Kenvue, Former Johnson & Johnson Consumer Health Unit, Launches Largest U.S. IPO Since 2021 with $50 Billion+ Valuation

Kenvue

Consumer Health Product Developer

VCBeat learned that on May 4, 2023 (U.S. time), Kenvue rang the opening bell at the New York Stock Exchange, trading under the ticker symbol “KVUE.” The company offered 172.8 million shares of common stock at $22 per share, raising a total of $3.8 billion, marking the largest U.S. initial public offering (IPO) since electric vehicle manufacturer Rivian went public in November 2021. On its first day of trading, the stock opened at $25.53 and closed at $26.90, representing a 22.27% increase over the offering price, with a market capitalization of $50.232 billion.

In fact, the U.S. IPO market remained sluggish throughout 2022. According to market data, a total of 345 companies went public in the U.S. in 2022 (290 on Nasdaq, 46 on the New York Stock Exchange, and 9 on the NYSE American), representing only one-quarter of the 2021 figure and marking the worst performance since the 2009 financial crisis. The largest IPO was that of financial services firm Corebridge Financial, which raised just $1.68 billion.

Kenvue’s impressive U.S. stock market debut has injected a much-needed boost into the IPO market, which had been frozen for nearly two years, signaling a potential turning point toward recovery.

So, the question arises: What is Kenvue’s background? Why is it so popular in the U.S. stock market? And how large is its market potential?

Kenvue was formerly the consumer health division of Johnson & Johnson.

According to public information, Johnson & Johnson was founded in 1886. With more than 260 operating companies across 60 countries and regions worldwide and a global workforce exceeding 130,000 employees, it is the world’s largest and most diversified company in healthcare, medical devices, pharmaceuticals, and consumer health products.

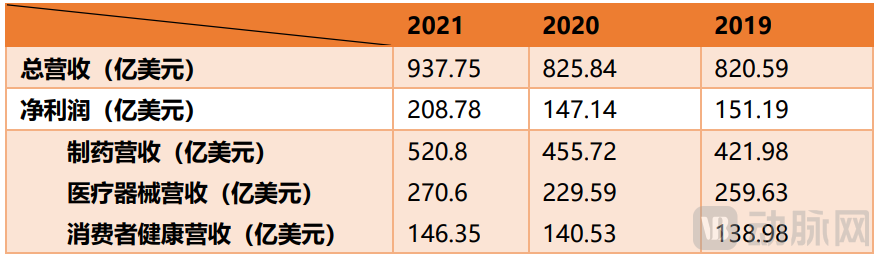

In 2021, Johnson & Johnson claimed the No. 1 spot among global pharmaceutical companies with total revenue of $93.775 billion, as its pharmaceutical and medical device businesses performed strongly amid the COVID-19 pandemic, becoming the key drivers of the company’s growth.However, the consumer health business generated $14.635 billion in revenue, accounting for only 15.6% of total revenue—less than one-sixth and significantly lower than the pharmaceutical and medical device businesses.

Johnson & Johnson’s Revenue, 2019–2021. Data source: Johnson & Johnson financial reports.

Meanwhile, the talc-based baby powder products within its consumer health business have been mired in “carcinogenic” controversies for over a decade, facing multiple lawsuits and substantial compensation claims. To resolve these claims, Johnson & Johnson plans to pay $8.9 billion in settlements over the next 25 years. This has further exacerbated the already weak revenue performance of its consumer health segment.

In November 2021, to address development challenges and further enhance the independence and focus of each business segment, optimize capital allocation, and improve financial performance, Johnson & Johnson undertook its largest spin-off and restructuring plan since its founding in 1886. This involved merging its pharmaceutical and medical device businesses into a “New Johnson & Johnson,” while spinning off its consumer health and personal care products business as an independent entity. In September 2022, “Kenvue” was officially established.

In fact, in recent years, not only Johnson & Johnson but also many multinational pharmaceutical companies have been focusing on their core businesses through spin-offs and M&A activities to enhance their core competitiveness.

For instance, in 2019, Novartis divested its Alcon eye care business; in 2021, Merck & Co. spun off its women’s health, mature products, and biosimilars portfolios into a new company that was subsequently listed independently; also in 2021, General Electric split GE Healthcare, GE Aerospace, and GE Vernova (its energy transition business) into three independent publicly traded companies; and in 2022, GSK demerged its consumer health business to establish Haleon. In addition, companies such as 3M and Medtronic have successively announced spin-off plans.

In fact, from the perspective of spin-off objectives, most multinational pharmaceutical companies aim to achieve refined management and strategically focus on their core businesses, thereby generating higher operating revenues. Nowadays, corporate spin-offs have become a standard practice for multinational enterprises to address challenges, representing an inevitable trend in the current market.

The name “Kenvue” draws inspiration from two concepts: “ken,” derived from the Scottish English word for knowledge, and “vue,” representing vision. The logo features white text on a green background, with a graphic design combining a rectangle and a sideways heart. The rectangle symbolizes scientific precision, while the heart evokes the warmth of care. Kenvue aims to leverage extensive knowledge to deeply explore human needs, delivering more meaningful personal health solutions to consumers worldwide.

Kenvue Logo. Image source: Kenvue official website

From the perspective of its brand portfolio, this newly spun-off company is not to be underestimated.Kenvue has a portfolio of 44 brands, with more than 10 of them achieving net sales exceeding $400 million in 2022.。

Kenvue’s Top 10 Net Sales in 2022. Source: Kenvue Official Website

Currently, multiple Kenvue brands rank first in their respective niche markets across North America or globally. For instance, Tylenol is the No. 1 pain reliever recommended by U.S. physicians for adults. Neutrogena ranks first among over-the-counter sunscreen and acne care brands recommended by U.S. dermatologists. Listerine is the top mouthwash brand recommended by U.S. dentists. The portfolio also includes well-known products among Chinese consumers, such as Band-Aid and Dabao.

Its business is broadly divided into three segments: Personal Care, Skin Health & Beauty, and Basic Health.

Kenvue’s Three Major Business Segments | Image Source: Kenvue Prospectus

The first business segment is personal care, encompassing over-the-counter (OTC) medications and wellness products, such as Tylenol for headache relief and cold symptom alleviation, the analgesic Motrin, and Zarbee’s cough syrup, totaling 16 brands.

The second business segment is skin health and beauty, dedicated to providing the best skincare products, encompassing 16 brands including Neutrogena, Aveeno, Dr. Ci:Labo, and Dabao.

The third business segment is Basic Health, which includes brands in wound care, oral care, baby care, and women’s health. It comprises 12 brands, including Listerine, Band-Aid bandages, OB tampons, and the infant and child care brand Vivvi & Bloom.

The prospectus shows that in 2022, Kenvue's total revenue was $14.95 billion, with a net profit of $2.087 billion.

Kenvue’s Financial Performance, 2019–Q1 2023 Data Source: Kenvue Prospectus

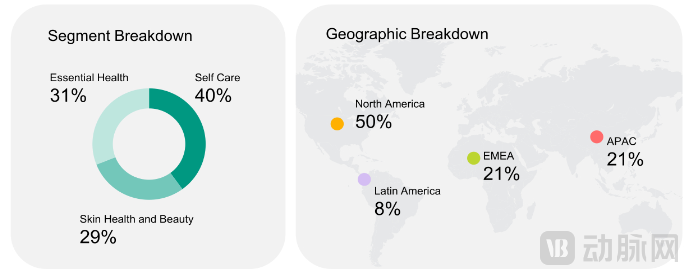

From a regional and business segment perspective, half of the revenue came from North America, and the revenue distribution among the three major business segments was relatively balanced: Personal Care generated $6.03 billion in revenue, a year-on-year increase of 6.9%; Essential Health generated $4.57 billion, a year-on-year decrease of 6.2%; and Skin Health & Beauty generated $4.35 billion, a year-on-year decrease of 4.2%. Notably, all sub-segments, including beauty and personal care, oral care, baby care, and women’s health, experienced declines.

Left: Revenue Share by Three Major Business Segments; Right: Revenue Share by Region. Source: Kenvue Prospectus

Overall, the total revenue scale in 2022 remained largely unchanged compared with 2021, but net income declined by 0.69% year over year. The company attributed the decline to foreign exchange impacts, asset divestitures, and constrained product supply. However, Kenvue stated that it remains profitable and expects moderate growth in the coming years.Kenvue’s total revenue in the first quarter of 2023 reached $3.852 billion, a year-on-year increase of 7.3%, surpassing the year-on-year growth rates of Johnson & Johnson’s other two divisions and indeed confirming the trend of performance growth.

Notably, 2020 was the only year in recent times to record a loss, namely the year prior to the spin-off from Johnson & Johnson. In that year, Johnson & Johnson’s total profit amounted to $14.714 billion, representing a year-on-year decrease of $404 million compared to 2019. Meanwhile, Kenvue’s loss of $879 million far exceeded the decline in Johnson & Johnson’s net profit. To some extent, this business segment dragged down Johnson & Johnson’s profitability, and the loss incurred that year undoubtedly strengthened Johnson & Johnson’s resolve to spin off this business.

As an independently spun-off consumer health and personal care company, Kenvue has positioned itself to compete directly with industry giants such as L'Oréal and Procter & Gamble. According to the publicly disclosed 2022 financial reports of L'Oréal and Procter & Gamble, L'Oréal reported annual sales of €38.26 billion ($42.293 billion), while Procter & Gamble recorded $80.187 billion, both maintaining a growth trend of approximately 5%. These figures are 2.83 times and 5.36 times that of Kenvue, respectively.

Moreover, they are continuously expanding their presence in the Chinese market. Procter & Gamble has been divesting its mass-market beauty businesses to increase the proportion of premium products, while L'Oréal is expanding its brand portfolio and entering new sectors through investments and mergers and acquisitions. To keep pace with these competitors, Kenvue is driving multi-dimensional innovation, primarily in product development and distribution channels.

On the product, Kenvue rapidly completed its strategic layout by leveraging established brands such as Neutrogena and Dabao. In addition, the company flexed its financial muscle by acquiring the premium hair care brand OGX and Japan’s medical aesthetics product manufacturer Ci:z Holdings, thereby bringing skincare brands Dr. Ci:Labo and LABO LABO into its portfolio to expand its brand lineup.

On the channelIn 2016 and 2017, Johnson & Johnson’s Consumer Health division launched two major brands, Aveeno and Dr. Ci:Labo, on Tmall, establishing them as leading brands in the industry. In May 2021, it entered into a deep strategic partnership with Douyin E-commerce, enabling brands such as Dr. Ci:Labo, Neutrogena, Listerine, and Aveeno to gradually appear on major short-video platforms, thereby continuously enhancing brand exposure. Currently, Kenvue’s e-channel sales account for a relatively small proportion, indicating substantial room for growth. In addition, Kenvue is seeking new growth opportunities in the medical aesthetics market; in September 2022, the first Chinese store of “Dr. Ci:Labo Medical Aesthetics Clinic” opened in Beijing.

From the perspective of Johnson & Johnson’s long-term development, Kenvue holds distinct advantages, with its infant care brands maintaining a leading position in the industry. Meanwhile, rising global consumer awareness of preventive health, continuously releasing market demand, and the growing application of e-commerce in the consumer health sector are reshaping the landscape. These trends have laid a solid foundation for Kenvue’s growth and provided momentum for its long-term sustainable development. Following its successful listing in the United States, Kenvue is expected to secure greater financial support, which will further accelerate its development trajectory.

However, Kenvue lags significantly behind L'Oréal and Procter & Gamble in terms of scale and revenue, with its beauty care business still on a downward trajectory. To break through its growth ceiling and secure a more competitive position within the industry, the company urgently needs to pursue greater innovation.