological advancements, they hold significant potential for future applications in targeted therapy and immunotherapy.

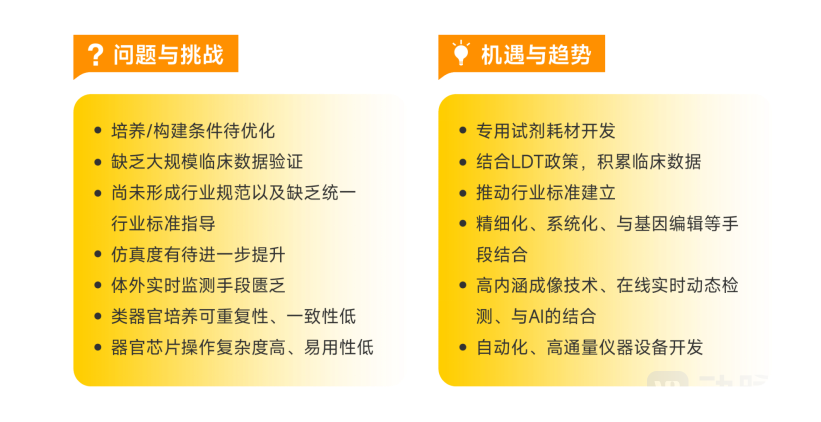

Although the market for using organoids in drug sensitivity testing is currently booming, certain developmental limitations must be viewed objectively.

One challenge lies in the difficulty of scaling up product applications due to the high heterogeneity of tumors.In organoid-based precision medicine experiments, personalized designs are required for each case based on patient and sample characteristics. Different tumor types, samples from different anatomical sites, and distinct cell types within the samples all necessitate specific culture methods and formulations. This complexity may hinder the near-term commercialization of organoid precision medicine, resulting in a slow growth of its market size.

Furthermore, some companies have pointed out that “even after completing technological and industrial iterations, the proportion of cancer patients who truly have the need and opportunity to benefit from organoid-based precision medicine remains relatively limited among both existing and newly diagnosed populations.”

Additionally, tumor heterogeneity is also manifested as spatial heterogeneity.“Whether the tumor tissue used for organoid culture encompasses all lesions directly impacts the accuracy of drug screening. Currently, organoids still need to address key challenges in more accurately reflecting clinical heterogeneity and the influence of the tumor microenvironment on drug response, in order to truly achieve precise guidance for patient medication.”Dr. Song Guangqi, founder of Puheng Technology, previously served at Zhongshan Hospital affiliated with Fudan University and possesses in-depth knowledge of the pain points associated with clinical product applications.

Source: Research interviews; chart by VCBeat

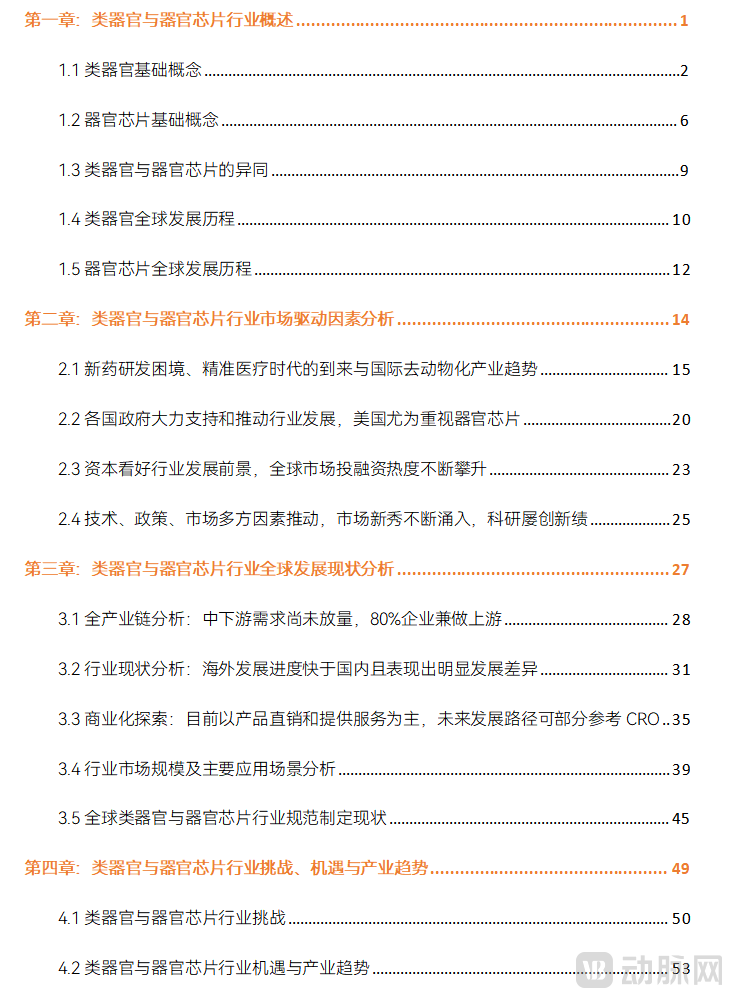

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Please scan the QR code to add our assistant and obtain the full report. After adding, please initiate your inquiry proactively.

Special Acknowledgments (in order of industry research):

Zhao Xiaoyang, Executive Partner at GTJA Investment; Xie Shutao, Vice President of Business Development at Bozhen Biotech; Yin Xiushan, Founder of Kunshi Biotech; Song Guangqi, Founder of Puheng Technology; Hua Guoqiang, Founder of Danwang Medical; Chen Zaizao, Deputy General Manager of Aweide Biotech; Lu Zhenghao, R&D Director of Organoids at Jingke Biotech; and other unnamed corporate executives and venture capitalists.