Are Platform Biotechs Still Investable? Insights from Recent IPO Filings and Strategic Shifts Toward Product-Centric Validation

Early this year, specialized media outlets in the overseas biotechnology sector published articles pointing out that emerging biotech companies will face five critical issues this year, one of which isAre Platform Companies Still an Attractive Investment?

Since the pandemic, “platform” companies have arguably become the hottest trend in the biotech venture capital sector. Once a platform technology is validated, it seems to imply that the company can replicate its success on a large scale, no longer needing to worry about its pipeline and products, nor about IPOs and returns.

Nowadays, reflection on platform-based companies has become an important manifestation of the industry’s return to rationality.At the recently concluded 2023 Sequoia Global Healthcare Industry Summit, it was mentioned in the dialogue between Shen Nanpeng and Philip S. Ross, Global Chairman of JPMorgan Investment Bank, thatThe biotechnology industry is shifting its focus from platforms back to products.

“A senior domestic investor provided VCBeat New Medicine with a more specific explanation of this trend: ‘The logic that having a technology platform alone can attract investors no longer holds.’”This year, there are virtually no pure-platform projects. Investors are not ignoring platform-based models per se; rather, they are disregarding platforms that rely solely on storytelling. The value of a platform must be validated through its products.。”

Reflections stem from the market performance of these platform-based companies: those with platforms but no products, yet commanding high valuations, suffered the greatest impact during the post-pandemic capital winter.

At the same time, investors are expected to invest early and in small-scale ventures, which undoubtedly imposes higher demands on them. “I have been studying this matter for approximately 10 years,“I started getting involved in this industry in 2010, and around 2020, I was willing to invest in a company based on just some preclinical data,” said the senior investor.

“It is not solely based on investment experience to make judgments,”Judgment requires extensive industrial experience.“. From pharmacology, toxicology, and PK/PD perspectives, we identify the gaps between animal models and humans, and infer the potential clinical implications of these gaps in the future.” The senior investor explained, “On one hand, it is essential to understand regulatory authorities’ views on these gaps; on the other hand, it is necessary to comprehend how clinical researchers address them. Additionally, corporate interests must be taken into account to determine how to maximize benefits for the company.”

In June 2022, Bay Bridge Bio published an article titled “Biotech Platforms Out, Products Back In,” using rigorous and detailed market performance data to explain why the market ultimately embraces the logic that “product is king,” and what this means for investors and startups.

This article was compiled and translated by VCBeat, hoping it will be helpful to readers:

1Platform Companies Hit Hardest in the Capital Winter

The booming biotechnology platforms are a hallmark of the coronavirus disease era. However, these high-valuation companies have been hit hardest by the post-pandemic capital winter.

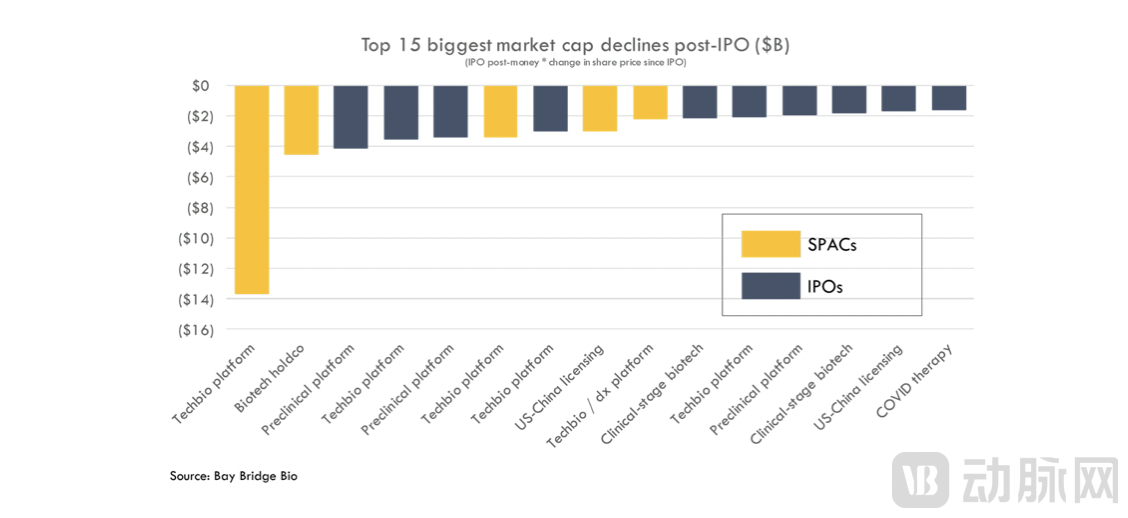

Since 2010, more than 500 biotech startups have gone public via IPOs and SPACs. We analyzed the biggest winners and losers in this cohort, measured by multiplying the IPO valuation by the change in stock price since the IPO.

Among the 10 worst-performing companies, seven are platform-based biotechnology firms. On the other hand, the best-performing companies all have de-risked assets (approved products or products in pivotal trials).

SPACs and techbio platform companies have been the worst performers: among the 10 biggest losers by market capitalization, five were SPACs and five were techbio companies. Although SPAC and techbio IPOs accounted for only a small fraction of biotechnology public market IPOs—with SPACs representing just 5% of newly listed companies yet comprising 50% of the 10 worst-performing stocks—similarly, techbio companies made up 5% of total entrants into the biopharmaceutical public markets but accounted for 50% of the 10 stocks with the poorest market capitalization performance.

For enterprises, this is a paradox: platform companies underperform, yet you need a platform to build an enduring company.

How do you resolve this paradox? One solution is to focus on the product first, and then build a platform to serve these products.

In the words of Genentech's founding CEO, Bob Swanson:

“We were intensely focused on the product, as it is the product that plays the decisive role. I know that Cetus was more keen on developing technology at the time. I said, ‘Alright, let’s build a product. We will develop the technologies needed to manufacture the product, allowing the product to drive scientific research, rather than the other way around.’ In fact, precisely because of this approach, we conducted better scientific research and also ended up with a viable product.”

2Why Are Products Often More Valuable Than Early-Stage Platforms?

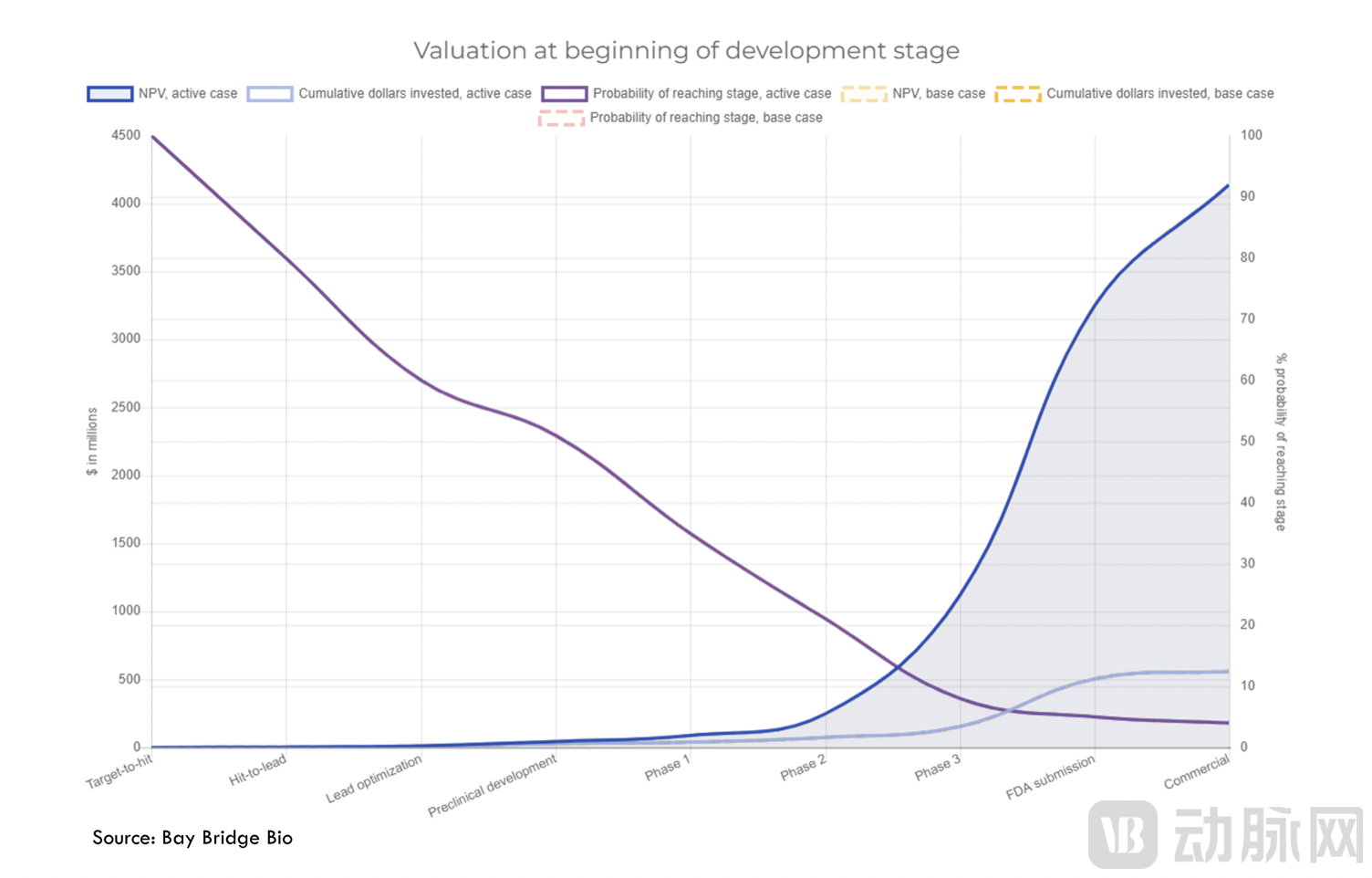

Three fundamental rules of biotechnology explain why products are often more valuable than early-stage platforms, and why platform companies become more valuable when they successfully develop strong products:

Value comes from making patients healthier. Products (i.e., pharmaceuticals) make patients healthier. Platforms can only help patients indirectly through the products they generate.

Drug development carries substantial risk. As a product advances through clinical development, its value grows exponentially. The combined value of hundreds of projects in the R&D phase does not equal that of a single approved blockbuster product.

Most value derives from first-in-class or best-in-class products. The combined value of hundreds of me-too products is lower than that of a single first-in-class or best-in-class product, as the latter can deliver meaningful clinical benefits and address patients’ serious unmet needs.

Our drug pricing calculator leverages data from studies on drug development costs to illustrate the aforementioned concepts:

In short: The quality of R&D projects is more important than the quantity. If project quality is low, the platform's value will diminish as it scales.A valuable platform is one that can identify a select few high-value projects, rather than a large number of mediocre ones.

If the chart above is correct, we can expect the best-performing stocks to be those of companies with late-stage products.

This is precisely what we observe in the IPO market performance data. During the 2010–2021 IPO boom, all companies with the largest market capitalization growth had mature and valuable products.

All of these companies either have commercial products, products pending regulatory approval, or products undergoing pivotal studies.

Many such companies possess not only advanced products but also platforms. However, the majority of their value derives from their product assets rather than their platforms.

It can be said that Foundation Medicine is the only company among these to have been acquired more for its platform value than for its product value.

Even BNTX (BioNTech) and MRNA (Moderna), the two stocks that sparked a frenzy around biotechnology platforms, saw their share prices truly rise only during the development of COVID-19 vaccines. Prior to the pandemic, MRNA traded below its IPO price.

Every time you see a biotech stock double or triple overnight on the back of strong data, it is actually this principle at work:Strong Clinical Data Is the Currency of Value in Biotechnology. Specifically, robust clinical data demonstrate which candidates have first-in-class or best-in-class potential and can deliver meaningful clinical benefits to patients with significant unmet medical needs.

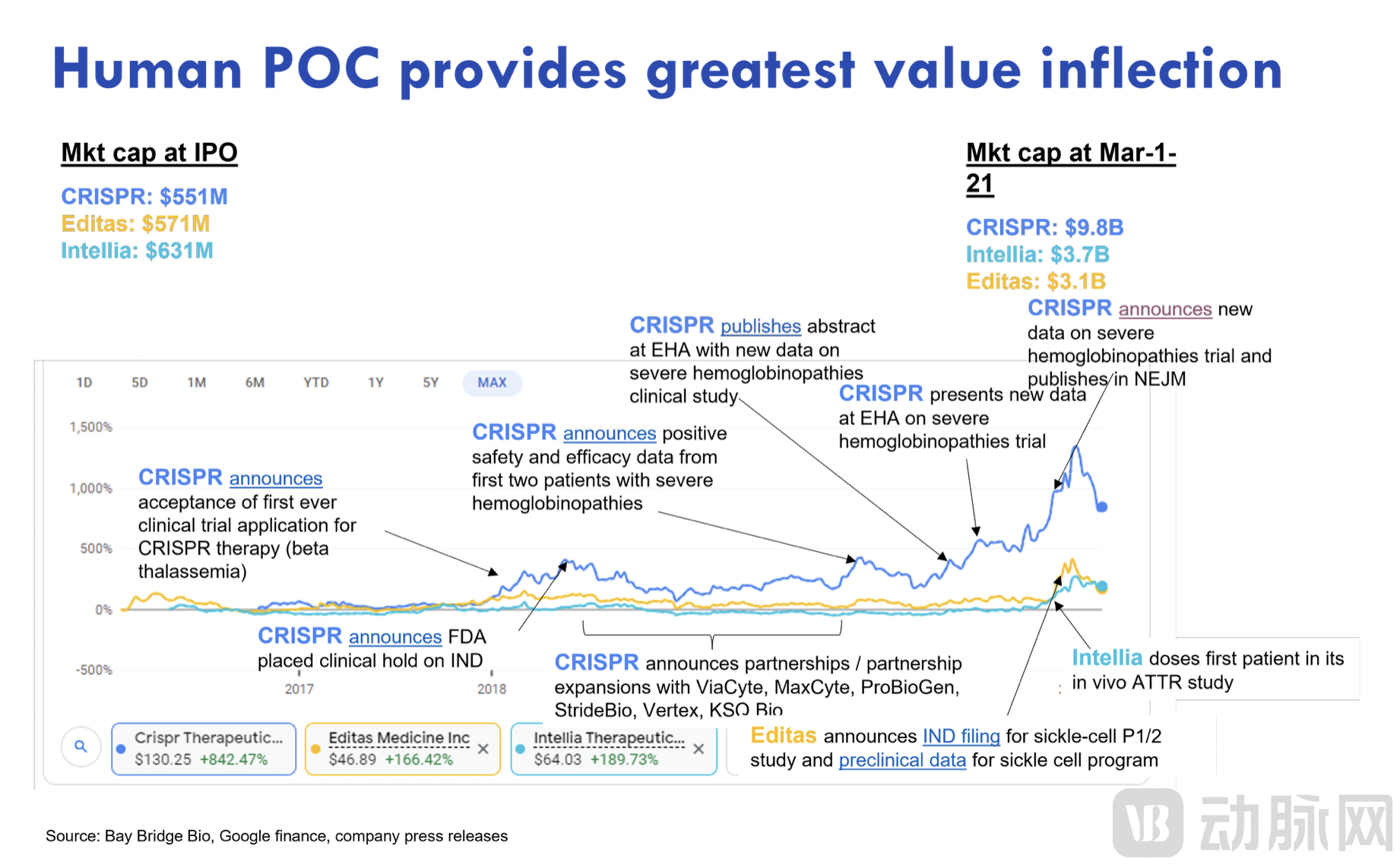

3CRISPR 1.0—The Initial Preclinical Platform

We can examine the initial clinical-stage platform biotech IPO cases of CRISPR pioneers Intellia, Editas, and CRISPR Therapeutics to further demonstrate the link between clinical progress and value creation.

These companies all went public before their products entered clinical trials, with valuations ranging from $550 million to $630 million. Prior to CRISPR Therapeutics entering clinical trials, the market capitalizations of several companies were quite similar. As CRISPR gradually released clinical study data demonstrating the drug’s efficacy, the market responded by assigning the company a higher valuation. Intellia and Editas entered clinical trials at a later stage; their stock prices began to rise only after they entered clinical trials and announced positive data.

Why Did CRISPR’s Stock Price Rise Following the Release of Clinical Data? The data indicate that CRISPR’s product offers significant clinical benefits (potential cure) to patients with unmet needs for severe hemoglobinopathies (sickle cell disease and beta-thalassemia), and holds first-in-class or best-in-class potential. (CRISPR’s clinical programs are on par with bluebird bio’s gene therapy research for severe hemoglobinopathies, suggesting first-in-class potential; moreover, CRISPR has best-in-class potential because it employs a non-integrating vector and utilizes a distinct technology—CRISPR—for gene editing.)

Notably, CRISPR had announced several partnerships for its platform, but none of these announcements impacted the stock price.

Data demonstrating scientific or technological differentiation (as opposed to clinical differentiation) also had no impact on stock prices. Scientific and technological differentiation is meaningful only when it leads to clinical differentiation.This enables the provision of better products to patients. During the COVID-19 bubble, a common investment strategy was to identify promising technological trends and then invest in companies with the best technologies in those future-oriented fields. This strategy overlooked a critical point: products are the mechanism through which new technologies realize their potential.

Just as investors during the dot-com bubble believed that the internet would change the world and consequently lost their entire capital, biotechnology investors may be correct in their assessment of a technology’s long-term prospects, yet they will still incur losses in the short term.Betting solely on technology while ignoring the fundamentals of companies and products is a high-risk strategy; in the long run, its returns underperform those of strategies focused on fundamentals.

4Pharma will only pay for valuable products with excessive risk.

The above data indicate that public equity investors reward products more than platforms. We also observe that most winners in the public markets are eventually acquired. So what do large pharmaceutical companies value?

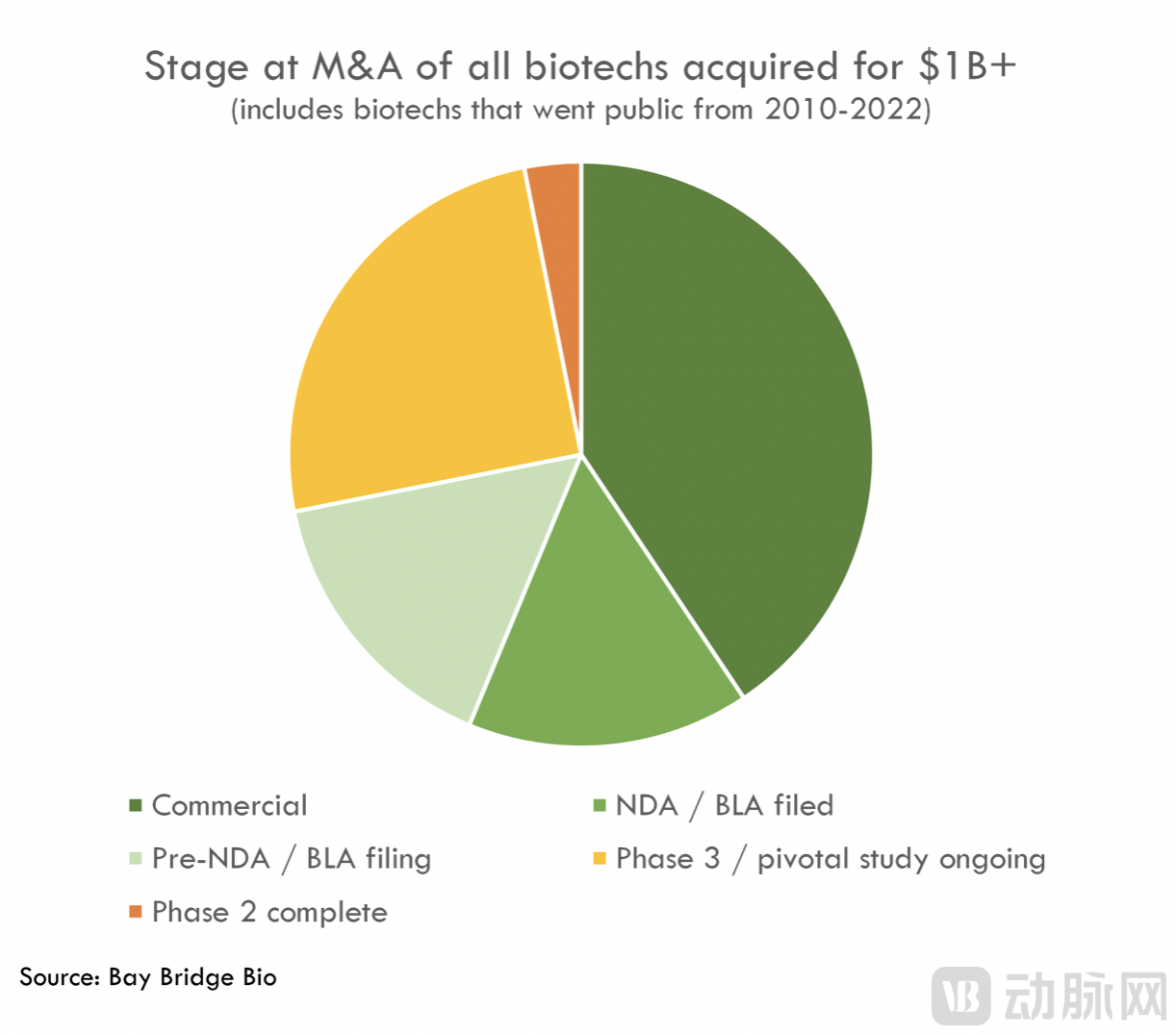

Among the more than 500 biotechnology startups that went public between 2010 and 2022, 32 were acquired for over $1 billion. All of these companies had de-risked products: 40% already had approved products, 31% had submitted or were about to submit regulatory filings for approval, and 25% were conducting pivotal studies.

Only one company—Five Prime Therapeutics, which was acquired by Amgen for $1.9 billion in March 2021—had completed Phase II studies and was on the verge of initiating Phase III trials.

5What Does This Mean for Startups?

The excitement surrounding platforms in recent years has been the exception, not the rule, in the biotechnology sector.Over the past 25 years, pure biotechnology platforms—those not yet demonstrating the potential for viable products—have secured substantial funding in only a few years: 2020–2021 and 1999–2000.

The period from 2020 to 2021 marked the COVID-driven bubble in the biotechnology industry, while 1999–2000 witnessed the genomics bubble.

Platform risk is the last risk that biotech investors are willing to bear in the business cycle, and alsoThe first risk they shed as the market shifted. Today, it is still possible to raise seed or Series A financing around a platform with no pipeline or product candidates, but the later-stage financing market poses greater challenges for platform-based companies. Even in 2020–2021, only a few tech-bio platform companies entered the public markets. The performance of these companies suggests that the number of listed entities will not improve in the short term.

This creates a paradox: it is difficult to raise capital for a pure platform, yet you need a platform to build an enduring company. History tells us that the way to resolve this paradox is to do what Bob Swanson did when creating Genentech—focus on products and build a platform that supports those products. Do not focus on the platform for its own sake.

What defines a good product? They possess first-in-class or best-in-class potential, deliver clinical value to patients with unmet clinical needs, mitigate the risks associated with human proof-of-concept studies, and feature robust intellectual property protection (including composition of matter patents for new chemical entities).

Certainly, companies that can develop remarkable products through their platforms will always thrive in any market environment. Genentech was founded in 1976, at the height of the stagflation era of the 1970s. At that time, there was no biotechnology financing market—nor even a biotechnology industry. If you wanted to grow stronger under such circumstances, there was no better strategy than that employed by Genentech.