Evolution of Surgical Robots: From Market Dominance to Fierce Competition

Ronovo

Minimally Invasive Surgical Robot Developer

Among the countless visions of the future world, robots have become an integral and important subset.

In industries such as manufacturing, agriculture, logistics, home services, and social networking, robotics has become a key technology for measuring industrial progress. In the healthcare sector, however, surgical robotics remains a relatively new technology and has not yet been widely adopted.

Over the past three decades of global development in surgical robotics, soft-tissue surgical robots represented by Intuitive Surgical’s da Vinci system have maintained a dominant and unparalleled market position. What transformations have surgical robots undergone? From the perspective of addressing clinical needs, is the product pathway exemplified by da Vinci truly the only viable option? This article explores the evolutionary history of surgical robots and reviews the innovative companies and products that have emerged both domestically and internationally.

——Introduction

In 1983, the concept of Minimally Invasive Surgery (MIS) was first proposed.[1]Compared with open surgery, minimally invasive surgery offers advantages such as reduced surgical trauma, less pain, minimal intraoperative bleeding, and faster postoperative recovery, making it favored by surgeons and patients alike.

However, with the gradual promotion and clinical application of minimally invasive surgery, surgeons have found that minimally invasive procedures, represented by various endoscopic techniques, place extremely high demands on surgical skills: In the absence of three-dimensional visual information and haptic feedback, surgeons must operate instruments for extended periods, requiring not only hand-eye coordination but also the ability to avoid tremors at the instrument tip caused by amplified hand shaking, as well as interference from the “chopstick effect” during surgery. These factors collectively increase the difficulty for open-surgery-trained surgeons in learning minimally invasive techniques.

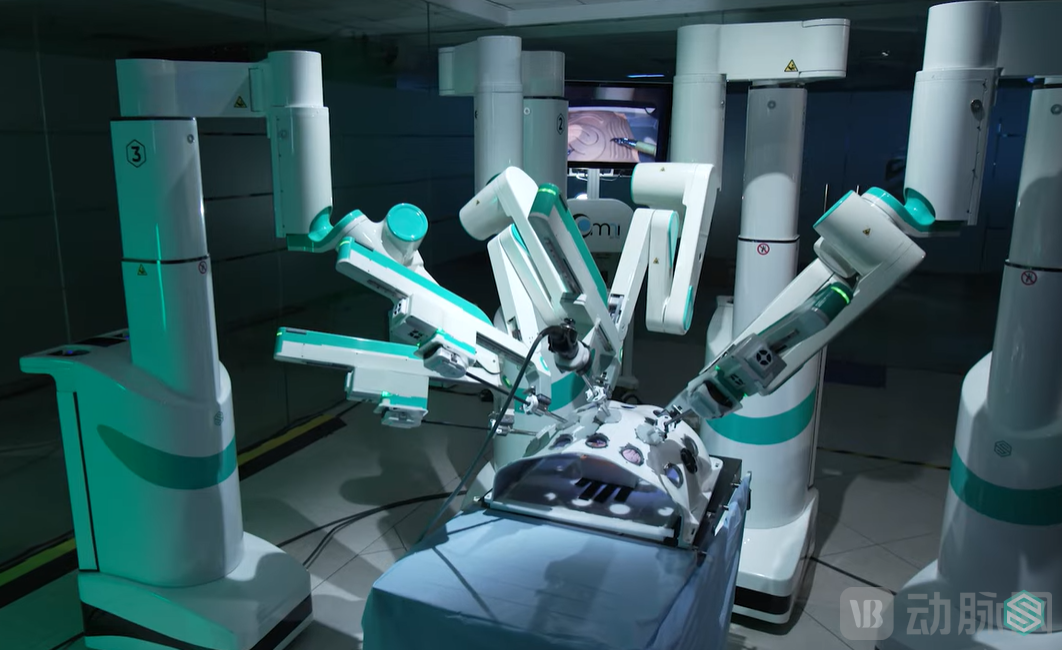

In 2000, the world’s first laparoscopic surgical robot, the Da Vinci Robot, was approved for market launch.[2], offering a novel technical pathway distinct from traditional laparoscopic minimally invasive surgery.

The da Vinci Surgical Robot Has Undergone Four Generations of Evolution

After 30 years of evolution across four generations, the da Vinci Surgical System offers numerous unique advantages over traditional laparoscopic surgical instruments:

1. High-Definition 3D Stereoscopic Vision System: Tissues within the field of view are magnified 10 times, presenting clear and realistic tissue details;

2. Master-slave control: Enables hand-eye coordination, eliminating the "chopstick effect" associated with traditional laparoscopic modes;

3. Tremor Filtration System: Significantly reduces tremors at the instrument tip;

4. Wristed Surgical Instruments: Surpassing the natural limits of the human hand, making high-difficulty surgical procedures such as suturing and knot-tying simple and easy to perform;

5. Motion Scaling: Enhances the precision of surgical instrument manipulation.

As the pioneer in the field of laparoscopic surgical robots, the da Vinci Surgical System has surpassed 7,500 installed units worldwide, with over 11 million robotic surgeries performed to date.[3]. Particularly in urological surgery, the penetration rate of robot-assisted radical prostatectomy (RARP) has exceeded 85%.[4], becoming the undisputed gold standard for surgical procedures in this disease category.

Designed by Freepik

The advent of surgical robots has enabled surgeons to perform procedures with greater flexibility and precision, while reducing intraoperative time. By alleviating the workload on physicians, these systems also lower the incidence of postoperative complications, leading to better prognoses for patients undergoing surgical treatment. If robotic surgery were to be widely adopted, it would have the potential to enhance hospitals’ surgical capabilities and bed turnover rates, thereby reducing the overall cost of disease management.

In China, laparoscopic surgical robots are included in the Class B management catalog for large-scale medical equipment. Their allocation is managed by provincial health administrative departments, which also issue allocation licenses. Other large-scale medical equipment under the same catalog includes medical imaging devices such as PET/MR and PET/CT.

Unlike the mature medical imaging equipment industry, China’s surgical robot industry is still in its infancy. As of the end of 2022, there were approximately 300 da Vinci surgical robots installed across China.[5], the installed base of domestically produced laparoscopic surgical robots remains negligible, which stands in stark contrast to the nearly 10,000 hospitals capable of performing minimally invasive surgeries, indicating a vast market potential.

Why Has China’s Surgical Robot Industry Lagged Behind Other Large-Scale Medical Devices? The Answer Lies in the Unique Demands of China’s Healthcare Market.

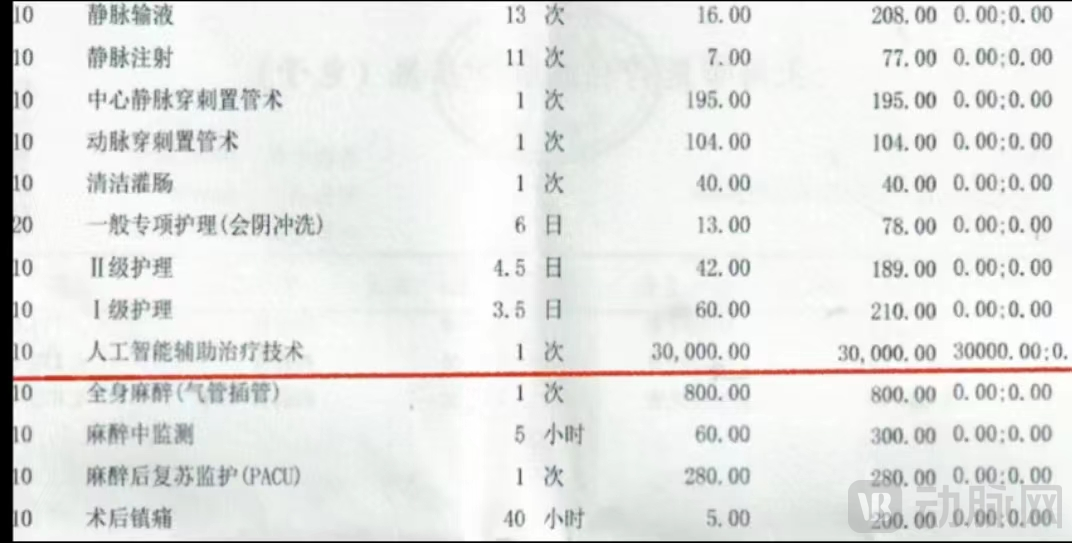

Currently, the vast majority of robot-assisted surgery (RAS) costs in China are borne by patients out-of-pocket, typically adopting a combined pricing model of “laparoscopic surgery fees + robotic system and accessory fees.”

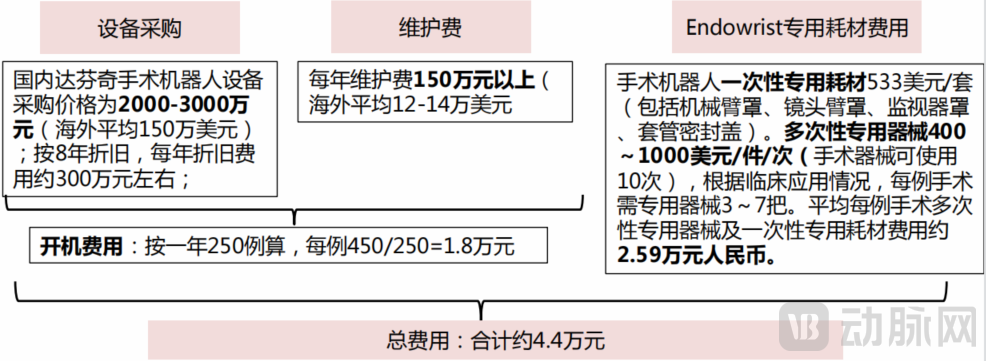

Typically, the procurement price of a da Vinci surgical robot for Chinese hospitals ranges from RMB 20 million to RMB 30 million, with additional costs for proprietary consumables and an average annual maintenance fee of RMB 1.5 million. These three components—equipment procurement, maintenance fees, and proprietary consumable costs—constitute the “robotic system and accessory expenses,” which are ultimately borne by patients.

Screenshot from Southwest Securities’ Special Report on Innovative Surgical Robots

According to estimates based on research data from Southwest Securities, the average “robotic equipment and accessory costs” per da Vinci surgical procedure amount to approximately RMB 44,000, of which the “system activation fee” accounts for RMB 18,000.

Taking robot-assisted radical prostatectomy (RARP) as an example, the cost of laparoscopic surgery is approximately RMB 40,000–50,000, with medical insurance covering around 50%. When the additional robot-related fee of RMB 44,000 is included, the financial burden on patients becomes substantial, thereby reducing their willingness to pay. If the costs associated with robot-assisted surgery (RAS) are not reduced, hospitals may face the awkward situation of having robotic systems but no patients. Naturally, hospitals carefully consider the return on investment when purchasing surgical robots, and the high costs of RAS undoubtedly raise the barrier to adopting these systems in healthcare institutions.

Xiaohongshu user @TuTuBuChiTu shares robotic surgery costs

Abroad, RAS costs are covered by health insurance in many regions.[6]; in China, the RAS procedure is not included in the medical insurance reimbursement catalogs of most provinces and municipalities.

In April 2021, Shanghai took the lead in including four robotic-assisted surgical procedures—radical prostatectomy, partial nephrectomy, total hysterectomy, and radical resection for rectal cancer—in its medical insurance reimbursement catalog.[7], with patients covering 20% of the cost, significantly improving the affordability of RAS.

In the long run, promoting the widespread adoption of currently approved and marketed surgical robots through medical insurance reimbursement is one possible pathway. However, this would undoubtedly increase the pressure on the national medical insurance fund, and it is highly challenging to achieve comprehensive coverage for all types of robotic surgery procedures across different regions. In economically developed first- and second-tier cities, the medical insurance fund can only cover a handful of common robotic surgeries; whereas in third- and fourth-tier cities with less developed economies, efforts to include robotic surgery costs in medical insurance coverage are even more difficult due to the high expenses involved.

In summary, the Chinese market fundamentally requires more inclusive and cost-effective surgical robot solutions.

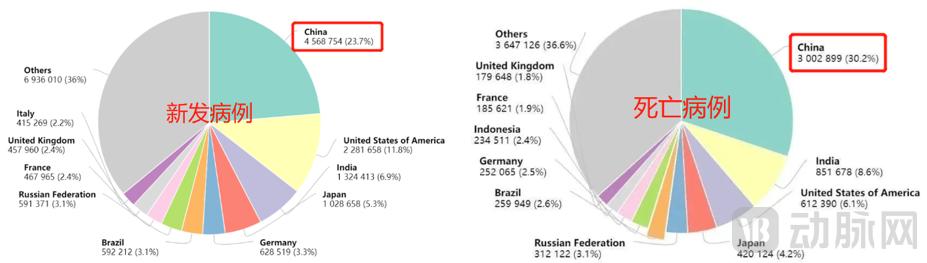

According to the “2022 National Cancer Report” released by the National Cancer Center, China recorded 4.57 million new cancer cases and 3 million cancer-related deaths in 2020, accounting for 23.7% and 30.2% of the global new and death cases, respectively. Both figures ranked highest worldwide and have shown a year-on-year increasing trend.

Screenshot from "2022 National Cancer Report"

Early detection, early intervention, and early treatment are the most effective measures for comprehensive cancer management. For early-stage tumors, radical resection is widely advocated in clinical practice, with postoperative cure rates reaching up to 90%. In cases of early-stage carcinoma in situ, adjuvant radiotherapy or chemotherapy is unnecessary after surgery, leading to a substantial increase in both five-year survival and cure rates.

The cancer surgical treatment market is vast, with strong demand for surgical interventions. The widespread adoption of RAS will inevitably require meeting the needs of multiple cancer types.Universal Applicability。

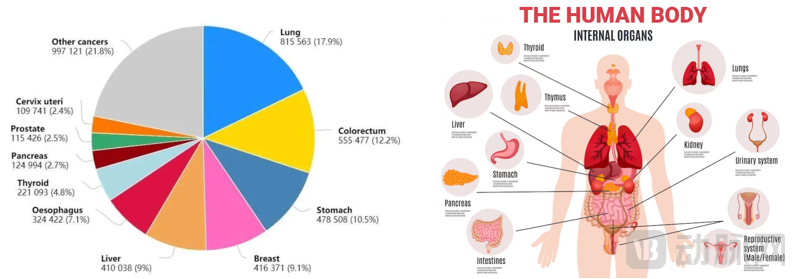

Among the new cancer cases in China in 2020, the following ten types accounted for 78% of the total: lung cancer, colorectal cancer, gastric cancer, breast cancer, liver cancer, esophageal cancer, thyroid cancer, pancreatic cancer, prostate cancer, and cervical cancer. Lung cancer ranked first with 820,000 new cases, followed by colorectal cancer, gastric cancer, breast cancer, and liver cancer (as shown in the figure below).

Screenshot from the “2022 National Cancer Report”; Designed by Freepik

Several types of cancer with high incidence in China share a common characteristic: the lesions at the site of carcinogenesis are relatively large. Surgical resection of early-stage tumors in these areas requires a larger operative field, posing certain technical challenges and risks.

The male prostate is comparable in size to a chestnut and is located within a confined surgical space. These characteristics leverage the advantages of surgical robots, represented by the da Vinci system, in performing delicate maneuvers in the deep pelvis, making robot-assisted radical prostatectomy (RARP) the surgical procedure with the highest penetration rate for surgical robots.

For large organs such as the stomach, liver, and breast, as well as the colorectum spanning the entire abdominal cavity, malignant tumor resection in these areas imposes higher demands on the multi-quadrant operational capabilities of surgical robots. Although existing commercialized surgical robots have undergone multiple iteration cycles, a comprehensive solution has yet to be found to address many factors that may affect the surgeon’s learning curve, procedural fluency, and surgical experience, such as minimizing intraoperative robotic arm collisions and avoiding repeated docking of robotic arms during surgery.

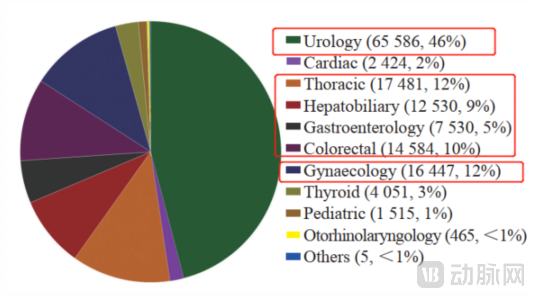

Clinical Surgical Composition of Endoscopic Surgical Robots in China (2019),Screenshot from Southwest Securities’ Special Report on Innovative Surgical Robot Devices

This represents a major bottleneck restricting the widespread adoption of existing surgical robots across multiple specialties. In China, there is a significant disparity in the penetration rates of robotic-assisted surgery (RAS) across different departments. Urology, represented by prostate cancer treatment, has the highest RAS penetration rate at 44%; thoracic surgery, exemplified by lung cancer treatment, has an RAS penetration rate of only 5%; while gynecology and general surgery, which account for 99% of minimally invasive soft-tissue procedures, have an RAS penetration rate of less than 1%.

Uneven development across specialties indicates that the market requires a broadly applicable, multi-specialty solution, with enhancing the multi-quadrant operational capabilities of robotic surgery being one of the key elements.

Surgeons are the direct operators of surgical procedures. Although robotic surgery has addressed issues such as hand-eye coordination and the “chopstick effect” inherent in traditional minimally invasive surgery (MIS), existing robotic systems, by employing novel port configurations and wristed instruments, have altered the operational habits associated with conventional laparoscopic surgery, making it difficult to leverage the surgical experience accumulated by laparoscopic surgeons.

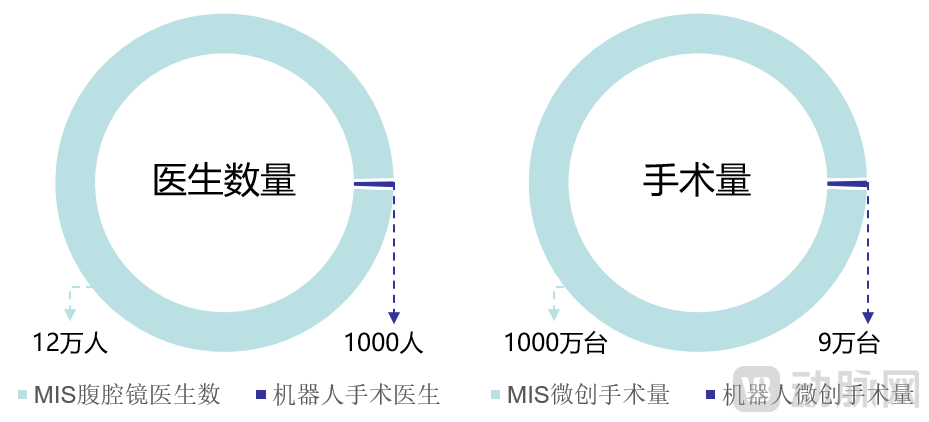

Currently, there are over 120,000 physicians in China performing traditional laparoscopic minimally invasive surgeries, yet fewer than 1% of these laparoscopic surgeons are formally trained and actively proficient in using the da Vinci Surgical System.

How to enable surgeons to sustain and enhance their expertise in conventional laparoscopic minimally invasive surgery, improve their operational experience, reduce the learning curve, and truly empower them with surgical robots constitutes a key consideration in the innovative design of surgical robotic systems.

It is evident that there remains a substantial unmet clinical need in the field of surgical robotics, necessitating novel solutions distinct from traditional laparoscopic surgical robot designs, with a strong orientation toward addressing clinical requirements.

The heavy burden of robotic surgery, uneven development across specialties, and the steep learning curve for physicians are not isolated issues in the Chinese market. As efforts to achieve widespread adoption of surgical robots advance, a growing consensus among industry experts holds that breakthrough innovations are needed to tap into untapped blue-ocean markets.

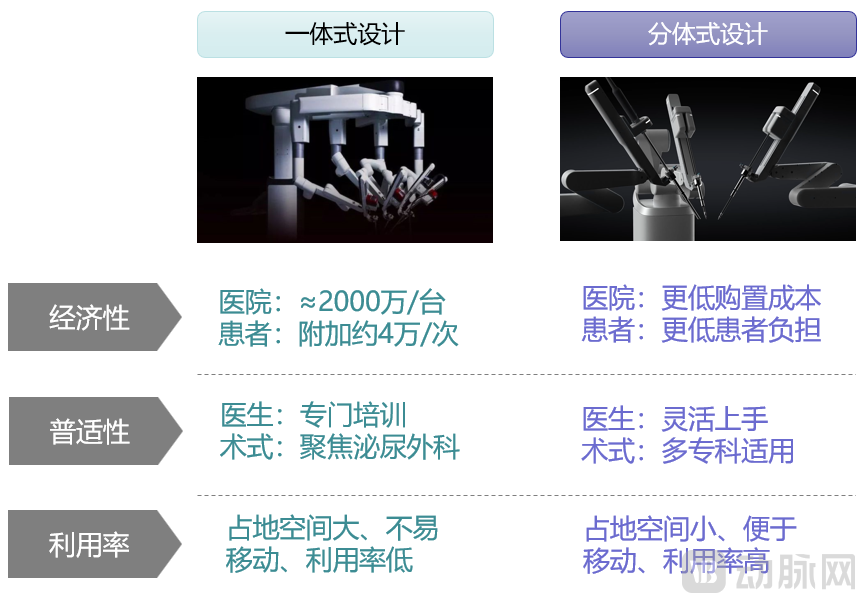

Taking the da Vinci surgical robotic system as an example, it consists of three components: the Vision Cart, the Patient Cart, and the Surgeon Console. The surgeon operates via the console, performing procedures on the patient based on the visual feedback of pathological tissues displayed by the Vision Cart. The robotic arms on the Patient Cart replicate the surgeon’s hand movements in real time to carry out surgical maneuvers.

Three Components of the Laparoscopic Surgical Robot (Screenshot from Intuitive Surgical’s Official Website)

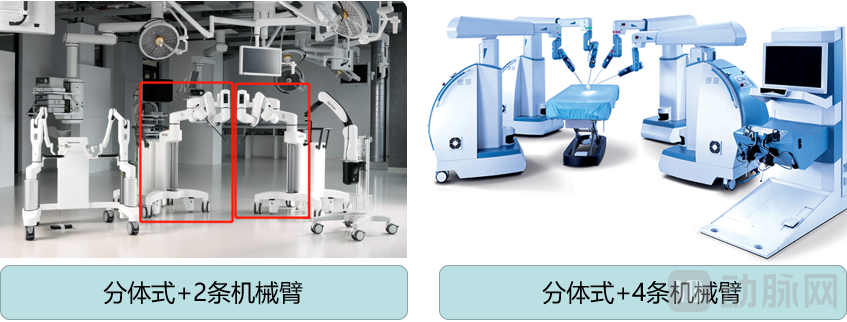

To expand multi-quadrant surgical capabilities, engineers have independently converged on the idea of distributing robotic arms—positioning them on both sides of the operating table to enhance system flexibility and degrees of freedom. Among these approaches, one design places the distributed robotic arms around the perimeter of the bedside in independent single-arm carts, known as “modular” surgical robots; another integrates the distributed robotic arms directly with the patient’s operating table, which we tentatively refer to as “table-integrated” surgical robots.

Different robotic arm configurations each possess distinct characteristics. To this end, we have summarized and organized several cutting-edge development trends of innovative laparoscopic surgical robots worldwide for the benefit of our readers.

Modular carts offer flexible mobility and customizable configurations, providing lower costs and broader surgical applicability compared to integrated designs. Surgeons can position different carts at various locations beside the operating table according to procedural requirements, significantly enhancing surgical flexibility and freedom. However, the key design challenge for modular surgical robots lies in enabling mutual localization among independent carts to determine their relative poses, which constitutes the fundamental core technology of modular robotic surgery.

Modular Surgical Robot (Screenshot from the company's official website)

Swiss medical device company Distalmotion has developed Dexter, a modular surgical robot comprising a surgeon’s console, two instrument arms on separate carts, and an endoscope control arm that can be mounted on either cart or directly clamped onto the patient’s operating table. Recently, the company completed a new funding round of approximately €140 million, led by Revival Healthcare Capital.

Four-Arm Modular Surgical RobotThe four-arm modular surgical robot preserves the traditional four-arm configuration of laparoscopic surgical robots, comprising three instrument arms and one endoscope control arm. Each of the four robotic arms is paired with its own independent modular cart. In theory, the number of carts in a modular design can be variable; hospitals may purchase different quantities of modular carts based on their actual needs. However, not every company developing modular surgical robots adopts this flexible cart configuration strategy.

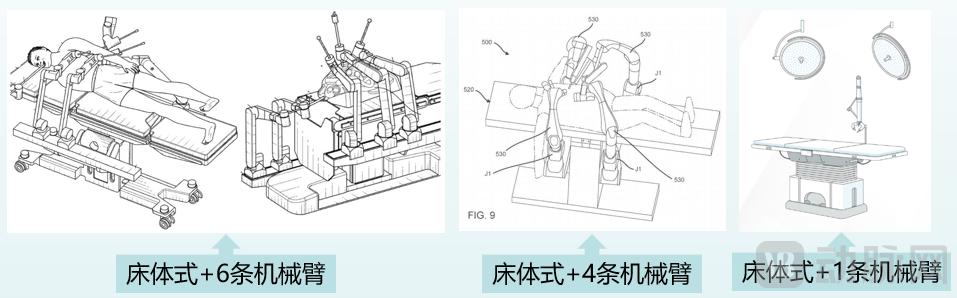

Distributing the robotic arms across the operating table creates a unique “bed-integrated” design. The advantage of this design is that it does not occupy any floor space in the operating room, thereby increasing available space and improving surgical workflow. However, since the robotic arm bases are connected to the hospital bed, they cannot be moved freely, resulting in obvious limitations.

Bedside Surgical Robot (Screenshot from Company Report)

Johnson & Johnson has a strong preference for bed-integrated designs. Two of its affiliated companies, Auris Health (acquired) and Verb Surgical (a joint venture with Google), have both developed laparoscopic surgical robots featuring this design. Specifically, Auris Health developed the Ottava surgical robot equipped with six robotic arms, while Verb Surgical created an “intelligent surgical platform” integrating four robotic arms into the operating table.

Single-port surgical robots also represent a major frontier in the exploration of laparoscopic surgical robotics. The most prominent advantage of single-port systems is reducing the number of incisions from the traditional three or four to just one. However, this comes at the cost of greater challenges in practical application: their use is largely confined to specific, narrow surgical specialties, and designs that deviate from conventional minimally invasive port placement habits result in a steeper learning curve for surgeons.

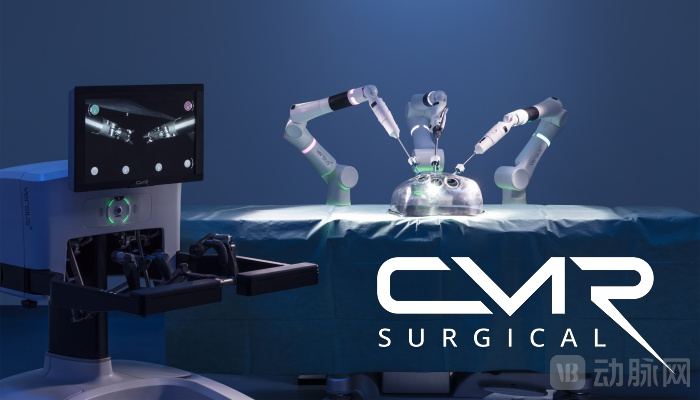

In March 2023, UK-based surgical robotics developer CMR Surgical announced that its self-developed Versius surgical robot had reached the milestone of completing 10,000 procedures.[8], becoming the first laparoscopic surgical robot to achieve successful commercialization after da Vinci.

Versius is a modular laparoscopic surgical robot (as shown in the figure below), comprising four independent robotic arm carts. The robot received EU CE certification in 2019 and has subsequently been approved for market launch in more than 20 countries and regions, including Australia, India, and the Middle East.

With 10,000 completed surgeries spanning 130 procedures across seven specialties—including colectomy, hysterectomy, hernia repair, and lobectomy—the company aims to surpass 1,000 installed units of the Versius surgical robot by 2025.

Versius Surgical Robot (Screenshot from the company's official website)

In the field of laparoscopic surgical robots, researchers and clinical experts have conducted extensive cutting-edge exploration and innovative attempts to continuously enhance the performance and efficiency of surgical robots. Through clinical research and market validation, the four-arm modular surgical robot has emerged as the first innovation to gain market recognition, representing another significant breakthrough in the surgical robotics industry following the da Vinci-style integrated surgical robots.

The four-arm modular design is not unique to CMR Surgical. Global medical technology giant Medtronic began developing its modular surgical robot in 2013, and after several years of development and optimization, its HUGO modular surgical robot received CE certification in late 2021.

Overall, modular surgical robots possess the following potential competitive advantages:

The modular architecture can achieve lower costs. First, the carts in a modular robotic system share similar structures, making equipment costs easier to control from a supply chain perspective. Second, the number of carts can be configured as needed, allowing specialists to select the appropriate quantity based on surgical requirements. For example, Ronovo, China’s first company specializing in modular surgical robots, has developed modular carts that support on-demand procurement by hospitals, thereby reducing initial acquisition costs. The company has also innovatively adopted a compatibility design, enabling its modular surgical robot to work with traditional surgical instruments and endoscopes already available in hospitals. This eliminates the need for additional purchases, further lowering operational costs.

Modular robotic surgical systems offer greater operational freedom. First, they allow for flexible preoperative positioning, enabling surgeons to configure the number and placement of carts according to the specific surgical procedure. Second, this flexible positioning facilitates the selection of optimal insertion sites and angles for surgical instruments. Surgeons can also continue to use traditional laparoscopic port placement strategies, leveraging their existing experience. Finally, the distributed arrangement of robotic arms not only minimizes the risk of collisions but also supports procedures requiring a larger working space, such as those in general surgery, thoracic surgery, and gynecology.

Modular robots offer greater flexibility. First, the modular design “decouples” the multiple robotic arms traditionally mounted on a single base into independent robotic arm carts. These standardized, compact robotic arms are easy to move and can be shared across different operating rooms, thereby improving utilization rates. Second, the modular carts have a small overall footprint, allowing them to flexibly fit into China’s standard 33-square-meter operating rooms. This eliminates the need for hospitals to allocate additional space, thus saving on spatial costs.

Medtronic initiated the development of its modular robotic system in 2013. In 2021, its modular surgical robot, HUGO, received CE marking, and subsequently obtained market approval in Canada and Japan for applications in general surgery, urology, and gynecology. The HUGO robot is specifically designed for soft-tissue surgeries, supporting multi-quadrant procedural workflows, and integrates with wristed instruments, 3D visualization, and Medtronic’s Touch Surgery™, a cloud-based solution for surgical video capture and management.

Ronovo is the first developer in China to create a split modular surgical robot. The company was founded in 2019, and its split surgical robot is Haishan One.TMThe system adopts a standardized cart design, allowing for flexible replacement and configuration with varying numbers of carts. Furthermore, the robot is compatible with traditional straight-handled instruments and vision systems used in conventional operating rooms, significantly reducing hospital acquisition costs and alleviating the financial burden on patients. The company’s proprietary robotic arm configuration and modular design enable coverage of an extensive surgical workspace spanning from the pelvis to the abdomen during procedures, thereby expanding multi-specialty applications in general surgery, gynecology, and thoracic surgery.

Haishan YiTMThe surgical robot adopts the same port placement and surgical instruments as traditional laparoscopy, enabling surgeons to quickly adapt without altering their established surgical habits, thereby reducing the learning curve for robotic surgery. It is reported that Haishan YiTMThe preclinical animal trials have received unanimous acclaim from top experts in China, and the robot is poised to enter human clinical trials. The company completed its Pre-B round of financing in 2022, with investors including LRI Jiangyuan Investment, Lilly Asia Ventures, Vivo Capital, Matrix Partners China, and GGV Capital.

CMR Surgical, founded in 2014 and headquartered in Cambridge, UK, is dedicated to developing next-generation universal robotic systems for minimally invasive surgery. Its independently developed modular surgical robot, Versius, has become the only laparoscopic surgical robot to achieve commercial success since the da Vinci system, and is regarded as the representative of modular surgical robots.

The Versius system, which is only one-third the size of the da Vinci Surgical System, has gained widespread popularity. To date, Versius has received regulatory approval for market launch in more than 20 countries and regions, including Europe, Australia, India, the Middle East, and Brazil, and has been used to perform a cumulative total of 10,000 laparoscopic procedures. CMR Surgical has completed its Series D financing round, with investors including Tencent, SoftBank Vision Fund, GE Healthcare, LGT Group, and Ally Bridge Group.

SS Innovations, founded in 2015 and headquartered in Haryana, India, is a company dedicated to the research, development, and manufacturing of surgical robotic systems. Its independently developed multi-arm surgical robot, Mantra, can be equipped with 3–5 independent robotic arm carts. The system has already received regulatory approval for market launch in India and has been used in over 100 surgical procedures. Mantra has gained widespread recognition for its exceptionally low price, which is only one-third that of the da Vinci Surgical System.

Over the past three decades, Intuitive Surgical’s da Vinci surgical robot has dominated and monopolized the soft-tissue surgical robotics industry. However, its widespread adoption across multiple clinical specialties remains hindered by inherent limitations. In response to the clinical needs of China’s minimally invasive surgery sector, several companies have invested substantial human and financial resources, adopting diverse technological approaches to launch surgical robots with varied configurations. Given the vast market potential, a critical development pathway—one that must not be overlooked—is to prioritize unmet clinical needs as key inputs for research and development, pursue forward-engineering strategies, engage in deep collaboration with clinical experts across various specialties, and continuously iterate and refine products, thereby forging an innovation-driven route independent of imitation. Emerging innovative technologies, exemplified by split modular designs, warrant close attention.

References:

[1] Zheng Minhua. Progress and Development Trends of Minimally Invasive Surgery[J]. Chinese Journal of Practical Surgery, 2002, 22(1):2.

[2] Yang M, Gao CQ. Current application status of robotic cardiac surgery[J]. Chinese Journal of Minimally Invasive Surgery, 2012, 12(7):5.

[3] J.P. Morgan Healthcare Conference 2022

[4] Hale GR, Shahait M, Lee DI, Lee DJ, Dobbs RW. Measuring Quality of Life Following Robot-Assisted Radical Prostatectomy. Patient Prefer Adherence. 2021 Jun 23;15:1373-1382. doi: 10.2147/PPA.S271447. PMID: 34188454; PMCID: PMC8236265.

[5] Robots “Performing Surgery” — People's Daily

[6] Surgical Robots: From a Lone Leader to a Thriving Ecosystem—A Look at the 50-Billion-Yuan High-Barrier Market as Domestic Leaders Gear Up for Takeoff

[7] Surgical Robots Gain Momentum: New Opportunities for a Medical Industry Revolution — Guojin Securities

[8] Versius used to perform over 10,000 cases