Boston Scientific Eyes $10B Shockwave Medical Acquisition as Vascular Calcification Market Heats Up

Shockwave Medical

Cardiovascular Disease Treatment Device Developer

Recently, Bloomberg reported that medical device giant Boston Scientific (BSX.N) is exploring the acquisition of cardiovascular medical device company Shockwave Medical (SWAV.O) to expand its cardiovascular product portfolio.

If Boston Scientific indeed acquires Shockwave Medical, it would be the company’s largest acquisition in recent times. However, neither Shockwave nor Boston Scientific has commented on the matter at this time.

Following the news, Shockwave Medical’s shares surged, with its market capitalization currently standing at approximately $10.5 billion, compared to Boston Scientific’s market cap of around $73.4 billion.

Analysts predict that Boston Scientific is poised to acquire a target for over RMB 70 billion, reigniting interest in the vascular calcification sector. Prior to Boston Scientific, another cardiovascular giant, Abbott, also moved to enter this space in February of this year.

Abbott Acquires Peripheral Interventional Atherectomy Leader Cardiovascular Systems, Inc. (CSI) for $890 Million; the Deal Has Drawn Significant Attention, with Shockwave and CSI Being Direct Competitors.

The attention from two cardiovascular giants, Boston Scientific and Abbott, indicates that this sector is heating up. The medical device industry is fiercely competitive and rapidly evolving, with new technologies exerting a significant impact on market dynamics.

The cardiovascular market remains the core focus for global industry giants, with growth increasingly driven by innovative products. Shockwave Medical’s flagship intravascular lithotripsy (IVL) system has already been commercialized in major cardiovascular markets worldwide. As leading companies intensify their investments in this space, can vascular calcification plaque modification technologies disrupt the global cardiovascular market? VCBeat (WeChat ID: vcbeat) has compiled an analysis.

Spotlight on Shockwave: What Makes It a Target for Industry Giants?

Shockwave Medical’s core product is its intravascular lithotripsy (IVL) system. True to its name, the launch of IVL sent shockwaves through the industry.

IVL, this star product, has been commercialized in the major cardiovascular disease markets of the United States, Europe, China, and Japan.Intravascular Lithotripsy (IVL) for Calcified Lesion Fragmentation was approved for market launch in Europe in 2018, received FDA approval in 2021, and was approved for marketing in China in 2022. Compared with other products that typically require up to a decade to achieve global commercialization, the rapid worldwide adoption of IVL underscores its clinical acceptance and the significant attention it has garnered.

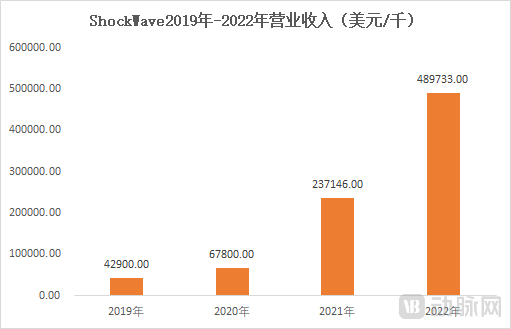

Since its IPO, IVL has demonstrated impressive commercial performance, maintaining robust growth from 2019 to 2022.

In 2022, Shockwave’s revenue reached $489 million, a year-on-year increase of 107%., a performance far superior to that of similar products. Taking CSI, which was acquired by Abbott, as an example, CSI’s revenue for fiscal year 2022 was $236.2 million, a decrease of $22.8 million, or 8.8%.

Unlike CSI, whose revenue is primarily derived from the peripheral intervention sector, Shockwave’s income is mainly driven by percutaneous coronary intervention (PCI) procedures in the coronary arena. In 2022, its revenue from the coronary segment reached $353 million, while peripheral revenue amounted to $132 million.

Shockwave has also demonstrated strong performance in the capital markets, with its share price surging 795.10% in just four years since going public. With a current market capitalization exceeding $10 billion, it is poised to become the latest tenbagger in the pharmaceutical sector.

Most medical devices have a relatively low market ceiling, as the diversity of surgical procedures, indications, application scenarios, and functional requirements makes it difficult for blockbuster products to emerge. Since its launch two years ago, IVL has generated nearly $500 million in sales. Given its rapid growth trajectory, IVL is poised to become a new blockbuster product in the coronary field.

What makes IVL a global phenomenon and a star product is its ability to address the challenge of treating vascular calcification.

Among vascular diseases, moderate-to-severe calcified lesions are regarded as the most formidable challenge in coronary intervention. Despite the rapid advancements in percutaneous coronary intervention (PCI), managing calcified lesions with PCI remains one of the major difficulties faced by interventional cardiologists.

Moderate-to-severe calcified lesions are major risk factors for procedural failure and acute vessel occlusion during percutaneous transluminal coronary angioplasty (PTCA). In particular, severely calcified lesions that are tortuous, angulated, or diffuse pose greater procedural risks and are associated with higher rates of immediate complications as well as early and late stent thrombosis. Although various solutions have been developed in the industry, primarily specializing in specialty balloons and plaque modification devices, both categories have their limitations.

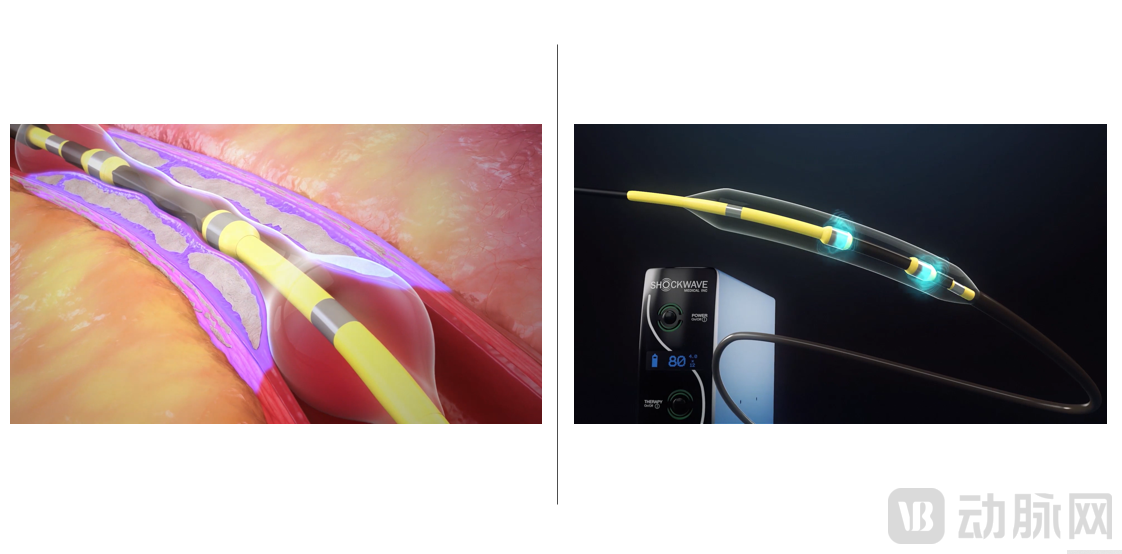

The innovation of IVL lies in drawing inspiration from shockwave technology used in kidney stone treatment. By delivering pulsed acoustic pressure waves to calcified lesions via a balloon catheter, it “fractures” the calcified plaques, thereby restoring vascular elasticity and remodeling blood flow in diseased vessels. Meanwhile, it avoids damage to the vascular intima, as the shockwave energy acts selectively on hard calcified lesions without harming the normal structure of the vessel wall.

IVL Product Schematic Diagram

Becoming a blockbuster product requires not only a high degree of innovation and strong competitive barriers, but also a large addressable market.

How High Is the Ceiling for Vascular Calcification Management?

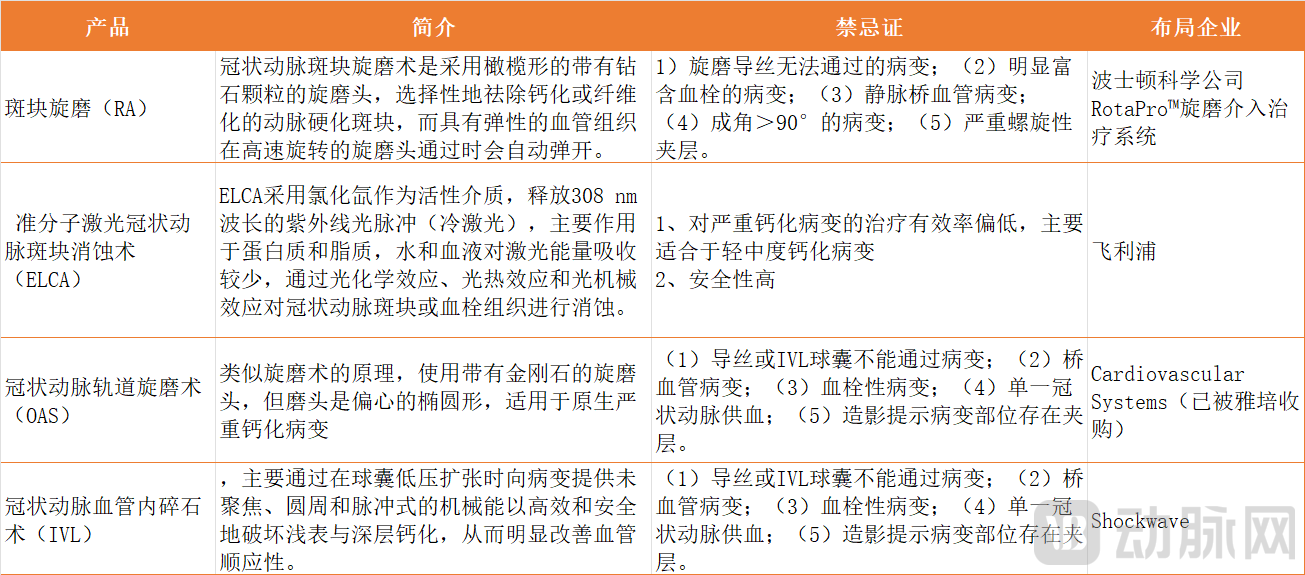

The market for vascular calcified plaque modification mainly consists of three segments: calcification management in PCI procedures, calcification management in peripheral artery disease, and lumen preparation for large-bore implants.

According to data from Frost & Sullivan, the number of PCI procedures in the United States increased from 592,700 in 2015 to 1 million in 2021, and is projected to reach 3.5 million by 2030. Among the 1 million patients undergoing PCI annually in the United States, up to 30% have calcified vascular lesions. In China, among the 1 million coronary artery disease patients receiving PCI, approximately 200,000 to 300,000 have moderate-to-severe calcified lesions. Globally, at least 500,000 patients require calcification management each year.

How to help physicians address the challenge of vascular calcification in percutaneous coronary intervention (PCI) has long been a key market focus for major global cardiovascular companies. The intravascular lithotripsy segment, where Shockwave Medical operates, is highly competitive, with its main players being Boston Scientific, Medtronic, Abbott, Cardiovascular Systems, Inc. (“CSI”), and Philips.

Although multiple companies have entered the field, the market size for vascular calcification treatment in China has yet to achieve significant growth.

Taking rotational atherectomy as an example, Boston Scientific’s coronary rotational atherectomy products have been in the Chinese market for a considerable period. However, due to early concerns about complications, their adoption was limited, with the number of rotational atherectomy procedures surpassing 10,000 only in 2021. Even in developed countries in Europe and the United States, the utilization rate of rotational atherectomy in percutaneous coronary intervention (PCI) remains at merely 5%.

The lack of market uptake is primarily due to safety concerns.The unresolved challenge with existing plaque modification devices is that coronary arteries often have thick calcium layers, and current plaque modification equipment struggles to treat these calcifications without damaging the blood vessels, thereby reducing the risk of complications. This limitation has resulted in restricted cardiovascular applications for plaque modification devices.

Another major factor limiting market size is the technical difficulty for physicians in operating rotational atherectomy devices, which leads to prolonged procedure times.Furthermore, given the relatively high prices of certain domestic products, the volume of procedures utilizing plaque modification devices in the coronary artery field in China remains low.

Shockwave’s IVL has achieved rapid growth in the coronary market, with two major advantages over similar products being safety and ease of use.

From a safety perspective, unlike existing balloon-based calcium modification technologies (such as predilation balloons, non-compliant [NC] high-pressure balloons, and specialized balloons), Intravascular Lithotripsy (IVL) is driven by sonic pressure waves rather than the expansion pressure of the balloon itself. The balloon requires only 4 atm to reach the operational pressure for pulse activation, thereby avoiding pressure-induced injury to the vessel wall associated with high-pressure balloons and reducing the risk of arterial dissection. Compared with coronary atherectomy, IVL operates via a "non-contact" mechanism. Unlike atherectomy, which causes significant traumatic intimal ablation, IVL preserves the integrity of the vascular intima and selectively targets calcified lesions. This approach significantly reduces the incidence of complications associated with atherectomy, such as vascular dissection, perforation or rupture, and burr entrapment.

IVL is also relatively simple to operate. The IVL procedure is very similar to conventional balloon angioplasty, making it easy for physicians to perform and associated with a low learning curve.

Leveraging its robust product portfolio, Shockwave has been applied in over 70,000 patients with coronary artery disease across Europe and the United States. Currently, there remains significant room for market penetration.Shockwave estimates that the total market size for intravascular lithotripsy is approximately $8.5 billion.

Shockwave is also exploring other niche markets beyond coronary and peripheral applications. It is primarily used in TAVR and endovascular aneurysm repair (EVAR) procedures to manage arterial calcification in the access vessels. Since calcification can hinder the endovascular delivery of implants, IVL can help physicians perform plaque modification beforehand. According to the consulting firm Clarivate, approximately 215,000 EVAR and thoracic endovascular aortic repair (TEVAR) procedures are performed globally each year, with up to 20% of these cases at risk due to lower extremity arterial calcification. Shockwave estimates that this access market is worth approximately $200 million.

In addition to its application in calcified vascular lesions, Shockwave Medical is developing the use of shockwave technology for the treatment of valvular disease. Leveraging the combined mechanical effects of shockwaves to decalcify tissue, this approach mechanistically avoids soft tissue injury and is intended for the treatment of aortic valve calcification.

IVL’s performance in terms of safety and ease of use has led the industry to believe that IVL is poised to become another blockbuster product in the coronary field, following stents.

Currently, multiple domestic companies are actively engaged in R&D and strategic positioning within this sector. These include Saihe Medical, Puchuang Medical, Blue Sail Medical, and Beixin Medical, among others. At present, domestically produced products have not yet been commercialized. Notably, several of these companies have secured financing exceeding RMB 100 million, indicating strong expectations from the Chinese capital market for these products.

In China, Shockwave Medical and Jian Shi have entered into a partnership to establish a joint venture and introduce Intravascular Lithotripsy (IVL) technology. Following the product’s market launch, Jian Shi’s Wuxi R&D and manufacturing base will set up a production line for the manufacture of Shockwave’s intravascular lithotripsy products.

As of now, Boston Scientific has not responded to whether it will acquire Shockwave Medical at a high price.

However, based on Boston Scientific’s recent M&A strategy, the company will continue to pursue an aggressive acquisition approach. Over the past decade, Boston Scientific has spent $18 billion on mergers and acquisitions, a strategy that has enabled it to maintain a leading position in multiple fields and rapidly enter other high-growth markets.

In recent years, Boston Scientific has successively acquired Acotec Scientific, M.I.Tech, Apollo Endosurgery, Inc., Obsidio, Inc., Prevtice, Farapulse, and Baylis Medical.

Boston Scientific’s M&A activities have primarily focused on three key areas: cardiac electrophysiology, endoscopic consumables, and peripheral interventions. These three business segments have also driven Boston Scientific’s high growth.

In these three major sectors, the inorganic growth driven by mergers and acquisitions is evident.

In the cardiovascular market, Boston Scientific reported cardiology revenue of $5.932 billion in 2022, with net sales increasing by 9.4%. This performance stands out compared to other cardiovascular giants; Medtronic’s cardiovascular business saw a year-over-year growth of 6% in fiscal year 2022. Abbott’s strongest performance was in the structural heart disease market, which grew by 6.3%, while its heart failure business revenue increased by 3.5%, and its electrophysiology business by 1.1%. Boston Scientific’s growth was primarily driven by left atrial appendage closure devices and cardiac electrophysiology products, as well as the impact of related acquisitions.

In the peripheral intervention sector, Boston Scientific reported operating revenue of $1.899 billion, a 4% year-over-year increase, primarily driven by growth in its peripheral drug-coated balloons, drug-eluting stents, and peripheral catheters and guidewires.

Boston Scientific’s fastest-growing business is its Urology division, which generated $1.773 billion in revenue, a 12% year-over-year increase. The primary growth drivers for the Urology and Pelvic Health businesses were the Rezūm System for treating benign prostatic hyperplasia (BPH), the SpaceOAR™ hydrogel product for prostate cancer treatment, and the acquisition of Lumenis’ surgical intervention business.

In the endoscopy business segment, Boston Scientific reported revenues of $2.221 billion, representing an 18% year-over-year increase. The primary growth drivers in the endoscopy field were the AXIOS electrocautery-enhanced lumen-apposing metal stent (EC-LAMS) and single-use duodenoscopes.

Neuromodulation Business: Boston Scientific reported fiscal year 2022 revenue of $917 million, with growth of less than 1%.

Based on the financial data released by Boston Scientific, the secret to its rapid growth can be simply summarized as: innovative products + acquisitions to enter new markets.

As the global cardiovascular sector matures, sustaining high-speed market growth in the future will depend on the drive of innovative products. Particularly in the Chinese market, mature products are affected by volume-based procurement, which compresses market space and shortens the lifecycle from innovative to mature products. For industry giants, not only is excellent product innovation capability required, but strategic M&A capability has also become increasingly important.

Reference: Intravascular Lithotripsy (IVL) for Percutaneous Coronary Calcification Fragmentation—New Advances in Interventional Treatment of Calcified Lesions—Chinese Journal of Cardiology