Fluorescence and 3D Endoscopy Drive Explosive Growth: Can Domestic Players Outpace Global Giants?

Olympus

Precision Machinery and Instrumentation R&D, Production, and Sales

The Low-Profile Endoscopy Market Is Experiencing Rapid Growth.

In the 2022 annual reports and Q1 2023 quarterly reports released by multiple domestic endoscopy companies, many reported growth rates exceeding 50%, outpacing several mature niche sectors.

In terms of performance, the combined endoscopy business revenue of four domestically listed endoscopy companies—SonoScape, Aohua Endoscopy, Haitai New Light, and Tiansong Medical—reached RMB 1.53 billion.Multiple companies sustained their growth into the first quarter. Haitai Optoelectronics reported Q1 operating revenue of RMB 148 million, a year-on-year increase of 58.76%. Sonoscape Medical’s endoscopic equipment revenue (flexible + rigid endoscopes) in Q1 2023 grew by 60% year on year.

From another perspective, the growth of the endoscopy industry can be intuitively gauged from the year-end bonuses of listed companies. According to Q1 quarterly reports and annual report data, Sonoscape Medical distributed approximately RMB 60 million in year-end bonuses alone in 2022. Aohua Endovision’s employee compensation payable increased by 74.43% year-on-year in 2022.

The endoscopy business of global giants has also delivered impressive performance. Olympus reported endoscopy-related revenue of JPY 461.5 billion (approximately USD 3.447 billion). Its revenue in the Chinese market amounted to roughly RMB 5 billion, and the company explicitly highlighted its optimistic outlook for growth in the Chinese market in its financial report.

Driven by both policy support and technological iteration, China’s endoscopy market is reaching a turning point of transformation. Based on annual report data, who has the opportunity to reshape the existing market landscape? What are the future market trends? VCBeat (WeChat ID: vcbeat) has conducted a comprehensive analysis.

Endoscopes are classified into two major categories: rigid endoscopes (e.g., laparoscopes, arthroscopes) and flexible endoscopes (e.g., gastroscopes, colonoscopes).

Let us first examine the rigid endoscope market. In 2024, the market size of rigid endoscopes in China is expected to exceed RMB 10 billion. The domestic rigid endoscope market is dominated by Japan’s Olympus, Germany’s Karl Storz, and the U.S.’s Stryker, which together account for over 90% of the market share. Domestic companies such as Sonoscape Medical, Tiansong Medical, and Shenyang Shenda Endoscope hold a certain portion of the market.

In recent years, multiple leading medical device companies have entered the rigid endoscope market, including Mindray from the patient monitoring sector and Kangji Medical from the minimally invasive surgical instruments sector, resulting in fierce competition in China's rigid endoscope market.New entrants have generally achieved high growth from a small base. According to Mindray’s 2022 annual report, its rigid endoscopy system grew by over 90%. Kangji Medical’s 4K medical endoscopic camera system generated RMB 20.56 million in revenue, representing a year-on-year increase of 233.4%.

However, in the rigid endoscope market, the domestic company with the strongest annual revenue performance is not one that holds a certain share of the end-user market, but rather AOT Optics, which serves as an OEM supplier for the global giant Stryker in the upstream segment.

In 2015, Stryker launched its fluorescence endoscopy system, capable of imaging specific tissues, which rapidly achieved high growth in the North American market. Leveraging this technology, Stryker reclaimed its leading position in the endoscopy sector, capturing over 70% of the global fluorescence endoscopy market share.

Stryker’s endoscopy business generated $2.423 billion in revenue in fiscal year 2022, a year-over-year increase of 13.2%.

Haitai XinGuang, a company listed on China’s STAR Market and a core supplier of Stryker’s fluorescence laparoscopes, has likewise benefited from the rapid growth of the fluorescence endoscopy market.

Haitai XinGuang reported revenue of RMB 480 million in 2022, a year-on-year increase of 53.97%. Among this, medical endoscopes achieved even higher growth, with revenue reaching RMB 360 million, up 60.78% from the previous year, accounting for 76.90% of total operating revenue. This strong growth momentum continued into the first quarter of this year, as Haitai XinGuang’s Q1 operating revenue reached RMB 148 million, representing a year-on-year increase of 58.76%.

As fluorescence endoscopy expands from the North American market to emerging markets, fluorescence-guided surgical procedures are gradually extending beyond abdominal surgery to other specialties, including urology and gynecology. Driven by these two major factors, the fluorescence endoscopy market is experiencing rapid growth, enabling Haitai Xin Guang, a contract manufacturer of fluorescence endoscopes for Stryker, to achieve a growth rate higher than that of Stryker.

In the rigid endoscope market, another technology experiencing rapid commercial scale-up is 3D endoscopy.Olympus is the driving force behind this technology. According to Olympus’s annual report, its laparoscopic business is primarily driven by the VISERA ELITE II 3D imaging system.

The advantage of 3D technology lies in its ability to recreate a three-dimensional surgical field that mirrors real-world vision. Although this technology emerged relatively early, its commercial performance has been lacking. With the commercial viability of 3D endoscopes now validated, 3D technology is poised to drive market growth.

Where Are the Growth Points in the Future Rigid Endoscope Market?

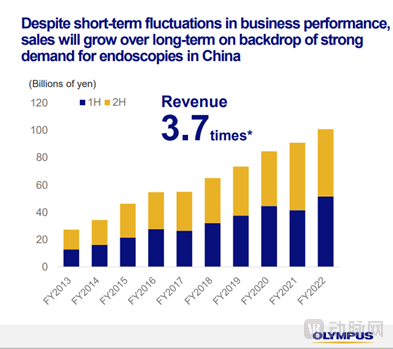

In terms of market structure, industry giants are optimistic about the growth of China's primary care hospital market.Olympus believes that, in accordance with the Work Plan for Comprehensively Enhancing the Comprehensive Capabilities of County-Level Hospitals issued by the National Health Commission in 2019, demand for surgical equipment in secondary hospitals will increase significantly. In light of this trend, Olympus will intensify its development efforts targeting China’s 7,900 secondary hospitals. Regarding its competitive advantages in the Chinese market, Olympus considers its greatest strength to be the trust it has built over many years in China.

Olympus China Market Revenue Changes

From the perspective of product development trends, endoscopic imaging is becoming increasingly high-definition and three-dimensional. Meanwhile, the integration of endoscopic imaging technologies has emerged as a prevailing trend.Building on traditional endoscopic technology, the integration of other imaging modalities—such as ultrasound, optical coherence tomography (OCT), fluorescence, and confocal microscopy—to create novel hybrid endoscopy products has become a key development trend. Domestic companies are accelerating the launch of integrated 3D, 4K, and fluorescence endoscopy systems.

Turning to the flexible endoscope market, driven by the widespread adoption of early gastrointestinal cancer screening, the introduction of novel endoscopic techniques, and the continuous rollout of policies such as tiered diagnosis and treatment, new healthcare infrastructure development, and enhanced service capabilities at primary care hospitals, the domestic flexible endoscope market has maintained a high growth rate, outpacing that of the rigid endoscope market.

However, the flexible endoscope market presents higher barriers to entry. Physicians require specialized training to master the use of flexible endoscopes, leading to greater product stickiness among trained users. Furthermore, as the processor units in flexible endoscopy systems are incompatible with scopes from other brands, market concentration is higher. Olympus, Fujifilm, and Pentax Medical dominate the domestic market, while Chinese-made flexible endoscopes hold a certain market share, with key players including Sonoscape Medical and Aohua Endoscopy.

In the field of flexible endoscopy, 4K is a key competitive factor. While 4K technology has already been widely adopted in the rigid endoscopy market, the flexible endoscopy market is just entering the 4K era.

Since flexible endoscopes are used for intraluminal imaging, they have lower resolution requirements compared to rigid endoscopes. Physicians place greater emphasis on practical performance characteristics during surgery, such as stability, maneuverability, insertability, flexibility, and shaft stiffness. Consequently, 4K flexible endoscopes have only begun to emerge in the global market in the past two years. In the flexible endoscope market, gastrointestinal endoscopes account for more than 65% of the share. Global companies are prioritizing the commercialization of 4K gastrointestinal endoscopes.

Since its global launch, the 4K flexible endoscope has achieved commercial validation.

Olympus is the leading company in the 4K gastrointestinal endoscopy market. Its 4K gastrointestinal endoscopy system, EVIS X1, launched in the U.S. market in 2020, has remained a primary driver of revenue growth two years after its release. Olympus also emphasized in its financial report that a key priority for the next fiscal year will be preparing for the commercial launch of the EVIS X1 system in the Chinese market.

Among domestic enterprises, Aohua Endoscopy launched its new-generation 4K ultra-high-definition endoscopy system, the AQ-300, in November 2022, becoming the first company in China to introduce a 4K flexible endoscope.

Although this product did not generate revenue for Aohua Endovision in 2022, the company considers it a key growth driver for 2023. In 2022, Aohua Endovision undertook extensive promotional efforts to introduce its 4K digestive endoscopy system into top-tier hospitals, resulting in a significant increase in expenses during the reporting period and a consequent decline in net profit.

In Q1 2023, Aohua Endoscopy’s AQ-300, its flagship product for high-end hospitals, already accounted for a significant proportion of orders and shipment volumes. In the first quarter of 2023, Aohua Endoscopy returned to a high-growth trajectory, reporting revenue of RMB 125.4868 million, a year-on-year increase of 53.77%. The net profit attributable to shareholders of the listed company amounted to RMB 15.6117 million, representing a year-on-year surge of 358.24%.

Based on the performance of 4K flexible endoscopes from Olympus and Aohua Endoscopy, the high-end market demonstrates strong acceptance of 4K digestive endoscopy products. In the future, 4K digestive endoscopes will become a key factor in competition within the high-end market.

In the primary healthcare hospital market, flexible endoscope growth is also substantial.

Sonoscape’s core market strengths lie primarily in secondary hospitals and below. In Q1 2023, Sonoscape’s installation volume in county-level hospitals and primary care facilities increased by 200% and 300% year-on-year, respectively, while installations in tertiary hospitals grew by 150% year-on-year. In 2022, Sonoscape generated RMB 610 million in revenue from its endoscopy business, representing a year-on-year increase of 34.70%. In Q1 2023, sales of endoscopy equipment (including both flexible and rigid endoscopes) rose by 60% year-on-year.

The primary product driving growth for Sonoscape Medical is the HD-550 series high-definition electronic endoscopy system. In terms of R&D layout, Sonoscape Medical’s strategy involves horizontal expansion of endoscope types (such as bronchoscopes, slim endoscopes, duodenoscopes, and endoscopic ultrasound scopes) and vertical enhancement of high-end endoscopic functionalities (such as optical zoom endoscopes and variable-stiffness endoscopes).

In the flexible endoscope market, the new growth driver is the disposable endoscope market.

In developed countries and regions overseas, the use of single-use endoscopes for diagnostic examinations of diseases in the gastrointestinal tract, respiratory tract, and urinary tract has been developing rapidly.Disposable endoscopic devices are consumables, significantly expanding the industry's market potential.

In the niche segment of single-use endoscopes, Boston Scientific has delivered impressive performance. In 2022, Boston Scientific reported net sales of $12.682 billion, a year-on-year increase of 6.7%. Of this, the endoscopy business generated net sales of $2.221 billion, up 3.7% year on year. The endoscopy business accounted for 17.5% of the company’s total revenue.

The primary product driving the growth of Boston Scientific’s endoscopy business is the EXALT™ Model B Single-Use Duodenoscope.Boston Scientific’s single-use duodenoscope, used for endoscopic retrograde cholangiopancreatography (ERCP), eliminates the risk of potential iatrogenic infections. Approximately 700,000 ERCP procedures are performed annually in the United States, with a global annual volume of around 1.5 million cases.

Previously, global endoscope manufacturers focused their single-use endoscope offerings on areas with lower requirements for image clarity and operational complexity, such as bronchoscopes and cystoscopes. Gastroscopes and colonoscopes demand higher image clarity, serve both diagnostic and therapeutic functions, and are closely evaluated by physicians for their performance.

Boston Scientific’s previously launched single-use endoscopes have primarily consisted of single-use bronchoscopes and single-use digital ureteroscope systems. How has Boston Scientific’s duodenoscope managed to stage a comeback despite intense competition from industry giants such as Olympus and Pentax? It has driven the industry’s shift from reusable endoscopes to single-use endoscopes.

Boston Scientific’s duodenoscope was launched in the U.S. market in 2019, with the key to its volume ramp-up being the company’s resolution of two major challenges five years after its initial launch.

First, the high cost of use is a major concern; adequate reimbursement is key to the adoption of any new technology. The per-procedure cost of single-use endoscopes is relatively high. Boston Scientific’s duodenoscope is positioned in the premium segment with a higher price point, which poses a barrier to physician adoption.

In the duodenoscope product category, Boston Scientific has collaborated with the U.S. Centers for Medicare & Medicaid Services (CMS), which has granted New Technology Add-on Payment (NTAP) status to the EXALT™ Model D Single-Use Duodenoscope. This CMS decision strengthens the incentives for hospitals and patients to adopt single-use endoscopes.

Secondly, it lowers the barriers for physicians to adopt single-use endoscopes. Boston Scientific’s duodenoscope offers physician-friendly clarity and ease of operation, requires no additional training, and meets clinical performance expectations.

Currently, single-use endoscopes have become a key focus area for major global players, with multiple Chinese companies also entering the market. Based on the development trajectory of Boston Scientific, reducing costs and enhancing performance are critical to breaking through the competitive landscape.

The Road for Domestic Endoscopes: A Long and Arduous Journey. Annual report data reveals that Chinese manufacturers are actively expanding their presence in both rigid and flexible endoscopy sectors, demonstrating impressive performance and holding the potential to reshape the market landscape. However, under the broader trend of import substitution, the domestic endoscopy industry is entering a critical period of market transformation. Who will break through? Who will secure influence over the industry’s direction? Only time will tell.