2023 White Paper on Mid-to-High-End Ophthalmic Equipment Industry: Surge in Ophthalmic Demand and Accelerating Domestic Substitution

The ophthalmology industry has become a key sector attracting capital attention.

A review of the financing history of domestic ophthalmology companies reveals that the number of financing events in the ophthalmology sector surged dramatically, rising from just 11 in 2015 to 34 in 2018. The trend peaked in 2021 with 45 deals and has since remained at a relatively high frequency.

From the perspective of funded companies, approximately 46% of financing events between 2015 and 2022 were concentrated in the field of ophthalmic device research and development.

The underlying reason is that most ophthalmic diseases cannot be cured with medication, which typically only serves to slow disease progression; therefore, the majority of patients prefer surgical intervention for definitive treatment. Furthermore, given the anatomical complexity of the eye, ophthalmic surgeries are highly dependent on specialized instruments. Consequently, ophthalmic devices play a more critical role in clinical ophthalmology than ophthalmic pharmaceuticals.Among these, the utilization and demand for ophthalmic equipment, particularly mid-to-high-end devices with higher technological sophistication, continue to rise.

After research by VCBeat,In the field of high-end ophthalmic equipment, optical coherence tomography (OCT), femtosecond laser systems, ophthalmic surgical microscopes, combined phacoemulsification and vitrectomy machines, fundus cameras (angiography), and optical biometers are receiving the most industry attention (listed in no particular order).These six major categories of high-end instruments and equipment (including consumables bundled with the equipment) each generate annual sales ranging from RMB 1 billion to tens of billions, indicating substantial market potential.

What is the current market landscape of the mid-to-high-end ophthalmic equipment industry? What progress have companies made? What emerging trends are evolving? To address these questions, VCBeat Research Institute dedicated six months to meticulously reviewing literature, extensively gathering data, and interviewing enterprises as well as frontline clinical experts, resulting in the “2023 White Paper on the Mid-to-High-End Ophthalmic Equipment Industry.” This report aims to provide readers with a more accurate, objective, and cutting-edge overview of China’s mid-to-high-end ophthalmic equipment market.

The following is the table of contents:

In China, the number of patients with ophthalmic diseases is substantial, affecting a broad population.

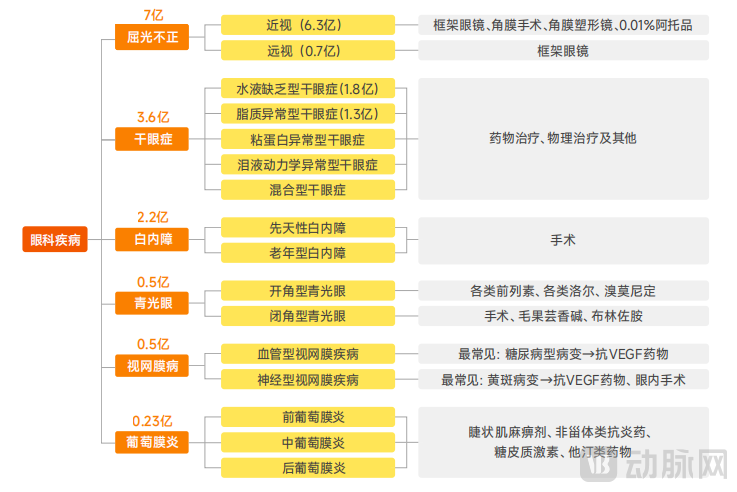

Based on data from the National Health Commission and the National Bureau of Statistics, it is estimated that in 2022, the number of patients with refractive errors in China exceeded 700 million, accounting for nearly 50% of the national population; the number of patients with dry eye disease approached 360 million, representing nearly 30% of the national population; and the number of patients with cataracts surpassed 220 million, with an incidence rate of 80% among individuals aged 60–89 years. Furthermore, although macular degeneration—a severe yet often overlooked fundus disease affecting middle-aged and elderly individuals—accounts for a relatively small proportion of the general population, it remains one of the top three causes of blindness worldwide. Given China’s vast population base, the current number of patients with this condition has reached nearly 30 million.

It is evident that as the prevalence of ophthalmic diseases continues to rise, more than half of the Chinese population is now affected by eye conditions, leading to a sustained increase in treatment demand.

Furthermore, the demand for ophthalmic diagnosis and treatment spans all age groups, covering conditions ranging from myopia in children to fundus diseases in the elderly, thereby encompassing the entire human life cycle.

Number of Patients with Various Ophthalmic Diseases

Number of Patients with Various Ophthalmic Diseases

Data sources: National Health Commission, public data; compiled by VCBeat.

A Blue Ocean of Demand Is Gradually Taking Shape: According to the China Health Statistics Yearbook, the number of admissions to specialized ophthalmology hospitals in China reached 2.374 million in 2021 (2022 data not yet released), with a compound annual growth rate (CAGR) of 15.35% over the past decade, indicating that a blue ocean of demand is gradually taking shape.

It is worth noting that from 2020 to 2022, diagnosis and treatment demand declined due to the impact of the pandemic. In 2023, following the lifting of pandemic restrictions, there was a rebound surge in the number of medical examinations, hospital admissions, and inpatient surgeries.

In the diagnosis and treatment of ophthalmic diseases, China has consistently maintained relatively low rates of diagnosis and treatment.

Behind this, on the demand side, the highly specialized and professional nature of ophthalmology has resulted in limited consumer awareness and attention to eye diseases; on the supply side, the development of domestic ophthalmic drugs and medical devices has long remained in its early stages, dominated by imports with relatively high prices, leading to insufficient penetration and affordability.

Moreover, despite the large patient population in China, the market size for ophthalmic devices and pharmaceuticals remains relatively small, with low penetration rates.

For instance, a 2019 Frost & Sullivan study comparing the prevalence of major ophthalmic diseases in China and the United States revealed that the number of patients with dry eye disease and uveitis in China was more than ten times that in the U.S. The number of patients with allergic conjunctivitis exceeded that in the U.S. by over 200 million, while the numbers of individuals with cataracts and myopia were each more than 100 million higher than those in the U.S. However, the market size for ophthalmic devices and pharmaceuticals in China was only one-eighth to one-fifth of that in the U.S., indicating insufficient breadth and depth of coverage for ophthalmic devices and drugs in China.

Notably, driven by the aging population and the trend of excessive screen time in China, the number of individuals with ophthalmic conditions is expected to continue rising. Meanwhile, as health awareness improves and more innovative devices and drugs become available, the penetration rate of ophthalmic treatments is poised for further growth.

In summary, the penetration rate of diagnosis and treatment in China's ophthalmology market is relatively low, indicating significant growth potential in the future.

Vast Growth Potential in the Ophthalmology Market: Driven by a large patient population with unmet needs, low market penetration, an accelerating aging process, and a trend toward younger onset of eye diseases, demand for ophthalmic medical services in China is steadily increasing.

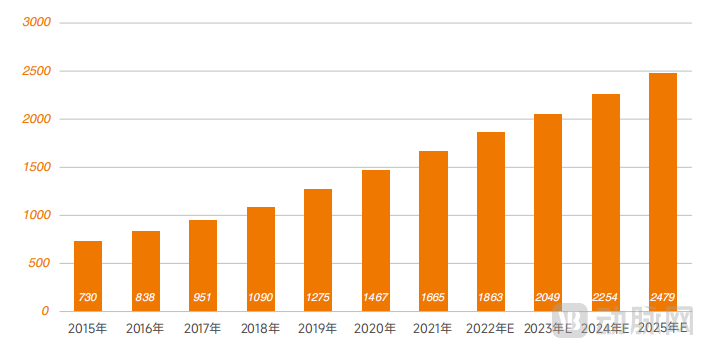

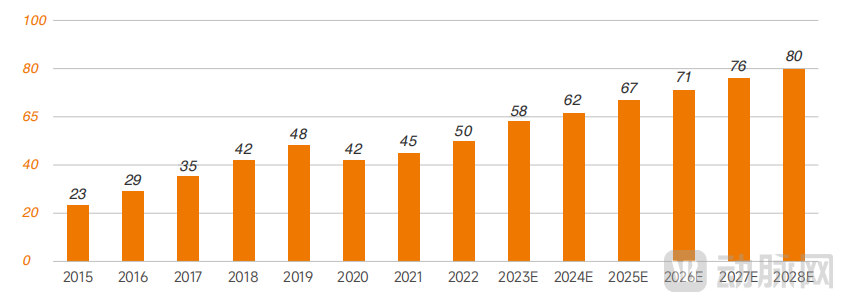

According to Frost & Sullivan data, the market size of China’s ophthalmic medical services was approximately RMB 186.3 billion in 2022. In terms of growth rate, the period from 2020 to 2022 was significantly affected by the COVID-19 pandemic, rendering its reference value for the subsequent ophthalmic medical services market relatively limited. Therefore, using the market growth rate from 2015 to 2019 (CAGR = 15%) as a benchmark and applying a conservative compound annual growth rate (CAGR) of 10%, the market size is projected to reach RMB 247.9 billion by 2025, indicating substantial room for growth.

Trends in the Market Size of Ophthalmic Medical Services in China (Unit: RMB 100 million)

Trends in the Market Size of Ophthalmic Medical Services in China (Unit: RMB 100 million)

Data source: Frost & Sullivan, VCBeat

Overall, the Chinese ophthalmic medical services market demonstrates a high degree of certainty in its continued expansion.

The global ophthalmic device market is highly concentrated, with clear competitive advantages held by industry giants: An overview of the competitive landscape in the global ophthalmic device market reveals that major players such as Alcon, Bausch + Lomb, Zeiss, Johnson & Johnson, and Topcon possess significant competitive advantages, boasting comprehensive product portfolios and capturing the vast majority of market share. According to Evaluate MedTech, the top 10 companies are projected to account for approximately 96.1% of the total market share by 2024.

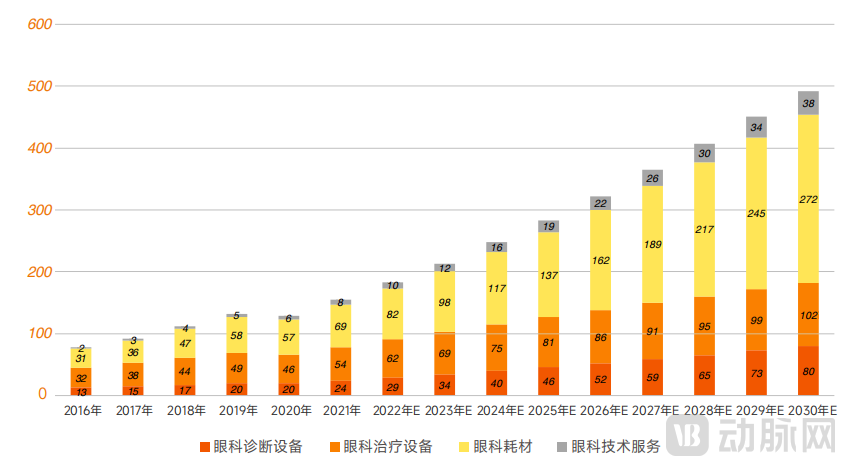

In terms of the market, according to Frost & Sullivan data, the market size of China's ophthalmic medical devices will exceed RMB 20 billion in 2023 (excluding contact lenses, orthokeratology lenses, etc.), among which ophthalmic diagnostic and therapeutic equipment accounts for the largest proportion, reaching 50.3%; ophthalmic consumables account for 44.5%; and ophthalmic technical services account for 5.2%.

This data indicates that the market size for ophthalmic instruments and equipment, which has received relatively low attention from the capital market, is actually quite substantial. However, due to the long-term monopoly by German and Japanese giants such as Zeiss and Topcon, domestic companies have maintained a weak presence in this field.

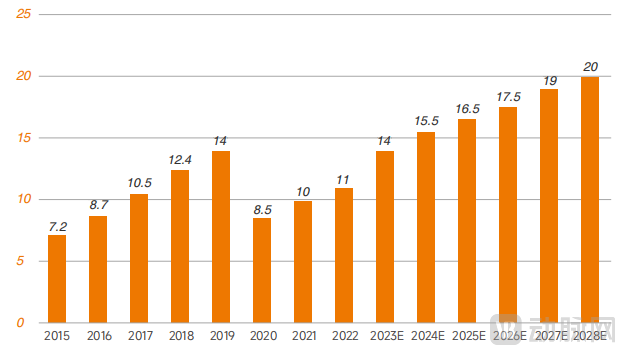

Over the next five years, ophthalmic medical devices will maintain a compound annual growth rate (CAGR) of 17%, with the market size expected to reach RMB 28.3 billion in 2025. From 2026 to 2030, the market is projected to grow at a rate of 12%, approaching RMB 50 billion by 2030.

Market Size of China's Ophthalmic Medical Device Industry, 2016–2030 (Unit: RMB 100 Million)

Market Size of China's Ophthalmic Medical Device Industry, 2016–2030 (Unit: RMB 100 Million)

Data Source: Frost & Sullivan. This table excludes contact lenses and their care solutions.

Facing a vast market, domestic innovative enterprises are accelerating technological and commercial breakthroughs, making import substitution promising.

OCT, short for Optical Coherence Tomography, is the "gold standard" in ophthalmic diagnosis. Applied in ophthalmology, OCT technology provides imaging that reveals retinal and choroidal lesions, facilitating the diagnosis of various eye diseases such as diabetic retinopathy and age-related macular degeneration.

In 2020, the number of ophthalmology outpatient visits in China reached 130 million. Among these, approximately 125 million were for individuals aged 65 and above, with over 40 million OCT examinations required annually.

However, China’s ophthalmic OCT market has long been dominated by imported brands. Prior to 2020, imported brands such as Zeiss, Heidelberg Engineering, Optovue, and Topcon accounted for more than 90% of the market share, with Zeiss and Heidelberg Engineering holding the largest portions. The localization rate was extremely low, indicating substantial potential for domestic substitution.

In recent years, a wave of domestic innovative enterprises has been established and entered the market, creating significant opportunities for the Chinese-made ophthalmic OCT sector. Among them, companies such as Bigway Medical, Moptim Medical, Swire Imaging, Topcon Medical (Note: "图湃" is likely Topcon or a specific brand like Tupai, but given the context of domestic brands, it refers to **Tupai Medical**), Weiren Medical, and Zhiding Medical have obtained certification from the National Medical Products Administration (NMPA) for their OCT products, marking their entry into the commercialization phase.

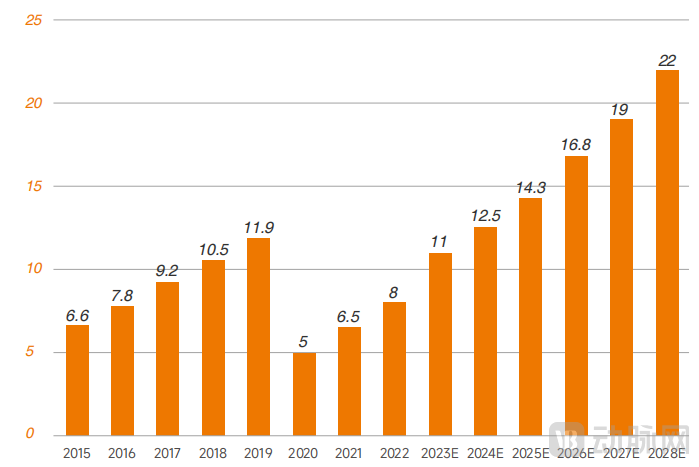

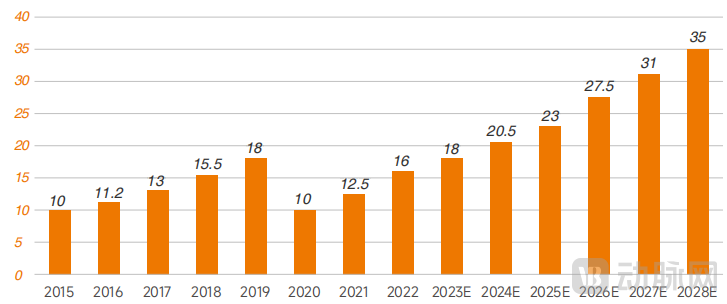

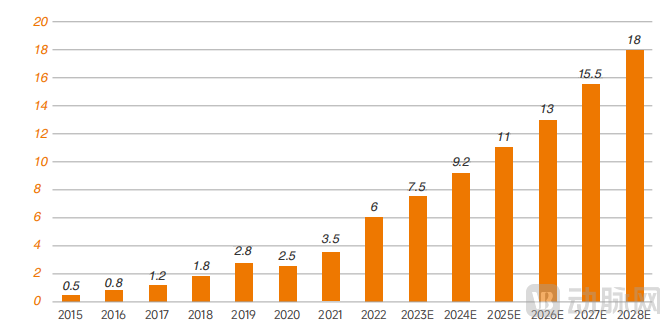

Driven by the rapid growth in demand for ophthalmic OCT products in China, the market sales scale of ophthalmic OCT continues to expand. Based on data disclosed by New Thinking Industry Research Center and through statistical analysis and calculations of public data from the National Centralized Procurement Network and various provincial centralized procurement networks, VCBeat has derived forecasts for the sales scale and growth trends of China’s ophthalmic OCT market.

Forecast of Sales Volume and Growth Trends in China's Ophthalmic OCT Market (Unit: 100 Million Yuan)

Forecast of Sales Volume and Growth Trends in China's Ophthalmic OCT Market (Unit: 100 Million Yuan)

Data Source: National and Provincial Procurement Websites

It is worth noting that from 2020 to 2022, the pace of industry expansion slowed due to the impact of the pandemic; however, demand was not suppressed but merely deferred.

Demand in recent years will be released in 2023. According to incomplete statistics, the number of ophthalmic OCT products listed in procurement bids during the first quarter of 2023 increased by 40% year-on-year, basically returning to pre-pandemic (2019) levels. Based on this projection, sales revenue for ophthalmic OCT products in 2023 is expected to exceed RMB 1.1 billion, essentially recovering to 2019 levels.

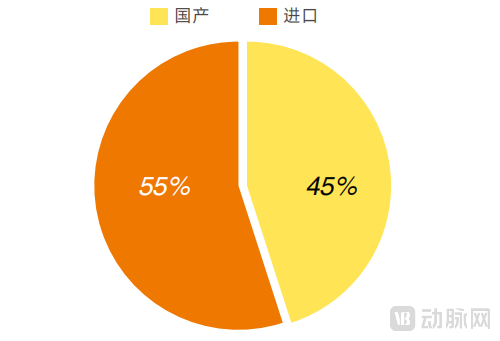

According to research by VCBeat Institute, a total of 485 OCT devices were awarded bids in public hospitals listed on government procurement platforms (including the national and provincial-level procurement websites) in 2022. Among these, 209 units were from domestic brands, 258 from imported brands, and the remaining 18 could not be traced. Of the 467 traceable ophthalmic OCT products, domestic brands accounted for 45%, approaching half of the market share, indicating a clear trend of domestic substitution.

Market Share of Domestically Produced OCT Devices Sold via Online Procurement Platforms in 2022

Data Source: National and Provincial Procurement Platforms

Among them, TopEye Medical has demonstrated particularly outstanding performance. In August 2021, TopEye Medical obtained registration certificates for two products: “BM-400K” and “YG-100K” (namely, Beiming and Yaoguang). In 2022, its first full year of sales, TopEye Medical secured bids for 79 units in public hospitals, achieving a 17% market share in sales and positioning itself as an industry leader. From January to April 2023, the hospital-end sales revenue of TopEye Medical’s ophthalmic OCT products reached nearly RMB 100 million, with a year-on-year sales growth rate exceeding 150%, thereby reshaping the competitive landscape of the sector.

In the future, the market size of ophthalmic OCT will consist of two parts: replacement of existing units and new purchases. Combining the replacement market with the incremental market, it is estimated that by 2028, the annual sales volume of ophthalmic OCT equipment in China will reach 2,000 to 2,400 units, with annual terminal sales revenue reaching RMB 2 billion to 2.4 billion.

Ophthalmic Surgical Microscope: Primarily used in ophthalmic surgeries to magnify the surgical field and provide illumination, it is the most critical large-scale platform-based surgical equipment in ophthalmology.

Since nearly all ophthalmic surgeries must be performed under an ophthalmic surgical microscope, this equipment is hailed as the “aircraft carrier” of the ophthalmic medical device sector, with individual unit prices ranging from hundreds of thousands to millions of yuan. For the past several decades, the market for ophthalmic surgical microscopes has been monopolized by German optical manufacturing giants such as Zeiss and Leica.

There is a significant gap in actual performance between domestically produced ophthalmic surgical microscopes and the aforementioned imported products. According to a survey of winning bid data from public hospitals, the market share of domestic products in this field is virtually negligible.

According to research conducted by VCBeat, among ophthalmic surgical microscopes listed on the public hospital procurement platforms (specifically the Zhejiang Provincial and Guangdong Provincial Procurement Networks) in 2021 and 2022, Zhejiang and Guangdong provinces recorded sales of 38 and 52 units, respectively. The total winning bid amounts were approximately RMB 60 million and RMB 80 million, respectively, representing a year-on-year increase of over 25%. Such robust growth during the pandemic underscores the clear status of these devices as essential medical necessities.

China’s Ophthalmic Surgical Microscope Market: Sales Scale and Growth Trend Forecast (Unit: RMB 100 Million)

China’s Ophthalmic Surgical Microscope Market: Sales Scale and Growth Trend Forecast (Unit: RMB 100 Million)

Data Source: National and Provincial Tendering and Procurement Websites

It is estimated (see the report for details on the estimation model) that by 2028, the annual market sales volume of ophthalmic surgical microscopes in China will reach RMB 3.5 billion.

Small Incision Lenticule Extraction (SMILE) is one of the most advanced corneal refractive surgical techniques worldwide. Unlike traditional procedures, SMILE does not require the creation of a corneal flap. Instead, it employs femtosecond laser photodisruption at two different depths within the corneal stroma to create an intrastromal lenticule, which is then extracted through a micro-incision measuring 3–4 mm.

Laser refractive surgery has undergone three technological iterations and is currently the mainstream approach for myopia treatment. Myopia surgeries can be categorized by surgical site into corneal refractive surgery, intraocular refractive surgery, and scleral refractive surgery. Currently, corneal refractive procedures are typically laser-based, primarily including femtosecond laser-assisted LASIK (FS-LASIK, "half-femtosecond"), transepithelial photorefractive keratectomy (TPRK, "all-laser excimer"), and small-incision lenticule extraction (SMILE, "full femtosecond").

VCBeat Institute selected the SMILE (Small Incision Lenticule Extraction) laser refractive surgery technology, which currently holds the largest market share among the aforementioned product technologies, for its research. Statistics show that in 2021 and 2022, seven and twelve SMILE laser devices, respectively, were sold through online bidding procurement in Zhejiang and Guangdong provinces. The unit price generally ranged from RMB 8 million to RMB 12 million, with total winning bid amounts reaching RMB 80 million and RMB 110 million, respectively; all were imported brands. However, as femtosecond laser equipment accounts for a higher proportion of sales in private hospitals compared to other categories of medical devices, we further referenced data published by Zeiss, which holds an absolute dominant position in this field, as a supplement.

According to data released by Zeiss, the number of VisuMax SMILE systems installed in China exceeded 300 units in May 2018 and surpassed 800 units by December 2022. This represents an average annual growth rate of approximately 110 units. Based on annual equipment sales of 110 units and annual consumable sales corresponding to 500,000 procedures, Zeiss’s annual sales volume for SMILE equipment and consumables amounts to approximately RMB 3.6 billion. The market size for femtosecond laser surgical equipment and consumables is projected to reach RMB 8 billion annually by 2028.

China's SMILE Laser Market: Sales Scale and Growth Trend Forecast (Unit: 100 Million Yuan)

China's SMILE Laser Market: Sales Scale and Growth Trend Forecast (Unit: 100 Million Yuan)

Data Sources: Bidding and procurement data posted on the Zhejiang and Guangdong provincial procurement platforms; Zeiss official website

As an ophthalmic ultrasound therapeutic device, the phacoemulsification and vitrectomy integrated system mainly consists of ultrasonic accessories, vitrectomy accessories, irrigation/aspiration accessories, the main unit, illumination accessories, and infusion/pressure accessories, serving as a critical tool for cataract and vitreoretinal surgeries.

From a historical perspective, vitrectomy surgery emerged in the 1970s and can be used to treat conditions such as retinal detachment, diabetic retinopathy, cataracts, endophthalmitis, and epiretinal membranes. The phacoemulsification-vitrectomy combined system is a critical piece of vitrectomy equipment; as the volume of vitrectomy procedures has increased, market demand for these integrated systems has been correspondingly unleashed.

The combined phacoemulsification and vitrectomy system has high technical barriers, with global suppliers predominantly consisting of European and American companies, including Alcon (USA), Geuder (Germany), and Bausch + Lomb (USA).

To meet the substantial domestic market demand, healthcare institutions at all levels have intensified their procurement of integrated phacoemulsification and vitrectomy systems in recent years. Currently, China’s demand for these integrated systems relies on imports, as no domestically manufactured devices are yet available on the market. In recent years, Chinese enterprises have also accelerated their research and development efforts in this field.

According to research by VCBeat, in 2021 and 2022, Zhejiang and Guangdong provinces sold 27 and 64 units of phacoemulsification and vitrectomy combination devices listed on public hospital procurement platforms (Zhejiang Provincial and Guangdong Provincial Procurement Networks), with total winning bid prices amounting to approximately RMB 25 million and RMB 58 million, respectively.

The consumables demand for vitrectomy is roughly aligned with its surgical volume, amounting to approximately 200,000–300,000 sets per year. Based on this, the sales market size for phacoemulsification-vitrectomy combined devices and their consumables in China was estimated at around RMB 1.1 billion in 2022. The annual market sales volume for these products is projected to reach RMB 2 billion by 2028.

Market Sales Scale and Growth Trend Forecast for China’s Combined Phacoemulsification and Vitrectomy Systems (Unit: RMB 100 Million)

Market Sales Scale and Growth Trend Forecast for China’s Combined Phacoemulsification and Vitrectomy Systems (Unit: RMB 100 Million)

Data Source: National and Provincial Tendering and Procurement Websites

Fundus cameras are the earliest clinical tool used for the assessment and detection of fundus diseases. The technology has evolved from initial standard 30°–50° posterior pole fundus photography, to later composite images from standard seven-field color fundus photography, and subsequently to wide-field fundus photography (WFP) and ultra-widefield fundus photography (UWFP). With each advancement, the capture range has expanded progressively, allowing for increasingly comprehensive observation of pathological lesions.

Over the past few decades, fundus cameras have been a critical tool in ophthalmic diagnosis and screening. The era of standard color fundus photography, characterized by low technical barriers, is gradually fading away, with ultra-widefield fundus imaging combined with angiography emerging as the dominant trend for the present and future.

The commercial ultra-widefield camera sector was pioneered by the UK-based company Optos, with Japanese and German manufacturers such as Nidek and Zeiss subsequently entering the market. In China, MicroClear Medical has launched its independently developed ultra-widefield camera products. Due to their strong performance and competitively priced offerings, the company has achieved rapid sales growth since 2021, delivering impressive market results.

According to research by VCBeat Institute, in 2021 and 2022, Zhejiang and Guangdong provinces respectively sold 20 and 40 units of ultra-widefield fundus cameras and angiography equipment listed on public hospital procurement platforms (Zhejiang Provincial and Guangdong Provincial Procurement Networks), with total winning bid prices amounting to approximately RMB 30 million and RMB 55 million, respectively. Such growth during the pandemic period indicates substantial market potential.

China’s Ultra-Widefield Fundus Camera Market: Sales Volume and Growth Trend Forecast (Unit: RMB 100 Million)

Data Source: National and Provincial Tendering and Procurement Websites

According to the prevailing industry consensus, ultra-widefield fundus cameras will gradually replace conventional color fundus photography. Consequently, cost-effective fundus camera products are poised to capture a broader market in lower-tier regions. The total market size for ultra-widefield fundus cameras is projected to reach approximately RMB 1.8 billion by 2028, achieving comprehensive substitution of conventional color fundus photography products.

Optical biometer is an instrument used in the field of clinical medicine, mainly for measuring axial length, corneal curvature, and intraocular lens power. It is widely applied in myopia prevention and control as well as in refractive cataract disease management.

High-end optical biometers were previously monopolized by imported brands such as the Zeiss Master series and the Tomey OA2000 series. In particular, the Zeiss Master 500/700 series products have secured an overwhelmingly dominant market share, making “Master” virtually synonymous with biometers.

According to research by VCBeat, in 2021 and 2022, a total of 46 and 72 units of optical biometers were sold through the public hospital procurement platforms (Zhejiang Provincial and Guangdong Provincial Procurement Networks) in Zhejiang and Guangdong provinces, respectively. The total winning bid amounts were approximately RMB 28 million and RMB 36 million, respectively, representing a 28% increase and indicating strong growth potential.

In the field of myopia prevention and control, the market potential for biometers in lower-tier markets is more extensive; however, the technological barriers and entry thresholds in this sector are relatively low, leading to intense price competition among domestic manufacturers.

According to incomplete statistics, in the field of myopia prevention and control, annual sales of optical biometers exceed 1,000 units, with a very rapid growth rate; future annual sales are expected to reach the order of tens of thousands.

For ophthalmic biometers, the high-end market in public hospitals remains dominated by imported products, presenting significant opportunities for domestic substitution.

In recent years, the state has introduced a series of policies to support the domestic substitution of medical devices. Some of these policies primarily aim to enhance the innovation capabilities of Chinese medical enterprises and focus on improving the quality and efficiency of medical device approvals, thereby laying the foundation for achieving domestic substitution.

Summary of Favorable Policies Related to Medical Equipment in China from 2016 to 2023

Source: Official Government Website

Driven by favorable national policies, the domestic substitution of mid-to-high-end ophthalmic equipment will continue to advance, enabling participating companies to capture greater market share and achieve more substantial growth.

Please scan the QR code below to get the full report for free.