Post-COVID Biotech A-Round Investors: Who's Leading the Charge and What Are They Backing?

How Have COVID-19 and the Capital Winter Impacted the Startup Ecosystem? U.S. Research and Analytics Firms Tend to Focus on Series A Financing Rounds.

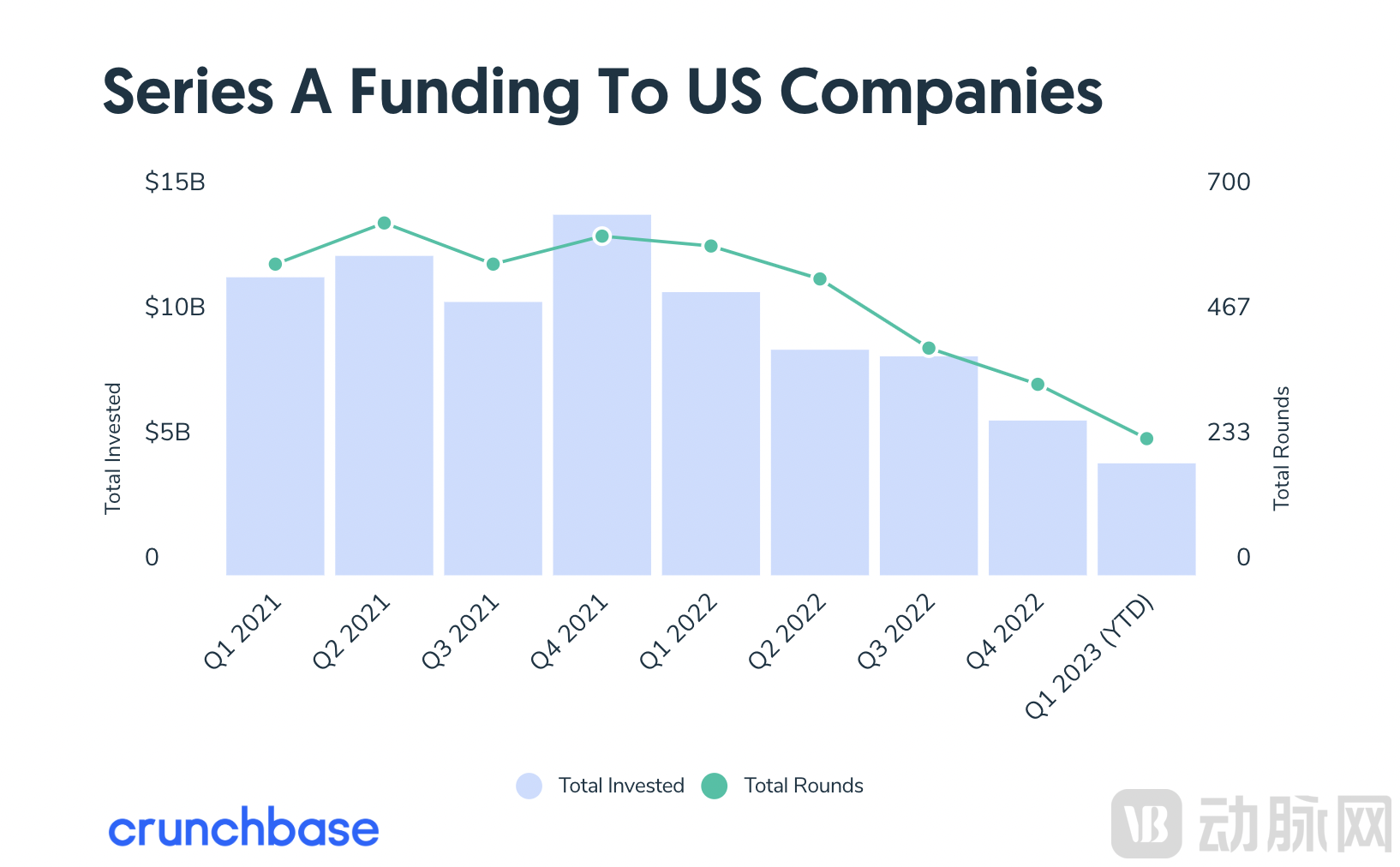

A recent study on U.S. Series A financing shows that the total investment amount will hit its lowest quarterly level in more than two years.

According to Crunchbase data, Series A funding for U.S. startups has declined for five consecutive quarters since peaking in late 2021. Over the long term, the total funding amounts for the past nine quarters are as follows:

Data source: Crunchbase

However, investors have also written some large checks. As of the end of March this year, at least five startups secured Series A financing rounds exceeding $100 million, with approximately 35 deals surpassing $30 million. As usual, life sciences companies accounted for the majority of the largest fundraising activities in recent months.Biotechnology companies, in particular, rank among the top in Series A financing rounds.。

Due to the unique nature of Series A financing,It is neither like seed-round financing, where the investment amounts are relatively small and institutional investors can cast a wide net; nor like Series B financing, which typically serves as a “crossover round” between venture capital funding and an IPO. By that stage, the company has already moved past its initial startup phase and achieved certain milestones in business development.Series A investors have always been the “tastemakers” of the biotech startup world.

In the current market environment, examining which companies have secured large Series A financing rounds and who is investing in them provides a valuable perspective for observing and analyzing shifts in capital market trends.

1Why Focus on Series A Funding?

In January this year, Paradigm, a New York-based startup, announced that it had secured $203 million in Series A financing. The company focuses on clinical patient recruitment and is dedicated to simplifying clinical trial development technologies for physicians, researchers, and pharmaceutical companies. Paradigm was founded by Arch Venture Partners and General Catalyst, with additional investors including F-Prime Capital and GV.

In March, Cargo Therapeutics, a biotechnology company headquartered in San Mateo, California, announced the completion of a $200 million Series A financing round to advance the research and development of next-generation CAR-T cell therapies. Lead investors included Third Rock Ventures and RTW Investments, among others.

Also in March, Rapport Therapeutics, a new Boston-based company, made its debut with $100 million in Series A funding. Rapport was co-founded by venture capital firm Third Rock Ventures and Johnson & Johnson’s investment arm, JJDC. Focusing on drug development for neurological disorders, Rapport’s platform leverages genomics, protein science, and brain imaging technologies to identify receptor-associated proteins (RAPs) for precision neurotherapeutics.

Series A investors have always been the “trendsetters” in the biotechnology startup community.In recent years, the seed-stage and late-stage financing markets have undergone significant changes amid intensifying competition, but the U.S. Series A market has remained largely unaffected to date.This is becauseThe U.S. Series A investment market has been dominated by a handful of funds for over a decade., capital is relatively concentrated, which means that if a biotech company fails to catch the attention of these few institutions, it will struggle to secure funding—even if it possesses genuine potential. On the other hand, most companies selected by these investors subsequently succeed in raising further capital and gain the opportunity to bring their drugs to market.

Why Are Only a Few Funds Active in the Series A Financing Market?This can be attributed to the difficulty of securing Series A financing.. The portfolio of skills required for Series A investment differs significantly from that needed for later-stage or seed-stage investing. While Series A investors do consider market feedback from later-stage investors and pharmaceutical companies, as well as collaborate with other venture capital firms participating in Series A rounds, they often rely on their own experience when evaluating companies.

Series B investors can leverage the work of Series A investors to supplement their own due diligence. In sourcing deals, Series B investors can identify investment opportunities by building relationships with earlier-stage investors, whereas Series A investors must cast a wider net across universities, seed-stage investors, angel investors, and standalone companies. Regarding investment approach, unlike seed investors who write numerous small checks, Series A investors maintain more concentrated portfolios, necessitating thorough due diligence on each transaction.

Emerging venture capital firms that can appropriately adjust their investment strategies in light of the unique characteristics of Series A investments will hold a competitive advantage over investors who are slower to adapt to market differentiation. However, execution risk is not the only challenge these investors face,They are also facing the most challenging late-stage financing market in years:

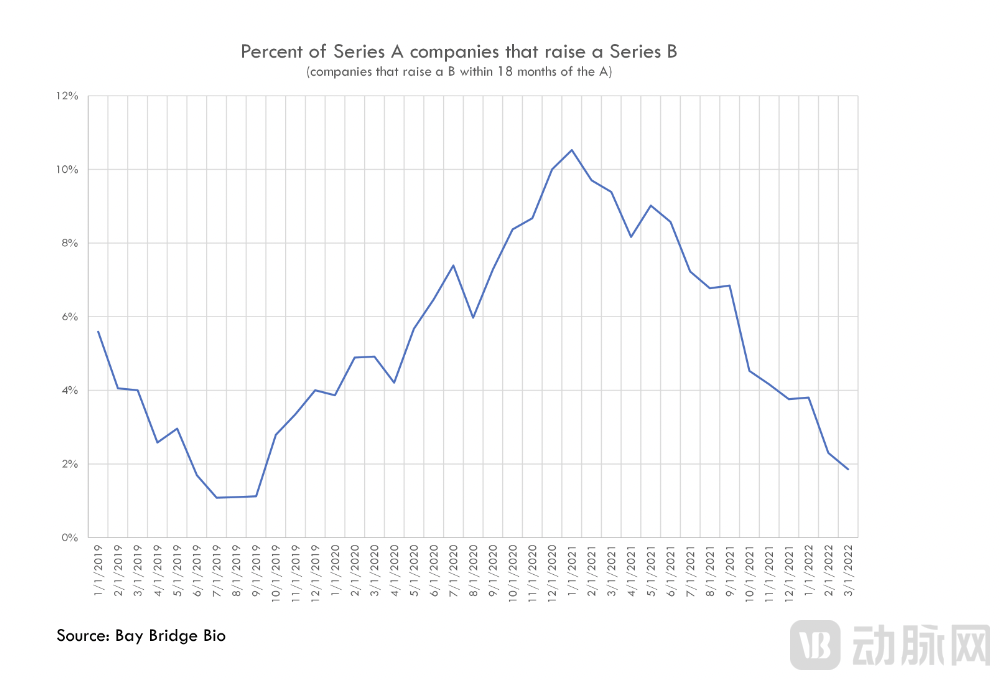

Data Source: Bay Bridge Bio

The chart above shows the monthly percentage of Series A companies that were able to continue raising their Series B rounds within 18 months. This proportion was approximately 5% before the slowdown in the IPO and crossover financing markets in 2019; it then rose to over 10% during the COVID-19 pandemic;It has now fallen to its lowest level in nearly three years, dropping below 2%.

VCBeat’s New Medicine previously published an article analyzing,U.S. Biotech Faces a Series A Funding CliffData from Silicon Valley Bank (SVB) and Bay Bridge Bio corroborate each other: Between July 1, 2020, and December 31, 2021, 356 biotech companies completed Series A financing rounds, whereas only 102 pharmaceutical companies announced Series B financing rounds in 2022. While U.S. biotech firms readily secure Series A funding, many are exhausting their cash reserves without securing subsequent Series B rounds—a prevailing challenge currently facing the U.S. biotechnology sector.

For these funds, this could present either a challenge or an opportunity. On one hand, the sluggish Series B financing market makes it more difficult for companies backed by Series A investors to raise follow-on capital. On the other hand, if Series A investors wish to allocate additional capital in later funding rounds, they will be able to secure more attractive valuations.

Institutions with the confidence and capacity to commit capital in later-stage financing rounds will benefit from the sluggish Series B market, while funds with weaker capabilities in late-stage investing will face greater challenges. For funds focused on rapid portfolio expansion and pursuing high returns through valuation mark-ups, a strategic shift is essential to compete effectively in the late-stage investment market.

2Who is investing in Series A?

Over the past decade, traditional biotechnology venture capital firms have profited from a robust IPO market. However, amid turbulence in the biopharmaceutical industry and a slowdown in the IPO market, these venture capital firms have scaled back their activities. Established biotech VC firms such as Atlas Venture, Versant Ventures, Third Rock Ventures, and 5AM Ventures are now ceding market share.

A new wave of biotechnology venture capital firms took up the baton at this juncture.Unlike traditional biotechnology venture capital firms, they have instead accelerated their investment activities.“Emerging” does not mean they are unfamiliar with the biotechnology investment sector, but rather indicates that their investment activities at the Series A stage have currently increased.Many of these “emerging” venture capital firms have been investing in biotechnology for years or even decades. They have historically focused their investments on the seed stage or later stages, occasionally participating in Series A financing rounds, but not as frequently as “established” Series A venture capital firms.

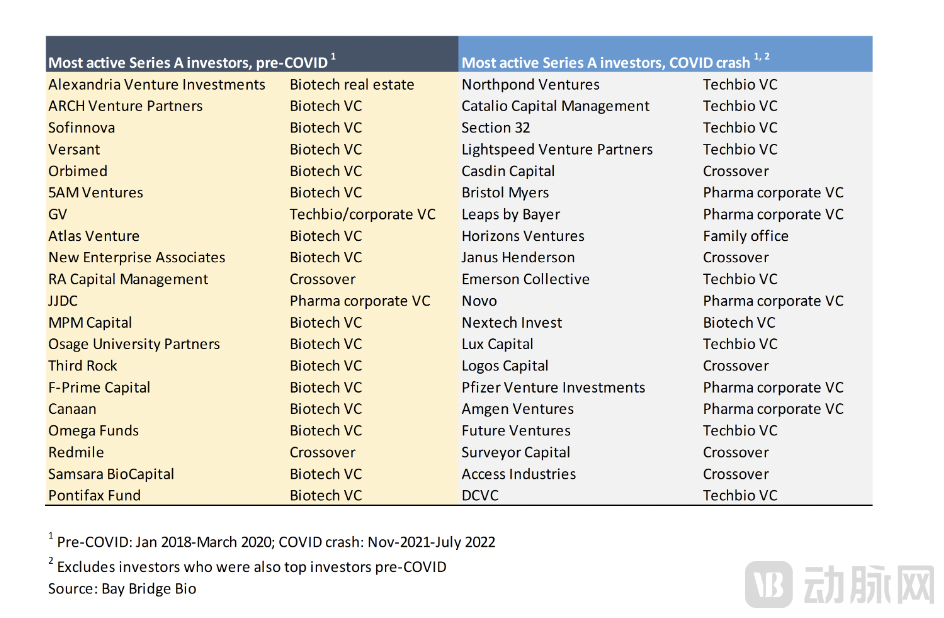

The left column lists the most active Series A investors in the pre-COVID era, most of whom are specialized biotech VCs; the right column lists the most active Series A investors during the COVID crash phase (November 2021–July 2022), excluding the top investors from the pre-COVID period.

Data Source: Bay Bridge Bio

The first category is TechBio venture capital firms.

At the beginning of this century, following the burst of the internet bubble, U.S. technology investors largely abandoned the biotechnology sector. However, starting in the mid-2010s, U.S. software investors began to test the waters in biotechnology. From around 2015 onward, software-focused investors started attempting to enter the biotechnology field.

Amid intensifying competition in the technology venture capital sector, they recognized the substantial returns generated by the biotechnology industry and decided to shift their focus, carving out a niche for themselves in biotech venture capital. In the view of software-focused VCs, new data science technologies could be applied to the field of biology, enabling the creation of a new class of more resilient companies built on these emerging technologies.

They focus on two areas overlooked by established venture capital firms: young scientist-founders and the integration of computational platforms with traditional drug discovery.

They have also introduced investment terms that are more founder-friendly, akin to those in the software sector. In the traditional biotechnology field, many companies are internally nurtured and incubated by venture capital funds. Flagship Pioneering is a prime example; such funds typically lead the Series A financing round of successfully incubated companies and ultimately acquire 50% or more of the equity post-Series A. TechBio VC firms invest smaller amounts compared to traditional biotech funds, but at higher company valuations.

Another positive change brought by these TechBio VCs is the establishment of a robust seed financing ecosystem. Prior to the entry of TechBio venture capital firms, there were few channels for biotech startups to raise initial capital unless one had close ties with major venture capital firms. Although some family offices and angel investors were active, the terms they offered were generally unfavorable, and their investment strategies were highly inconsistent. Frankly speaking, the seed market for biotechnology was poor. The situation changed when TechBio VCs entered the field.

In the United States, prior to the COVID-19 pandemic, techbio venture capital firms primarily focused on seed-stage investments, with only a few funds participating in Series A rounds (typically through co-investments with established biotech venture capital firms). As these investors accumulated experience, an increasing number entered the seed-stage space. By 2021, the seed financing ecosystem in the biotechnology sector had experienced explosive growth. The entry of techbio VCs helped establish a truly founder-friendly seed funding ecosystem, with investors beginning to pay closer attention to the distinct differences and characteristics among founders of various companies—developments that have been positive for the industry. While the argument that “software is eating biotechnology” may be overhyped, it is certain that many promising companies have received funding from these venture capitalists.

Beyond these positive contributions, techbio funds have also imported a more controversial strategy from the software venture capital circle: marketing and hype. In the past, limited partners (LPs) were intrigued by the narratives these funds crafted about the industry’s future. However, as the biotechnology market bubble has burst, LPs are beginning to question the stories they hear from venture capitalists (VCs). A major challenge facing techbio funds is whether investment returns can live up to the “hype.” If the market remains sluggish, the true winners will be those who make sound investment decisions and deliver capital returns, rather than those who raise large sums of money and secure spots on hot deal lists.

The second category is cross-industry investors.

Cross-sector investors were once the backbone of the biotechnology financing ecosystem. However, since the pandemic forced cross-sector deals to a halt, these investors have begun seeking refuge in the Series A market.

Many cross-sector investment firms were already active in Series A financing rounds before the COVID-19 pandemic, striving to capture market share from venture capital firms that had long dominated early-stage investments. As established VC firms yielded ground, these cross-sector investors finally secured their position as key players in early-stage investing.

Some of these companies failed to adhere to the fundamental principles of valuation and corporate fundamentals during the COVID-19 pandemic, ultimately leading to the formation and bursting of a bubble.In some cases, these funds have adopted a more market-centric approach rather than investing based on fundamentals (the fundamentals of companies and their R&D products), with only a small subset of firms being overly excited about the potential demonstrated by COVID vaccines.

These institutions must make the following adjustments in the Series A market: 1. Establish new information networks to identify Series A deals. 2. Tighten their strategies to adapt to a higher-risk financing stage and a less supportive late-stage financing market.

The third category is the strategic investment departments of pharmaceutical companies.

Strategic investment divisions of large pharmaceutical companies have long been active in Series A financing rounds. These investors typically pursue different objectives than other venture capital (VC) firms: while traditional VCs aim solely to generate returns for their limited partners, corporate strategic investment arms must also serve the strategic interests of their parent companies. Leveraging substantial cash reserves on their balance sheets, pharmaceutical companies’ strategic investment divisions are well-positioned to capitalize on current market volatility, making investments that diverge significantly from those of traditional VC firms and align with specific strategic financial goals. In less competitive markets, these entities may secure favorable deals for their parent companies through equity investments, R&D collaborations, and licensing agreements.

Major pharmaceutical companies will face significant losses in the coming years due to the erosion of exclusivity for key drugs. Large-scale mergers and acquisitions have long been a common strategy for these companies to address this revenue gap, and they have also served as a major driver of returns for mature biotech venture capital firms and public equity investors. Last year, heightened scrutiny from the Federal Trade Commission (FTC) resulted in mixed outcomes for pharmaceutical companies pursuing such blockbuster deals.

However, M&A activity has clearly rebounded this year, with Pfizer’s acquisition of Seagen serving as a bellwether. Pharmaceutical companies can supplement their pipelines not only through mergers and acquisitions but also by establishing relationships with platform companies at early stages. Pharma firms can serve as ideal partners for these companies, bringing valuable expertise in drug development and providing substantial cash reserves. This trend is further evidenced by the frequent out-licensing of pipelines by Chinese ADC developers to multinational corporations (MNCs) this year.

3What is the situation in China?

As analyzed in previous articles, there are differences in the degree of innovation and financing practices between the Chinese and U.S. biotechnology industries: U.S. biotech companies generally exhibit a higher level of technological innovation and take longer to advance a drug candidate to the Investigational New Drug (IND) stage, typically requiring an average of three to four years. They also secure larger Series A funding rounds with fewer financing rounds overall. In contrast, Chinese companies pursuing fast-follow or me-too strategies can progress more rapidly, often advancing projects to the IND stage within one year of establishment. However, these companies typically undergo more frequent financing rounds, including additional tranches such as Pre-A and A+ rounds.

However, in the biopharmaceutical sector, domestic and international investors differ slightly in their perspectives and timing. Nevertheless, the fundamental drivers of the industry remain essentially the same. From a capital perspective, the pre-Series A and Series A stages are largely conceptual, with Series A financing playing a critical transitional role in corporate development. When we evaluate Series A investments today, we are essentially assessing a watershed moment for growth.

Therefore,By examining the volume of Series A financing rounds and the investors behind them, we may uncover some interesting insights into China’s biotechnology investment market.

According to the VBData database, a total of 92 financing events occurred in China in the first quarter of 2023, among which 36 were related to Series A (Pre-A/A/A+), accounting for 40% of the overall market, remaining the dominant stage.

An analysis of Series A financing deals reveals that investment activities in small molecules, large molecules, nucleic acid drugs, synthetic biology, and even CXO and AI-driven drug discovery are all on a comparable scale, indicating that the industry has not exhibited a herd-like rush to bet on specific sectors. In terms of investors, government-backed funds are actively participating behind the scenes in niche cities such as Tonghua and Jiaxing. Meanwhile, in industrial hubs like Suzhou and Shanghai, in addition to mainstream market-oriented funds, there is a growing presence of strategic investments from large enterprises, such as China Merchants Group, Simcere, and Beta Pharma.

The diverse investment entities and their underlying motivations are also driving the industry into a case-by-case phase, emphasizing the innovative operational capabilities of individual projects, with value investing coming to the fore.

Of course, another critical backdrop that must be mentioned is that, despite tangible progress in the development of novel therapies, research and development (R&D) in the biotechnology sector has been grappling with escalating costs for decades. Although venture capital (VC) investments in biotechnology have generated substantial returns in recent years, progress in delivering high-value drugs has remained less than ideal.

The biopharmaceutical industry is unique in that it is one of the most innovative sectors in the global economy, while most of its leading companies have been established for over a century. Startups and venture capital firms have injected new vitality into the industry, but significant challenges remain to be addressed. As emerging venture capital entities successfully take the baton, they will have the opportunity to drive genuine transformation.

But are they truly prepared to lead the industry into its next boom, or are they merely a flash in the pan? Only time will tell.

Reference Article:

The next generation of biotech VCs,Bay Bridge Bio

Getting To Series A Has Gotten Harder,crunchbase news