Revenue Soars but Net Margins Slide: Is the 'Botox King' Still a Hot Investment?

IMEIK

Developer of Biomedical Soft Tissue Repair Materials

Haohai Biological Technology

Medical Biomaterials R&D and Manufacturer

Giant Biogene

Skin Care Product R&D Developer

On April 11, 2023, Fosun Pharma announced that its drug registration application for RT002 (i.e., DaxibotulinumtoxinA) for the temporary improvement of moderate to severe glabellar lines in adults caused by corrugator supercilii and/or procerus muscle activity had recently been accepted for review by the National Medical Products Administration. This means that,Fosun Pharma Officially Enters the Botulinum Toxin Market。

In fact, in the past year or two,Many pharmaceutical giants are expanding into the upstream segment of the medical aesthetics industry through mergers and acquisitions or by building their own capabilities., in addition to Fosun Pharma,Huadong Medicine, Sihuan Pharmaceutical, Teyi Pharmaceutical, Yunnan BaiyaoIn recent years, many have also rapidly entered the medical aesthetics sector, with a significant number already reaping the rewards. This situation is primarily driven by the “profit miracle” in the upstream segment of the medical aesthetics industry.

According to the annual report data recently released by upstream companies in the medical aesthetics industry, theirThe gross profit margin in 2022 was generally maintained at over 70%.Among them, the three major hyaluronic acid players—Bloomage Biotechnology, Haohai Biological Technology, and Imeik—reported gross profit margins of 78.37%, 68.98%, and 94.85%, respectively, in 2022, while Giant Biogene and Jinbo Bio, which are vertically focused on the collagen sector, posted gross profit margins of 84.8% and 82.29%, respectively, in the same year.

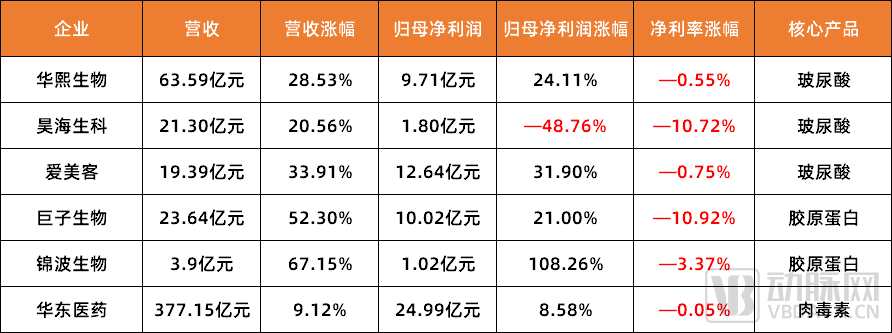

Figure 1. Financial Data of Upstream Medical Aesthetics Companies in 2022 (Source: Corporate Annual Reports for 2022)

However, this is not the sole focus of VCBeat. Through further analysis of annual reports, VCBeat has also identified several intriguing phenomena:First, although upstream medical aesthetics companies all achieved revenue growth, their net profit margins declined to varying degrees in 2022. Second, regarding product portfolios, these companies were seeking new growth curves in 2022: Imeik began laying the groundwork for botulinum toxin products, while Bloomage Biotechnology rapidly entered the collagen sector. Third, at the strategic level, upstream giants represented by Bloomage Biotechnology are gradually transitioning from B2B to B2C markets.

So, what exactly is the reason behind this?

Why Are Upstream Players in the Medical Aesthetics Industry Reaping the Biggest Rewards?

“Those upstream eat the meat, those downstream sip the soup, while those in the middle can’t even gnaw on the bones.”, this phrase could not be more apt to describe the medical aesthetics industry in the past year or two.

In fact, unlike the highly profitable upstream segment of the medical aesthetics industry, the midstream and downstream sectors have been trapped in a “profitability paradox” in recent years, with average net profit margins below 10%. A significant number of companies and institutions have also shut down. According to data from Qichacha, a total of 811 medical aesthetics enterprises and institutions across China ceased operations or were deregistered between January and October 2022. It is no surprise, then, that Jin Xing, Chairman and CEO of So-Young International Inc., lamented,“2022 was a true winter for the medical aesthetics industry, with the market not only shrinking partially but even experiencing its first negative growth in 20 years.”

So, how exactly is this wealth gap within the industry created?

Currently,China's medical aesthetics industry has entered a phase of business growth driven primarily by technological and product innovation., while the upstream segment of the medical aesthetics industry, dominated by raw material producers and product manufacturers, is inherently driven by technology and materials. This sector features high entry barriers and low market penetration. Furthermore, as non-surgical treatments carry relatively lower risks, their business models are more stable and easier to scale, thereby yielding stronger profitability.

In short, materials and technologies can turn potential demand into reality, thereby driving changes in the industry. Since most of these materials and technologies are controlled by upstream companies in the medical aesthetics sector, they hold absolute “say.”

Unlike the upstream sector, the mid- and downstream segments of the medical aesthetics industry are characterized by business model innovation, low entry barriers, and high replicability. Coupled with the vast market potential of the industry, these factors have attracted a large number of enterprises. However, once these companies reach a certain scale, they enter a phase of intense internal competition. To break free from this hyper-competitive environment, mid- and downstream medical aesthetics firms have placed their bets on marketing, specifically on customer acquisition strategies.

Taking the listed company Ruili Medical Aesthetics as an example, its financial data shows that from 2017 to 2020, Ruili Medical Aesthetics’ annual revenue exceeded RMB 100 million each year, and its gross profit margin remained basically at around 50%. However, its net profit margin declined year by year, dropping from 15.4% in 2017 to 2.98% in 2020. The profit margin is further narrowing, mainly due to the rapid growth of its customer acquisition costs.Ruili Medical Aesthetics also acknowledged in its IPO prospectus filed that year that it was heavily reliant on promotional, advertising, and online marketing activities to promote its brand and services.

The head of a medical aesthetics institution lamented to VCBeat,“They have no bargaining power with upstream suppliers, while downstream they are burdened by substantial marketing costs, making this inherently a low-margin business.”

Who Among the Upstream “Big Three” Is More Profitable?

By categorizing the businesses of multiple upstream medical aesthetics companies, it was found that they are currently mainly concentrated inHyaluronic Acid、Botulinum ToxinandCollagenThree Niche Segments: This Is Why Hyaluronic Acid, Botulinum Toxin, and Collagen Have Been Dubbed the “Big Three” of the Upstream Aesthetic Medicine Industry in Recent Years. So, Which One Is More Profitable?

·Hyaluronic Acid: The “Three Musketeers” of Medical Aesthetics Have Divergent Fortunes

When it comes to the upstream sector of the medical aesthetics industry, hyaluronic acid is undoubtedly a prominent player. As the first niche segment to emerge within this upstream landscape, hyaluronic acid has indirectly driven the development of the entire medical aesthetics industry. With continuous industry advancement, three leading companies—known as the “Three Musketeers of Medical Aesthetics”—have risen to prominence in the hyaluronic acid market: Imeik, Haohai Biological Technology, and Bloomage Biotechnology.

By analyzing their 2022 annual reports, VCBeat found that while the “Three Musketeers of Medical Aesthetics” delivered markedly different results in 2022, their commonalities were also evident.1. Revenue increased across the board, Imeik, Haohai Biological Technology, and Bloomage Biotech recorded revenue growth of 33.91%, 20.56%, and 28.53%, respectively;Second, net profit margins are all showing a downward trend.. The key difference lies in the fact that Imeik maintained high net profits through high gross profit margins, while Bloomage Biotech achieved dual growth in revenue and net profit, albeit with a decline in the growth rate of profitability. Haohai Biological Technology ranked last, becoming the only company to record “increased revenue but stagnant profits.”

Behind the divergence in performance lies the rapidly evolving landscape of the hyaluronic acid market and the distinct development paths pursued by three companies. In terms of business composition, Imeik continues to deepen its presence in the medical aesthetics sector while expanding into new products beyond hyaluronic acid; Bloomage Biotechnology has achieved rapid growth by leveraging functional skincare products; and Haohai Biological Technology has continuously diversified its business through mergers and acquisitions, establishing a tripartite model encompassing “medical aesthetics, ophthalmology, and orthopedics.”

The fact that the three major hyaluronic acid players are all seeking new business growth points indicates thatChina’s Hyaluronic Acid Sector Is “Cooling Down”, primarily due to the increasing number of competitors in the hyaluronic acid sector and the maturation of technology, prices for hyaluronic acid—from raw materials to end products—have been declining year by year. According to a report by Frost & Sullivan, the average price of hyaluronic acid raw materials decreased gradually from RMB 210 per gram in 2017 to RMB 124 per gram in 2021, representing a drop of over 40%.

·Collagen: Revenue growth exceeded 50%, with the industry in a phase of rapid market expansion

In recent years, a wave of IPOs has been sweeping through the collagen sector.In late 2022, Giant Biogene successfully went public, becoming the first listed company in China’s collagen industry.; In March 2023, Jinbo Bio successfully passed the review for its listing on the Beijing Stock Exchange (BSE), following its previous listings on the NEEQ and the STAR Market.

The Rise of Collagen in the Secondary Market: Driven by Surging Growth Rates, Giant Biogene and Jinbo Bio Report Revenue Increases of 52.3% and 67.15% Respectively in 2022, Far Outpacing the “Big Three” Hyaluronic Acid Players

Among them, the majority of Giant Biogene's revenue growth stemmed fromComfyandCollgeneTwo flagship products: According to financial reports, Comfy and Collgene generated revenues of RMB 1.613 billion and RMB 618 million, respectively, in 2022, accounting for 68.2% and 26.2% of the total annual revenue. Jinbo Bio’s “growth engine” stems from its recombinant humanized type III collagen, which was approved for market launch in June 2021.“Weiyimei”, this is currently the only injection-grade recombinant humanized type III collagen biomaterial for medical use. In the first three quarters of 2022, Weiyimei achieved cumulative revenue of RMB 73.95 million from this single product.

Although the full-year revenue and net profit performance was acceptable, in the collagen sector, both gross margin and net profit margin declined significantly compared to the same period last year.. Taking Giant Biogene as an example, financial report data shows that its gross profit margin was 84.4% in 2022, while from 2019 to 2021, the figures were 83.3%, 84.6%, and 87.2%, respectively. This indicates that after rising for three consecutive years, Giant Biogene’s gross profit margin has fallen back to the 2020 level. In response, Giant Biogene stated in its financial report that the decline in gross profit margin was primarily due to the expansion of product types and the development of new sales channels.

Figure 2. Collagen-based injectable fillers under development in China (Data sources: Giant Biogene prospectus, Jinbo Bio prospectus)

Looking ahead, collagen is emerging as a new favorite in the medical aesthetics industry, following hyaluronic acid. As an emerging technology, it boasts high tensile strength and biodegradability, and promotes cell growth when used as a scaffold for artificial organs or as wound dressings, thereby facilitating synergistic repair of wounds with newly generated cells and tissues. According to data released by Grand View Research, the market size of collagen in China was RMB 28.7 billion in 2021 and is projected to reach RMB 173.8 billion by 2027, representing a compound annual growth rate (CAGR) of 35.01% from 2021 to 2027.

· Botulinum Toxin: Low market penetration; major players are increasing investments, but it has not yet become a key revenue driver

Due to its versatility and compatibility with other aesthetic treatments such as hyaluronic acid fillers, botulinum toxin enjoys high repurchase rates and practical utility in the medical aesthetics industry. Consequently, over the past two years, numerous listed companies—including Imeik, Haohai Biological Technology, Huadong Medicine, and Fosun Pharma—have aggressively expanded their presence in the botulinum toxin niche market. However, given the high industry barriers,Major players have largely entered the market through distribution agreements and equity investments, primarily by signing cooperation agreements with botulinum toxin manufacturers in South Korea, the United States, and Germany.

However, as of now,Botulinum toxin has yet to become a major revenue driver, with overall progress remaining relatively slow.. In September 2021, Imeik spent RMB 856 million to acquire a 25.42% equity stake in the South Korean botulinum toxin company Huons BioPharma Co., Ltd., aiming to address its shortcomings in botulinum toxin products. However, according to its financial reports, as of the end of the first half of 2022, the investment progress for Imeik’s research and development project on injectable Type A botulinum toxin stood at 22.86%.

In addition, Fosun Pharma began filing for market approval of RT002 (daxibotulinumtoxinA, a type A botulinum toxin) on April 11. However, due to factors such as clinical demand and market competition, the extent to which this product will contribute to Fosun Pharma’s financial performance remains uncertain.

Even so, fueled by capital injection, the botulinum toxin segment—a niche upstream sector of the medical aesthetics industry—is expanding rapidly. According to iResearch’s 2022 Report on China’s Medical Aesthetics Industry, botulinum toxin has become the second most popular injectable medical aesthetic treatment, surpassed only by hyaluronic acid. Additionally, data show that the global market size for botulinum toxin reached USD 5.09 billion in 2020, representing a year-on-year growth of 18.65%.Botulinum toxin brands with precise positioning, unique advantages, or outstanding marketing capabilities are expected to capture a larger market share.

Overall, among the three major players in the upstream medical aesthetics sector, hyaluronic acid demonstrates the strongest revenue-generating capability, although its momentum is gradually cooling. Collagen is experiencing relatively rapid overall growth; however, its current revenue base remains small, with substantial capital currently allocated to R&D and market expansion. Despite significant interest from industry giants and considerable future market potential, botulinum toxin has yet to become a core business for these enterprises.

Rising Revenue, Stagnant Profits: What Is Holding Companies Back?

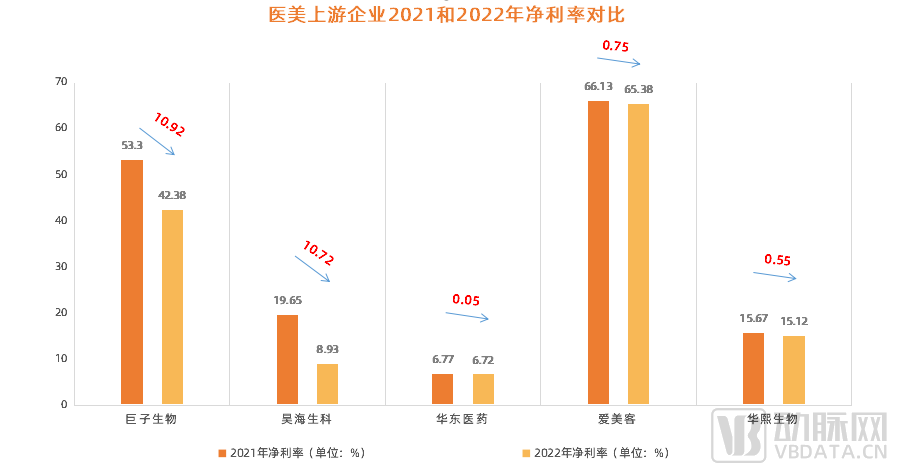

As stated at the beginning,Although upstream medical aesthetics companies all achieved revenue growth in 2022, their net profit margins collectively declined., with Haohai Biological Technology and Giant Biogene seeing their net profit margins drop by as much as 10 percentage points, while Bloomage Biotech and Imeik also experienced slight declines in net profit margin.

Figure 3. Comparison of Profit Margins Among Upstream Enterprises in the Medical Aesthetics Industry (Data Source: Corporate Annual Reports for 2022)

The low gross profit margins in the mid- and downstream segments of the medical aesthetics industry are due to high customer acquisition costs. So, what exactly is holding back the upstream segment? By analyzing financial reports and overall industry trends, VCBeat has summarized the following four points:

First, the shrinking profit margins in the downstream medical aesthetics sector are exerting continuous downward pressure on prices upstream.

Over the past two years, “profitability challenges” have been a persistent label associated with the development of downstream enterprises in the medical aesthetics industry. Under the impact of the pandemic, these downstream players have generally faced operational difficulties, leading to a decline in demand for their products and, consequently, affecting upstream enterprises to some extent. Furthermore, following a period of explosive growth in the medical aesthetics market, customer acquisition costs for terminal medical aesthetic institutions remain high. In an environment of continuously shrinking profit margins, upstream medical aesthetic products, represented by hyaluronic acid, are under sustained pressure to reduce prices.

Second, upstream medical aesthetics companies are all in a transitional phase, with significant upfront investments and no economic benefits generated to date.

As previously mentioned, major upstream players in the medical aesthetics industry are currently seeking new breakthroughs. For the “big three” hyaluronic acid manufacturers, Bloomage Biotech officially entered the collagen industry in April 2022 by acquiring a 51% equity stake in Yierkang; Haohai Biological Technology expanded its business into radiofrequency and laser-based aesthetic treatments in February 2022 by spending RMB 205 million to acquire a 63.64% equity stake in Ohymech, a manufacturer of laser medical devices; Imeik extended its product portfolio to include regenerative materials and botulinum toxin, leveraging this expansion to secure exclusive distribution rights for its botulinum toxin products and venture downstream into the skincare sector.

However, financial reports indicate that these new businesses have not yet generated economic benefits as they are still in the investment phase, thereby compressing the net profit margin to some extent.

Third, traffic restrictions and logistical disruptions during the pandemic placed significant operational pressure on upstream medical aesthetics companies, leading to severe product backlogs.

2022 was the year in which the medical aesthetics industry was most severely impacted by the pandemic. The primary reason was that continuous lockdowns introduced significant uncertainties across the entire sector, indirectly causing operational and production difficulties for upstream enterprises and leading to widespread product backlogs.

Taking Bloomage Biotech as an example, its financial report shows that the net cash flow from operating activities in 2022 decreased by 50.2% year-on-year to RMB 640 million, primarily due to increased payments for inventory procurement and expenses. It is reported that Bloomage Biotech’s inventory scale has continued to rise, reaching RMB 1.162 billion by the end of 2022, a year-on-year increase of 63.80%. Of this RMB 1.162 billion in inventory, finished goods accounted for as high as 82.40%.

Fourth, the increasing number of market entrants and fragmented product pipelines have intensified overall competition, leading to a gradual erosion of absolute industry advantages.

In recent years, driven by rapid capital influx, the number of participants in the upstream segment of the medical aesthetics industry has surged. In addition to listed companies such as Huadong Medicine crossing over into the medical aesthetics sector, nearly 85% of medical aesthetics startups that secured financing in the primary market over the past one to two years are concentrated in the upstream segment.

It is precisely for this reason that the product categories in the upstream medical aesthetics sector are continuously expanding. It is reported that, in addition to the three major players in the upstream medical aesthetics market, niche segments such as medical dressings, functional skincare products, chemical peeling agents, and microneedles are also experiencing rapid development. This has intensified overall industry competition, making it increasingly difficult for certain products to be selected by downstream medical aesthetics institutions. The absolute advantage these products once held across the entire industry chain is gradually diminishing.

Final Remarks

An institutional partner focused on the consumer healthcare sector once told VCBeat that there will always be a market for consumer healthcare. Once this gateway is opened, demand will persist regardless of how many years pass into the future, although such demand will gradually evolve with technological iterations.

Therefore,For consumer healthcare companies, the initiative lies not with the market but with themselves. The extent of their growth potential, their ability to pioneer breakthrough technologies, and their capacity to launch more innovative business promotion models will all constitute their core competitiveness in this sector.

Especially for the upstream sector of the medical aesthetics industry, which is inherently technology-driven, market competition will gradually intensify in the future against the backdrop of the industry’s accelerating upward extension, leading to a fundamental shift in the competitive landscape. However, in this field, the innovativeness of technology and the ability to establish effective distribution channels will always remain the core criteria for evaluating enterprises.

·References:

1. “Bloomage Biotech Leads in Revenue as Performance Diverges Among the ‘Three Musketeers’ of Medical Aesthetics” – The Beijing News;

2. “Giant Biogene, the ‘Blue-Chip Stock’ of Medical Aesthetics, Discloses Its First Post-IPO Financial Report: 2022 Sales Reached RMB 2.36 Billion, Marketing Expenses Doubled” — 21st Century Business Herald;

3. “Botulinum Toxin and Collagen ‘Take the Baton’ from Hyaluronic Acid: Upstream Aesthetic Medicine Capitalization ‘Blossoms on Multiple Fronts’” — Shanghai Securities News;

4. “Financing with the Left Hand, Acquiring with the Right: Why Is the Upstream Medical Aesthetics Sector So Frenzied?” — Financing China.