Sequoia and Legend Capital Quietly Back CBCT Sector as Domestic Substitution Accelerates with Multiple IPO Filings

With Sinovision Technologies filing its prospectus earlier this month, five leading Chinese medical imaging equipment manufacturers have submitted their filings in less than a year—an unprecedented milestone.

“While the pace of technological innovation under the banner of ‘domestic substitution’ is astonishing, the future competition is truly concerning as numerous high-tech enterprises crowd into an already somewhat saturated track. In fact, apart from United Imaging Healthcare, which has entered the mid-to-high-end market, other companies focusing on CT and MRI have failed to deliver results that would reassure investors.”

However, medical imaging equipment manufacturers still have room to maneuver. They can strive to become leaders in niche segments or pursue differentiated R&D pathways. The latter, in particular, offers numerous entrepreneurial opportunities within the vast medical imaging landscape.

For example, CBCT.

CBCT is the abbreviation for Cone Beam CT, also known as cone-beam computed tomography.

Although CBCT is also a type of CT, it differs from the spiral CT commonly used in clinical practice. Spiral CT acquires continuous cross-sectional images of the human body by emitting fan-beam X-rays through unidirectional rotation, then reconstructs these layers into images. Its essence lies in reconstructing two-dimensional data from one-dimensional projection data, and subsequently stacking multiple consecutive 2D slices to generate a 3D image. In contrast, CBCT emits cone-beam radiation to obtain 2D projection data, which is directly reconstructed into a 3D image, thereby providing a more stereoscopic visual effect.

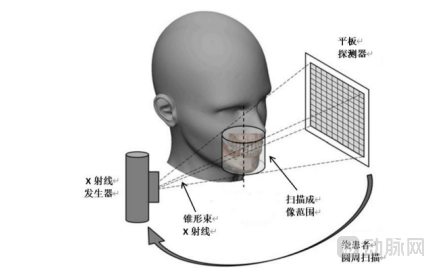

Principle of Oral CBCT Imaging (Image Source: Langshi Medical Prospectus)

It is precisely due to its advantages in spatial resolution that cone-beam computed tomography (CBCT) is widely used in dentistry, gynecology (for breast examination), and radiation oncology. Among these applications, dental CBCT is the most extensively utilized device in this field. With low radiation dose, isotropic imaging, and high spatial resolution, CBCT-generated three-dimensional images can clearly depict the entire dentition and pathological tissues, thereby assisting physicians in surgical procedures and medication management.

In radiotherapy, cone-beam CT (CBCT) guidance is more commonly used than ultrasound or MRI guidance. Its advantage lies in ensuring the reproducibility and consistency of patient positioning for each treatment session. MV-CBCT systems, which utilize megavoltage beams, can reconstruct axial, coronal, and sagittal images from acquired two-dimensional projections. Both Varian’s Halcyon and Accuray’s TOMO employ this approach for image-guided radiation therapy (IGRT).

Comparison of Indicators Between Traditional Spiral CT and CBCT (Data Source: Compiled from Public Information)

Leading domestic dental CBCT manufacturers—Meiya Optoelectronic, LargeV Instrument, Fussen Technology, and Born Digital—have all been active in this field for over a decade. While they are no longer newcomers among imaging equipment companies, they cannot yet be considered seasoned veterans.

However, in terms of market share, according to the 2021 data provided by Zheshang Securities Research Institute, Meyer Optoelectronic ranked first with 29%, followed closely by LargeV Instrument with 18%. Although only LargeV Instrument completed a Series A financing round in 2016 among the two companies, they together have captured nearly half of the dental CBCT market.

Without the involvement of policy and capital, domestic substitution in this sector has proceeded quietly.

Compared with the vast and complexly branched field of radiology CT, CBCT is a small yet promising niche, where companies deeply involved are highly specialized.

Although Meyer Optoelectronic, a publicly listed company, has a broad business layout, its medical division is uniquely anchored by dental cone-beam computed tomography (CBCT). Annual report data show that the company’s dental CBCT business has demonstrated a sustained upward trend, with operating revenues of RMB 484 million, RMB 454 million, RMB 656 million, and RMB 716 million in 2019, 2020, 2021, and 2022, respectively.

Langshi Instrument, which filed its prospectus last year, has gone “all in” on CBCT. Its operating revenues for 2019, 2020, and 2021 were RMB 221 million, RMB 219 million, and RMB 410 million, respectively, with corresponding profits of RMB 20 million, RMB 18 million, and RMB 64 million. Notably, 99.9% of Langshi Instrument’s operating revenue was derived from dental CBCT.

A comparison of data from the two leading CBCT companies reveals that, although both achieved leapfrog growth in 2021, their scale remains far smaller than that of major medical equipment sectors such as CT and MRI. In terms of profitability, however, dental CBCT has outperformed most domestic medical equipment manufacturers, driven by a combination of favorable factors.

First, the competitive landscape was relatively moderate. Before domestic CBCT technology reached maturity, German brand CAVO Dental, Italian NewTom, and Japan’s Morita dominated the market for large general hospitals, while Finnish Planmeca, German Sirona, and American Carestream occupied the second tier, primarily targeting large specialized dental clinics. However, the vast majority of these enterprises merely relocated their sales teams to China, establishing distribution channels without conducting any local R&D.

Amid the trend of “domestic substitution,” the aforementioned companies lack the capacity for rapid localization and domestic production seen in joint ventures such as GPS. They are unable to mitigate policy-related risks or provide hospitals with safe and efficient after-sales services; fault repairs and X-ray tube replacements must either be coordinated through distributors or outsourced to third-party service providers.

As a domestically produced CBCT, the enterprise’s greatest advantage lies first in its “domestic” status, and second in its comprehensive, stable, and timely original manufacturer after-sales service and training system. For maintenance and training services in most regions, Meiya Langshi can achieve same-day response upon call, striving to ensure continuous equipment operation and helping medical institutions save significant costs.

Next are the core components that are easily substitutable with domestically produced alternatives. Cone-beam CT utilizes a cone-shaped X-ray beam emitted from an X-ray generator, eliminating the need for rotation and thus obviating the requirement for core components such as slip rings and high-voltage generators. This results in lower manufacturing costs and a lower unit price.

In cone-beam computed tomography (CBCT) systems, the flat-panel detector accounts for a high proportion of the value, representing 30%–40% of total costs, and constitutes the core barrier limiting CBCT development. The X-ray tube ranks second, accounting for approximately 10% of total costs. Currently, domestic CBCT manufacturers primarily rely on a model of “imported consumables with third-party processing” for procurement. As companies such as United Imaging Healthcare and Nanovision (Shansiwei) deepen their in-house R&D efforts, upstream costs are expected to be further reduced, potentially leading to lower retail prices for domestically produced CBCT systems.

Currently, imported CBCT systems targeting the mid-to-high-end market are priced between RMB 400,000 and RMB 2.5 million. However, public hospitals and high-end private medical institutions can purchase a specialized dental-grade CBCT from Langshi Instrument for under RMB 400,000. Primary healthcare institutions can acquire a “four-in-one” intelligent dental CBCT for less than RMB 300,000, with a single device integrating four major functionalities: CBCT, panoramic imaging, cephalometric imaging, and intraoral photography.

It is worth noting that the low-price strategy of domestically produced CBCT has sacrificed a portion of profits, yet still maintains a relatively high gross profit margin. The gross profit margin of Langshi Medical has consistently fluctuated around the 40% mark, outperforming the vast majority of domestic medical equipment manufacturers engaged in the production of CT and MR systems.

Finally, there is the vast market driven by the growth of private hospitals. Data from a report by Zheshang Securities Research Institute shows that private specialized dental hospitals experienced rapid development during the second decade of the millennium, with the number of institutions registering a compound annual growth rate (CAGR) of 17.7% from 2016 to 2020. The number of individual dental clinics reached 82,455 in 2020, while specialized dental hospitals numbered only 945.

Unlike large general hospitals, individual dental clinics, constrained by limited capital, prioritize cost-effectiveness when purchasing equipment and generally do not consider expensive imported devices. Consequently, the incremental market growth in recent years has naturally fallen to domestic CBCT manufacturers that have established a presence in the primary healthcare market.

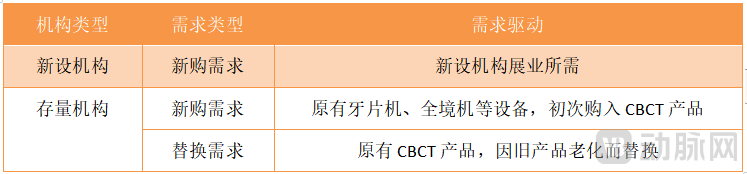

Langshi Instruments’ Demand-Driven Approach (Source: Shanghai Stock Exchange)

Particularly in the past two years, the implementation of volume-based procurement for dental consumables has caused previously high-margin segments, such as orthodontic brackets and dental implant systems, to lose momentum. In response to this policy shift, many dental hospitals have begun developing specialized services, enhancing user experience through improved dental examinations and post-operative follow-ups, and seeking new revenue streams.

During this process, many dental clinics have incorporated dental CBCT into their service offerings to seek new avenues for growth. It is evident that both MeiYa and Langshi experienced a surge of over 50% in 2021. Riding on this momentum, the market dividends generated by dental clinics will continue to fuel the growth of domestically produced CBCT systems in China for several years.

Although domestic dental CBCT manufacturers that strategically positioned themselves early are now riding the wave of growth, their future is not without challenges.

The relatively low demand for core components was once the key driver behind the domestic substitution of dental CBCT systems in China, but it may also attract more companies to enter the field due to lower barriers to entry. In this context, companies such as Meiya and Langshi have been able to achieve rapid expansion during market growth by heavily relying on dental CBCT equipment. However, if they lose competitiveness in their core products, the associated risks could completely push them out of the medical market.

In recent years, several startups have launched dental CBCT systems. Companies such as Youfang Medical and Dentifi have secured tens of millions in financing and entered the market with strong momentum, backed by integrated digital dental marketing ecosystems.

Amid this trend, the top-tier companies’ primary imperative is to seize emerging opportunities and expand aggressively, while their secondary priority is to accelerate the R&D of diversified products to mitigate potential risks arising from an overly concentrated business portfolio.

Taking Zhejiang Langshi Instrument Co., Ltd. as an example, in addition to continuously improving and upgrading its existing dental cone-beam CT products and manufacturing processes, the company is primarily focused on two initiatives: first, further exploring demands along the specialized clinic sector by developing new products such as ENT cone-beam CT systems and clear aligners; and second, monitoring advanced overseas products and attempting to invest in startups engaged in the R&D of innovative technologies, including painless anesthesia and laser ablation.

Beyond hardware breakthroughs, software must keep pace. Domestic equipment manufacturers generally provide free post-processing systems; however, their imaging performance lags significantly behind that of mid-to-high-end devices from South Korea and Europe. Although enhancing capabilities in this area may not enable companies to capture the mid-to-high-end market, it can effectively boost competitiveness in the low-end market at similar price points.

It is also important to note that this wave of oral CBCT procurement is centered on individual dental clinics. Therefore, in addition to providing equipment and routine maintenance support, manufacturers should prioritize the development of AI capabilities to enable assisted teaching, annotation, and reconstruction. In primary healthcare settings, where the professional proficiency of dentists varies significantly, artificial intelligence can help enhance the diagnostic and treatment capabilities of both dentists and nurses.

In summary, although a clear tiered structure has emerged among grassroots dental CBCT providers, the maturity of upstream core component suppliers, the sustained growth of downstream private medical institutions, and the limited technical barriers for midstream equipment manufacturers mean that startups still have the opportunity to catch up and surpass incumbents by leveraging high-quality hardware and software, after-sales services, and digital dental ecosystems, thereby reshaping the market landscape for dental CBCT.

While dental CBCT embodies the current prosperity of CBCT technology, its technical iteration ceiling is clearly visible. In terms of “great prospects,” its application scenarios may lie outside the field of dentistry.

In addition to the aforementioned applications in breast imaging and radiotherapy guidance, high-resolution cone-beam computed tomography (HR-CBCT) angiography has been proven effective for visualizing vascular anatomy. Compared with the more commonly used three-dimensional digital subtraction angiography (3D-DSA), HR-CBCT offers higher spatial resolution. When combined with appropriate acquisition protocols and reconstruction algorithms, HR-CBCT provides clear delineation of anatomical structures, thereby supporting clinical decision-making in the treatment of neurointerventional diseases.

Currently, HR-CBCT is commonly used in clinical practice for pre- and post-treatment evaluation of aneurysms; localization for surgery or stereotactic radiotherapy planning of cerebral arteriovenous malformations; identification of dural arteriovenous fistulas; counting and localizing different ostia within the sinuses; assessment of collateral circulation in stroke; visualization of distal vessels beyond the occlusion site; and identification of false lumens as well as intracranial atherosclerosis or dissection. It may also hold value in the treatment of conditions such as carotid-cavernous fistulas, vasospasm, and spinal vascular malformations in the future.

However, HR-CBCT also has certain drawbacks, including the need for general anesthesia during examination, limitations in vascular phase resolution that make it difficult to isolate arterial or venous phases alone, and the requirement for higher contrast agent doses and increased radiation exposure due to longer acquisition times. The technology still requires further improvement.

Several domestic companies are currently engaged in the research and development of CBCT for neurointerventional applications. Taking the startup Rayence Smart Medical as an example, the company has developed a highly cost-effective CT system based on CBCT architecture, featuring a short C-arm with Z-axis rotational scanning.

The imported array detectors required for CT scanners cost approximately RMB 1–10 million, whereas the domestically produced flat-panel detectors used in CBCT systems cost only RMB 50,000–100,000. Based on this approach, the CBCT reduces the cost associated with traditional CT scanners—from RMB 2–30 million down to RMB 200,000–500,000—thereby addressing the pain points of prohibitively expensive existing CT equipment, limited availability in primary healthcare institutions, and delayed diagnosis and treatment for stroke patients. Hence, it is termed “Ultra-High Cost-Performance CT.”

To address the challenges associated with CBCT, such as the difficulty of three-dimensional reconstruction, poor soft-tissue clarity, and inability to meet the clinical diagnostic requirements for stroke, RaySee Smart Healthcare employs digital imaging techniques. It enhances CBCT images using models incorporating intelligent scatter suppression, three-dimensional reconstruction, and image quality enhancement algorithms, thereby ensuring compliance with clinical diagnostic standards for stroke.

Overall, CBCT has broad application potential in neurointerventional procedures; however, startups should carefully weigh the input-output ratio before entering this space. After all, breaking into the neurointerventional CBCT market requires a high entry cost, and once in, companies will face direct competition from multinational imaging equipment giants such as GE Healthcare and Philips.

RaySee Smart Healthcare has indeed proposed a primary care strategy akin to dental CBCT, but whether this model can be truly replicated is a question only time can answer.