Over 200 Million Patients but Market Size Still Below $15 Billion: Why Has the Hearing Health Sector—Backed by Tencent and Xiaomi—Yet to Take Off?

In recent years, both the dental and ophthalmology sectors have emerged as hot tracks fiercely contested by capital market investors. According to incomplete statistics from the VCBeat Orange Database, there have been over 100 financing deals completed in each of these fields over the past three years, with multiple companies currently preparing for initial public offerings (IPOs).ButThe hotter these two sectors become, the more they highlight the decline of their “peer”—the hearing sector.。

So, just how bleak is the hearing health sector? VCBeat has uncovered some key data.

First, let us examine the market size.In 2021, the market size of hearing aids in China was RMB 6.112 billion., while the market sizes of ophthalmology and dentistry, both belonging to the consumer healthcare sector, have long surpassed the RMB 100 billion mark; additionally, in the primary market, according to publicly available data compiled byOver the past three years, only nine financing deals have occurred in the hearing sector., which is vastly different from the hundreds of financing rounds seen in the dental and ophthalmology sectors over the past three years. Finally, focusing on publicly listed companies, annual reports show that Jinhao Medical, as the first listed company in China’s hearing care sector, recorded a revenue of RMB 195 million in 2022, whereas Aier Eye Hospital Group reported a revenue of RMB 16.11 billion, and Topchoice Medical reported a revenue of RMB 2.719 billion in the same year, indicating a significant overall disparity.

But in fact, as “peers,”The mandatory requirements for the hearing sector are no less stringent than those for dentistry and ophthalmology.. Taking the patient population as an example, according to official data,Currently, 220 million people in China suffer from varying degrees of hearing loss., with the elderly population being the primary group; individuals aged 60 and above account for 55.31% of all patients with hearing impairment, and this figure is projected to rise further in the future as population aging intensifies.

Yet even so, the hearing care sector has not yet experienced a market boom comparable to that seen in ophthalmology and dentistry. What, then, are the underlying reasons?

Market Penetration Rate Stands at Only 5%: Where Exactly Is the Hearing Care Sector Bottlenecked?

Why does the market fervor in dentistry and ophthalmology lead to associations with the hearing care sector? This is primarily because the three fields share numerous similarities. For instance, their core products are predominantly medical devices; their market models are largely consistent; and they all benefit from a substantial patient base. Furthermore, they all operate within the broader macroeconomic trend of transitioning from overseas monopoly to domestic substitution.

Yet it is precisely for this reason that, in stark contrast to the dental and ophthalmology sectors, the industry continues to raise questions:Why Has the Hearing Sector Failed to Emerge?

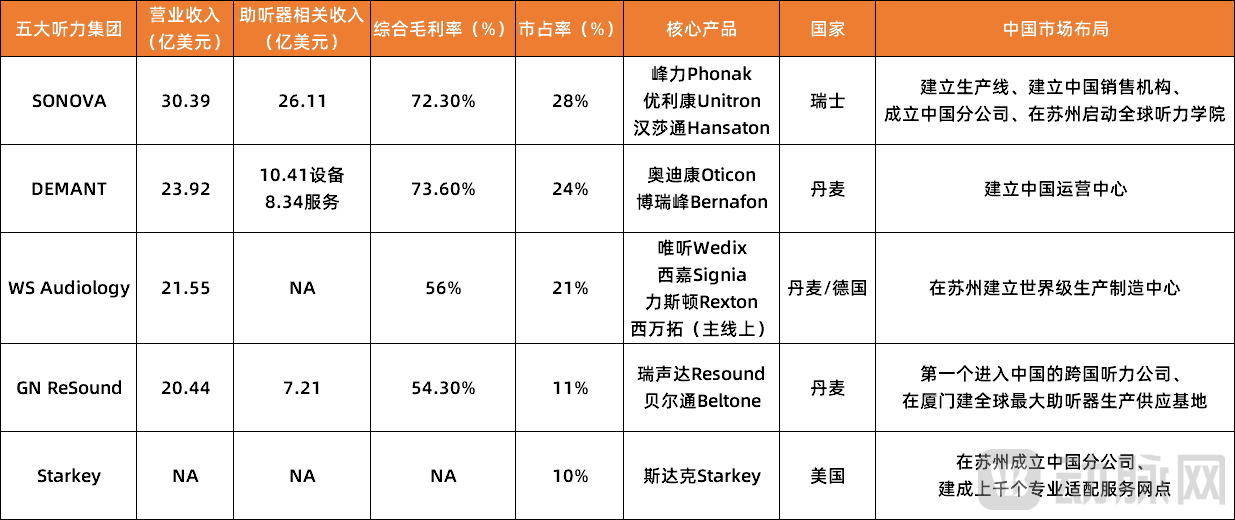

Before analyzing the root causes, let us first examine the industry background of the hearing care sector. Although the hearing industry is still in its early stages of development in China, it has long been a mature industry abroad, where five major manufacturers have already emerged, namelySonova、Demant、GN ReSound、WS AudiologyandStarkey, according to the data,The top five manufacturers currently account for approximately 95% of the global hearing aid market share.. Additionally, in terms of market penetration rate, according to the latest data, the hearing aid penetration rates in the UK and France have both exceeded 40%, while that in the US is approximately 27%.while China has only about 5%。

Figure 1. Revenue and Product Overview of the Top Five Manufacturers in 2022 (Source: Corporate Annual Reports)

Figure 1. Revenue and Product Overview of the Top Five Manufacturers in 2022 (Source: Corporate Annual Reports)

In line with this overarching trend, the reasons for the current stagnation of the hearing care sector in China have become largely clear.The first issue that comes to light is the weak competitiveness in core technologies, leaving domestic players vulnerable to being “strangled” by overseas giants.。

Hearing assistive devices are categorized based on the degree of hearing loss.Hearing Aid Fitting, Middle Ear Implants, and Cochlear ImplantsAmong the three approaches, hearing aid fitting—primarily targeting patients with mild-to-moderate hearing loss—is more favored by the market due to the larger patient population. Consequently, companies focusing on this segment have concentrated their core product pipelines in the hearing aid sector.

ButThe core technologies of hearing aids are primarily chips and algorithms., with the chip serving as the brain of the hearing aid, directly determining its amplification performance, sound quality, noise reduction capabilities, and ability to adjust and process sounds in complex environments. However, whether in the industrial or medical sector, chips remain a “chokepoint” technology in China; consequently, many domestic hearing aid manufacturers still rely on imported chips. The publicly listed company Jinhao Medical also acknowledged in its annual report that,The performance of the company’s in-house developed hearing aid chips currently reaches the level of mid-to-low-end imported chips, but there is still a certain gap compared to high-end imported chips.

The same holds true for algorithms. Although the market environment is relatively more favorable compared to that of chips, latecomers will inevitably face significant challenges in breaking through the dense patent web woven by the five major manufacturers. Furthermore, there are varying degrees of differences in manufacturing processes and the internal structure of components.

Beyond technology, the second major obstacle hindering the development of the hearing care sector is insufficient market education.. As a healthcare sector with strong consumer attributes, achieving scalable growth inevitably requires substantial investment in market education; however, the hearing care sector currently lacks certain key elements for market expansion.

First, the key consumer groups in the industry were not identified, nor were customer segments precisely differentiated using products at varying tiers.. A professional investor focused on the consumer healthcare sector stated in an interview with VCBeat, “Because the industry’s understanding of the hearing care sector is still insufficient, thereforeThe entire market is currently still in a phase of unregulated, wild growth, and the vast majority of companies have yet to clearly define their target customers for their products.", this is actually a major issue."

The second point is insufficient product strength.. A senior industry practitioner told VCBeat, “To date, there is no hearing product on the market that has gained widespread recognition, which means that corporate brands have not yet established a strong presence. Additionally,”At this stage, there is no product that offers exceptional value for money., the entire industry is exhibiting a polarized trend. Low-end products are inexpensive but perform poorly, potentially even damaging patients' residual hearing; whereas high-end products are costly, typically priced above RMB 10,000, and generally require replacement every 3–5 years, which to some extent dampens consumers' willingness to purchase.

The third point is that the service fails to keep pace.. Slightly different from ophthalmology and stomatology,Hearing products, represented by hearing aids, are actually composed of “30%” product and “70%” service., but as it stands, there is still a significant gap in the service segment of the industry. This is reflected in multiple aspects, such as the number of offline stores; according to statistics,China currently has approximately 10,000 hearing aid dispensing stores, yet they must serve a patient population exceeding 200 million., In addition, the infrastructure of these stores is not yet fully developed, and there is a relative shortage of qualified professionals. Furthermore, as these stores are primarily located in first- and second-tier cities, thereforeAccessibility and satisfaction with hearing product services have consistently remained low.。

Fourth, market channels have yet to establish sound mechanisms, and no industry leader has emerged.. In fact, the emergence of Aier Eye Hospital has, to some extent, spurred the development of the entire ophthalmology industry. However, in the hearing care sector, no such benchmark enterprise has yet emerged. As a result, a standardized market promotion mechanism has not been established, which is precisely why the market circulation costs in the hearing care sector remain exceptionally high, according to industry insiders.70% of the costs in the hearing aid industry are tied up in the distribution channel.。

Overall, from a technical perspective, core control over chips, algorithms, manufacturing processes, and component construction remains largely in the hands of overseas giants. Meanwhile, at the market level, the lack of mature distribution channels, coupled with varying degrees of deficiencies in infrastructure and personnel, has led to insufficient awareness of the hearing care sector in the domestic market, resulting in patients not attaching sufficient importance to it.Many individuals with hearing loss believe that hearing decline is a natural part of aging, thereby missing the optimal intervention window for hearing aids.Therefore, it is not difficult to explain why the hearing care industry currently exhibits low market penetration, a small market size, and lukewarm growth.

Tencent and Xiaomi Enter the Fray, Multiple Investors Double Down: Is the Hearing Care Sector a Lucrative Business?

It is an undisputed fact that the hearing care sector remains relatively “small” at present, yet this very characteristic presents a significant opportunity. Beneath the vast market potential, the industry may be on the verge of a turning point. Precisely for this reason, professionals eager to explore new avenues within the healthcare field have increasingly turned their attention to the comparatively niche area of hearing health over the past one to two years.

In May 2022, leveraging its expertise in artificial intelligence voice technology,iFLYTEKLaunched the iFlytek Smart Hearing Aid; in September 2022,Tencent Tianlai LabLaunched its first fully self-developed core algorithm solution for hearing aids, in collaboration with hearing aid manufacturersZhiTing TechJointly developed and launched the ZhiTing (Tencent Tianlai Inside) hearing aid, "Public Welfare Edition for the Elderly."

Figure 2. Financing in China’s Hearing Sector Over the Past Three Years (Data source: VCBeat Orange Database)

Figure 2. Financing in China’s Hearing Sector Over the Past Three Years (Data source: VCBeat Orange Database)

In addition to large enterprises directly entering the fray, startups in the hearing care sector have also gained recognition from the capital market one after another over the past year or two.BOIN Hearing, HEARIN.AI, Xiaowei Health, Aikesheng Hearing Aids, Jiuyi Medicalhave all completed financing, and a significant number of startups in the hearing sector are also currently engaging with investors.

Does this mean that the hearing sector will gradually gain momentum?

In the view of many interviewees,This is an inevitable trend that follows the current momentum.First, in terms of market size, China has a considerable elderly population, and according to data from the “2022 White Paper on Hearing Health for Ear Care Day,”At least 30% of adults aged 65 and older have hearing loss.. Looking further ahead, population aging will drive a rapid increase in the elderly population; meanwhile, individuals born in the 1960s and 1970s will soon become the core elderly demographic, possessing strong purchasing power and a greater willingness to try new things.

Secondly, at the technical level, with more leading enterprises and capital successively investing, and driven by emerging technologies such as digitalization and artificial intelligence, the hearing sector is gradually overcoming critical technological bottlenecks. For example, in terms of algorithms,BOIN Hearingas an example, it has developedSpeech Enhancement Algorithm, this algorithm is scientifically designed based on composite factors such as speech signals and auditory characteristics. It compensates for patients' hearing loss by modifying articulation patterns, thereby making speech easier to understand.

Additionally,The Intervention of Digital Technology May Usher in a New Development Revolution for the Hearing Aid Industry. For instance, in terms of fitting methods, many companies have adopted online digital technologies, primarily using apps as platforms, to disrupt traditional offline fitting practices and make the process smarter and more convenient. Furthermore, the application of digital technology has significantly enhanced the compensatory performance and controllability of hearing aids, while also endowing these devices with features such as low noise, low distortion, energy efficiency, miniaturization, and high adjustability.

In addition to market size and technological innovation, the hearing sector also benefits from policy support and the momentum of domestic substitution at the market level.In 2022, the State Council issued the “14th Five-Year” National Health Plan, incorporating ear and hearing health initiatives into the Outline of the Healthy China 2030 Planning. Additionally, the hearing sector, dominated by device products, will accelerate the pace of domestic substitution in the future, providing more growth opportunities for Chinese brands.

Finally, it also holds significant advantages in supply chain, production costs, and market channels. Taking market channels as an example, the online channel for hearing aids has seen substantial growth in recent years. It is reported that up to 2 million consumers have purchased hearing aid-related devices online, accounting for approximately 25% of the market share, with a trend of continued expansion in the future. As a specific case, on January 6, 2022, ZhiTing’s brand—ZhiTing 32-Channel Smart Hearing Aid—surpassed 1 million units in sales on its first day of crowdfunding launch on Xiaomi Youpin.

It is precisely for this reason thatMajor Foreign Hearing Aid Giants Have Recently Intensified Their Efforts to Expand Offline Retail Presence in China, in fact, it has set its sights on the inflection point marking the launch of China’s hearing care market—a lucrative opportunity.

"Left or Right: Who Will Break Through?"

August 2022,The FDA Announces the Establishment of a New OTC Hearing Aid Category, Allowing for a New Class of Hearing Aids to Be Sold Without a Doctor’s Prescription, It is reported that the bill officially came into effect on October 17, 2022.

Under this new regulation, hearing aid-related technologies are continuously innovating, while new channel service models are rapidly being established, subtly reshaping the market landscape for hearing aids.: On one side are OTC products primarily targeted at patients with mild-to-moderate hearing loss, it primarily relies on online sales and is also a key direction for breakthroughs by many leading enterprises and startups;On the other side are medical-grade hearing aids designed for individuals with severe hearing impairment., with a primary focus on offline channels, driven mainly by traditional industry giants and some startups.

So, which market path is ultimately better? Should the future direction be to the left or to the right?

During this interview, both investors and seasoned industry practitioners unanimously agreed that both pathways hold market value. There is no distinction of superiority or inferiority between them, nor is there any basis for claiming that one will emerge as the clear leader ahead of the other. In fact, the two are more likely to maintain a complementary relationship in the future.

Specifically, OTC hearing aids are designed for individuals with mild-to-moderate hearing loss, thus requiring less advanced technology compared to medical-grade hearing aids; furthermore, they rely primarily on online sales.Therefore, it would be more akin to an “electronic product.”Therefore, its products enjoy greater market accessibility and a relatively larger market size. According to industry insiders, the market size of China's OTC hearing aid market is estimated to be in the range of hundreds of billions of yuan.

In addition, unlike medical-grade hearing aids, which are dominated by overseas giants, OTC hearing aids are a relatively new category where all players are still in the early stages, presenting future opportunities for all.

Medical-grade hearing aids, designed for patients with severe hearing impairment, demand higher performance in core technologies such as chips and algorithms. In this regard, as previously mentioned, China is gradually breaking through this technological bottleneck and has already achieved some results. Additionally,Since OTC hearing aids and medical-grade hearing aids have a predecessor-successor relationship, the rapid development of OTC hearing aids will, to some extent, cultivate a large user base for medical-grade hearing aids., which will also enable the market size to soon exceed RMB 10 billion.

Furthermore, as the substitution of imported products with domestically produced ones gradually advances, experts predict that within the next 3–5 years, at least two to three leading overseas companies will sequentially exit the Chinese market. This will create a certain volume of market growth space in the medical-grade hearing aid sector for more domestic enterprises.

Therefore, from an overall perspective,The two market development paths essentially involve using products with varying levels of sophistication to precisely segment customer groups., which is a typical indication of the industry's healthy development.

Regardless of the path chosen, a critical factor for capturing a larger market share in China’s domestic market will be providing patients with comprehensive hearing solutions. This entails establishing hearing service centers that offer not only multi-dimensional product portfolios but also corresponding services, including speech rehabilitation, thereby achieving true vertical integration from production to sales and forming a closed-loop industry ecosystem.

From desktop-sized devices in the late 19th century to units weighing less than one gram by the end of the 20th century, and now to increasingly intelligent and personalized hearing products, although the industry has advanced relatively slowly, a technological inflection point on the supply side may be emerging amid steadily growing market demand.