White Paper on the Radiopharmaceutical Industry: Mapping Nearly 7,000 Global Pipelines in the Race for Innovation in Targets, Ligands, and Radionuclides

The Radiopharmaceutical Market Feels No Chill from the Capital Winter! This Niche Sector, Once Constrained by Multiple Bottlenecks and Marked by Uneven Development, Is Now Thriving with the Approvals of Lutathera and Pluvicto.

2022 was a year of unprecedented activity in the radiopharmaceutical market, characterized by robust financing, product advancements, and commercial collaborations. The emergence of new entrants, novel targets, and new radionuclides made radiopharmaceuticals a bright spot amidst the broader downturn in the innovative drug sector. As 2023 began, radiopharmaceuticals remained at the forefront of the innovative drug market, sustaining their strong momentum. Companies such as Grand Pharma, Hengrui Medicine, Sinotau Pharmaceuticals, and Hexin Pharmaceutical have further accelerated the pace of radiopharmaceutical R&D and financing.

As the demand in the radiopharmaceutical industry enters a new cycle of rapid expansion, we conducted surveys on15 companies and interviews with 18 industry experts jointly explore the driving forces behind the sustained boom in the radiopharmaceutical sector.

Core Views:

In 2022, cumulative financing reached nearly RMB 900 million; amidst a sluggish market for innovative drugs, the radiopharmaceutical industry stood out with its exceptional financing performance.The release of major policies, such as the “Medium- and Long-Term Development Plan for Medical Isotopes (2021–2035)” and the “Technical Guidelines for Clinical Evaluation of Radiopharmaceuticals for Internal Use,” has sent strong positive signals. The impact of these favorable policies was first reflected in financing, with the radiopharmaceutical industry delivering strong performance in the capital market as expected. In 2022, radiopharmaceuticals accounted for the highest proportion of financing rounds exceeding RMB 100 million among all subsectors within the innovative drug industry.

With 75 drug candidates under development in China and nearly 7,000 entering clinical trials overseas, innovative radiopharmaceutical R&D has entered a high-yield phase.According to statistics from VCBeat, there are 75 pipelines under development in Chinese enterprises, while 6,468 pipelines have entered clinical trials overseas. Among them, Lutetium [177Lu]-labeled drugs are gaining significant momentum,Actinium [225[Ac]-labeled drug-targeted alpha therapy has rapidly gained attention, gallium [68[68Ga]-Labeled Drugs and Other Novel Tumor Imaging Agents Are Gaining Significant Momentum.There is little disparity in actual R&D capabilities between domestic and international markets, and the global radiopharmaceutical R&D market is flourishing.

The expansion of the radiopharmaceutical industry hinges on breakthroughs in novel targets, new molecules, new indications, and new radionuclides.As the radiopharmaceutical industry experiences explosive growth, pipeline homogenization has inevitably emerged. For instance, a significant number of pipelines are focused on SSTR and PSMA targets, aiming at neuroendocrine tumors and prostate cancer, while an increasing number of companies are also laying out strategies around FAP. There are few successful cases of innovative radiopharmaceuticals in the industry, necessitating that companies explore more targets such as Her2, CD38, and NTSR-1, more molecules including nanobodies and peptides, and actinium [225Ac], Astatine [211At] and other radionuclides, as well as more indications such as renal cell carcinoma, pancreatic cancer, and lung cancer,Simultaneously focus on addressing key issues such as upstream radionuclide supply and downstream nuclear medicine department development.

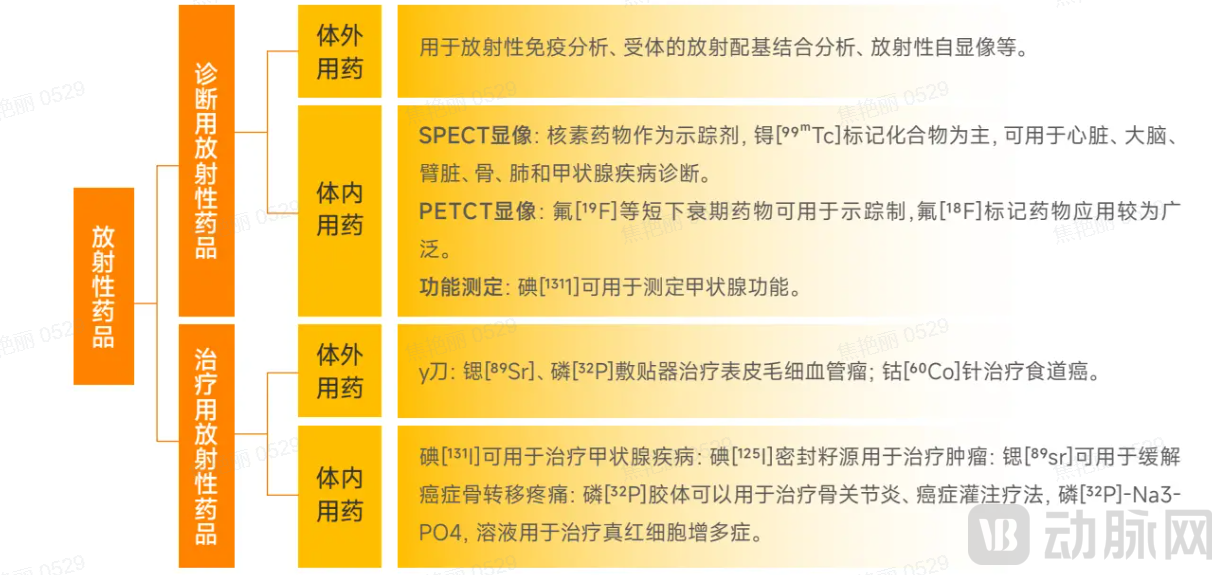

Based on their clinical applications in nuclear medicine, radiopharmaceuticals can be classified intoIn Vivo RadiopharmaceuticalswithIn Vitro Nuclear MedicineTwo categories. In vitro radiopharmaceuticals mainly refer to radioisotope-labeled immunodiagnostic reagents, while in vivo radiopharmaceuticals can be classified according to their specific applications intoDiagnostic RadiopharmaceuticalsandTherapeutic Radiopharmaceuticals。

According to the Technical Guidelines for Clinical Evaluation of Radiopharmaceuticals for In Vivo Diagnostic Use, in vivo diagnostic agents are a class of radiopharmaceuticals administered internally to obtain images or functional parameters of target organs or pathological tissues for disease diagnosis; they can be used for health screening, disease diagnosis, assessment of organ structure/function, and patient management. According to the Technical Guidelines for Clinical Evaluation of Radiopharmaceuticals for In Vivo Therapeutic Use, in vivo therapeutic agents are a class of drugs that selectively deliver radionuclides with cytotoxic levels of radiation to pathological sites, leveraging the decay characteristics of the radionuclides to emit rays or particles that exert a cytotoxic effect on diseased cells, thereby achieving therapeutic objectives.

Classification of Radiopharmaceuticals (Image source: Zhonglun Vision)

Compared with other drugs, radiopharmaceuticals have multiple advantages. First,Visualization, it can accurately visualize the location of tumors, intuitively display whether plaques are present in the brains of patients with Alzheimer’s disease (AD), as well as the location and density of such plaques, and delineate the extent of myocardial ischemia in the diagnosis of heart disease; secondly,Quantifiable, enabling the calculation of absorbed dose after administration, assisting physicians in adjusting dosages to ensure therapeutic efficacy while minimizing adverse reactions; thirdly,Better Drug Resistance Performance, radiopharmaceuticals rely on direct internal irradiation from radionuclides, thereby reducing the likelihood of radioresistance in tumor cells. Despite concerns regarding “nuclear radiation,” these unique advantages establish radiopharmaceuticals as an indispensable component of precision medicine.

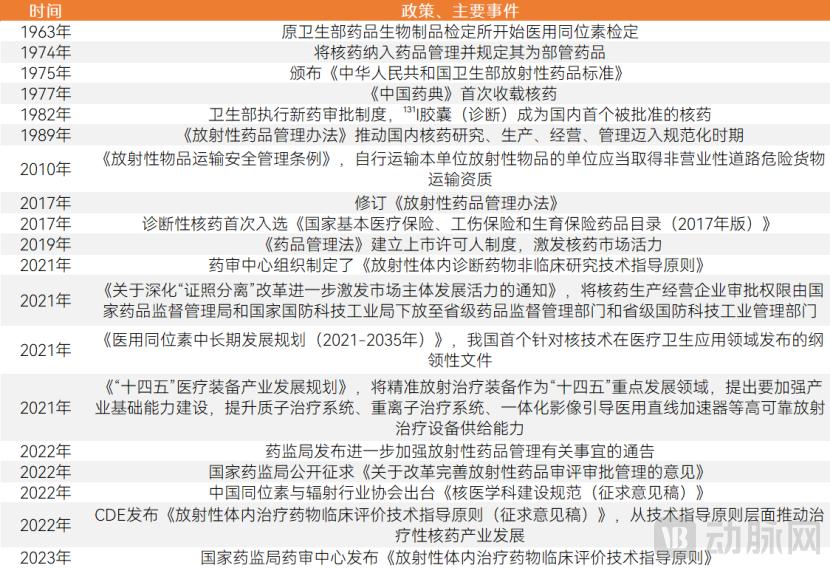

Overall Positive Policy Landscape, Yet a Gap Persists Between Regulation and Reality

China's Policies on Nuclear Pharmaceuticals

On the R&D front, policies are shifting from diagnostic radiopharmaceuticals to therapeutic ones.To meet the rapidly growing demand for clinical trials of therapeutic radiopharmaceuticals, further streamline the clinical development pathway for these agents.On the raw material front, policies are focused on addressing the challenges in the production and supply of medical isotopes.It is pointed out that by 2025, breakthroughs will be achieved in a number of key core technologies for the development of medical isotopes; the construction of one to two dedicated production reactors for medical isotopes will be initiated at an appropriate time to ensure stable and independent supply of commonly used medical isotopes. By 2035, active efforts will be made to promote the global expansion of China’s medical isotope industry.

Domestic regulatory policies for radiopharmaceuticals need to be more scientific, and there are still many ambiguities in the registration process.The regulatory landscape for radiopharmaceuticals is complex, posing certain obstacles to their clinical development. For instance, the approval process for adding new items and increasing capacity in nuclear medicine departments during clinical trials is protracted. Additionally, policy requirements mandate that usage plans for medical radioisotopes for the following year be finalized at the end of each year, and any mid-year adjustments to these plans involve a lengthy administrative procedure. Furthermore, compared with overseas markets, domestic regulation of radiopharmaceuticals in China exhibits certain uncertainties. For example, radioimmunoassay reagents are classified as radiopharmaceuticals in China, whereas they are not so classified in some European and American countries; iodine [125In China, interventional therapeutic agents such as sealed seed sources and microspheres are regulated as drugs, whereas in the United States, they are classified as medical devices. The requirements and standards for Investigational New Drug (IND) applications involving radionuclide raw materials, such as gallium, are not aligned with those of the U.S. Food and Drug Administration (FDA). The unique characteristics of radiopharmaceuticals also preclude their regulation from fully adhering to traditional pharmaceutical regulations. These discrepancies have caused considerable regulatory confusion for many enterprises.

A Ray of Sunshine in a Sluggish Market: Nearly 900 Million in Financing in 2022

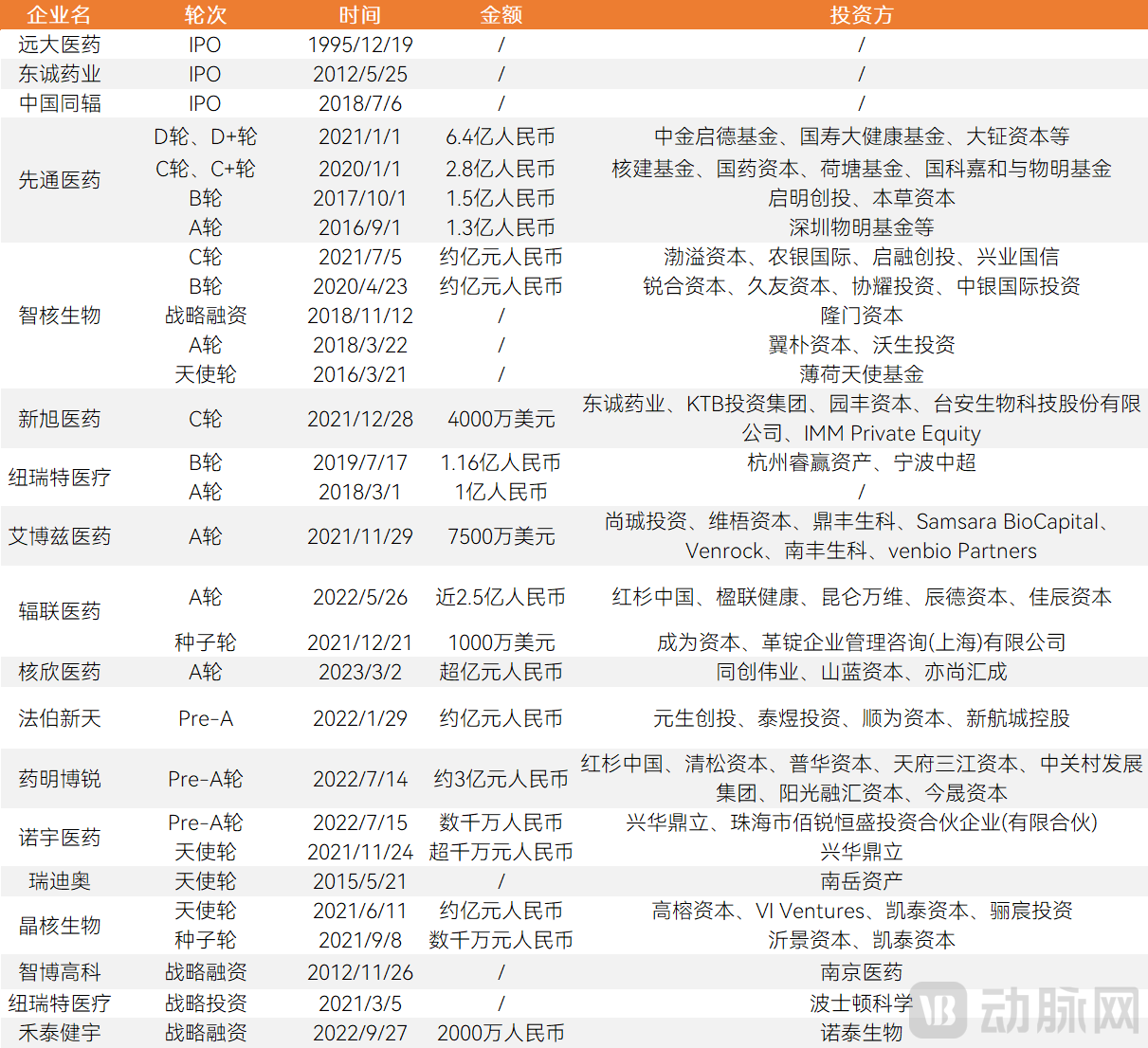

In China’s radiopharmaceutical sector, nearly 70 investment firms have made strategic investments, completing a total of 29 financing rounds with an aggregate amount exceeding RMB 3.354 billion. Industry enthusiasm surged in 2022, with annual financing reaching nearly RMB 900 million. Three companies—Grand Pharma, Dongcheng Pharmaceutical, and China Isotope & Radiation Corporation—have already completed initial public offerings (IPOs), while numerous startups have secured substantial investments from prominent institutional investors. Both large enterprises and startups are demonstrating robust growth momentum.

Detailed Overview of Investment and Financing in China's Nuclear Medicine Enterprises

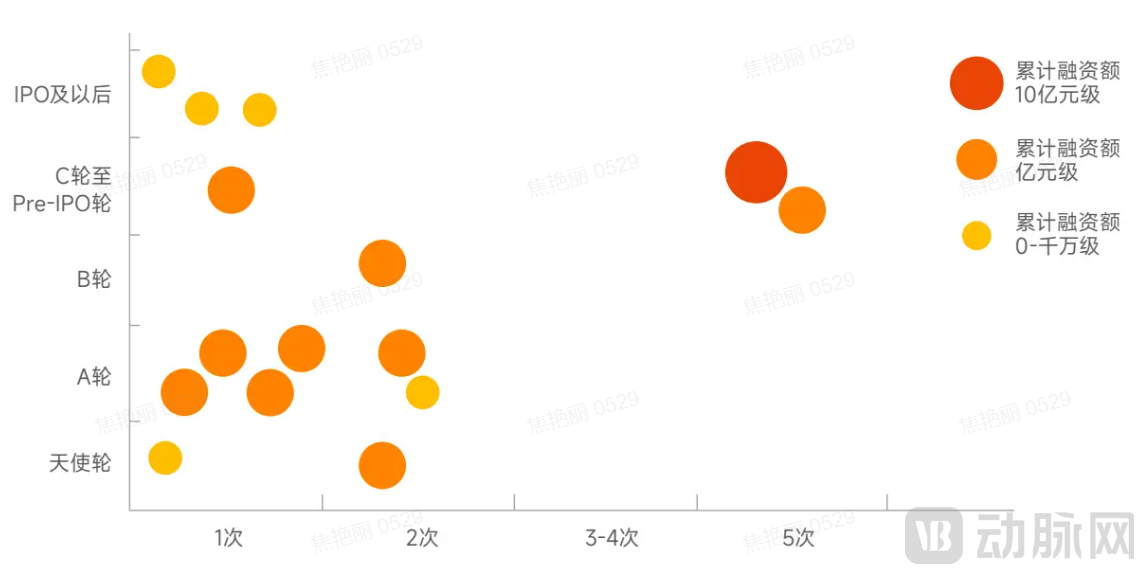

Frequent large-scale financing deals exceeding RMB 100 million: Nuclear medicine was the subsector with the highest proportion of such financing events in the innovative drug field in 2022.In terms of investment rounds and frequency, companies at the Series A stage are the most numerous, accounting for 31%. Eight companies have secured cumulative financing exceeding RMB 100 million, representing a significant 50% share. Among them, Xiantong Medicine has completed its Series D+ round, with cumulative financing surpassing RMB 1 billion. Furthermore,It is common for single financing rounds in the early stages to exceed 100 million yuan.In recent years, the innovative drug sector has exercised caution regarding large-scale investments. As the capital market cooled in the second half of 2022, nuclear medicine emerged as the sub-sector with the highest proportion of financing deals exceeding RMB 100 million that year. This demonstrates the strong capital attraction and significant investment potential of China’s nuclear medicine market, which is still in its early stages of development.

Distribution of Investment Rounds and Frequency for Chinese Nuclear Medicine Companies

Therapeutic radiopharmaceutical companies, as well as those with differentiated innovation capabilities across the upstream and downstream segments of the industry, are currently more favored.In terms of investment direction, innovative therapeutic radiopharmaceuticals, RDCs (Radiopharmaceutical Drug Conjugates), and oncology are sectors favored by investment institutions. Companies capable of addressing key challenges across the upstream and downstream value chains are particularly sought after. This investment trend is expected to persist in the coming years.

The radiopharmaceutical industry chain is extensive, with each segment characterized by high levels of specialization and significant barriers to entry. The industry can be divided into three main sectors: the upstream supply of medical isotopes; the midstream research and development, manufacturing, and distribution of radiopharmaceuticals; and the downstream clinical application, where radiopharmaceuticals are used for patient diagnosis and treatment.

Strong Upstream Bargaining Power in Radiopharmaceuticals Amid Supply Shortages

(1) Common isotopes shine in diagnostics, while emerging theranostic nuclides dazzle

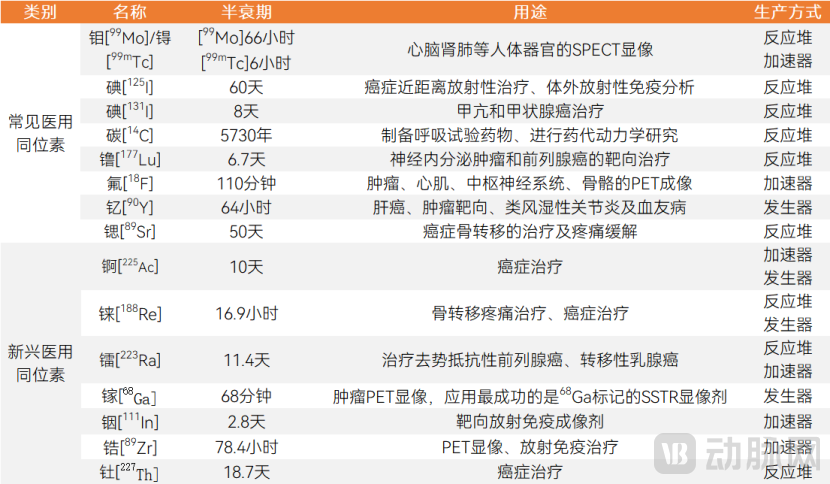

Radioisotopes applied in the medical field are referred to as medical isotopes, which serve as the foundational raw materials for the research, development, and production of radiopharmaceuticals. For many biotech companies in fields such as antibody-drug conjugates (ADCs) and antibodies, midstream R&D is the core focus; consequently, upstream enterprises providing enzymes and gene synthesis services generally command lower valuations and have less bargaining power. However, the radiopharmaceutical sector differs, as it exhibits a greater dependence on upstream supplies. Currently, more than 100 radioisotopes are used in the medical field, with over 30 medical isotopes available for disease diagnosis and treatment. Among these, eight are commonly used clinical diagnostic and therapeutic medical isotopes, namely molybdenum [99Mo]/Technetium[99ᵐTc], Iodine [125I] Iodine [131I] Carbon [14C], Lutetium [177Lu], Fluorine [18F] Yttrium [90Y], Strontium [89Sr], Actinium[225Ac], Gallium [68Emerging isotopes such as Ga are also under development, offering complementary advantages to commonly used radionuclides in SPECT/PET imaging and disease treatment.

Overview of Common and Emerging Medical Isotopes

Gallium[68Ga] is a superior diagnostic radionuclide that will largely replace fluorine[18F] Widely used in tumor imaging.Radionuclides suitable for tumor imaging include fluorine[18F] Gallium [68Ga], Indium[111In], Zirconium [89Zr] etc. Gallium [68Ga] has a half-life of 68 minutes. Its short half-life, coupled with advantages such as simple methodology, mild conditions, rapid processing, and low cost, makes it highly suitable for the requirements of diagnostic radiopharmaceuticals. Gallium[68Ga] and lutetium [177Lu] is the most popular theranostic radionuclide. In glioma, DOTA-octreotate labeled with 177Lu-DOTATATE and 68Ga-DOTATATE has been approved by the FDA for targeted radionuclide therapy and PET imaging, respectively. In 2020, 68Ga-PSMA-11 became the first FDA-approved agent for PET imaging of PSMA-positive prostate cancer.68Gallium Radiopharmaceuticals.

Comparison of Several Radionuclides Commonly Used in Tumor Imaging

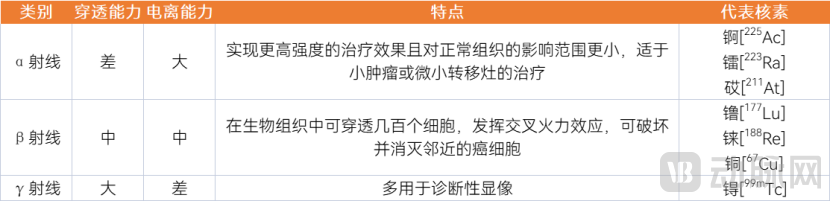

Therapeutic radionuclides are transitioning from beta-emitters to alpha-emitters, actinium[225Ac], Astatine[211At]、Thorium[227Th] Huge potential.In the field of therapeutic radiopharmaceuticals, the industry currently focuses on lutetium [177β-emitting radionuclides, represented by Lu, have garnered the most attention; however, industry focus is shifting from β-emitters to α-emitters. Compared with β-rays, α-particles possess greater mass, higher potency, and a shorter range. Targeted alpha therapy (TAT) can exert significant cytotoxic effects within a limited area around the target site, thereby delivering lower harmful radiation doses to surrounding healthy tissues and organs. This approach achieves more potent therapeutic efficacy while minimizing impact on normal tissues.

Comparison of Alpha Rays and Beta Rays

(2) Shortage of Medical Isotopes Is a Global Challenge, and China Is Reversing the Import Monopoly on Isotopes

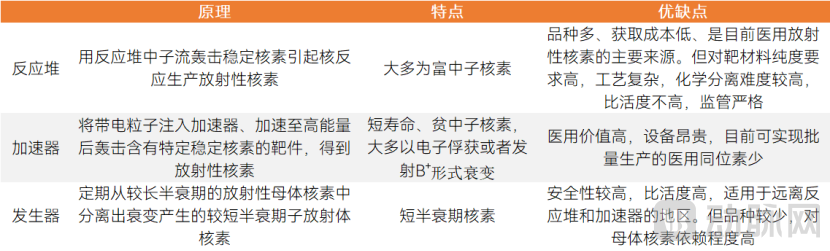

To fortify the nuclear medicine industry chain at its source, midstream R&D enterprises are accelerating their upstream layout of medical isotopes, bringing onto the agenda the reversal of China’s reliance on imported medical isotopes.Affected by factors such as time sensitivity, supply chain instability, and the impending shutdown of certain overseas reactors, there is an urgent need to break the import monopoly on medical isotopes. China will accelerate the localization of medical isotope production through measures such as developing accelerators, constructing dedicated medical isotope production reactors, incorporating medical isotope production into the annual production plans of existing reactors, and strengthening talent development. Notably, many midstream R&D enterprises are also actively engaging in upstream radionuclide supply, promoting the transition of more medical isotopes from the laboratory to industrialized, large-scale production.

Accelerators are highly efficient, convenient, and environmentally friendly, representing one of the key development trends in the production of medical isotopes.However, the majority of accelerators used in China rely on imports.There are four primary methods for producing medical isotopes: reactor irradiation, accelerator irradiation, extraction from high-level radioactive waste, and generator-based production. Reactor irradiation is currently the predominant method for producing medical isotopes; however, it involves cumbersome operations and complex processes, and nuclear reactors have not yet achieved full commercialization. In contrast, accelerators can be commercialized more readily. According to statistics from the Nuclear Medicine Branch of the Chinese Medical Association, China has a total of 120 medical cyclotrons distributed across 117 medical institutions nationwide. The primary application of medical accelerators in China is the production of fluorine [18F], and will accelerate the promotion of domestically produced compact cyclotrons, deploy medium- to high-energy cyclotrons, and ensure the supply of fluorine [18F] Stable Production, Molybdenum Preparation [99Mo], Actinium [225Ac] and other medical isotopes.

Comparison of Major Production Methods for Medical Isotopes

The large-scale commercialization of radiopharmaceuticals will compel upstream sectors to resolve radionuclide supply issues.From the perspectives of both production capacity and the technical barriers associated with accelerators, it is not advisable for midstream enterprises to invest heavily in independently establishing operations in the highly specialized upstream sector. First, the supply capacity for commonly used radionuclides is not inadequate. Luo Zhifu, current Chairman of the Isotope Branch of the Chinese Nuclear Society and a researcher at the China Institute of Atomic Energy, stated in an interview that the issue of medical isotope supply will inevitably be resolved. Taking molybdenum-99 as an example, based on a projected annual growth rate of 5%, China’s annual consumption by 2030 is expected to remain below 30,000 curies. In contrast, operating an existing reactor at full capacity could yield an annual production of 100,000 curies of molybdenum-99. Second, multiple specialized companies both domestically and internationally are already increasing their efforts in lutetium-[177Lu], Actinium [225Ac] and other radionuclides, and as more innovative radiopharmaceuticals are commercialized, upstream suppliers will inevitably be compelled to actively provide the corresponding radionuclides.

Midstream Enters High-Output Phase

The development of original, therapeutic radiopharmaceuticals in the midstream sector is a highlight. Both in China and overseas, the industry has entered a high-yield phase of radiopharmaceutical R&D and production.

(1) NMPA- and FDA-approved radiopharmaceuticals are predominantly diagnostic agents, with innovative targeted radiopharmaceuticals already having received FDA approval.

According to statistics from VCBeat, a total of 140 nuclear medicine products have been approved by the NMPA, including 73 radioimmunoassay kits; meanwhile, 118 nuclear medicine products have received FDA approval, encompassing innovative therapeutic radiopharmaceuticals such as Lutathera and Pluvicto.

NMPA-approved radiopharmaceuticals are predominantly diagnostic agents, with yttrium [90Y] Microsphere Injection has been approved in China.Currently, 22 classes of diagnostic radiopharmaceuticals have been approved, mostly for imaging diagnosis, and 10 classes of therapeutic radiopharmaceuticals have been approved, including iodine [125[I] Sealed seed sources, iodine [131I] Sodium Chloride Oral Solution, Technetium [99Tc] Methylene Diphosphonate Injection, primarily indicated for tumors, thyroid diseases, etc. Overall, the market position of NMPA-approved therapeutic radiopharmaceuticals is not ideal; iodine [131I] Sodium Iodide Capsules and Iodine [131I] Sodium iodide oral solution has demonstrated strong market performance, with total sales ranging from RMB 100 to 200 million and a compound annual growth rate exceeding 30%. The domestic therapeutic radiopharmaceutical sector still requires time for further development. Driven by rising cancer incidence and enhanced corporate innovation capabilities, the radiopharmaceutical market is shifting toward therapeutic agents. More innovative therapeutic radiopharmaceuticals are expected to gain approval in the near future. According to Zhou Chao, CEO of Grand Pharma, therapeutic radiopharmaceuticals are projected to account for 60% of the global radiopharmaceutical market by 2030. Currently, Grand Pharma’s yttrium-90 [90Y] Microsphere Injection has been approved for market launch, becoming the first product in China approved for the treatment of liver metastases from colorectal cancer.

China has approved 73 radioimmunoassay kits, but non-radioactive analytical methods are the mainstream.Radioimmunoassay products are regulated as drugs in China. The National Medical Products Administration (NMPA) has approved 73 radioimmunoassay kits from companies such as the Beijing Institute of Biotechnology, Jiuding Medicine, and Union Pharmaceutical Technology Group. Radioimmunoassay is commonly used for the quantification of trace substances, including various hormones, microproteins, tumor markers, and drugs. However, due to risks of radioactive contamination and hazards, limited shelf life, and low levels of automation, it is being replaced by methodologies such as chemiluminescence.

NMPA and FDA-Approved Radionuclides for Radiopharmaceuticals

China lags behind Europe and the United States in the approval of innovative radiopharmaceuticals; the FDA has approved multiple novel therapeutic radiopharmaceuticals, advancing more rapidly in the RDC sector.In recent years, the United States has witnessed robust growth in therapeutic radiopharmaceuticals. Bayer’s Xofigo received FDA approval for market launch in 2013; Novartis’s Lutathera was approved by the FDA in 2018 for the treatment of patients with somatostatin receptor-positive (SSTR+) gastroenteropancreatic neuroendocrine tumors; and Pluvicto gained FDA approval in March 2022 for the treatment of patients with metastatic castration-resistant prostate cancer. Radiopharmaceutical drug conjugates (RDCs), represented by Lutathera and Pluvicto, have further bolstered industry confidence in radiopharmaceuticals, accelerating the market’s transition from diagnostic to therapeutic applications.

Sales of the two blockbuster drugs, Lutathera and Pluvicto, have reached hundreds of millions of dollars, with Pluvicto regarded as the next $2 billion mega-blockbuster.Lutathera was approved by the FDA in 2018 for the treatment of patients with SSTR-positive gastroenteropancreatic neuroendocrine tumors (GEP-NETs) and has since received regulatory approval in the United States, the European Union, France, Canada, and China’s Taiwan region. Lutathera’s revenue reached $167 million in 2018, grew to $441 million in 2019, and amounted to $471 million in 2022. Pluvicto targets PSMA-positive patients, who account for approximately 80% of those with metastatic castration-resistant prostate cancer (mCRPC). It significantly addresses the unmet needs of patients who derive limited benefit from PARP inhibitors, representing a substantial market opportunity. Novartis regards Pluvicto as its next blockbuster drug with annual sales exceeding $2 billion; its revenue in 2022 was $271 million.

With Lutathera and Pluvicto launching in more countries, expanding their indications, and unlocking greater commercial potential, Pluvicto’s annual production value could exceed $6 billion.Lutathera currently has a narrow indication, with a patient population of only tens of thousands in Europe and the United States, and its supply chain is insufficient to support large-scale clinical application. As the supply chain matures, indications expand, and the patient population grows, the sales of both drugs are expected to achieve further breakthroughs. Lutathera is currently undergoing Phase II clinical trials in China, while Pluvicto has submitted an Investigational New Drug (IND) application in China. Meanwhile, Novartis is exploring combination therapies involving Lutathera and other drugs, as well as applying Lutathera to conditions such as glioblastoma and breast cancer. Pluvicto is poised to become a second-line therapy for prostate cancer and is expanding into metastatic hormone-sensitive prostate cancer. Recently, Novartis announced the construction of a new production facility in Annapolis, India, dedicated to manufacturing Pluvicto. The annual production capacity is projected to reach 250,000 vials by 2024. With each vial priced at $27,000, this implies an annual output value exceeding $6 billion.

Xofigo’s sales performance has been underwhelming, prompting radiopharmaceutical companies to adopt a more cautious approach in selecting indications and strategizing their medical isotope portfolios.Xofigo, developed by Bayer, has been approved in more than 50 countries, including the United States and China, for the treatment of castration-resistant prostate cancer with symptomatic bone metastases and no known visceral metastases. However, Xofigo’s sales performance has been relatively lackluster, partly due to the supply of radium [223Ra] There are few manufacturers of radium isotopes. On the other hand, there are already many drugs available for treating this indication, placing Xofigo under significant competitive pressure. Therefore, in the development of radiopharmaceuticals, companies need to carefully consider market conditions and select indications with clear clinical value, where existing treatments have limitations, and where the advantages of radiopharmaceuticals can be fully leveraged.

Amid the surge in popularity of RDC drugs, five products involving gallium [68Ga]-labeled diagnostic radiopharmaceuticals have received FDA approval and are replacing traditional SSTR imaging and PSMA imaging.A major feature of RDC drugs is their ability to achieve integrated diagnosis and therapy, gallium [68Ga] and Lutetium [177Lu] have similar coordination chemistry properties, allowing the same compound to be labeled for both imaging and therapy. Gallium [68[68Ga]-labeled radiopharmaceuticals can be used for positron emission tomography (PET) of PSMA-positive lesions and PET imaging of neuroendocrine tumors. Their diagnostic sensitivity and specificity for neuroendocrine tumors both exceed 90%, and they have altered the diagnosis and treatment strategies for 50%–60% of patients with neuroendocrine tumors. With the successive approvals of Lutathera and Pluvicto, as well as multiple lutetium-based177Lu]-based prostate cancer drugs and neuroendocrine tumor drugs have entered clinical trials, gallium[68The popularity of Ga-labeled drugs will rise rapidly.

(2) Global radiopharmaceutical R&D is booming, lutetium [177Lu] Extremely high interest, with some degree of homogenization in targets and indications

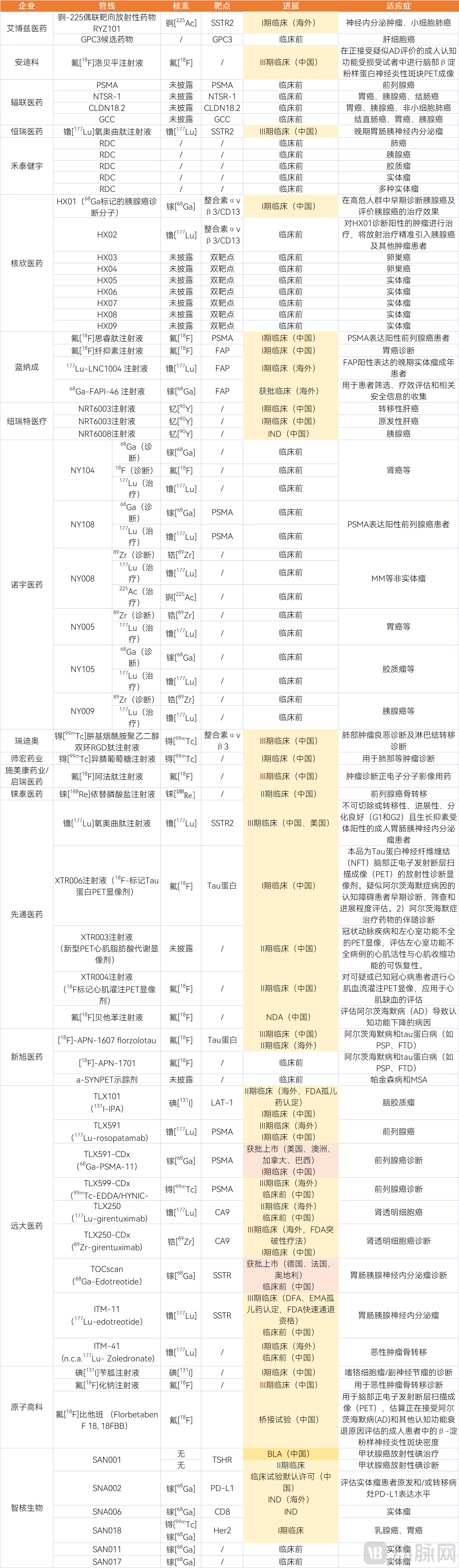

VCBeat has reviewed the disclosed pipelines of radiopharmaceuticals under development by Chinese companies, identifying a total of 74 pipelines. These include diagnostic and therapeutic radiopharmaceuticals, with a significant number being RDC (Radionuclide Drug Conjugate) pipelines. Companies such as Grand Pharma, Nuoyu Pharmaceutical, Xiantong Pharmaceutical, Fulian Pharmaceutical, and Lannacheng are among the innovative forces in the radiopharmaceutical market.

Overview of Nuclear Medicine Drugs in Development by Chinese Companies

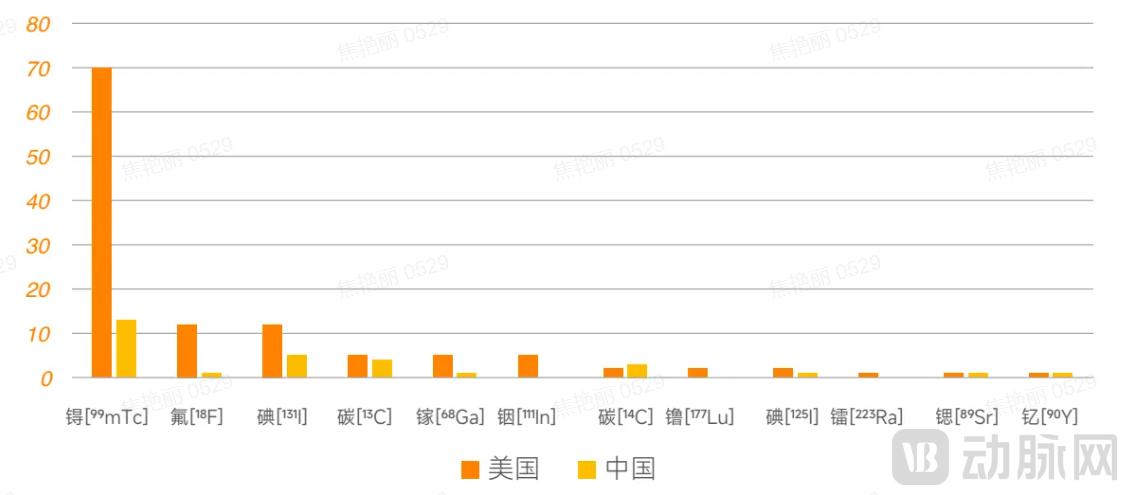

Furthermore, VCBeat conducted an inventory of overseas radiopharmaceutical pipelines in clinical stages based on ClinicalTrials.gov, identifying a total of 6,468 pipelines in clinical development. Among these, 2,482 are based on fluorine [18F], 586 items based on gallium [68Ga], 356 items based on yttrium [90Y], 220 lutetium-based177Lu], 123 items based on zirconium [89Zr], 22 items based on actinium [225Ac], 8 items based on rhenium [188Re]。

An analysis of the R&D pipelines in China and the United States reveals that radiopharmaceutical drug conjugates (RDCs) constitute a significant component.RDC, also known as Targeted Radionuclide Therapy (TRT), works by conjugating tumor-specific targeting moieties with radionuclides to achieve targeted tumor destruction. It utilizes radiolabeled targeting molecules for disease treatment, enabling precise radiotherapy of lesions within the body.

RDC is the only drug in clinical practice capable of achieving integrated diagnosis and therapy.By incorporating isotopes with short half-lives, Radiopharmaceutical Drug Conjugates (RDCs) enable rapid distribution from the bloodstream to target tissues. The radionuclides bind to primary or metastatic tumors, emitting signals within their extremely short half-lives to generate comprehensive medical imaging data via molecular imaging techniques. A key feature of this platform is its modularity: by simply swapping the radionuclide component while maintaining similar targeting moieties and linkers, integrated theranostic products can be developed, such as those conjugated with fluorine-18 [18F] Gallium [68Ga] and other components constitute diagnostic products, precisely targeting the location, conjugated with lutetium [177Lu], Actinium [225[Ac] constitute therapeutic products, reduce R&D costs, and facilitate more precise medication administration by physicians. This is currently the only field in clinical practice capable of realizing the concept of integrated diagnosis and therapy. Grand Pharma’s pipeline assets TLX591, TLX250, and ITM-11 are all accompanied by corresponding diagnostic products: TLX591CDx, TLX250CDx, and TOCscan. Similarly, SNA011 and SNA017 in Zhihe Biopharma’s pipeline are also developed with a focus on integrated diagnosis and therapy.

Radiopharmaceuticals are ushering in a second spring for peptide drugs, with targeted peptide radiopharmaceuticals representing a key direction for Radiopharmaceutical Drug Conjugates (RDCs).More than 100 peptide drugs have been approved worldwide, but the emergence of cell therapy and gene therapy has gradually overshadowed them. Peptides serve as important targeting vectors for radiopharmaceuticals, forming a natural synergy with these agents. Compared with antibodies, peptides offer unique advantages in tissue penetration and pharmacokinetic properties. Furthermore, the specific expression and conjugation capabilities of peptide molecules meet the technical breakthrough requirements for Radiopharmaceutical Drug Conjugates (RDCs). The FDA has approved several peptide-targeted radiopharmaceuticals for the diagnosis and treatment of neuroendocrine tumors with high somatostatin receptor (SSTR) expression and prostate cancer with high prostate-specific membrane antigen (PSMA) expression. Notably, Lutathera utilizes the peptide Octreotide, while Pluvicto employs a PSMA-binding motif, demonstrating the feasibility of developing RDCs based on peptide molecules.

Comparison of Several Important Targeted Molecules in RDCs

Lutetium [177Lu]-labeled drugs have become the mainstream in RDC development.Lutetium [177Lu] is a therapeutic radionuclide whose value in the treatment of prostate cancer and neuroendocrine tumors has been validated. Most pipelines remain focused on prostate cancer and neuroendocrine tumors, while a small number are exploring lutetium [177Lu]-labeled drugs in renal cell carcinoma, colorectal cancer, and other indications, as well as lutetium [177[Lutetium]-labeled drug in combination with small-molecule drugs. Accompanied by lutetium[177Lu]-labeled drug popularity, gallium[68Ga]-labeled drugs have seen a surge in R&D interest, with currently 586 gallium[68[Ga]-labeled radiopharmaceuticals are in the clinical stage, mostly as diagnostic products, compared with lutetium [177Lu] in combination to achieve integrated diagnosis and therapy. In the future, gallium [68Ga] can also be combined with actinium [225Ac] match.

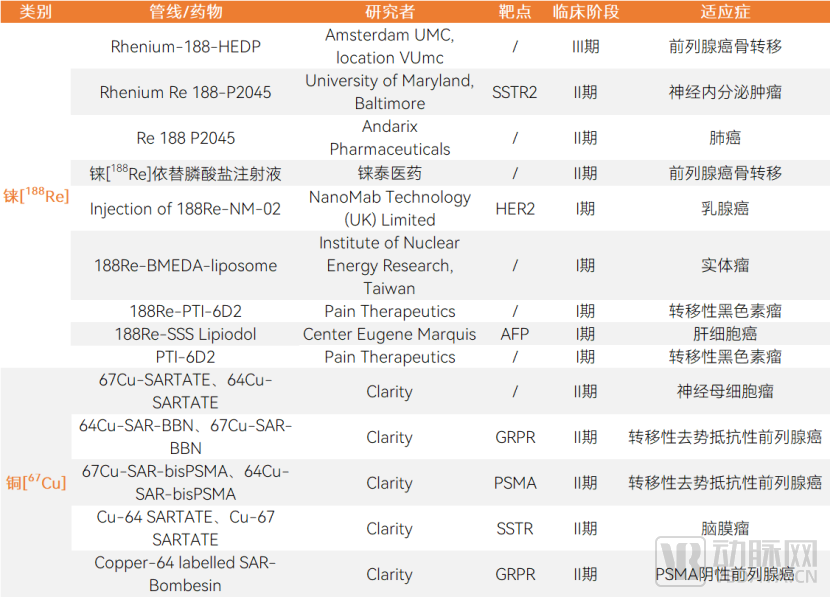

Except for Lutetium [177Lu] In addition, copper [67Cu], Rhenium [188Re] and other beta rays are also gaining increasing attention.First, copper[64Cu]/Copper[67Cu] can achieve true theranostic integration. Copper[64Cu]/Copper[67[Cu] The representative company in this niche market is Clarity. Clarity has established a presence in the copper [64Cu]/Copper[67[Cu], Focusing on Cancer Treatment, Copper [64Cu] for PET and molecular radiotherapy, copper[67[Cu] accumulates readily in cancer cells and emits beta radiation capable of killing them, making it suitable for cancer therapy. By utilizing the same metal element, true integration of diagnosis and therapy is achieved. Clarity currently has three main product lines: SARTATE for neuroblastoma, SAR-Bombesin for breast and prostate cancers, and SAR-bisPSMA for prostate cancer. In addition, rhenium-based agents currently entering clinical trials...188[Re]-labeled drugs include nine items, with indications such as melanoma, hepatocellular carcinoma, prostate cancer, and lung cancer. The most advanced overseas pipelines are those of Andarix Pharmaceuticals and the University of Maryland, Baltimore, both in Phase II clinical trials. In China, Rhenium Tai Medicine’s rhenium [188Re] Etidronate Injection has completed Phase II clinical trials.

Copper in the clinical stage [67Cu], Rhenium[188Re] Labeled Drugs

The development of radiopharmaceuticals is evolving from beta-emitting radionuclides to alpha-emitting radionuclides, with actinium [225Ac], Astatine [211At], Thorium [227Th] Huge potential.

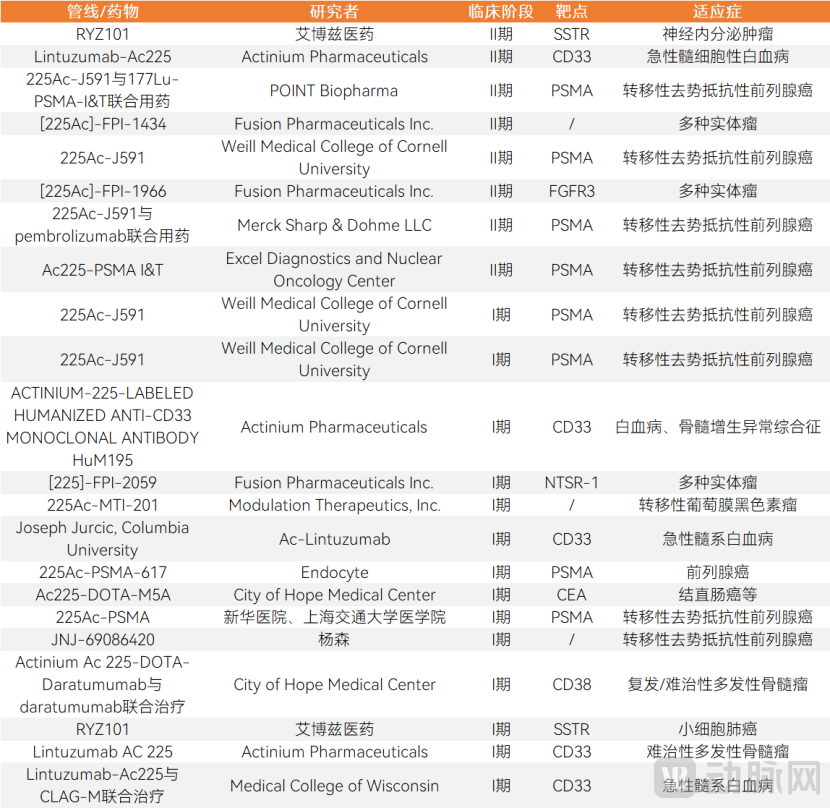

Globally, there have been 22 actinium[225[Ac]-labeled radiopharmaceuticals enter clinical trials.Actinium[225The indications for [Ac] include prostate cancer, neuroendocrine tumors, and breast cancer. Currently, Chinese companies have launched two actinium-based225Ac]’s radiopharmaceutical pipeline includes 22 actinium-based [225Ac] The radiopharmaceutical pipeline has entered clinical trials, with eight candidates in Phase II and 14 in Phase I; none have yet entered Phase III. It is reported that Aiboz Medicine’s RYZ101 is the world’s first actinium-based [225[Ac] Conjugated Targeted Radiopharmaceuticals, Aiming to Deliver the High-Efficiency Radioisotope Actinium [225Ac] delivered to tumor sites expressing SSTR2. Fusion Pharmaceuticals and Actinium Pharmaceuticals are also actinium [225Key players in [Ac]-labeled radiopharmaceuticals include Actinium Pharmaceuticals, whose Lintuzumab-Ac225 pipeline targeting CD33 for the treatment of acute myeloid leukemia is in Phase II clinical trials, and Fusion Pharmaceuticals, whose [225Ac]-FPI-1434 pipeline for various solid tumors is also in Phase II clinical trials.

Actinium Entering the Clinical Stage [225Ac] Radiopharmaceuticals

Astatine entering the clinical stage [211At] There are a total of 6 radiopharmaceuticals, with indications including hematologic malignancies, ovarian cancer, and thyroid cancer.Astatine[211[Astatine-211] has seen relatively rapid progress in the treatment of hematologic malignancies, with Fred Hutchinson Cancer Center’s pipeline candidate 211At-BC8-B10 currently in Phase II clinical trials. In 2023, Professor Weibo Cai’s team from the Departments of Radiology and Medical Physics at the University of Wisconsin–Madison, together with Professor Xiaoli Lan’s team from Union Hospital, Tongji Medical College, Huazhong University of Science and Technology, published an article in the European Journal of Nuclear Medicine and Molecular Imaging, elaborating on astatine-[211[Astatine] marks the preclinical research achievements of PSMA-targeted ligand drugs and provides valuable strategies for more extensive safety studies, demonstrating astatine's211The prospects for the clinical translation and application of astatine-labeled drugs will drive the advancement of astatine[211Application Research of At] in More Tumors.

Astatine-[211[At] Radiopharmaceuticals

Bayer is positioning itself in thorium [227Th] Major Companies in the Radiopharmaceutical Industry.Thorium [currently entering the clinical stage]227All nuclear medicine pipelines belong to Bayer. Bayer is developing a Thorium Conjugate Targeting (TTC) research platform and leveraging this platform to develop drugs for various cancers, including PSMA-positive prostate cancer, mesothelin-expressing tumors, HER2-positive tumors, and non-Hodgkin lymphoma. Among these, Bayer is exploring the combination of BAY2315497 injection with Darolutamide (BAY1841788) for the treatment of metastatic castration-resistant prostate cancer; this study is currently in Phase I clinical trials.

Thorium[ entering the clinical stage227Th] Radiopharmaceuticals

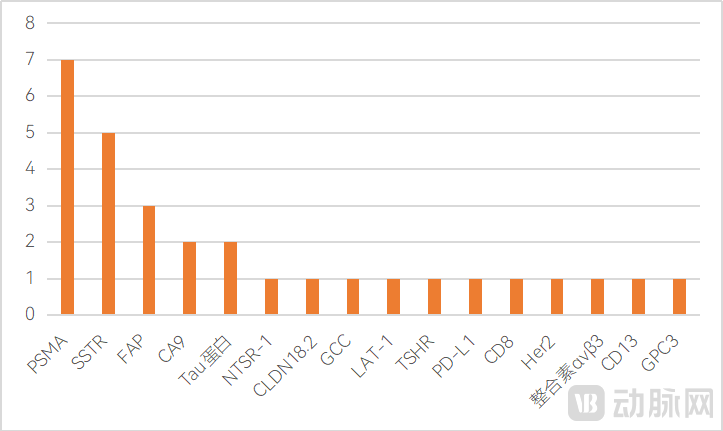

In terms of targets and indications, many domestic R&D pipelines for Radiopharmaceutical Drug Conjugates (RDCs) are developing generic or improved novel drugs benchmarked against Novartis’s two approved products. PSMA and SSTR are hot targets in radiopharmaceutical development, with numerous pipelines focused on prostate cancer and neuroendocrine tumors, where homogenization has begun to emerge.

Overview of Targets in the R&D Pipelines of Radiopharmaceuticals by Chinese Enterprises

There are few successfully validated targets in the field of radiopharmaceuticals, and FAP, which Novartis is currently developing, may be the next rising star.Fibroblast activation protein (FAP) is a type II transmembrane serine protease that is highly expressed in cancer-associated fibroblasts of various epithelial tumors, such as gastric cancer, esophageal cancer, and lung cancer, while showing no or low expression in normal tissues and benign tumor stroma, thus holding broad therapeutic prospects. Previously, Novartis entered into an assignment agreement with iTheranostics, a subsidiary of SOFIE Biosciences, acquiring global exclusive rights to develop and commercialize the therapeutic applications of an FAP-targeting agent library (including FAPI-46 and FAPI-74), thereby raising industry expectations for FAP. Currently, Lannacheng’s 177Lu-LNC1004 injection has entered Phase I clinical trials for the treatment of adult patients with FAP-positive advanced solid tumors; POINT Biopharma’s radiopharmaceutical pipeline, [Ga-68]-PNT6555 and [Lu-177]-PNT6555, is also focused on FAP.

In the future, the industry needs to identify patterns of success for radiopharmaceuticals across a broader range of tumor types and molecular subtypes.Currently, apart from local administration and the treatment of hematologic malignancies, there are only two successful cases of therapeutic radiopharmaceuticals in the field of solid tumors. Numerous R&D challenges remain to be addressed, such as determining which tumors are suitable for radiopharmaceutical therapy, assessing which molecular type—peptides, antibodies, or small molecules—holds greater potential, overcoming key issues associated with peptide-based radiopharmaceuticals like insufficient targeting moieties and renal clearance, and addressing challenges related to antibody-based agents, including their large molecular weight, slow tissue penetration, and excessively long half-life. Moving forward, the industry needs to create more successful radiopharmaceutical cases across a broader range of tumor types, molecular formats, and targets.

(3) Two leading companies dominate nuclear pharmacy resources

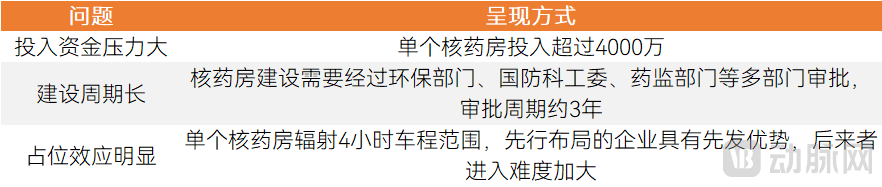

It is unlikely for emerging radiopharmaceutical companies to establish their own nuclear pharmacies; instead, a “collaborative sharing” model will be more prevalent.China’s nuclear pharmacy resources are primarily concentrated in two companies: China Isotope & Radiation Corporation (CIRC) and Dongcheng Pharmaceutical. VCBeat Research Institute assesses that, with licensing authority delegated to provincial and municipal levels, emerging enterprises tend to build their own nuclear pharmacies during the R&D phase, while most opt for collaborations with established nuclear pharmacy operators during large-scale commercialization. Establishing self-owned nuclear pharmacies imposes significant financial pressure; construction typically takes at least three years, with initial investment per facility exceeding RMB 40 million, and break-even is generally achieved at annual revenues of around RMB 10 million. Consequently, emerging radiopharmaceutical companies will likely first focus on building competitive advantages in single-product categories before partnering with nuclear pharmacy networks operated by firms such as CIRC and Dongcheng Pharmaceutical.

Barriers to Nuclear Pharmacy Construction

Future Trends

The global radiopharmaceutical market is in a phase of rapid development. VCBeat believes that future efforts should focus on innovation in radiopharmaceutical targets, indications, and radionuclides; strengthen collaboration across the upstream and downstream segments of the industry chain; promote synergy between radiopharmaceutical companies and developers of antibody-drug conjugates (ADCs) and peptide-drug conjugates (PDCs); and pay close attention to the growth of the radiopharmaceutical CRO/CDMO sector.

Competing in the Trends of Target Innovation, Indication Innovation, and Radionuclide Innovation

The prospects for combination therapy with radiopharmaceuticals are promising.Radiopharmaceuticals can be combined with various other drugs, such as synthetic lethality therapies and tumor immunotherapies, to achieve enhanced therapeutic efficacy. Several studies on radiopharmaceutical combination therapies are currently underway. The Peter MacCallum Cancer Centre in Australia is conducting a Phase I clinical trial combining the PARP inhibitor talazoparib with 177Lu-DOTA-Octreotate peptide receptor radionuclide therapy (PRRT) for the treatment of neuroendocrine tumors. OncoC4 is conducting a Phase II clinical trial combining ONC-392 with Lutetium Lu 177 Vipivotide Tetraxetan for metastatic castration-resistant prostate cancer.

Innovate in targets, molecules, indications, and radionuclides to develop first-in-class therapies.There are few successful cases of innovative radiopharmaceuticals, leaving room for latecomers. Going forward, the key factors determining whether the radiopharmaceutical market can expand are further target validation, more innovative targeting molecules, and broader indications. For instance, regarding targets, many clinically validated targets—such as EGFR, HER2, PD-L1, ALK, KRAS, BRAF, ROS1, and NTRK—have not yet been successfully applied in radiopharmaceuticals, presenting a window of opportunity for strategic layout. Beyond SSTR and PSMA, companies are already focusing on expanding into additional targets and indications. For example, Novartis has partnered with Bicycle Therapeutics to develop radioligand conjugates based on bicyclic peptides; Nuoyu Pharma has completed target screening and clinical development strategy validation for dozens of targets across major disease areas including pancreatic cancer, renal cancer, gastric cancer, prostate cancer, and Parkinson’s disease; Bayer’s pipeline of RDCs targets Her2, CD20, CD22, and MSLN; Zhihe Bio is targeting PD-L1 and Her2, with a focus on breast cancer, gastric cancer, and thyroid cancer; Ipsen is targeting NTSR-1, with its pipeline currently in Phase I clinical trials. In terms of molecular innovation, both peptides and antibodies have their respective advantages and disadvantages, necessitating the discovery of more breakthrough molecules; regarding radionuclide innovation, actinium [225Ac], Astatine [211At], Rhenium [188Re] Gallium [68Ga] is an innovative radionuclide worthy of anticipation.

The Rapid Rise of Nuclear Medicine CRO/CDMO

There are approximately 30 innovative radiopharmaceutical companies in China, corresponding to a substantial market for radiopharmaceutical CROs/CDMOs. The domestic radiopharmaceutical CRO/CDMO sector is currently in its nascent stage. Over the next three years, as more companies enter the field and a large number of drug candidates advance into clinical trials, the radiopharmaceutical CRO/CDMO industry is poised to reach a peak in development.

(Note: All data and information in this article are current as of April 15, 2023.)

Special Thanks: Yang Nan, Vice President of Investment at Xinxi Capital; Fulian Medicine; and Yan Chenglong, Co-founder and General Manager of Nuoyu Medicine.

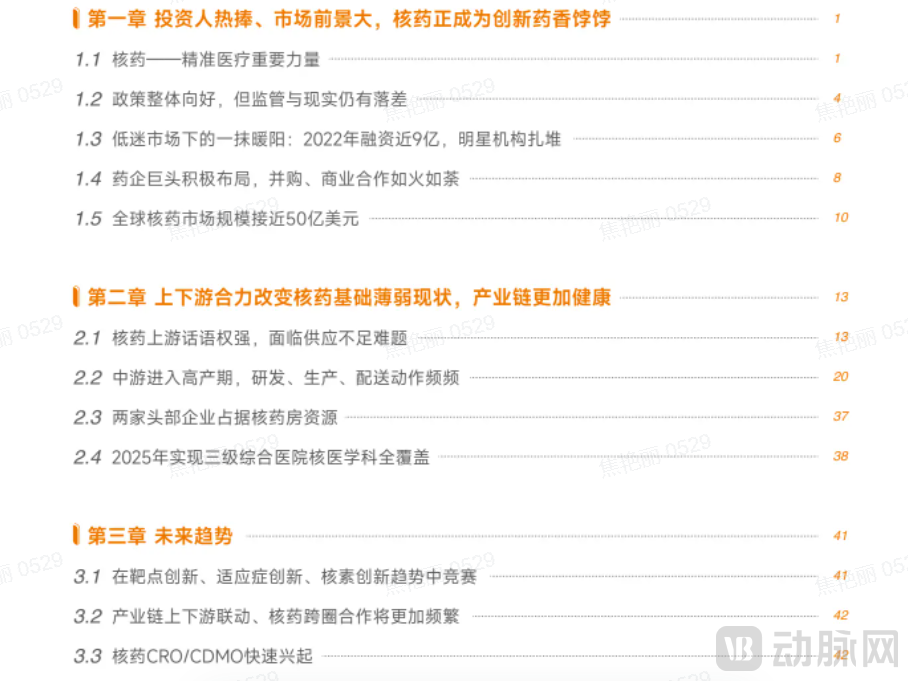

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Please scan the QR code to add our assistant and access the full report. After adding, please initiate your inquiry.

References:

Peptide Research Society: The Development of Global Nuclear Medicine — The Rise of RDC Drugs!

Medium- and Long-Term Development Plan for Medical Isotopes (2021–2035)

Zhong Lun Vision: Decoding Nuclear Medicine—An Overview of Regulatory Frameworks for the Radiopharmaceutical Industry and Key Investment Compliance Considerations

Brief Report on the 2020 National Survey of Nuclear Medicine by the Chinese Society of Nuclear Medicine