From 2C to 2B: An 18-Fold Revenue Surge Offers Key Insights into Solving Digital Therapeutics’ Commercialization Challenges

Akili

Digital Medicine Therapy Developer

Pear Therapeutics

Developer of Digital Healthcare Solutions

Better Therapeutics

Prescription Digital Therapeutics Provider

DarioHealth

Digital Therapeutics Platform Operator

Not long ago, Pear Therapeutics, a representative company in the digital therapeutics sector, announced that it was seeking bankruptcy protection. Although its failure was not entirely attributable to issues with digital therapeutics per se, but rather to a confluence of internal and external factors, this event serves as a stark warning for the digital therapeutics industry, which is still in its early stages of development.

In addition to Pear, several publicly listed digital therapeutics companies have also released their annual reports. How did they perform? What common challenges do they face? Are there any successful development models worth emulating? VCBeat (WeChat ID: VCBeat) has analyzed the annual reports of these publicly listed digital therapeutics companies.

The most evident issue is that low revenue remains one of the biggest challenges facing publicly listed digital therapeutics companies.

Pear Therapeutics, touted as the “first publicly traded digital therapeutics company,” has now filed for bankruptcy protection, yet its annual report remains a valuable reference. According to the report, the company generated $12.694 million in revenue in 2022, representing a substantial 202% increase from the $4.208 million recorded in the previous year. However, this revenue was merely a drop in the bucket compared to Pear’s enormous expenditures—after deducting various high costs, the company’s operating loss in 2022 reached as high as $123 million.

A comparison of revenue and costs reveals that “the more you earn, the more you spend” is a major problem for Pear. Compared with 2021, Pear’s revenue increased by $8.486 million, but its operating costs in 2022 rose by $17 million year over year, far outpacing revenue growth. In fact, Pear faced the same issue of “the more you earn, the more you lose” in the prior year.

Comparison of Pear’s Annual Report Metrics Over the Years (Chart by VCBeat)

While this demonstrates that Pear’s “front line” was overstretched, the core issue remains insufficient revenue.

Akili, known for treating pediatric ADHD with game-based digital therapeutics, also reported lackluster revenue. It generated only $323,000 in revenue in 2022, down from $538,000 in 2021. However, the decline was primarily due to the absence of partnership income in 2022. Viewed solely from a product revenue perspective, Akili’s earnings increased from $186,000 in 2021 to $323,000, representing a growth rate of 73.7%.

Comparison of Akili's Annual Report Metrics Over the Years (Chart by VCBeat)

However, Akili only went public in 2022, raising capital to support its commercialization efforts; achieving tangible results within such a short timeframe is no easy feat. Furthermore, Akili has demonstrated slightly better control over operating costs compared to Pear Therapeutics, reporting an operating loss of $90.68 million in 2022. Given its current financial position, the company remains viable. Whether Akili can make significant commercial progress and generate higher revenue in 2023 will determine if it can avoid meeting the same fate as Pear Therapeutics in the future.

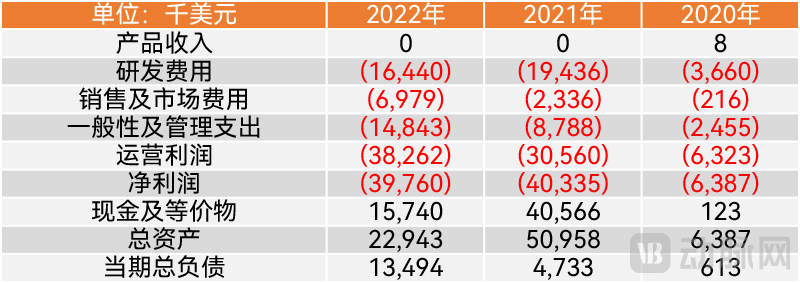

Better Therapeutics, which went public shortly after Pear, faces a more challenging situation. The products of Pear and Akili have at least secured FDA medical device clearance, allowing them to commence commercialization. To date, Better has yet to obtain FDA approval, resulting in its annual reports showing “zero” revenue for two consecutive years.

Better’s Annual Report Metrics Over the Years (Chart by VCBeat)

With zero revenue, even though Better managed to keep its operating costs remarkably low at just $38.26 million, it was still akin to trying to cook without rice. In an effort to save itself, Better not only began laying off employees but also completed a round of private financing to secure the funds needed for its product launch. Reportedly, its senior executives contributed significantly to this private financing round.

Relatively speaking, DarioHealth, which has long been publicly listed, boasts the strongest revenue performance among US-listed digital therapeutics companies. It achieved $27.66 million in revenue in 2022, a 34.8% increase from the previous year. Notably, even after deducting various sales expenses, DarioHealth still realized a gross profit of $9.66 million.

Dario’s Annual Report Metrics Over the Years (Graphic by VCBeat)

Dario’s revenue far exceeds the combined total of Pear, Akili, and Better Therapeutics, yet its operating loss stands at only $56.81 million, lower than that of both Pear and Akili. From this perspective, Dario’s operations are quite pragmatic and sustainable.

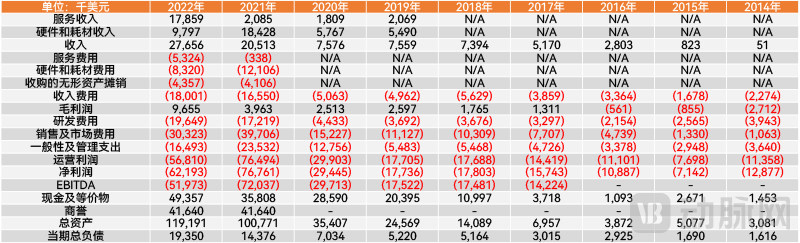

Expanding the scope beyond U.S. stocks, the revenue of Tali, a well-known Australian digital therapeutics company, is impressive. In fiscal year 2022, it achieved revenue of AUD 881 million (approximately USD 582 million), representing a substantial 60.6% increase from the previous fiscal year. Compared with U.S.-listed digital therapeutics companies, whose revenues peak at less than USD 30 million, Tali’s revenue is undoubtedly at a giant scale.

Tali's Key Annual Report Indicators in Recent Years (Chart by VCBeat)

However, a closer analysis reveals that Tali’s revenue is not as impressive as it appears on the surface. Product revenue amounted to only A$13.17 million in fiscal year 2022, accounting for just 1.5% of its total revenue, which is even weaker than its performance in previous years. Notably, in fiscal years 2021 and 2020, Tali’s product revenue stood at A$34.24 million and A$47.23 million, respectively, representing 6.2% and 7.6% of its total revenue.

Tali’s revenue is primarily derived from other income, including fees received from collaborative research and development (R&D), donation income, and R&D tax subsidies. Among these, R&D tax subsidies constitute Tali’s primary source of income, reaching AUD 614 million in fiscal year 2022.

Despite substantial revenue, Tali’s costs were also exorbitant. Compared with fiscal year 2021, Tali’s advertising and promotion expenses increased by 1.39 times, reaching AUD 2.114 billion. The full-year operating loss amounted to AUD 6.936 billion, representing a 42.8% increase from the previous year.

According to annual reports, the product pipelines of listed digital therapeutics companies fall into two categories: broad diversification and high focus. A representative of the broad diversification strategy is Pear Therapeutics, which maintains multiple product pipelines spanning various indications.

Pear has developed a pipeline of up to 17 product candidates, with primary indications spanning addiction cessation as well as sleep disorders, depression and anxiety, migraine, and irritable bowel syndrome. These investigational pipelines require corresponding investments to complete product design, exploratory trials, and subsequent clinical trials.

Among these 17 product pipelines, three have received FDA approval and entered the commercialization phase. This has made Pear one of the companies with the largest number of approved digital therapeutics. However, even by 2022, only one product was truly generating significant revenue, while the other two were still in stages requiring substantial marketing investment.

Due to revenue growth falling short of expectations, coupled with an unfavorable U.S. economic and financing environment, Pear’s seemingly extensive product pipeline has instead become a burden, keeping its costs persistently high. Clearly, overestimating its own capabilities and spreading its resources too thin contributed to Pear’s failure. This is not unique to Pear; indeed, it is a common pitfall among startups. However, this issue was particularly pronounced in Pear’s case.

In contrast, the product pipeline strategies of other publicly listed digital therapeutics companies are more focused.

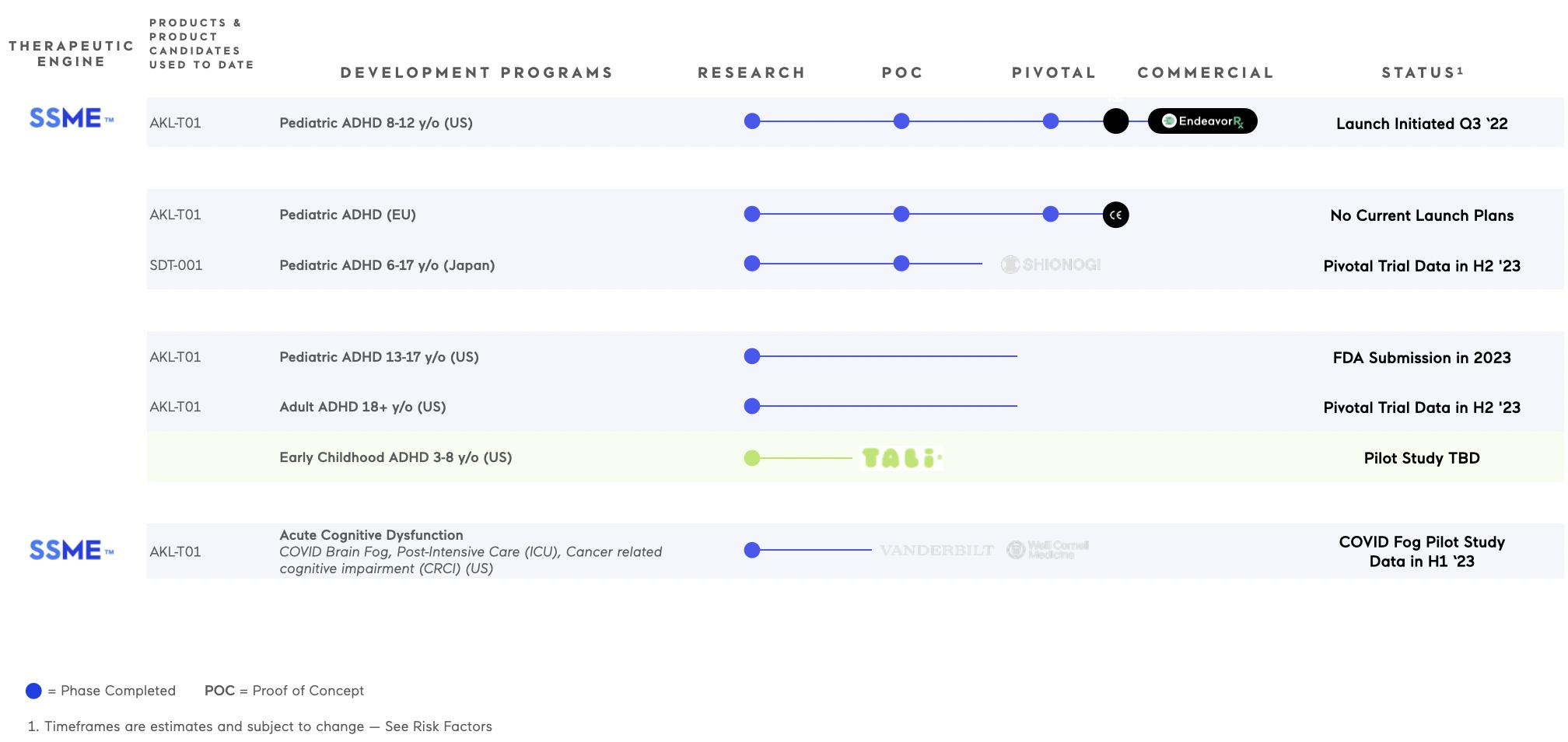

Taking Akili as an example, its annual report shows that it currently has seven product pipelines. However, a closer look reveals that these seven pipelines actually target only two indications: attention-deficit/hyperactivity disorder (ADHD) and cognitive impairment. In contrast, Akili’s prospectus in early 2022 listed a much broader pipeline of 13 products. Clearly, Akili’s decision to focus its product pipeline is a rather pragmatic choice.

Akili’s seven product lines actually target only two types of indications (image from Akili’s annual report)

ADHD is its primary indication, with as many as six of its seven product pipelines targeting ADHD across different age groups, covering patients from age 3 through adulthood. Compared with pursuing a broad range of indications, its product development is markedly more focused, and the R&D timeline is significantly faster.

Another indication is cognitive impairment training, with post-COVID-19 “brain fog” sequelae being a key area of focus. Currently, Akili is collaborating with healthcare institutions to evaluate the efficacy of its existing products in addressing cognitive impairments that emerge after recovery from COVID-19. Given the large population affected by COVID-19 and the potential for reinfection, demonstrating efficacy could yield promising prospects. This may well be a crucial reason why Akili has chosen to retain this product pipeline.

Dario was also highly focused in its early stages, primarily centering its business on chronic disease management for diabetes. Prior to its strategic transformation, Dario had already achieved relatively stable revenue. Although the scale was modest, hovering around $7 million, Dario secured approval for its digital therapeutic for diabetes as early as 2015, enabling an earlier commercialization process. Furthermore, its effective cost control kept operating losses below $30 million.

Given the vast market potential for consumer-focused diabetes management, competition in this sector is also intense. Dario’s initial competitors included pharmaceutical and medical device giants such as Abbott, Asensia (formerly Bayer’s diabetes division), Johnson & Johnson’s LifeScan, Roche, and Sanofi. These industry leaders hold the majority of the market share in blood glucose monitoring systems (BGMS) for diabetes self-management, making it challenging to compete against them.

The consumer-focused diabetes chronic disease management market is highly competitive. In response, Dario initiated a strategic transformation in 2020. First, Dario began to gradually adjust its business model, transitioning from direct-to-consumer (DTC) to a B2B2C approach. By leveraging the strengths of its consumer solutions platform and selling to B-end clients such as health plans and employers, Dario significantly expanded commercial growth opportunities within traditional healthcare channels while reducing marketing costs.

Meanwhile, Dario expanded into other types of chronic disease management through three acquisitions in 2021. In early 2021, Dario acquired Upright Technologies, and then acquired Physimax in early 2022, launching the digital therapeutic for chronic pain, Dario Move, through resource integration. In mid-2021, Dario also acquired PsyInnovations, announcing its entry into the behavioral health sector.

Unlike Pear, which relies entirely on its own efforts to expand its multi-product pipeline, Dario has achieved indication expansion by acquiring mature product pipelines. This approach not only enables rapid revenue generation but also leverages the resources of the acquired companies to explore further commercial opportunities. It must be acknowledged that Dario’s timing for mergers and acquisitions was excellent; 2021–2022 coincided with a period of widespread recognition for digital health, making it relatively easy to raise the capital required for these acquisitions.

Changes in Dario’s B2B and C2B Revenue (Chart by VCBeat)

In analyzing Pear’s failure, we pointed out that Pear relied almost exclusively on the consumer (C-end) market, with little success in business-to-business (B-end) partnerships. In contrast, Dario’s B2B2C strategy has already shown initial results in terms of revenue. In 2021, B-end revenue accounted for only 4% of its total income; by 2022, although C-end revenue declined, B-end revenue surged 18-fold from $851,000 the previous year to $16.38 million, significantly increasing the share of B-end revenue to 59.2%.

Clearly, regardless of whether pursuing a broad layout or a highly focused strategy, the most important principle is to act within one’s means; meanwhile, B2B represents a crucial revenue stream for digital therapeutics companies with limited income.

Judging from the current performance of several publicly listed digital therapeutics companies, even in relatively mature overseas markets, these enterprises still lack sufficient commercialization capabilities and face significant revenue challenges. A slight misstep in strategy could lead to failure. This indicates that digital therapeutics remains in its early stages, and the market still requires cultivation. Both companies and investors need considerable patience to await further market maturity.

Of course, it is undeniable that digital therapeutics (DTx) have their own advantages, such as stable output (more stable than manual output), lower costs (zero marginal cost), and more convenient real-world data collection (using the product itself provides feedback data). These are unique value creations of digital therapeutics, which cannot be replaced by drugs or devices. This also means that digital therapeutics still have huge development space.

VCBeat will continue to closely monitor developments in this field and deliver the latest first-hand reports.