MRD Testing Industry Report: Nearly 20 Products Launched in Three Years, Clinical Battle Between Two Dominant Technologies Set to Begin

In recent years, next-generation sequencing (NGS) has emerged as a leading technology. As NGS technology has matured, gained visibility among clinical experts, and achieved broader acceptance, numerous NGS-based minimal residual disease (MRD) detection products have entered the stage of clinical application research. From hematologic malignancies to solid tumors, and from single-cancer types to pan-cancer approaches, MRD testing has gained significant momentum in recent years. This trend is reflected in the accelerating frequency of industry guidelines and consensus statements, increased industrial collaborations, and the continuous advancement of numerous prospective studies.

However, both domestically and internationally, the technical pathways for NGS-based MRD detection remain inconsistent. Unlike the previous two years, when various companies were promoting novel methodologies, the current focus has shifted toward leveraging well-established methods to demonstrate clinical value and validate clinical effectiveness. The battle for clinical adoption is imminent. Meanwhile, the pilot program for Laboratory Developed Tests (LDTs) within hospitals has been officially implemented. What opportunities and challenges will this model present to enterprises, and what will be its future trajectory?

This article focuses on the technological advancements in the NGS-based MRD detection industry. Through surveys of 12 companies and interviews with nearly 18 experts, it analyzes the development and commercialization of MRD detection technologies, leading to the following conclusions:

Interventional studies related to MRD testing are ongoing and may change clinical guidelines and the treatment landscape.Currently, as a crucial tool for evaluating perioperative treatment outcomes and monitoring recurrence, the clinical significance of minimal residual disease (MRD) detection in guiding adjuvant therapy is being continuously validated. However, the key to addressing clinical challenges lies in moving beyond merely “proving efficacy” to determining “how to intervene.” For instance, clinicians are beginning to explore interventional studies using MRD as a biomarker to guide clinical decision-making, such as how to adjust treatment regimens based on MRD results—including whether to add or switch medications and how to schedule dosing.

Currently, multiple interventional studies related to MRD detection are underway, such as CIRCULATE-US, COBRA, CIRCULATE-Japan, and DYNAMIC-III. These studies may reshape existing clinical guidelines and the treatment landscape.

Combined detection of mutations, methylation, and other markers represents a future direction for development, while integrated interpretation remains a challenge.Undoubtedly, mutation detection is currently the mainstream approach; however, single-modality testing may lack comprehensiveness. Methylation signals are relatively concentrated, providing robust signal clusters for detection, and demonstrate higher sensitivity and specificity in low-frequency circulating tumor DNA (ctDNA). This represents a novel hallmark emphasized in the 2022 special issue on “Hallmarks of Cancer.”

Combined detection of mutations and methylation may improve assay performance and represents a primary focus of technological innovation both domestically and internationally; however, further foundational biological research is required to advance the interpretation of combined detection results.

LDT projects launched in pilot hospitals will enjoy a first-mover advantage, but the LDT pilot program is not the end goal.Under the siphon effect, LDT pilot hospitals and their partner companies during this phase are likely to be concentrated among industry leaders. LDT projects capable of collaborating with these pilot hospitals will gain a first-mover advantage, yielding benefits for enterprises in terms of both data assets and brand influence.

In the long term, once LDT policies mature, inclusion in the LDT catalog or project initiation will become a prerequisite for new projects. However, the LDT pilot program is not the end goal; an exit mechanism driven by clinical needs and IVD standards will compel companies to prioritize R&D and enhance product capabilities. Under this new model, the standardization of LDTs will be further strengthened.

Overview: Frequent industrial collaboration activities, with a compound annual growth rate of 66.6% in recent years

The concept of MRD has existed for over a decade. It was initially applied to hematologic malignancies, namely leukemia and other blood and lymphatic system disorders, where it was defined as Minimal Residual Disease. With the growing body of clinical data on ctDNA-based MRD in solid tumors, the concept of Molecular Residual Disease has gained broader acceptance.

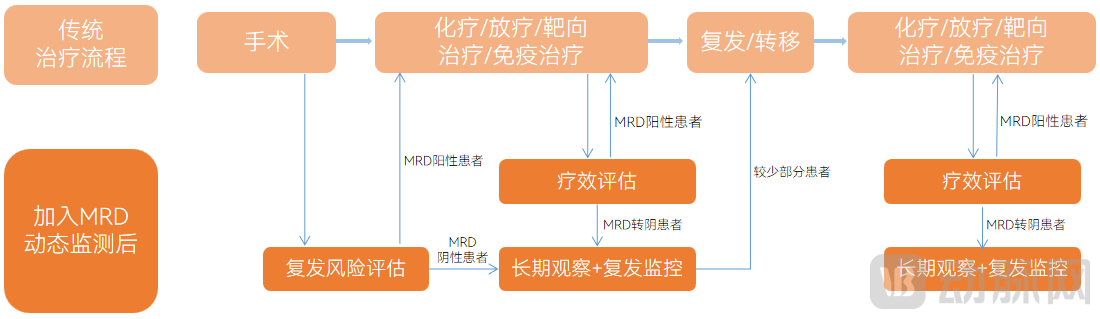

Dynamic monitoring of minimal residual disease (MRD) spans the entire process of precision oncology diagnosis and treatment. Its primary application scenarios include adjuvant treatment decision-making, prognostic assessment, postoperative recurrence monitoring, efficacy monitoring of immunotherapy, surrogate endpoints in clinical trials, surgical decision-making based on neoadjuvant therapy response, and participant screening for clinical trials. Among these, prognostic assessment, adjuvant treatment decision-making, and postoperative recurrence monitoring represent the core application scenarios of dynamic MRD monitoring, as illustrated in the figure below:

The Role of Dynamic MRD Monitoring in Precision Oncology Diagnosis and Treatment

Image Source: LeadLeo Research Institute

International studies have shown that dynamic monitoring of minimal residual disease (MRD) can identify the risk of disease recurrence earlier than traditional CT imaging. The specific lead times vary by cancer type: approximately 10.7 months for breast cancer, 6.5 months for pancreatic cancer, 5.2 months for lung cancer, and 11.5 months for colorectal cancer.

Driven by the continuous maturation of the companion diagnostics industry, the application of precision medicine has expanded. From early screening to minimal residual disease (MRD) detection and companion diagnostics, precision oncology diagnostics now cover the entire care continuum. Unlike companion diagnostics, MRD detection and early screening impose different requirements on testing.

higher. Meanwhile, they differ in terms of target populations, treatment stages, objectives, and technical requirements, as detailed below:

Differences Among Companion Diagnostics, MRD Testing, and Early Screening

Image source: VCBeat.

MRD testing is relatively mature in hematologic malignancies and is emerging as a promising field in solid tumors. In the realm of hematologic malignancies, Adaptive Biotechnologies’ clonoSEQ received FDA approval in September 2018 for MRD detection in patients with acute lymphoblastic leukemia (ALL) or multiple myeloma (MM), and was included in Medicare coverage in January 2019.

In China, in April 2021, the Center for Drug Evaluation (CDE) began drafting the “Technical Guidelines for Detecting Minimal Residual Disease in Clinical Trials of Drugs for Multiple Myeloma” regarding applications in hematologic malignancies. The final version was released in November of the same year, leading to increasingly comprehensive clinical standards for MRD detection products in hematologic malignancies.

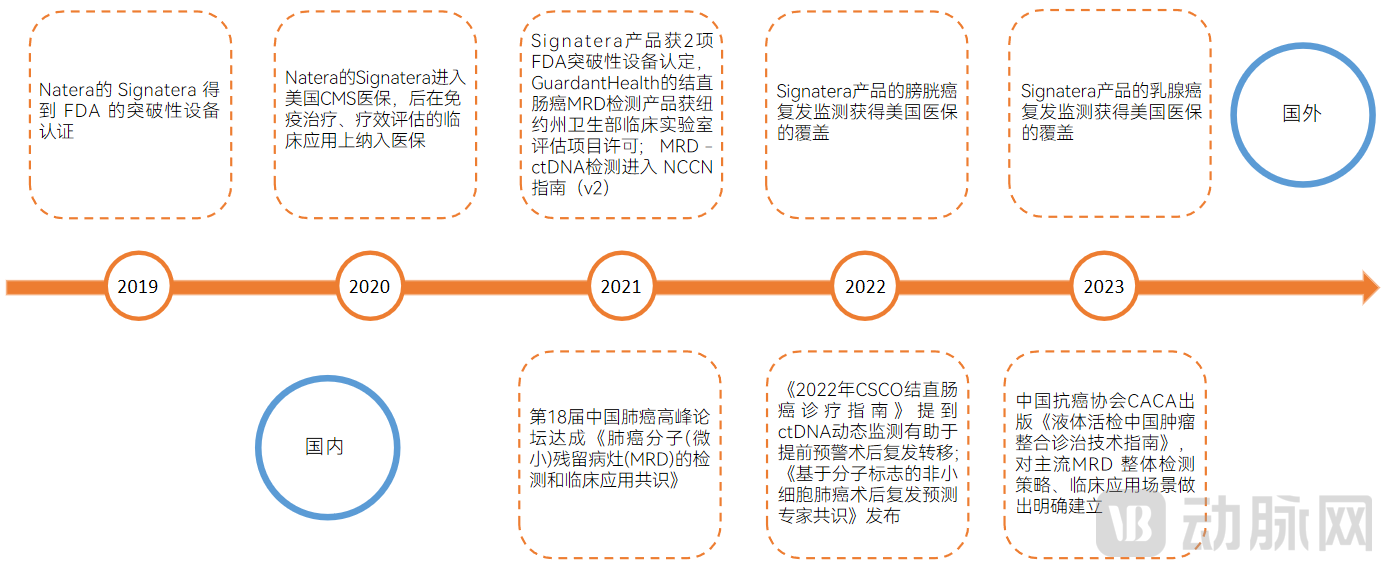

In the field of solid tumors, the exploration and application of MRD testing have primarily emerged over the past five years. It remains largely in the clinical research stage and is gaining significant momentum. The development of MRD testing for solid tumors has been driven primarily by advances in next-generation sequencing (NGS). Notable milestones include regulatory approvals abroad, represented by Natera and Guardant Health, and the establishment of guideline consensuses in China, as detailed below:

Major Events in the MRD Testing Industry for Solid Tumors in China and Abroad

Image source: VCBeat.

Overall, since 2020, the MRD testing industry has gradually gained momentum both domestically and internationally. With the publication of clinical findings, product launches, and corporate collaborations, various industrial developments across multiple dimensions have successively emerged.

Abroad, in May 2020, AstraZeneca partnered with Invitae (ArcherDX) to develop personalized lung cancer diagnostic tests; in January 2021, Grail announced collaborations with Amgen, AstraZeneca, and Bristol-Myers Squibb to evaluate early cancer detection technologies; in February of the same year, Exact Sciences, a molecular diagnostics company, announced the acquisition of the sequencing laboratory Ashion.

In China, in October 2020, Genetron Health and ImmuneOnco entered into a collaboration to accelerate the productization of MRD testing for hematologic malignancies. In November, Zhenhe Technology announced the market launch of its MRD detection product, LungBooster, marking the first commercialized MRD testing service for lung cancer in China.

In May 2021, Geneseeq published the results of China’s first multicenter prospective study on minimal residual disease (MRD) in colorectal cancer in the *Journal of Hematology & Oncology*. In June, Natera entered into an exclusive partnership with BGI Genomics to introduce Signatera to China.

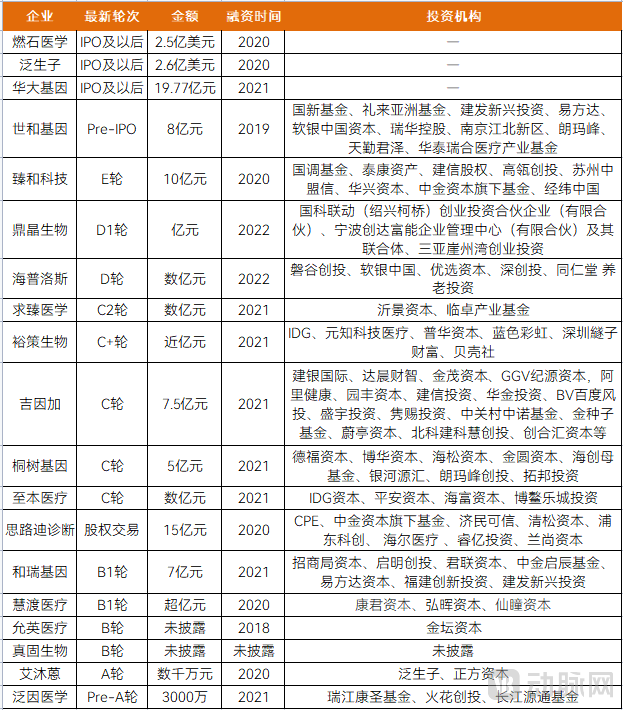

The MRD testing industry in China began to heat up in the second half of 2020. Unlike companion diagnostics, MRD testing demands higher technical capabilities and presents greater entry barriers, resulting in a pronounced head effect. Currently, three companies have gone public; most firms are concentrated at Series C and later stages, with few at Series A or earlier. Those early-stage investments are primarily strategic moves by leading players to expand their product portfolios and build competitive advantages.

Prospective studies of MRD detection products impose stricter requirements on patient screening and management. Unlike early screening, MRD testing requires enrolled participants to be patients with confirmed diagnoses for prognostic monitoring, resulting in a target population that is significantly smaller than that of early screening.

On the other hand, unlike early screening and companion diagnostics, MRD testing products have a long usage cycle (generally two and a half years), which means that large-scale prospective studies also require a longer duration. Consequently, long-term patient management and long-term sample management become challenging.

Meanwhile, leading domestic players have all established a presence in the field of solid tumors, with most covering pan-cancer indications. Although the competitive landscape is not yet crowded, the mainstream technical approaches are Tumor-agnostic and Tumor-informed, mirroring international trends, where innovation directions remain relatively narrow. With each company boasting strong competitive capabilities, the clinical competition is poised to intensify.

On the other hand, we observe that innovative enterprises such as ImmuOnco and FanYin Medicine continue to secure financing. These companies are technological leaders and have strategically differentiated themselves by focusing on hematologic malignancies.

Overall, under the high barriers to entry, financing in the MRD detection sector has not been particularly intensive in recent years. The requirements for innovative enterprises are stringent, while leading players possess substantial strength, with technological advancements largely keeping pace with international standards. Although the market size is smaller than that of early cancer screening, there are fewer participants, and the clinical need is more imperative. Clinical guidelines and consensus statements have been released at a faster rate, accompanied by more urgent calls from the clinical community, creating promising opportunities for development both domestically and internationally. Specifically, the financing landscape in recent years is as follows:

A Review of Financing in the MRD Testing Industry

Image source: VCBeat.

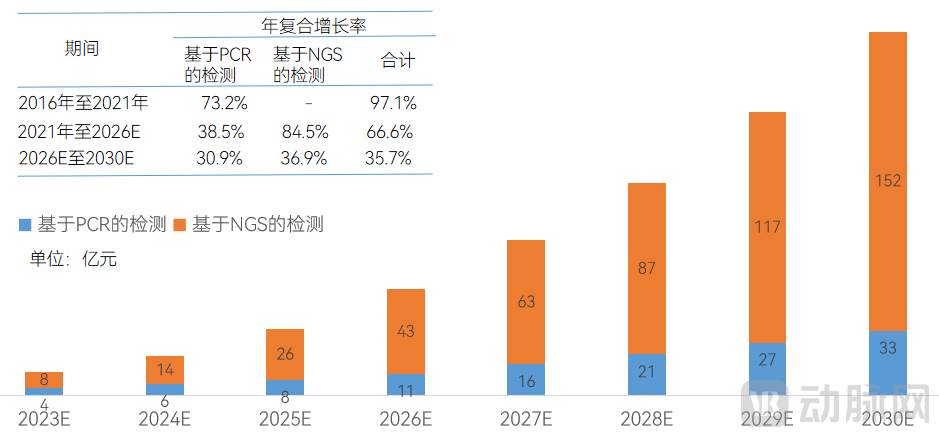

China’s cancer prognosis and monitoring market is poised for accelerated growth. According to Frost & Sullivan, the market size in China increased from RMB 14.3 million in 2016 to RMB 400 million in 2021, representing a compound annual growth rate (CAGR) of 97.1%. It is projected to reach RMB 5.4 billion by 2026, with a CAGR of 66.6% from 2021 to 2026, and further expand to RMB 18.5 billion by 2030, reflecting a CAGR of 35.7% from 2026 to 2030. The specific market sizes are as follows:

Market Size of the MRD Testing Industry Based on PCR and NGS

Source: Frost & Sullivan; prepared by VCBeat.

Technology: Non-uniform pathways, entering clinical validation phase

Globally, technical approaches under next-generation sequencing (NGS) are not standardized. Unlike the previous two years, when companies were promoting new methodologies, the current focus is largely on leveraging well-established, stable methods to deliver value in clinical settings and validate clinical effectiveness. The battle for clinical adoption is imminent.

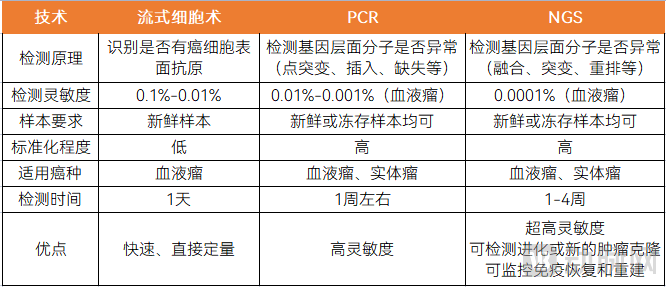

Currently, the primary technologies for minimal residual disease (MRD) detection are flow cytometry, polymerase chain reaction (PCR), and next-generation sequencing (NGS). Among these, flow cytometry is mainly used for hematologic malignancies, while PCR and NGS are primarily applied to both solid tumors and hematologic malignancies. The management of hematologic malignancies is more mature; over the past two decades, flow cytometry has been the predominant clinical technique for MRD detection.

In recent years, with the application of minimal residual disease (MRD) detection in solid tumors, PCR and NGS, particularly NGS, have been increasingly utilized for MRD testing. The table below outlines the differences among flow cytometry, PCR, and NGS in terms of detection principles, sensitivity, sample requirements, and other aspects.

Differences Between Flow Cytometry, PCR, and NGS

Image source: VCBeat.

The technical difficulty of MRD detection varies across different cancer types in solid tumors, primarily due to differences in the amount of ctDNA released into the bloodstream. The detection of solid tumors is more challenging than that of hematologic malignancies, mainly because solid tumor cells and hematologic malignant cells release different amounts of detectable ctDNA into the blood, with hematologic malignancies releasing significantly higher levels of ctDNA compared to solid tumors.

Similarly, mutation sites vary across different cancer types, lesion sizes differ, and the corresponding levels of ctDNA released into the bloodstream also vary, indicating that the technical difficulty of MRD detection differs among various cancer types.

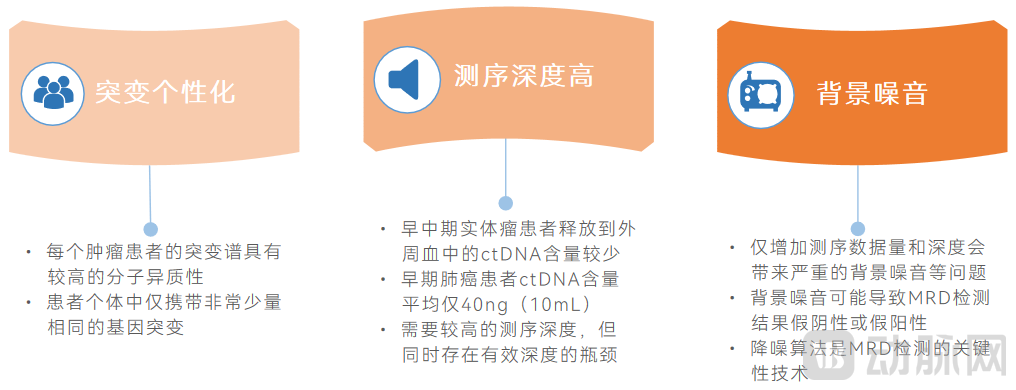

The technical challenges of MRD testing are mainly reflected in mutation personalization, sequencing depth, and background noise.

Technical Challenges in MRD Detection

Image source: VCBeat

Furthermore, postoperative recurrence rates vary across different cancer types; notably, lung cancer exhibits a relatively high postoperative recurrence rate, as detailed in the table below:

Postoperative Recurrence Rates of the Five Most Common Cancers

Image source: VCBeat.

Compared to single-cancer MRD testing, pan-cancer testing offers greater universality. In the field of solid tumor MRD detection, pan-cancer assays demonstrate broader applicability. On one hand, even within the same anatomical site, differences in cytological morphology lead to variations in relevant mutation sites; for example, lung adenocarcinoma differs from lung squamous cell carcinoma.

On the other hand, the tumor itself may undergo distant metastasis or experience certain transformations after developing drug resistance, potentially leading to new lesions and inducing mutations at new sites.

There are also differences in the choice of technological approaches among foreign companies. In the international market, products from Natera, Neogenomics, Invitae, and Exact Sciences are based on the tumor-informed approach, while Guardant Health and Grail have adopted the tumor-agnostic approach, reflecting divergent technological strategies.

Domestic companies are primarily focused on solid tumors, with varying technological approaches. We have compiled statistics on the solid tumor MRD products released by some domestic companies. According to incomplete statistics, as of April 2023, a total of 19 solid tumor MRD testing products had been launched in China. We categorized them based on the two mainstream technical pathways: Tumor-informed and Tumor-agnostic strategies, as detailed in the table below:

Overview of MRD Detection Products for Solid Tumors Released by Domestic Companies

Image source: VCBeat.

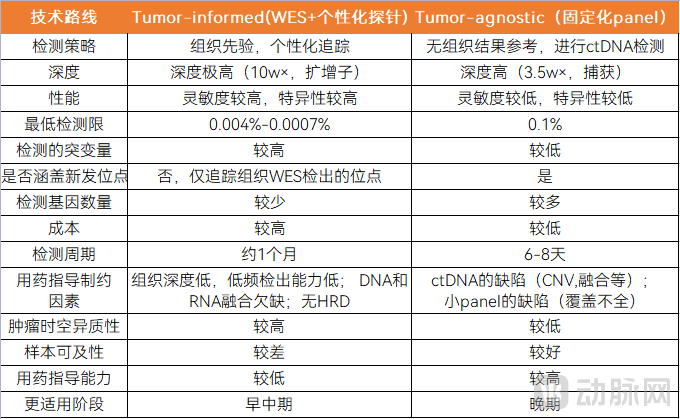

Mainstream: Tumor-informed and tumor-agnostic approaches each have their unique characteristics

Tumor-Informed Assays require testing of tumor tissue using whole-exome sequencing (WES) combined with a personalized panel. The tumor-informed strategy first involves performing high-throughput sequencing (primarily WES) on the patient’s tumor tissue to identify tumor-specific mutations. A customized personalized panel is then designed by selecting a defined number of high-abundance trunk mutations (typically comprising only 16–50 tumor-specific mutations). Finally, these mutations are detected in the patient’s plasma circulating tumor DNA (ctDNA), effectively constituting a WES plus personalized panel approach.

Tumor-informed analysis strategies, by targeting a limited number of mutation sites, significantly reduce the risk of false positives arising from technical and biological backgrounds (such as clonal hematopoiesis). This approach also enables ultra-deep sequencing, thereby enhancing detection sensitivity. Representative products include Signatera.

Tumor-Agnostic Assays: Tumor-agnostic assays do not require the acquisition of tumor tissue for fixed-panel testing. The tumor-agnostic strategy primarily employs a universal, large-scale panel covering three to four hundred genes or more, which is equivalent to fixed-panel testing.

By employing a fixed mutation panel, there is no need to obtain patient tumor tissue for sequencing in advance, which can significantly simplify the workflow, reduce costs, and shorten the turnaround time for assessing patients’ MRD status.

In the decision-making process for adjuvant therapy, delays in initiating treatment may compromise therapeutic efficacy; therefore, rapid assessment of a patient’s minimal residual disease (MRD) status to facilitate timely clinical decisions is also crucial. A representative product is the Guardant Reveal MRD test, which employs a fixed panel to detect ctDNA methylation and genomic mutations. The table below outlines the differences between tumor-agnostic and tumor-informed strategies, including detection approach, sequencing depth, and performance characteristics.

The Difference Between Tumor-Informed and Tumor-Agnostic

Image source: VCBeat

In terms of approval and regulation, tumor-agnostic assays may be relatively easier to manage. Compared to the highly variable nature of personalized panels, fixed panels offer a higher degree of standardization. For instance, the literature cited in the NCCN Guidelines for colon cancer is primarily based on tumor-informed approaches. Furthermore, personalized panels present certain regulatory challenges; ultimately, what may be approved is not a fixed product but rather a standardized process, which will require consensus with regulatory authorities.

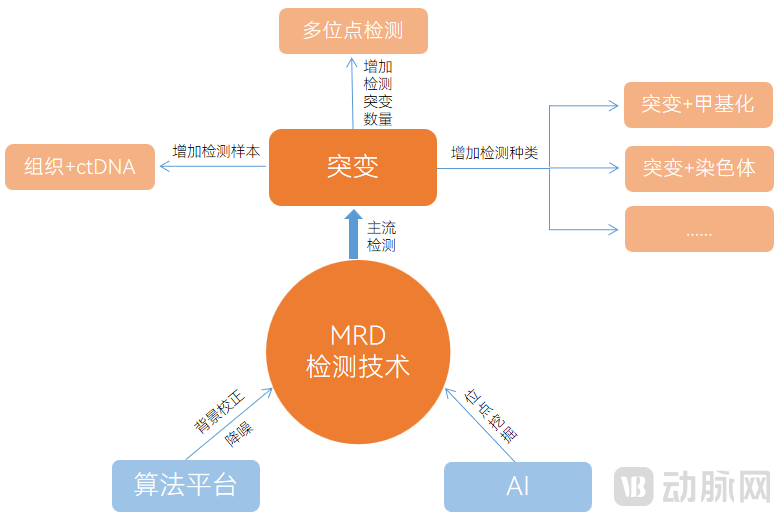

In addition to the two mainstream technical approaches, tumor-agnostic and tumor-informed, there are other innovative solutions for MRD detection. These innovative solutions primarily enhance the sensitivity of single tests by detecting a broader range of biomarkers, mainly through increasing the number and diversity of biomarkers.

We observe that the directions of exploration include multi-mutation detection to increase the number of detected mutations, combined multi-omics detection of mutations and methylation to expand the types of detection, and combined detection of mutations and chromosomal abnormalities. Meanwhile, in terms of algorithm platforms and AI applications, there are initiatives to develop specialized algorithm platforms and AI-enabled solutions for mining mutation sites.

Multi-mutation site detection, which increases the number of detected mutations, can enhance sensitivity. For the tumor-informed assay approach, companies both in China and abroad are developing their own solutions. For instance, the classic Signatera test uses only 16 loci, but some companies are now expanding locus selection to improve sensitivity by increasing the number of detected mutations. In addition to whole-exome sequencing (WES), whole-genome sequencing (WGS) is also being employed for tissue mutation detection to further enhance sensitivity.

Expanding the range of detectable targets through combined mutation and methylation testing can enhance product performance. Compared with other biomarkers in clinical applications, DNA methylation alterations typically emerge early in tumorigenesis. Moreover, tumor tissue DNA methylation patterns generally exhibit high consistency across extensive genomic regions and demonstrate specificity across different tissues and cancer types, enabling tissue-of-origin identification for cancers of unknown primary site. Tumor-specific ctDNA methylation assays hold potential value in detecting minimal residual disease (MRD) following surgery or other curative treatments.

Detection of chromosomal instability can effectively identify tumor metastasis. Chromosomal instability is the foundation of cellular carcinogenesis; low-to-moderate levels of CIN confer a growth advantage to tumor cells, while high levels of CIN are associated with tumor metastasis. The MSK-MET study, involving over 25,000 samples across 50 cancer types, has confirmed the relationship between chromosomal instability and tumor metastatic burden. Therefore, incorporating chromosomal instability serves as a valuable supplement for assessing tumor recurrence and metastasis, providing better decision-making support for clinical treatment.

Co-detection Strategy for Tumor Tissue and ctDNA. This strategy simultaneously performs whole-exome sequencing on tumor tissue samples and deep targeted sequencing using a fixed panel on patient plasma ctDNA. By integrating data from both sample types, bioinformatics algorithms are employed to determine MRD status. The fixed panels used in such technologies typically focus on hotspot mutations, which simplifies the workflow to some extent. However, due to inter-patient heterogeneity, some patients may not harbor any of the mutations included in the fixed panel.

In addition to expanding the variety and volume of tests, noise reduction within algorithmic platforms is also critical. For cancer types with high patient heterogeneity or lacking hotspot mutations, as well as in scenarios requiring extremely high sensitivity and specificity for earlier detection, highly sensitive, customized testing methods are needed to accommodate diverse clinical applications.

This necessitates that the algorithm achieves highly accurate mutation tracking across diverse samples, different sequencing platforms, and various panels.

For example, Zhenhe Technology’s MinerVa® platform utilizes a 769-gene panel (product: Baishibo®) that covers various mutation types, including driver mutations, clonal mutations, and passenger mutations. By employing a differentially weighted panel design, it achieves high sequencing depth (≥30,000X) in tumor hotspot regions, thereby ensuring the sensitivity of MRD detection.

AI technology can help optimize detection methods and improve cost-effectiveness. When designing fixed panels, AI technology can be used to select important loci from hundreds of thousands or more sample data, combining parameters such as occurrence frequency, tumor type, sample type, detection depth, and limit of detection to form a relatively economical, practical, and efficient panel testing solution. The selected loci can target single cancer types or pan-cancer types.

For instance, Huisuan Gene leveraged its proprietary sample database and AI technology to rapidly develop a distinctive NGS-based MRD solution applicable to pan-cancer MRD detection. Furthermore, through big data mining, novel methylation markers were identified; these markers exhibit high levels of methylation across 17 types of solid tumors, enabling pan-cancer MRD detection while effectively reducing costs.

AI technology, through model training, holds significant importance for the discovery of novel loci and new biomarkers. It meets the demand for large-panel testing in minimal residual disease (MRD) detection. In the future, as sample sizes accumulate, AI technology will play an increasingly vital role, further providing optimized solutions for MRD detection. Specifically, the technological innovation strategies for MRD detection are primarily illustrated in the figure below:

Innovative Solutions for MRD Detection Technology

Image source: VCBeat.

Commercialization: LDTs as the primary model, supplemented by partnerships with pharmaceutical companies

Currently, no MRD testing products for solid tumors have received NMPA approval in China. The prevailing business model is primarily based on Laboratory Developed Tests (LDTs), supplemented by collaborations with pharmaceutical companies. In terms of payment, few domestic MRD testing products have established partnerships with insurance providers. Overall, the MRD testing industry remains in the early stages of commercialization and has a long way to go.

Overall, LDT policies in China are becoming increasingly standardized, and currently, the in-hospital pilot programs for LDTs have entered the implementation phase.

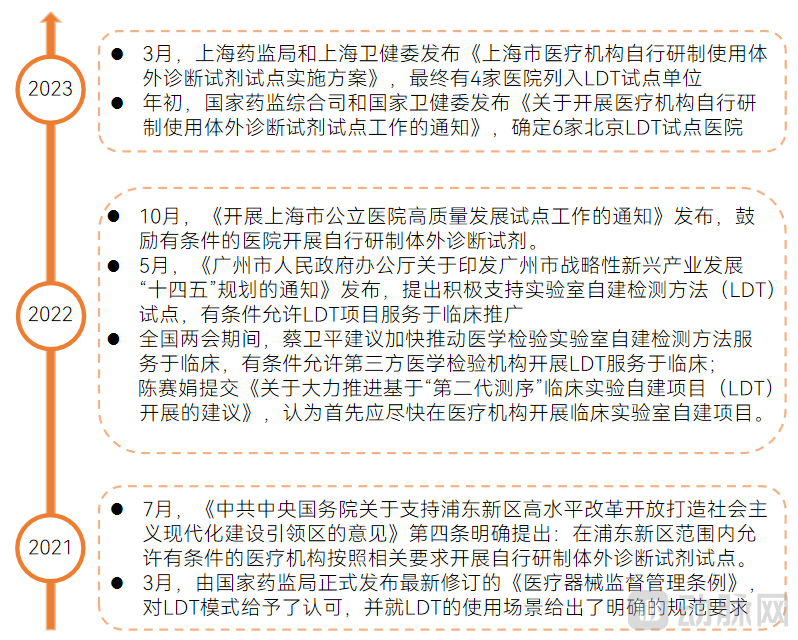

Recent LDT-Related Policies and Notices in China

Image source: Compiled from public information, produced by VCBeat.

The figure below highlights the key points of two major pilot documents on in-house Laboratory Developed Tests (LDTs) released in 2023. The policies aim to strengthen regulation and control risks, with an emphasis on qualifying credentials and clarifying rights and responsibilities, as detailed below:

Key Points of Two In-House LDT Pilot Documents

Image source: Compiled from public materials, produced by VCBeat.

Pharmaceutical companies are expanding oncology drug development from late-stage to early-stage patients. From the perspective of pharmaceutical companies, many have shifted their focus from treating late-stage cancer patients to adjuvant and neoadjuvant therapies for early-stage patients. This trend toward expansion from late-stage to early-stage patients is evident in both targeted therapy and immunotherapy.

Compared with advanced-stage disease, patients with early-stage tumors require longer follow-up periods, larger-scale studies, and greater investment in follow-up management to achieve predefined clinical endpoints after treatment. MRD testing for patients with early-stage tumors naturally aligns with pharmaceutical companies’ needs in developing drugs for early-stage cancer.

MRD testing companies and pharmaceutical companies can collaborate both before and after drug approval to accelerate new drug development. For pharmaceutical companies, MRD testing products can be used in the clinical treatment of solid tumors for patient screening and monitoring, thereby accelerating new drug development.

On the one hand, prior to drug approval, MRD testing constitutes a critical component of pharmaceutical companies’ clinical trials. It is employed for patient enrollment screening, stratification, and the exploration of biomarkers and companion diagnostic markers. Furthermore, some clinical trial results utilize MRD as the basis for patient enrollment and treatment stratification, enabling pharmaceutical companies to conduct retrospective studies by integrating MRD test results with the overall treatment regimen. On the other hand, post-approval, MRD testing can also serve as an adjunct to guide therapeutic decisions regarding medication use.

Pharmaceutical companies can provide MRD testing firms with extensive sample collections, thereby accelerating product development. The R&D of solid tumor MRD detection technologies hinges on two critical factors: technical capability and sample availability. The integration of superior technical prowess with robust sample access is central to ensuring product performance and expediting the development process.

For MRD testing companies, pharmaceutical firms possess a large volume of clinical samples tested using gold-standard assays. Through long-term follow-up, it is possible to definitively determine whether each patient associated with these samples experiences recurrence. Consequently, MRD products can be validated based on extensive sample data; the larger the sample size, the more accurate the determined threshold becomes. Ultimately, these samples serve to both accelerate product development and optimize product performance.

Meanwhile, testing companies can integrate MRD testing into clinical trials and develop companion diagnostic products, thereby achieving win-win cooperation with pharmaceutical companies.

FDA Releases Draft Industry Guidance Encouraging the Use of MRD Testing in the Development of Therapeutics for Early-Stage Solid Tumors. In June 2022, the FDA issued a draft industry guidance on the application of ctDNA in drug development for early-stage solid tumors, encouraging the use of ctDNA-based MRD testing to facilitate the development of therapeutics for early-stage solid tumors.

The draft indicates that ctDNA testing can not only screen patients with targetable mutations for inclusion in clinical trials, but also, based on ctDNA-derived MRD, is more likely to be used to enrich for patients at high risk of recurrence, assess treatment response, and even serve as an early study endpoint. MRD testing is becoming an integral part of drug development, significantly enhancing its efficiency.

NGS Automation Bridges the Last Mile to Clinical Implementation. NGS automation enables the systematic integration of wet-lab processes—including sample pre-processing, nucleic acid extraction, library preparation, hybridization capture, and high-throughput sequencing—with dry-lab workflows such as bioinformatics data analysis, medical annotation and interpretation, and report generation, along with comprehensive quality control across the entire workflow. This achieves a one-click, intelligent, and fully automated end-to-end process from sample to report, significantly enhancing the efficiency and clinical accessibility of NGS testing.

“Integrated” platform technologies are encouraged by policy. On April 8, 2022, the General Office of the Guangzhou Municipal People’s Government issued the “14th Five-Year Plan for the Development of Strategic Emerging Industries in Guangzhou,” which emphasized that, in the field of medical laboratory testing, active support should be provided for pilot programs on Laboratory Developed Tests (LDTs). The plan encourages the development of “integrated” platform technologies and the R&D of high-end integrated inspection and testing equipment, aiming to overcome key technical challenges related to instrument stability, reliability, miniaturization, and intelligence.

Meanwhile, by integrating with hospital information systems, precision diagnostics companies provide hospitals with a complete data flow covering the entire NGS workflow—including aggregated patient information, clinical data, sample information, experimental data, and quality control systems. This enables automated collection, storage, dynamic analysis, and visual presentation of full-process NGS data, as well as deeper integration of in-hospital genetic testing big data. Consequently, it establishes a real-world data-based platform for in-hospital NGS laboratories, comprehensively enhancing the accumulation and efficient utilization of tumor genetic testing data within the hospital.

Additionally, companies can provide hospitals with digital management services for samples and other aspects. The MRD testing cycle is lengthy, requiring sample management after each test. Furthermore, due to tumor heterogeneity, significant variations may exist between samples, posing substantial challenges to sample management. In this context, digital management is essential.

Trend: Expansion of MRD Testing Applications and Continued Standardization of LDTs

Application: Scenario expansion, with interventional therapy as the key focus

As MRD testing emerges as a key opportunity following companion diagnostics, its application in solid tumors has expanded. On one hand, it has extended from the perioperative period to cover the entire cancer diagnosis and treatment continuum; on the other hand, MRD testing is being applied to a broader range of cancer types. Meanwhile, numerous interventional studies are poised to reshape clinical guidelines and treatment paradigms, with drug holidays representing one application of MRD-guided therapeutic intervention.

Combined Detection of Mutations and Methylation: The Primary Direction for Future Technological InnovationUndoubtedly, mutation analysis is currently the mainstream detection method. However, single-modality testing may lack comprehensiveness. In contrast, methylation signals are more concentrated, providing robust signal clusters that offer higher sensitivity and specificity in low-frequency circulating tumor DNA (ctDNA). Multi-omics combined detection integrating mutations and methylation can enhance diagnostic performance and represents a key focus of technological innovation both domestically and internationally.

For example, Guardant Health’s MRD detection product evaluates ctDNA by integrating two dimensions: somatic mutations and methylation alterations. Cohort data demonstrate its effectiveness in predicting clinical recurrence of colorectal cancer.

Hospital adoption serves as the threshold for Laboratory Developed Tests (LDTs), with varying levels of recognition across different collaborations. As hospitals bear the primary risk, they inevitably impose stringent requirements on LDT projects and corporate qualifications for partnership. Therefore, gaining entry into pilot hospitals for collaboration itself constitutes a significant barrier. Beneath this barrier, product recognition varies necessarily. For NGS-based LDT products, while there are approved pathways in the United States, none currently exist in China. Against the backdrop of the ongoing implementation of LDT hospital pilots this year, China is likely to establish market entry thresholds and grant "legitimate" status through hospital adoption rather than by creating formal approval pathways.

As LDT pilot programs roll out, competition among companies is likely to center on hospital partnerships for LDT products. The location where LDTs are performed will become a new benchmark, sparking channel competition for access to top-tier tertiary hospitals participating in the pilots. Companies that survive will be those with both strong R&D and marketing capabilities. LDT projects already implemented locally within hospitals may have priority access to the official LDT catalog, thereby gaining “legitimate” status. Other projects not selected may remain in a state of tacit approval during the pilot phase; however, in the long term, once LDT policies mature, inclusion in the LDT catalog will likely become a prerequisite for launching new projects.

Chapter 1 OverviewSituation: Intensive industrial cooperation dynamics, with a compound annual growth rate of 66.6% in recent years

1.1 Progress: Solid Tumors Are Gaining Momentum, and MRD Testing Has Heated Up in Recent Years

1.2 Financing: The head effect is prominent, and entry barriers are high

1.3 Market Size: The CAGR over the past six years was 66.6%, and it is projected to reach RMB 18.5 billion by 2030.

Chapter 2 Technology: Inconsistent pathways, entering the clinical validation phase

2.1 Application: NGS Offers the Highest Sensitivity, While Solid Tumor Detection Poses Greater Challenges

2.2 Layout: Domestic companies focus on solid tumors, with broader applicability across pan-cancer types

2.3 Mainstream Approaches: Distinct Characteristics of Tumor-informed and Tumor-agnostic Methods

2.4 Innovation: Multi-Mutation, Multi-Omics, and AI Empowerment

Chapter 3Commercialization: Primarily LDT-based, supplemented by partnerships with pharmaceutical companies

3.1 LDT Model: The LDT pilot program has entered the implementation phase and will continue to be standardized

3.2 Collaboration with Pharmaceutical Companies: Mutual Benefit and Win-Win, Gradually Expanding into Early-Stage Development

3.3 Empowerment: NGS Automation Solves the “Last Mile” Problem

Chapter 4 Trends: Expansion of MRD Testing Applications, with LDTs Becoming Increasingly Regulated

4.1 Application: Scenario Expansion, with Interventional Therapy as a Key Focus

4.2 Innovation: Multi-analyte combined detection is the future direction of innovation, with mutation plus methylation being the mainstream approach

4.3 Model: Entering the LDT pilot program offers a first-mover advantage, but it is not the end goal

Please scan the QR code below to get the full report for free.

Special Acknowledgments (in the order of research interviews):

Mr. Liu Sheng, Senior Product Manager at Qiuzhen Medicine

Ms. Xia Lin, CEO of Huisuan Gene

Mr. Wang Huiyong, CTO of Huisuan Gene

Mr. Du Bo, Founder and CEO of Zhenhe Technology

Dr. Chen Weizhi, Chief Scientific Officer at Zhenhe Technology

Ms. Gong Yuhua, Product Director at Geneseeq, and others