Amid Mass Exodus of 5,746 Chip Firms, Hearing Aid Chip Sector Emerges as a Hotspot for Strategic Investment and Innovation

In 2022, 5,746 chip manufacturers collectively “disappeared.”

The dataset released by Qichacha has immediately drawn attention from both within and outside the industry to the chip sector. Discussions such as “the bubble in the chip market has burst,” “the chip industry is collectively entering a winter,” “chips are inevitably subject to cyclical downturns,” and “chip projects are increasingly difficult to divest” have been pervasive. However, the hearing aid chip segment stands out as an exception.

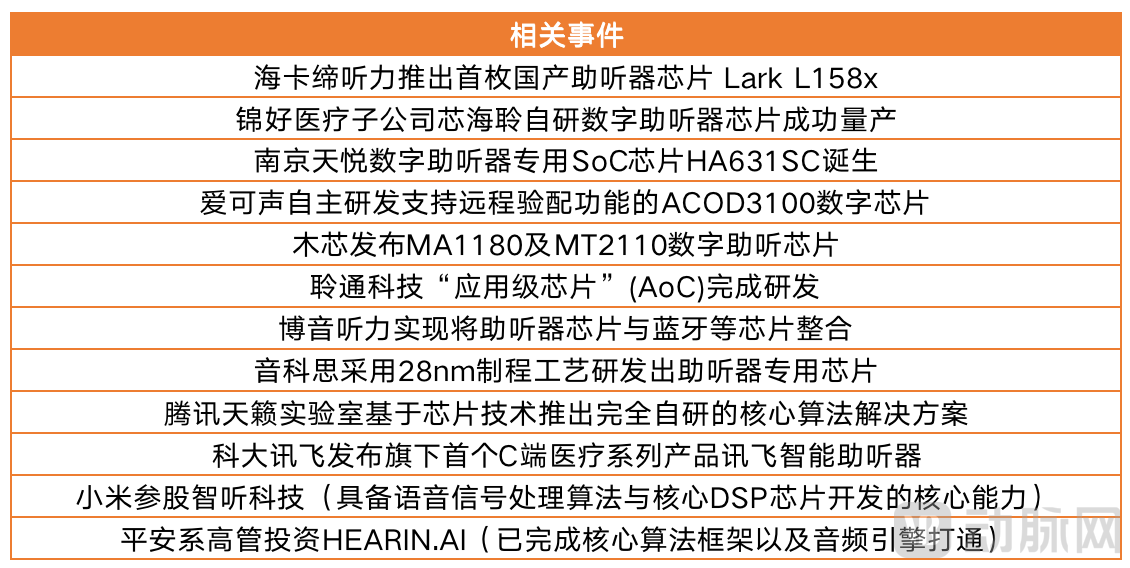

In recent years, not only have most domestic manufacturers, such as Nanjing Tianyue, Haikadi, Aikesound, and Xinshailing, raced to break through hearing aid chip technology and bring products to market, but emerging tech companies like Tencent, Xiaomi, and iFlytek have also continued to exert significant efforts in the hearing aid sector.

In 2022 alone, digital hearing aid smart chips such as Tianyue HA631SC, Haikadi Lark L158x, Aikesound ACOD3100, Muxin MA1180, and MT2110 were successively launched. Tencent’s Tianlai Laboratory and iFlytek have also rolled out related solutions, while executives from the Ping An group and Xiaomi have strategically entered the hearing aid market through investments.

As demand for hearing aids continues to surge, the industry has reached a critical inflection point in its upward trajectory. Chips have clearly become a key strategic high ground that most domestic Chinese manufacturers are rushing to secure. But the question remains: why are the majority of domestic Chinese hearing aid manufacturers choosing to tackle the technical challenges associated with chip development? And as opportunities begin to emerge, how should companies pivot their strategies?

Digital chips and speakers account for 50%-80% of the total device cost.

From a market perspective, the hearing aid market has long been monopolized by imports.The world’s top five hearing care groups—WS Audiology, Sonova Group, W.D.H Hearing Group, GN ReSound Group, and Starkey Hearing Technologies—account for more than 90% of the global hearing aid market.

Meanwhile, the world’s five largest hearing care groups have established formidable entry barriers in the premium hearing aid market through their offline fitting channels, high-end product supply chains, and proprietary R&D systems. Historically, control over key technologies—including related chip technology, fitting software, and market positioning—has been held by foreign companies. In China, there is a shortage of technical expertise among chip R&D personnel, and the development of the critical hearing aid industry chain remains relatively backward, with most domestic players engaged primarily in assembly and contract manufacturing, lacking core competitiveness.

Chen Chirong, founder of Lingtong Technology, told VCBeat: “The hearing aid industry is technology-driven, requiring core technologies and functionalities to attract users. Algorithms and chips are the key enablers. The five major overseas hearing aid manufacturers all develop their own algorithms and chips in-house, which constitute their core competitive barriers and represent the strategic entry point for technological R&D in China.”

In fact, one of the keys to resolving industry pain points lies in breakthroughs in chip technology.It serves as the foundational technology for hearing aids, enhancing enterprises' risk resilience. It is also key to breaking the current monopoly, providing support for future hearing aid development, and reducing production costs.

“A hearing aid can sell for 1,000 yuan, 20,000 yuan, or even 50,000 yuan; the most critical difference lies in the chip.”As competition intensifies in the future, or when the five major platforms engage in price wars, having higher costs with comparable performance will place you in a highly disadvantageous position. Therefore, from a cost perspective, breakthroughs in core technologies are critically important.“Domestic manufacturers must possess their own core competitiveness to build a moat for future development,” said a practitioner in the hearing aid industry.

The strategy of purchasing core components such as application-grade chips at high prices and then investing heavily in market sales to rapidly gain market entry is no longer viable. Only by controlling the price of digital hearing aids can we challenge the monopoly of high-priced overseas products while leaving sufficient profit margins for all links in the industry chain.

According to Jinhao Medical’s prospectus, although the cost proportions of digital chips and speakers vary across different digital hearing aid products due to differences in features and specifications, the combined cost share of digital chips and speakers in overall digital hearing aids ranges from 50% to 80%, with the average unit price of digital signal processing chips exceeding RMB 60.

The company’s self-developed digital chips not only build its core competitiveness but also significantly reduce the cost of digital processing chips. As the cost of core raw materials decreases, the company’s digital hearing aid products featuring in-house chips will offer a more compelling price-to-performance ratio, enabling them to compete effectively with similarly priced products in the same market. Only by breaking through the core technologies of hearing aids and achieving localization—from chips, receivers, and microphones to panels and even casing materials—can product costs be reduced, thereby freeing hearing aids from their historically prohibitive pricing. This will further enhance product performance, better tailor offerings to the Chinese market’s needs, and ultimately secure a strong position in the hearing aid industry.

It is precisely for this reason that, in recent years, most companies have gradually shifted their focus to the research and development of hearing aid chip technologies, aiming to rapidly capture market share.

Chips are the foundation of personalization, intelligence, and OTC availability.

Generally,User awareness, purchasing power, as well as product channels and services are typically key factors determining whether individuals with hearing loss proactively choose to wear hearing aids. However, the historically high prices of hearing aid products and the complex processes involved in hearing care services have effectively barred most individuals with hearing loss from accessing them.

Individuals with hearing impairment not only need to make multiple trips between the fitting center and their homes for hearing aid fittings after purchase, but also require offline specialty stores for repairs and routine maintenance based on their needs, making the process quite cumbersome. This is also a leading cause ofKey Reasons for the Decline in Hearing Aid Adoption Among Individuals with Mild Hearing Loss。

In the future, with the growing awareness of self-purchase among individuals with hearing impairment and the deepening of non-traditional sales channels for hearing aids,The traditional offline hearing aid fitting business model will be disrupted, with new online sales channels or offline direct-to-consumer channels becoming the trend.Effectively address the issue of hearing-impaired patients being unable to use hearing aids due to high unit prices and complex purchasing processes.

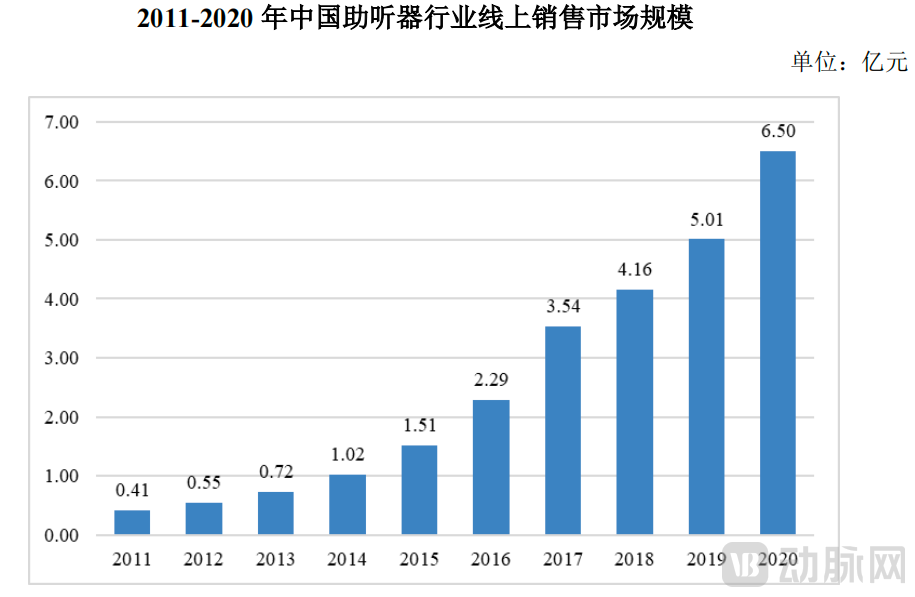

Data further corroborates this development trend. Based on online hearing aid sales data in China, the sector has experienced rapid growth from 2015 to the present. In 2020, the total value of online hearing aid sales in China reached RMB 650 million, representing a 29.90% increase compared to 2019.

Online Sales Market Size of China's Hearing Aid Industry, 2011–2020

Data Source: Zhiyan Consulting, “Research Report on the Market Operation Pattern and Strategic Consultation of China’s Hearing Aid Industry (2021-2027)”

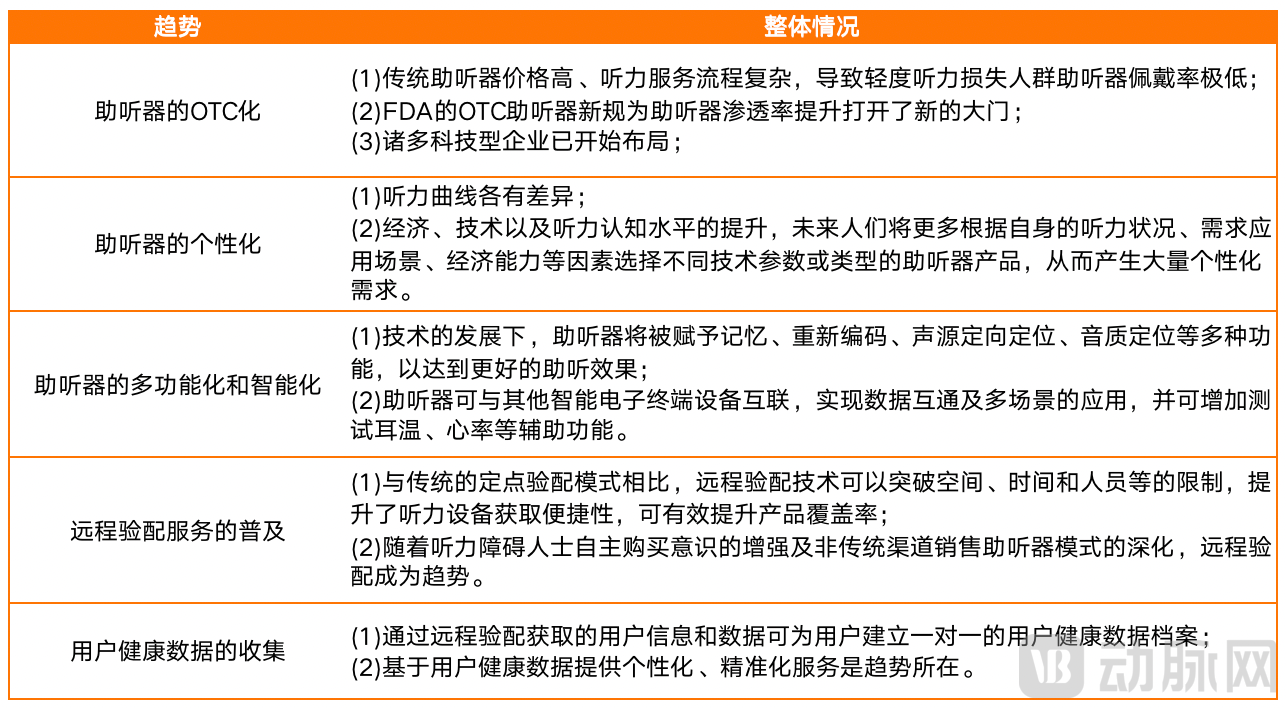

Meanwhile, the future trends in the hearing aid industry include over-the-counter (OTC) availability, personalization, multifunctionality, and intelligence, as well as the widespread adoption of remote fitting services and the collection of user health data.The implementation of core technologies, such as chips and algorithms, not only further facilitates the deployment of remote fitting but also serves as the foundation for enhancing hearing aid quality, meeting the industry’s demands for personalization, multifunctionality, and intelligence, and enabling the development of hearing aids tailored to individual audiometric curves.

Future Development Trends of Hearing Aids

It is precisely for this reason that, as the foundation of online sales,Remote fitting has nearly become a standard R&D feature for domestic hearing aid manufacturers. As the core technology, chip technology is naturally a key focus of their R&D efforts.

Help enterprises take the lead in seizing new opportunities and capturing the mid- to low-end markets

From a market strategy perspective, domestic manufacturers must embrace innovative technologies at the earliest opportunity to swiftly seize emerging opportunities and compete with industry giants when new market trends arise., and the most critical factor is mastering underlying technologies such as chips and algorithms.

First, large companies are slow to pivot; industry leaders lack the rapid innovation capabilities and tolerance for error in single product lines that startups possess. To compete with international brands, small and medium-sized enterprises (SMEs) and new market entrants must develop their own unique characteristics. Product structures or relatively simple innovations are easily followed and imitated; to remain competitive, it is necessary to create original, differentiated features from the perspective of chips and algorithms.

Secondly, the five major hearing aid groups hold a significant advantage in the high-end hearing aid market. Their expansion into the mid- and low-end markets may instead undermine their premium brand positioning and brand premium, thereby eroding the price integrity of their existing high-end products. Small and medium-sized enterprises (SMEs) and new market entrants can focus on the mid- and low-end segments, achieving price reductions by mastering core technologies such as chip design. While breaking through in core technologies, they can also optimize their supply chains and concentrate on online e-commerce and offline non-fitted retail channels to develop more innovative hearing aids with superior cost-performance ratios, thereby further increasing product penetration rates.

It is evident that whether in terms of market demand, future development trends, or key market strategies, none can bypass the breakthrough in hearing aid chip technology.

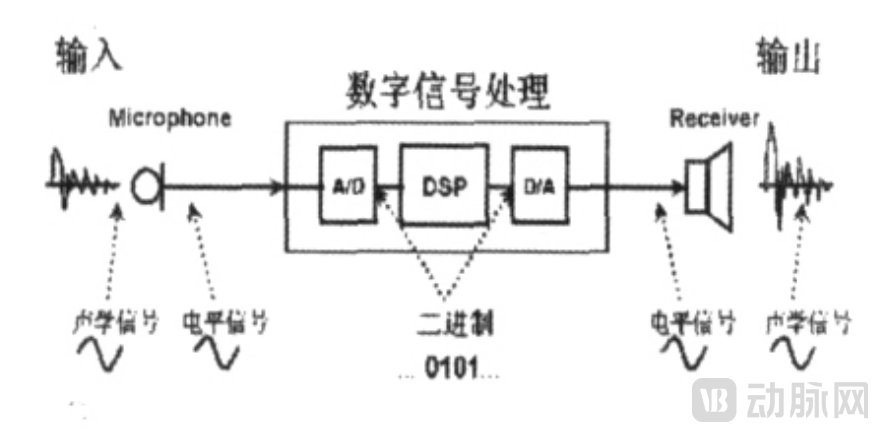

The digital signal processing module (DSP chip), as the most critical core component of digital hearing aids, has its processing capability that almost determines the quality of algorithms and the performance of the hearing aids. AndNoise reduction, compression, open-fit configuration, wireless technology, frequency lowering, directional technology, and feedback suppression are all integrated into this tiny chip.

Although digital hearing aids, like their analog counterparts, use microphones and speakers as energy transducers, DSP chips empower them with high signal-to-noise ratios, dynamic gain adjustment, and automatic environmental adaptation—features unattainable by traditional analog hearing aids. It was for this reason that the advent of the world’s first fully digital audio signal processing chip in 1998 propelled the development of hearing aids to unprecedented heights.

Basic Working Principle of Digital Hearing Aids

In the current hearing aid industry, leading global hearing aid brands independently conduct the research and development of hearing aid chips.Domestic hearing aid manufacturers, having started relatively late, rely primarily on chips supplied by companies such as ON Semiconductor and IntriCon Corporation in the United States. This dependence on hearing aid chip suppliers necessitates further breakthroughs to enhance corporate risk resilience.

In light of industry development trends and the iterative advancements in hearing aid technology, future hearing aid products will achieve increasingly higher precision in signal processing. The use of powerful software for hearing aid fitting and adjustment will become widespread. Feedback cancellation will increasingly focus on eliminating feedback without compromising sound amplification levels, while noise reduction capabilities will continue to strengthen. Meanwhile, hearing aid designs will become more miniaturized, with custom-fit hearing aids emerging as the preferred choice for users.To meet the above requirements, both chips and algorithms are indispensable.

How to Pivot?

Jiang Xianquan, Chairman and General Manager of BOIN Hearing, believes that in the past two years, the industry has focused on the integration of low-power Bluetooth functionality and professional hearing aid chip capabilities; however, power consumption and performance represent only the basic functions of a chip.Chip manufacturers must not only address the “bare-bones” hardware issue but also possess the capability for secondary chip development to achieve greater enhancements in hearing aid performance. R&D efforts should focus on improving performance in line with the needs of new consumers in the Chinese market, such as Bluetooth connectivity and vital sign monitoring, ultimately enabling the deployment of smarter and more personalized hearing aid devices in China.

MuXin Technology’s Chief Operating Officer, Xi Jinmiao, recently shared insights on “The Path to Breakthroughs for Domestically Produced Dedicated Chips” at the “Healthy Hearing Technology Forum,” summarizing the development direction into five key points:

First, addressing the challenge of going from 0 to 1;

Second, promptly customize products based on market feedback to meet customer needs, thereby achieving localized customization. Meanwhile, leverage local advantages to effectively enhance service efficiency;

Third, continue to collaborate with manufacturers on chip design;

Fourth, through local services and efficient application software (m-fit), we help customers rapidly achieve product realization from chip to final product;

Fifth, enhance the cost-effectiveness of products while developing more high-end offerings to meet market demand.

Yang Dongyi, Chairman of Nanjing Tianyue, believes that chips must incorporate algorithms, and that the requirements for computing power and power consumption in digital hearing aids will inevitably increase gradually in the future. Therefore, the key points to grasp in chip research and development are, first,Achieving a balance between computing power and low power consumption, with an algorithm-first approach—where chip algorithms precede chip architecture. The chip architecture and the chip itself are then designed based on the continuously decomposed requirements of hearing aid algorithms.

Based on the development trajectories of the five major global hearing aid groups, Starkey has currently launched multiple AI-powered product series, integrating artificial intelligence technology into its chips. These hearing devices feature body index tracking, brain index tracking, touch-controlled audio streaming, task reminders, and user-accessible analytics for monitoring hearing aid system performance. Furthermore, Starkey has introduced a customizable memory program for "Mask Mode," helping users better understand speech from individuals wearing masks.

By using the Starkey Thrive app, users can monitor their physical and brain health, customize personalized settings, and adjust their hearing aids. With the SoundCheck app, users can conduct hearing assessments on their smartphones, check ambient decibel levels in real time, and save assessment results and data. The collection of this data further facilitates future hearing tracking and communication with hearing healthcare professionals.

Starkey Thrive App

Monitor physical and brain health, perform personalized settings, and adjust hearing aids through the hearing aid.

Image source: Starkey official website

Starkey SoundCheck App

Conduct hearing assessments; measure ambient decibel levels; save hearing assessment results, etc.

Image source: Starkey official website

Last year, Signia, a hearing aid brand under the WS Audiology Group, showcased a range of hearing products and solutions at the China International Import Expo (CIIE). Its newly launched Phantom AX series hearing aids, powered by Signia’s Augmented Xperience (AX) platform with Holographic Beamforming technology, innovatively employ two independent processors to separately handle speech and environmental sounds, enabling users to achieve a three-dimensional speech recognition experience in various listening environments.

Sonova’s Phonak has recently launched the 7th-generation Naída Ultra-Power hearing aid, which features Phonak’s new-generation PRISM chip with twice the RAM of its predecessor. Building on this advancement, Phonak has also upgraded its sound processing system, next-generation AutoSense OS, and Dual-High Frequency Reshaping technology.

Under the W.D.H Hearing Group, Denmark’s Oticon has also achieved independent R&D and manufacturing of hearing aid-specific chips, developing the Velox™ platform chip technology. Building on this foundation, Oticon continuously iterates its product technologies, enabling features such as Opn™ BrainHearing technology, the 360° OpenSound Navigator system, and spatial sound source localization, with a particular focus on enhancing chip performance.

GN Hearing has also achieved in-house chip development. The company’s latest launch, ReSound ONE, represents an innovative upgrade achieved by combining its receiver system with a new sound processing chip featuring advanced Digital Feedback Suppression (DFS Ultra III). Meanwhile, the Linq Q introduces a new chip platform, enabling personalized device fitting and other capabilities.

An exploration of the five major overseas hearing care groups reveals that,“In-house chip development” is virtually a standard feature for hearing aid manufacturers.After all, this is the key to enabling enterprises to achieve iterative product upgrades, rapid innovation, and reduced product costs. Leveraging chip technology not only allows companies to swiftly capitalize on emerging trends in hearing aid development—such as remote fitting, personalization, and intelligence—but also further optimizes product performance, thereby building a corporate “moat.”

Despite years of development, the world’s five major hearing care groups naturally maintain a technological lead in their respective fields.However, while looking up at the “star-studded sky,” domestic hearing aid manufacturers are also gradually stepping forward, rapidly breaking through hearing aid chip technology and achieving independent research and development of products and core technologies.

For example, Haikadi’s Lark L158x has achieved dedicated hearing assistance, full integration, single-chip design, and ultra-low power consumption; BOIN Hearing has completed the R&D of multi-thought hearing aid algorithms and created the “CloudHear” platform, which encapsulates the cores of various manufacturers’ platforms and Bluetooth chips into a HYBRID solution; Lingtong Technology has completed the R&D of core hearing aid algorithms and performed algorithm integration and optimization on digital signal processing (DSP) chips; Nanjing Tianyue’s HA601SC adopts low-power design technology, an MCU+DSP multi-processor core architecture, and built-in multi-channel digital hearing aid audio processing algorithms, employing hardware-software co-design to ensure that audio processing algorithms operate with low power consumption and high efficiency; Aikesound’s ACOD3100 features EDNR environmental detection noise reduction technology and supports remote fitting and wireless transmission; Muxin Technology’s MT2110 can operate directly in zinc-air battery or lithium battery application scenarios without requiring external DC-DC converters or LDOs, and features low-power design, built-in sound effect mode adjustment, and dynamic volume compression; Xinshiling’s 32-channel dual-microphone digital hearing aid chip has been commercially deployed...

Tencent’s Tianlai Lab, iFlytek, Xiaomi, Skyworth, and other domestic innovators have also successively invested in the research and development of hearing aid devices. The current hearing aid market is witnessing a surge in momentum. In this process, beyond investments in chip and algorithm technologies, the choice of strategic pathway is most critical.

The report “Current Status and Development Trends of Hearing Health in China” indicates that the number of elderly people aged 65 and above, who constitute the main population with hearing impairment, has reached 120 million in China. However, the penetration rate of hearing aids in China is only about 5% (according to data from the Centers for Disease Control and Prevention), which is far lower than the over 30% penetration rate seen in developed countries such as the United States.

Although the hearing aid industry currently faces challenges such as the difficulty of breaking through core algorithms and the foreign monopoly on application-level chips, China’s market is sufficiently large. By selecting appropriate development paths, identifying diverse solutions, and ultimately resolving core technological issues, companies will certainly be able to upgrade and iterate hearing aid devices. This transformation will evolve them from purely medical devices into wearable devices that combine medical hearing assistance with consumer attributes, thereby successfully establishing a viable business model in the hearing aid sector.

Although Chinese hearing aid manufacturers started later, they have achieved significant breakthroughs in core technologies such as chips through independent R&D and multi-party collaborations. In this context, with the entry of companies like Tencent, iFlytek, and Skyworth, the industry will see an influx of interdisciplinary talent, bringing innovative perspectives that integrate insights from various sectors to hearing aid product development and driving the launch of diversified products.

Reference Article:

1. Development and Prospects of Digital Hearing Aids

2. 2022 Hearing Aid Industry Research Report